Australia holds steady with GSS to the fore

KangaNews conducted its annual survey of supranational, sovereign and agency (SSA) issuers’ funding outlooks in August 2019. The 30 responses forecast a return to core-market focus in the year ahead. The Australian market’s role seems mature, with the main growth expectation for Kangaroo issuance being in the green, social and sustainability (GSS) bond space.

Laurence Davison Head of Content and Editor KANGANEWS

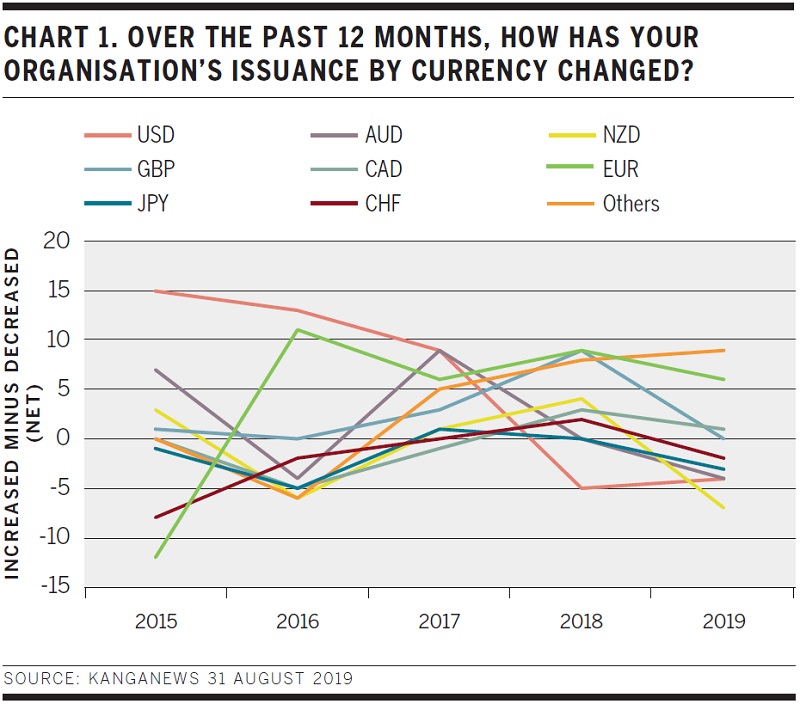

SSA issuers report that they spread the funding net relatively wide in the 12 months leading up to the latest KangaNews survey. For the first time since the survey’s inauguration in 2015, the most commonly reported increase in funding markets accessed is the “other” group (see chart 1).

More borrowers also report a greater use of euro funding than a smaller one. But two other global core markets – US dollars and yen – had net-negative incremental use. The Antipodean currencies suffered in the past year, with the Kauri market in particular proving a hard task for SSAs. Eleven issuers report a smaller proportion of New Zealand dollars in their funding mix compared with just four saying they used the currency more.

