Back to the future

Benchmark mid-curve issuance has re-emerged as the tenor of choice in the Kangaroo supranational, sovereign and agency (SSA) market in 2019. Technical factors are driving supply and demand in Australian dollars, and while domestic investors are having a harder time seeing value, global volatility is augmenting Antipodean markets’ appeal for offshore borrowers.

Matt Zaunmayr Senior Staff Writer KANGANEWS

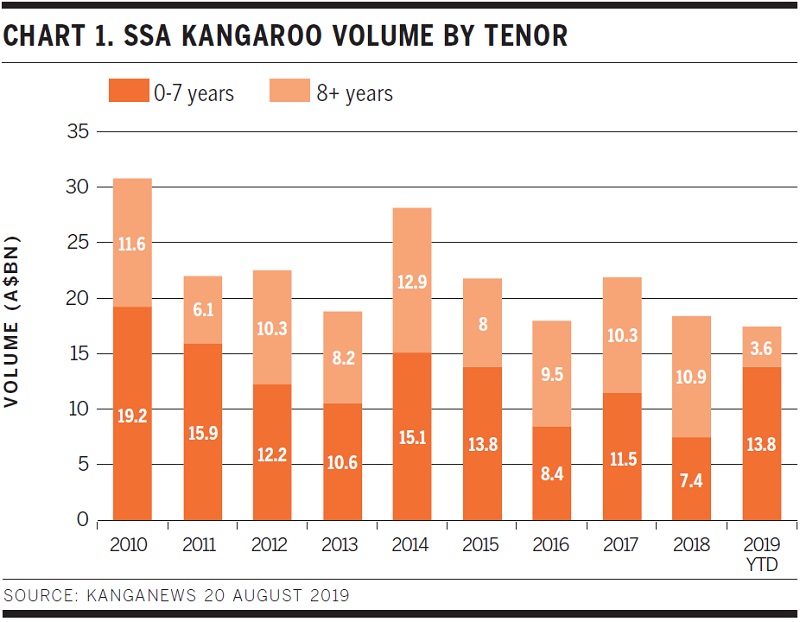

Supply of SSA deals with 0-7 year tenor in Australian dollars in 2019 is already approaching double the total volume for 2018 and is primed to challenge a decade-high for volume set in 2010. Meanwhile, volume at the longer end of the curve is well below the run rate set over the last 10 years (see chart 1).

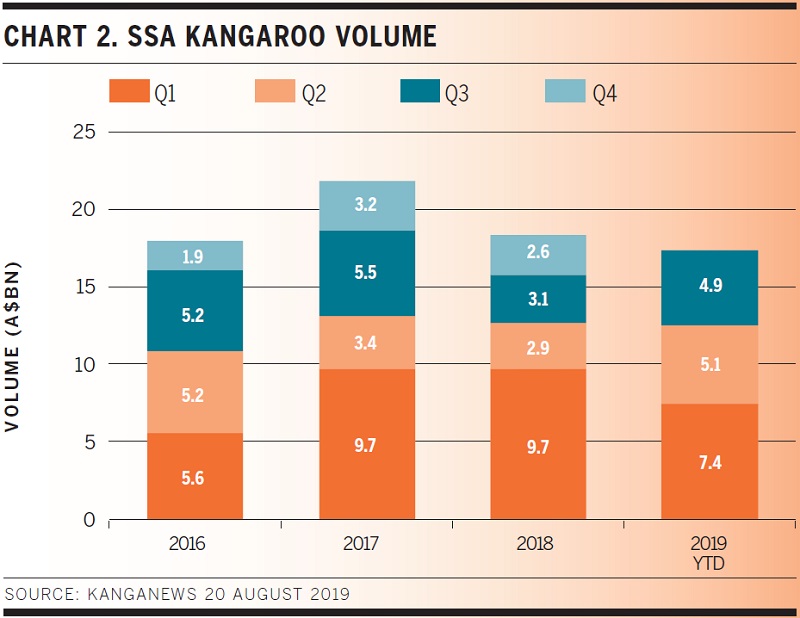

Supply from the sector in 2019 started in typical fashion, with a flood of issuers pricing deals in Q1. However, the market fell out of favour towards the end of March. According to KangaNews data, between early March and mid-May there were no benchmark SSA Kangaroos at any tenor. At the same time, SSA supply to the Kauri market – which had a near-record year in 2018 – was suppressed (see box).

