SSAs take GSS bonds to the next stage

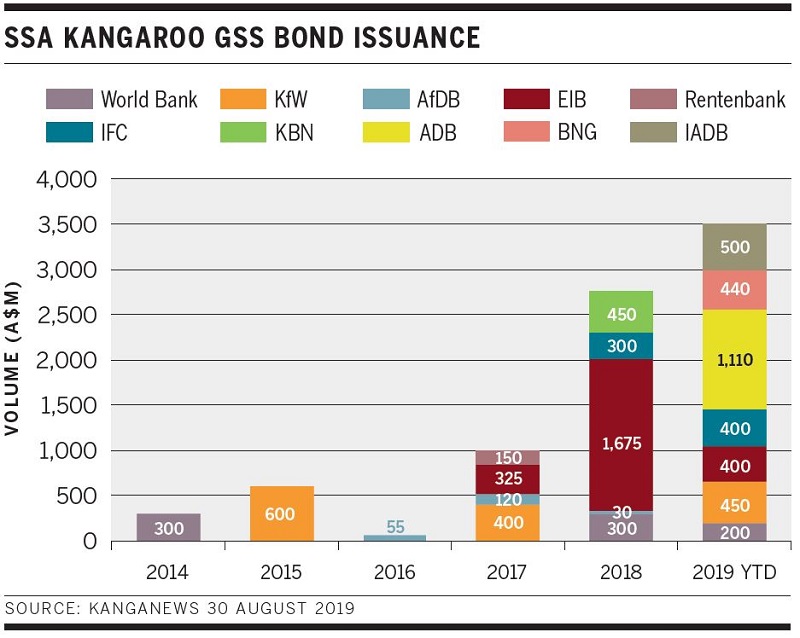

Supranational, sovereign and agency (SSA) issuers were among the global pioneers of the green, social and sustainability (GSS) bond market. As the sector prepares for its next quantum leap, some of the Kangaroo market’s most prominent GSS issuers (see chart) talk to KangaNews about their programmes and what comes next.

PROGRAMME EVOLUTION

Rich The GSS market has become more codified over the years through the adoption of various principles and standards, now including the EU taxonomy. How have your programmes evolved alongside these market developments?

This was by engaging with investors on the process of green-bond issuance and reporting, as well as being a founding member of the executive committee of the green-bond principles (GBP), coordinated by the International Capital Markets Association (ICMA). We initiated harmonised impact reporting and still contribute to the evolution of green-bond impact reporting.

A few milestones have already been reached along the way, providing guidance on issuance process, reporting and verification. These include the GBPs, the international financial-institution framework for green-bond impact reporting harmonisation and the EU green-bond standards (GBS).

The EU taxonomy is a crucial step forward and establishes an important reference for concrete cooperation among policymakers, project specialists, market practitioners and civil society grappling with the question of what should qualify as green or sustainable.

For the bank of the EU, this particular initiative is very relevant and a dedicated sustainability funding team has been created within European Investment Bank (EIB)’s capital-markets department to adapt our funding to these structural developments.

Having shaped the very first green bond in 2007, I am heading this team. It is directly responsible for issuance of climate-awareness bonds (CABs) and sustainability-awareness bonds (SABs) in all currencies, ensuring continuity as the framework evolves. Our first initiative has been to revise use-of-proceeds language to allow for the gradual alignment of CAB and SAB eligibility criteria with the EU taxonomy as it takes shape.

Kommunalbanken Norway (KBN) has been proactive, updating our original 2013 green-bond framework in June 2016 to meet the developing market standards.

We are also currently reviewing the framework in line with the release of the EU taxonomy. Our eligible-project categories have not changed dramatically over the years. But the eligibility criteria for each category have evolved in line with the technological frontiers.

In addition, our process for project evaluation and selection is more stringent. Also, of course, the focus on quality of impact reporting has increased.

Rich How has the process of developing the EU taxonomy and the report’s release informed the development of issuers’ green-bond programmes?

Being the bank of the EU, EIB intends to align its activities with the EU taxonomy as it evolves over time. This applies to loans and bonds. On the funding side, we have already reflected this in our CAB and SAB use-of-proceeds documentation.

We are now working closely with our project experts on the infrastructure needed to establish a reliable link between EIB’s sustainable lending and funding. Project-finance activities need to be mapped, selected, marked, allocated, monitored and reported to the capital-market audience according to their contribution to the sustainability objectives set by the EU.

A large part of public spending is nowadays already either social or sustainable – and this part will grow.

We aim for a smooth transition. In the first round, we will assess how well our current criteria match the criteria of the taxonomy and what is needed to make our framework ‘EU compliant’.

We have scheduled an update of our eligibility criteria and our green-bond framework for later this year, where clearly we will bear the current version of the taxonomy as well as the EU GBS in mind.

SSAs' global GSS programme updates and plans

Supranational, sovereign and agency (SSA) issuers’ green, social and sustainability (GSS) bond programmes are not static objects. Some of the market’s biggest players update KangaNews on global and issuer-level developments.

FAN Inter-American Development Bank (IADB) has a social-bond programme called EYE – for education, youth and employment – which had US$1.5 billion outstanding as of July 2019.