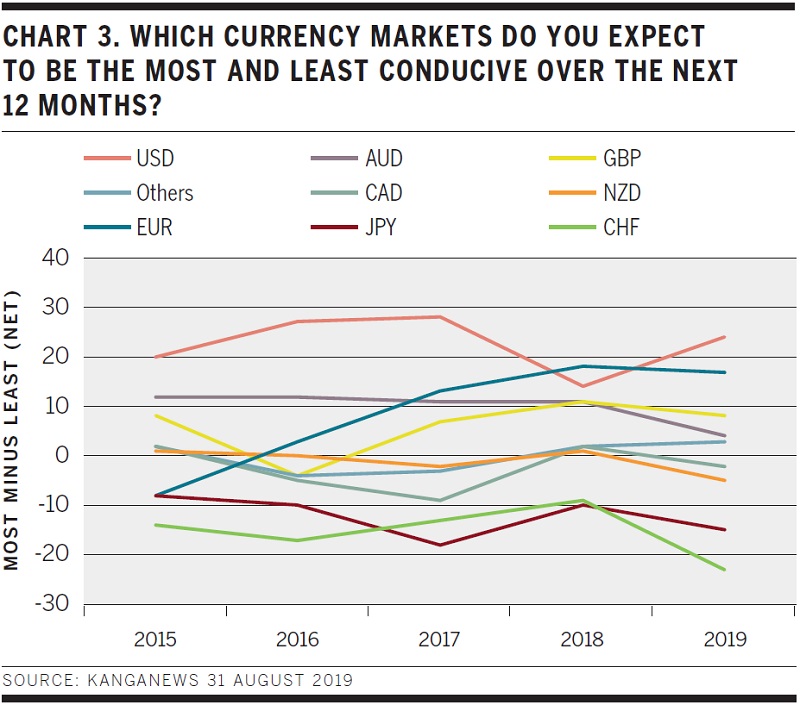

Funding strategies appear to be diverging, at least when it comes to currency selection. The KangaNews survey has its highest-ever proportion of issuers indicating the use of more than 10 currency markets in the past 12 months, but also a record proportion of borrowers limiting their issuance to fewer than three currencies (see chart 2).

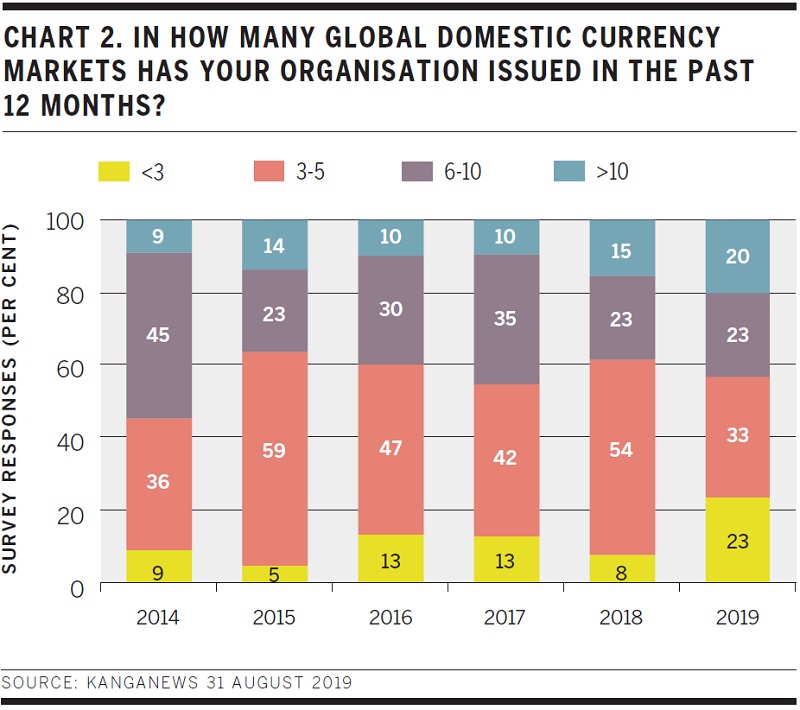

Looking ahead, SSAs expect the next 12 months to feature a return to core-market reliance. The overwhelming majority of survey respondents forecast US dollars to be among the most conducive in the year ahead with euros not far behind (see chart 3). The sterling and Australian dollar markets are also in net-positive territory.