However, Kangaroo supply picked up again between mid-May and mid-August (see chart 2), with the majority of benchmark deals being at five-year tenor.

Benchmark deals have come from issuers which have consistently maintained a mid-curve presence in Australian dollars such as Asian Development Bank (ADB), European Investment Bank, Inter-American Development Bank, International Finance Corporation (IFC), KfW Bankengruppe (KfW) and World Bank.

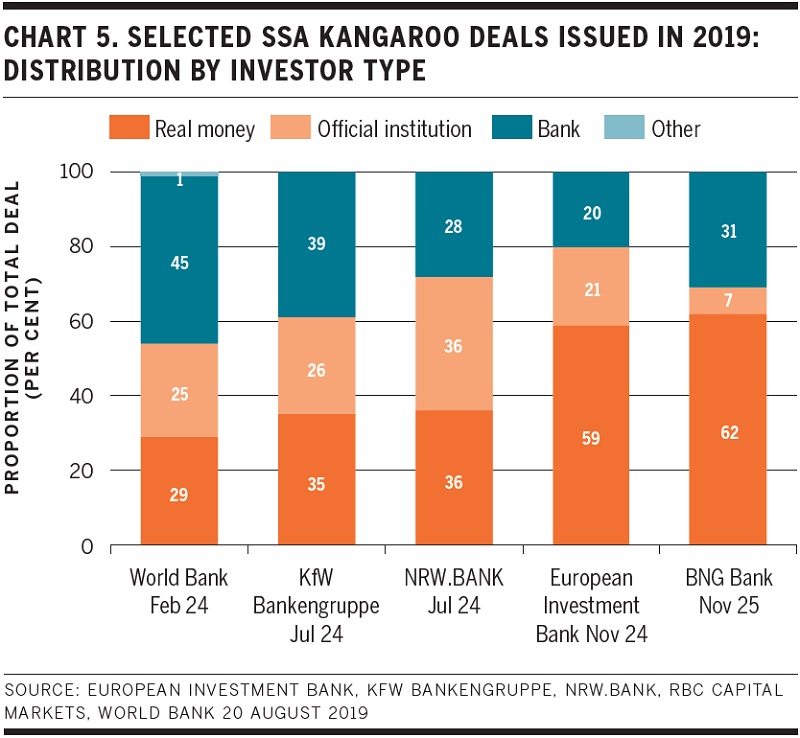

Deals have also come from those less active in Kangaroo mid-curve issuance. BNG Bank priced its first mid-curve deal since 2014 with a A$300 million (US$201 million), long six-year sustainability bond on 29 May. NRW.BANK printed a A$450 million, five-year deal on 19 July – its first Australian dollar deal in the belly of the curve since before the financial crisis.

Technical drivers

The resurgence of mid-curve SSA Kangaroo issuance has been part of a risk-on tone in the Australian dollar and global markets, induced by dovish positioning from central banks. The Reserve Bank of Australia (RBA) cut the cash rate in June and July, and market participants expect more to come before the end of the year.

Meanwhile, the Reserve Bank of New Zealand (RBNZ) decided on a 50-basis-point cash-rate cut at its August meeting. Yuriy Popovych, director, international fixed income at TD Securities in Singapore, says this move may reinforce market expectations that the RBA will cut its cash rate again sooner rather than later as central banks globally look to give their currencies an advantage.

The RBA’s dovish outlook caused a significant rally in Australian dollar government-bond spreads during June and July – increasing the relative value of the SSA sector. “SSAs broadly have been offering a good pick-up to government bonds in a low-rate environment, which has been particularly attractive for investors in Asia,” says Popovych.