The EYE-bond programme focuses on the lifecycle approach to building human capital from early childhood care and education through formal primary and secondary education, as well as programmes that facilitate labour-market placement by improving the transition from school to work through vocational training.

Rich Do you expect the EU taxonomy to provide the basis for a common global language for green bonds?

We believe comparability in GSS finance may be achieved if the individual approaches to sustainability, while reflecting local challenges and priorities, are aligned in their classification structure or architecture – in other words, their core objectives, activities and technical screening parameters.

Different significance thresholds may still be adopted as technical-screening criteria in the context of different, though converging, paths. This is what we understand to be common language in green finance.

Rich Is the move towards a common language being driven more by issuers or investors?

What is changing, though, is that the TEG process initiated by the EC facilitated the opinions of NGOs, think tanks and regulators to be incorporated into the development of the green-bond market. This may add some complexity, as these actors do not necessarily have the same pragmatic approach as market actors do. This makes it even more important that issuers and investors join the conversation even if they are outside the relatively small TEG – as we are.

THE KANGAROO MARKET

Rich What have been the main developments in the Australian dollar market for GSS bonds?

GSS supply from supranationals has been complemented by issuance from state treasuries, domestic and international banks and corporates. This is providing more issuer diversity to the market.

The main development we have noticed is that investor focus and engagement in the sustainability space has really taken off. More and more Australian investors are now also looking at ESG factors as part of their overall investment strategies.

In addition to seeing some specific green-focused accounts in the book, the ticket sizes from many of our regular investors reflected a green focus. It is also worth noting that more than 60 per cent of this trade went to Australian investors. This domestic engagement was particularly pleasing to see.

The domestic bid appears stronger for CABs than our regular Kangaroos. Reflecting the same trend, GSS-focused interest out of Japan has also been key to our CAB placements, in particular in the longer end of the curve. Overall, our interaction with the investor base in Kangaroo GSS bonds has been very positive.

Green Capex is not enough

While green, social and sustainability (GSS)-labelled bonds are providing assurance to the market, capex projects alone are not enough for a two-degree world. Amy West, head of sustainable finance at TD Securities in New York, discusses market growth.

Supranational, sovereign and agency (SSA) issuers have been at the forefront of financing sustainability-linked technologies and projects since the start of the market, including being pioneering issuers of GSS bonds.

But if the committed two-degree limit above pre-industrial levels laid out in the Paris Agreement on Climate change is to be fulfilled markets will have to keep evolving to a broader approach towards environmental impact, West says.

IF AN ISSUER COMES TO MARKET WITH A GSS BOND, INVESTORS INTUITIVELY LOOK AT WHAT ELSE THE COMPANY HAS DONE IN THE ESG SPACE. IT IS NOT A SURPRISE THAT MANY OF THE WORLD’S LARGEST INVESTORS LOOK AT ESG BEYOND LABELLED GSS BONDS.

GSS EVOLUTION

Rich There is ongoing debate globally about whether labelled bonds are doing as much as can be done to redirect capital to fund the transition to a low-carbon economy. Do SSAs have a role to play in developing things like transition bonds in the same way as they have done with GSS bonds?

The report of the EC’s TEG has, for example, retained the principle that “transition activities” – those that contribute to a transition to the EU’s goal of a zero net-emissions economy in 2050 but are not yet operating at that level – are part of the transformation effort and therefore deserve to be mapped via GSS issuance.

Rich Do you think the market will evolve towards a more broad-based understanding of issuers’ environmental impact – perhaps in such a way that specifically labelled bond issuance is no longer required? Or will highlighting particular projects in the way GSS bonds do always have a value?

What we are working towards is broader transparency and increasing information and data so investors have better information for decision-making. With improved data and technology, investors can extend their focus on risk management to take climate and social risks into account – or purposeful investing to include a wider range of investments.

Labels are helpful. But at the end of the day what matters is that sustainable activities are financed, not how bonds are labelled.

An important consideration is to understand the purpose of the institution and how that institution achieves its objectives. It could be sufficient for investors if an institution is transparent and publishes information on all its lending projects rather than just highlighting a select amount.

In future, investors could focus more on the issuer itself. If the issuer’s mission supports ESG and provides transparent reporting and evaluation for its lending projects, technically any bond from that issuer could be considered as fulfilling the socially-responsible-investment requirement.

For EIB, GSS bonds have to provide a clear and easily understandable link between finance and the real economy – sustainable funding and sustainable lending. The impact reporting associated with green bonds – requiring the collection of reliable and comparable information on projects’ contribution to core sustainability objectives – is a crucial component of accountability for the use of funds. A realistic and constructive dialogue with capital markets can develop on this basis, providing a powerful incentive for strategic change.

This has occurred as issuers are looking at how to develop their asset bases and, at the same time, as the focus on general ESG principles has increased in the market. Also, issuers increasingly see the need to relate their GSS frameworks to their broader strategies on sustainability and climate risks.

The value of labelled issuance and the ability of investors to measure the impact of their investments and to compare supply from different issuers will continue to be an important factor in future. I believe the move towards this holistic view, and perhaps a situation where labelled issuance is no longer required, is some time off.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news