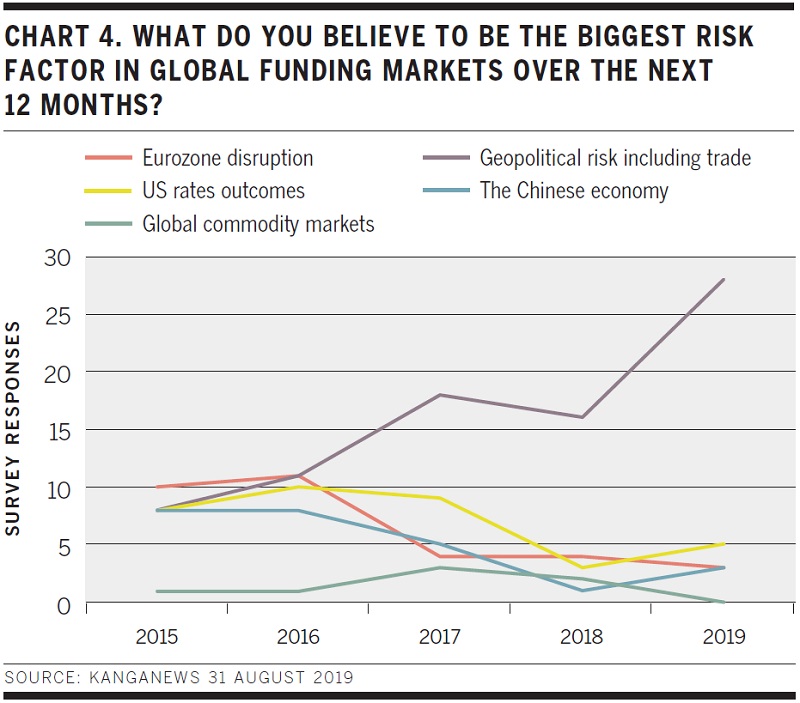

The survey gives one clear indication of why – other than mean reversion – SSAs seem to expect to be funding a greater proportion of their tasks in core markets in the coming months. Geopolitical risk has been a concern for global high-grade issuers for some years. However, in 2019 it is named by virtually every survey respondent as the leading risk factor for the year ahead (see chart 4). Borrowers are perhaps forecasting a coming flight to certainty in market selection.

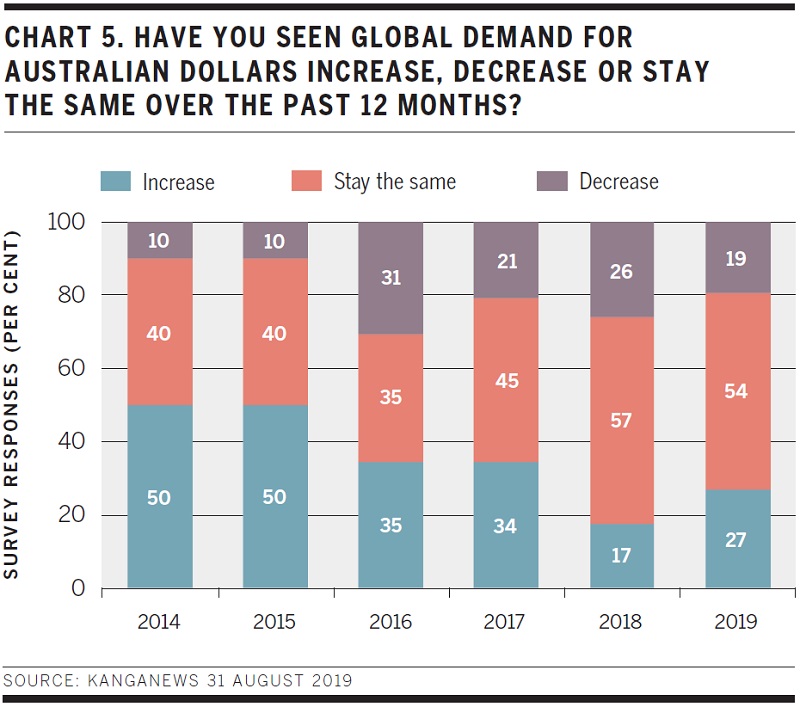

The Australian dollar appears to be playing a relatively mature role in SSAs’ funding portfolios. Its position has held up well despite a falling cash rate and yield relativity as more than 80 per cent of survey respondents say demand for Australian dollars has stayed the same or even increased in the past 12 months (see chart 5).

