Origin’s euro return a hit with investors for credit and ESG

Origin Energy (Origin) returned to the euro market for the first time since 2014, on 5 September, with a deal that highlighted European investors’ appetite for duration and for issuers with clearly articulated environmental, social and governance (ESG) strategies. Deal sources say the euros market remains highly globally competitive for corporate issuance.

Origin’s €600 million (US$661.7 million), 10-year deal was led by BNP Paribas, Citi and Goldman Sachs. The deal was marketed with the possibility of being executed in euros or sterling given both have been providing attractive options for price and tenor.

Peter Rice, Sydney-based general manager, capital markets at Origin, says the combination of strong euro demand and euro cross-currency swap levels made it the more attractive option of the two.

The issuer has a €1 billion hybrid which it plans to call in September and a €500 million senior maturity in October, for which this transaction was a partial refinancing.

Rice says the current period is the strongest he has seen the euro market, revealing that Origin’s 1 per cent coupon swapped back to Australian dollars with an interest rate of around 3.2 per cent.

Busy period

The deal came amid a busy execution period. Joe Hunt, executive director at Goldman Sachs in Sydney, says the European market has reopened after northern summer holidays earlier than is typical with supportive conditions since the final week of August.

“The market has had one eye on the European Central Bank meeting on 12 September with a strong consensus for a new QE programme to be delivered but with some variance as to the exact parameters. Issuers have therefore been eager to de-risk funding tasks early and avoid potential risk-off events,” says Hunt.

“September is always busy, but the primary market had a very active end to August and this carried on into the start of September,” Kate Stewart, managing director and head of debt capital markets, Australia at BNP Paribas in Sydney, tells KangaNews. “Investors have money to put to work and are keen to look at new issues ahead of potential risk factors.”

Ian Campbell, managing director and head of debt capital markets Australia and New Zealand at Citi in Sydney, says there was €7.3 billion worth of corporate issuance on the day that Origin came to market, adding to the success of the transaction was their ability to revise its pricing by 20 basis points from launch guidance to final pricing indicates how deep the euro market currently is, and their marketing effort was well received.

He says easing in geopolitical tensions on execution day, based on improving news on the protests in Hong Kong as well as indications the US and China would meet for further talks to try to settle the trade war, added to the positive market tone.

Hunt tells KangaNews that, with nine other corporate issuers on screens on the same day, it was important to have Origin in the market as the first to launch on the day. He reveals the deal was eventually 2.5 times oversubscribed, with very few bids dropping out as the price was revised by 20 basis points and volume upsized to €600 million from the launch volume of an expected €500 million.

“There is a significant desire for duration from European investors in order to achieve a yield pick-up and issuers can take advantage of this. Negative yielding shorter-dated issues are still being supported but we are seeing longer tenors outperform. Origin opted for 10-year tenor, which allowed it to achieve compelling pricing at levels at or inside tenor-adjusted comparable bonds,” says Hunt.

The market environment meant a swift turnaround between roadshow and execution for Origin. The issuer was ready with a refreshed EMTN programme shortly delivering its FY19 results on 22 August. It met investors in the UK and continental Europe on 2-4 September and was ready to execute on 5 September.

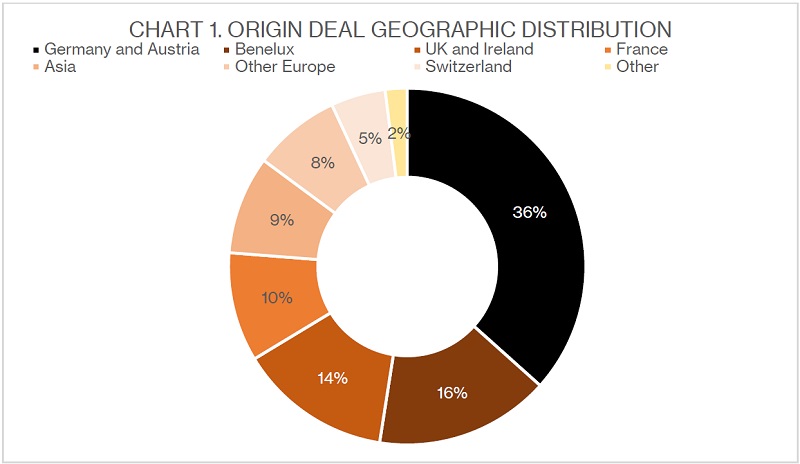

Deal statistics show the majority of demand came from continental Europe, with Germany in particular providing a significant bid (see chart 1). Asset managers and insurers were allocated the majority of the transaction (see chart 2).

Source: Goldman Sachs 12 September 2019

Source: Goldman Sachs 12 September 2019

Credit story

Stewart says euro pricing conditions remain as conducive to Australian dollar-based issuers as they were in the first half. Origin’s challenge was re-establishing its name in the euro market after a protracted absence, but Stewart tells KangaNews it dealt with this by delivering a very positive credit story and a clearly articulated ESG strategy at roadshow.

Given five years has elapsed since Origin’s last euro transaction, a degree of refamiliarisation was required with European investors. Campbell says: “The issuer’s credit has fundamentally changed since its last debt-capital markets transaction so a thorough marketing exercise was important. One component of this has been the issuer’s move from a project-funding style financing for Asia-Pacific LNG into it being an operating asset which spins off material cash.”

Rice tells KangaNews he was impressed with the level of knowledge investors had of Origin’s development, though a refresh was still necessary to explain corporate strategy around the new phase of the APLNG project as well as a deleveraging and simplification of corporate structure that Origin has implemented.

Rice says investors have responded well to Origin’s commitment to maintain its triple-B credit rating, having been upgraded by Moody’s Investors Service and S&P Global Ratings in April.

Given Origin’s absence from the market, Campbell says the deal group used names from the Australian regulated-utilities sector such as AusNet Services, Ausgrid Finance and APA Pipelines as comparables.

ESG attention

ESG was a significant talking point at roadshow, deal sources confirm. As an energy company based in a country heavily reliant on coal-fired power generation, environmental consideration could have been as an impediment to issuance. However, leads say Origin’s deal result demonstrates the value of a well-articulated plan for addressing sustainability and ESG concerns.

Hunt says: “We were conscious of the growing ESG focus and several investor meetings were focused on this topic. However, Origin’s sustainability initiatives, commitment to increasing renewables generation and exiting from coal were well received with little if any impact on investor participation.”

Origin has committed to exit coal-fired generation by 2032 and significantly to increase its capacity for renewable-energy generation. Rice says the company has a sound sustainability strategy and he was well prepared for in-depth discussions on its targets as well as how it intends to achieve and report on them.

“We had many conversations on the various aspects of our ESG reporting, as well as the possibility for Origin to issue green bonds in the future. This is something we will take into consideration,” says Rice.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Vicinity’s domestic print shows ongoing appetite for real estate

Vicinity Centres’ Australian dollar return provides another example of investor support for a wider range of corporate sectors – in this case, an oversubscribed book coming in for an issuer in the retail real estate sector as it seeks to move on from the pains of the pandemic. The issuer says domestic market conditions proved attractive for pricing and tenor.

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.