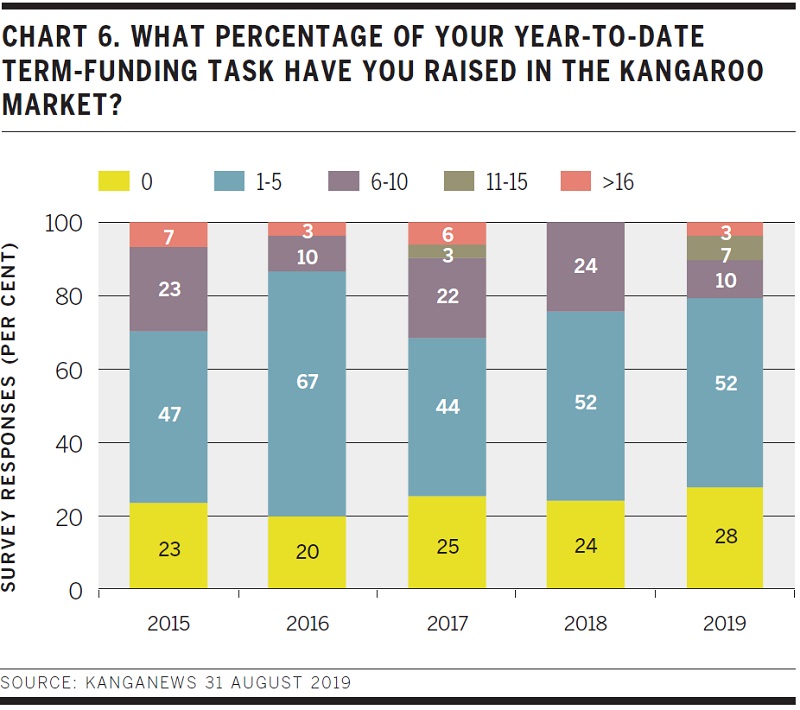

Kangaroo bonds tend to provide a consistent but small component of SSAs’ funding tasks. A large majority of those that have accessed the market in recent months report that it provides up to 5 per cent of their total funding – a figure that has remained relatively consistent over the years (see chart 6).

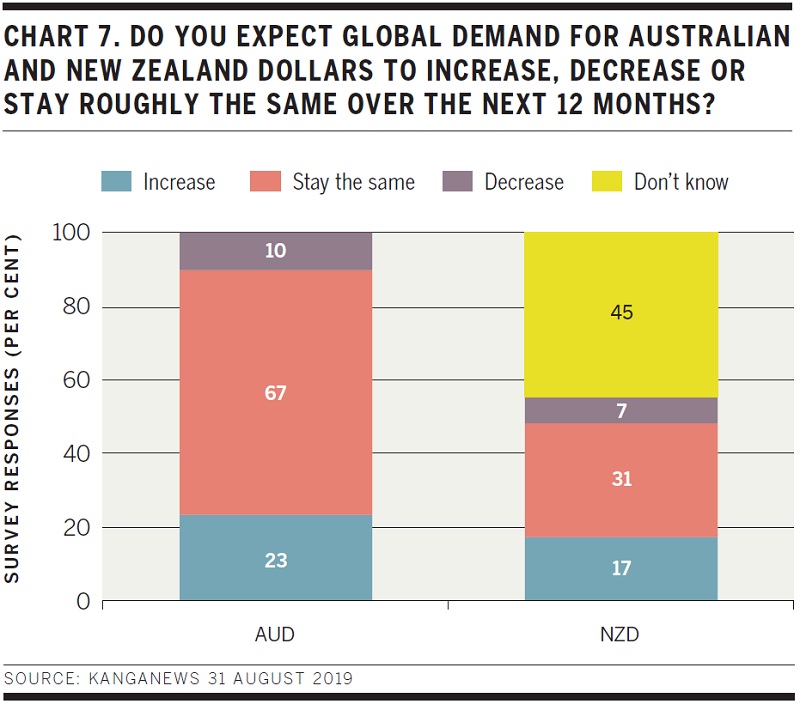

Nevertheless, issuers do not expect the Kangaroo market’s role to diminish despite an eroding Australian dollar rates advantage. Nearly a quarter of survey respondents expect greater demand for Australian dollars in the year ahead and just 10 per cent expect demand to fall (see chart 7).

Borrowers’ outlook for New Zealand dollar demand is also weighted towards the positive, though nearly half the issuers that responded to the KangaNews survey are not close enough to the Kauri market to take a view.

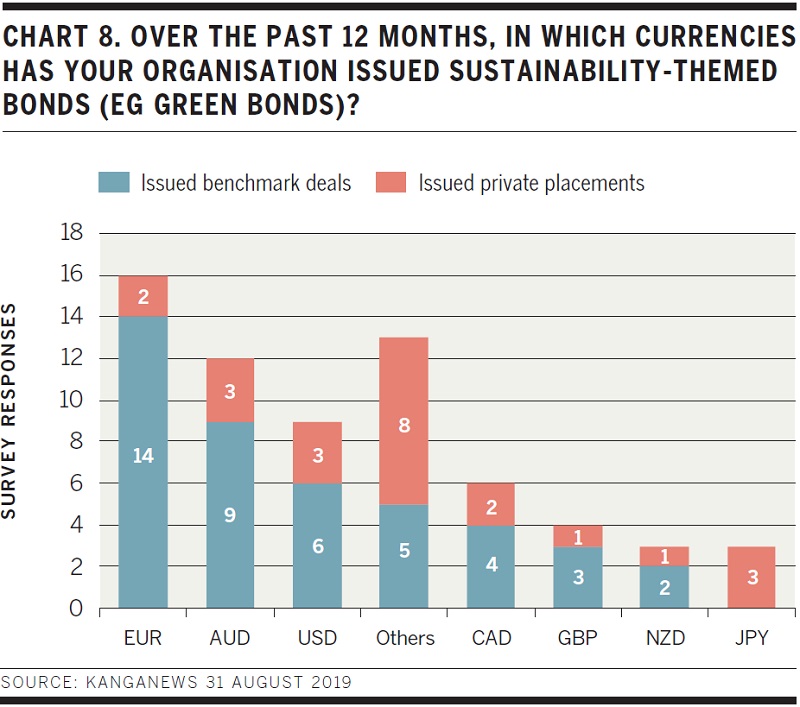

The area where the Australian dollar market clearly scores is for the issuance of GSS bonds. The KangaNews survey is naturally weighted towards issuers that are engaged with the Kangaroo and Kauri markets. Nonetheless, the fact that more issuers report the placement of sustainability-themed issuance in Australian dollars even than US dollars in the past year (see chart 8) is a clear testament to the development of the sector in Australia, and to SSA issuers’ leadership within it.

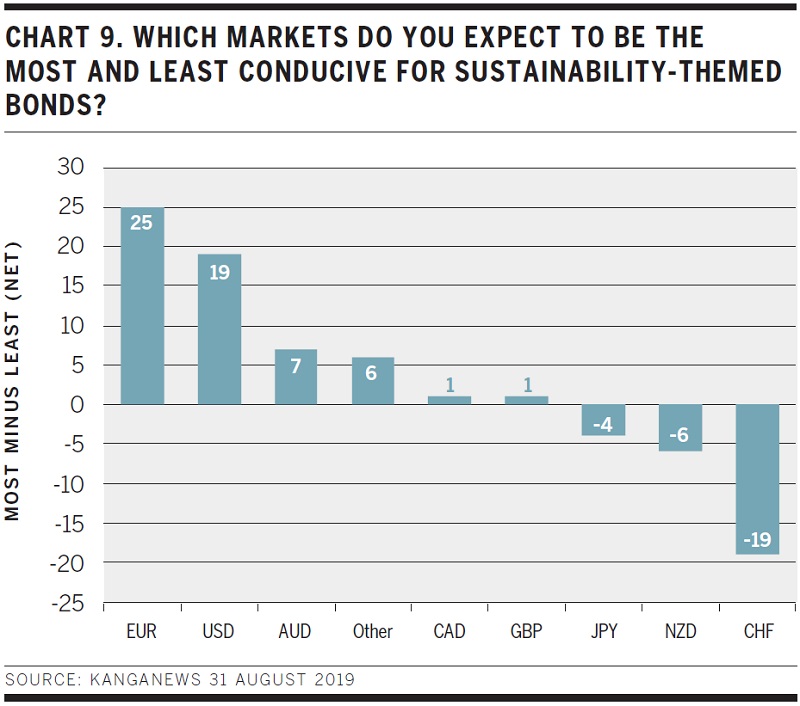

Perhaps unsurprisingly, SSA issuers expect the US dollar market will rise to compete with the global leader – euros – for GSS issuance. But Australian dollars still receive a clear net-positive response when it comes to which markets will be most conducive for GSS issuance (see chart 9).

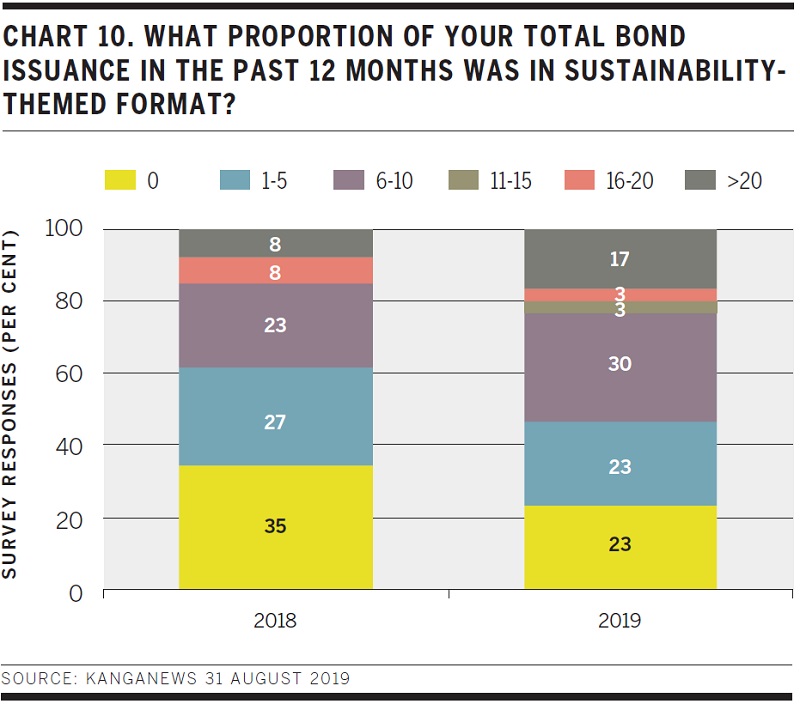

Use of GSS bonds is also growing within the SSA sector. More than half the 2019 survey respondents report printing more than 6 per cent of their issuance in some kind of sustainability format – compared with just over a third in 2018. Meanwhile, nearly 20 per cent of issuers say GSS issuance formed more than a fifth of their total in the past 12 months (see chart 10).

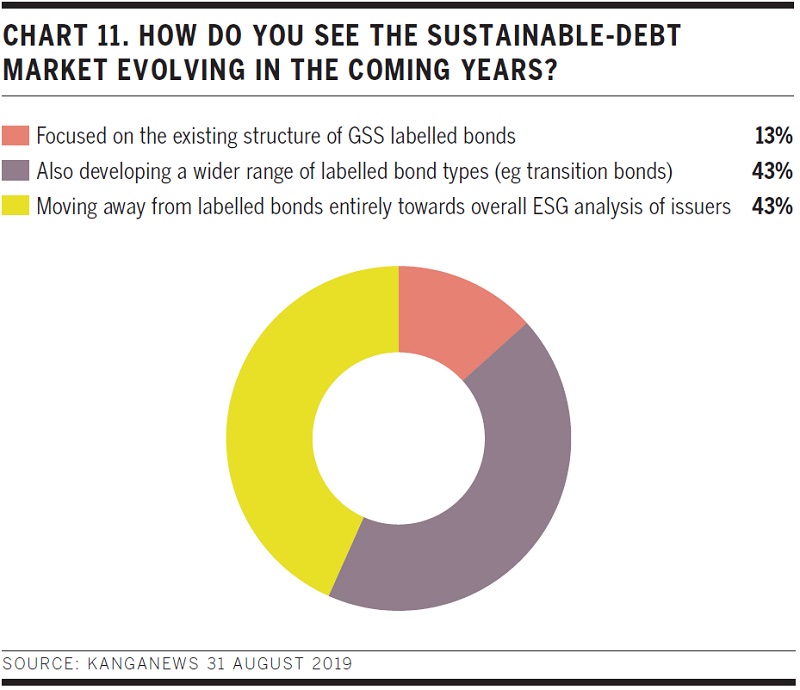

At the same time, issuers do not expect the sustainable debt market to stand still. Only a minority believe GSS bonds will remain the focus of the market. Opinions are divided on whether evolution will be towards a wider range of themed bonds or away from labelling issuance entirely in favour of a broader understanding of issuer-level credentials (see chart 11).

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

Quantum leap for Canadian provinces as Québec smashes Kangaroo record

Investor diversity, relative value and the growing status of the Australian dollar market lined up for Province of Québec as it shattered the record volume for a Canadian province Kangaroo transaction. The A$1.35 billion, 10-year print was nearly four times larger than any previous deal from the sector – a record that had stood for a decade.