Petar Bogdanovic, Brisbane-based portfolio manager and Australian fixed-interest strategist at QIC, confirms that with Australian government bond yields below 1 per cent out to 12 years’ maturity the SSA sector has become increasingly attractive. He says QIC is aware of increasing engagement from its domestic peers with SSA names.

Spread to government bonds has been particularly important in demand levels for deals such as NRW.BANK’s, which priced at 52 basis points over semi-quarterly swap. According to Yieldbroker, on the day prior to NRW.BANK’s launch the April 2024 Australian Commonwealth government bond was marked at 10.6 basis points below semi-quarterly swap.

Tatjana Beuer, director, capital markets funding at NRW.BANK in Düsseldorf, told KangaNews after the deal priced: “Being a relatively new Kangaroo issuer with a lack of liquid outstanding lines we still have to pay some basis points in premium compared with our euro targets. This is worthwhile for us, however – and our aim is to match our euro or US dollar pricing in due course.”

SSA spreads in general became more attractive compared with semi-government bonds from late June into early August, giving a good pick-up for investors. However, according to Popovych this dynamic has deteriorated slightly since the beginning of August.

Nevertheless, issuance in Australian dollars remained attractive for SSAs into the middle of Q3. Spread movement in the five-year part of the curve is exemplified by new lines placed by ADB in January and August, which priced at 42 and 35 basis points over semi-quarterly swap, respectively.

Furthermore, Popovych says: “US dollar swap spreads have tightened, increasing the cost of US dollar issuance and making other markets comparatively more attractive.”

Large US dollar tier-two capital deals priced by National Australia Bank and Westpac Banking Corporation in the wake of the Australian Prudential Regulation Authority (APRA)’s total loss-absorbing capacity equivalent announcement in July further widened the Australian dollar basis swap for offshore issuers.

Local-market constraints in Australia mean that market users expect the major banks will need to raise most of the capital uplift in offshore markets such as euros and US dollars. Popovych says the recent supply in US dollars and the expectation of more to come in other markets has been sufficient to move basis spreads and has added further to the momentum in the Australian dollar market.

Given the majority of tier-two issuance is expected to come at the long end of the curve, in the long run this may be where the greatest benefit also comes for Kangaroo SSA supply. However, Popovych says in early September demand for Australian dollars from Japanese investors was not sufficient to stoke issuance, while the mid-curve gains ancillary benefit.

Demand sources

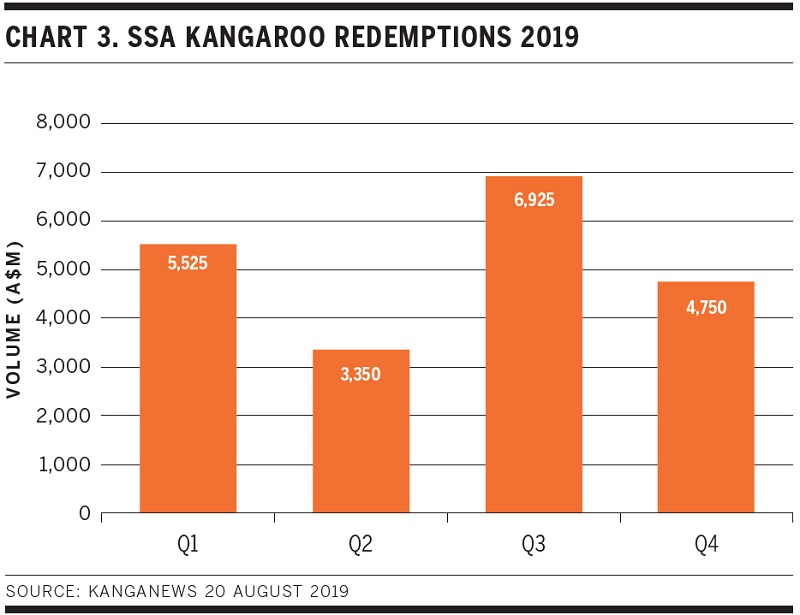

Other technical factors – such as Australian dollar redemptions for SSAs in Q3 being higher than at any other point during 2019 (see chart 3) and a cheapening Australian dollar – are also creating significant tailwinds for Australian dollar demand with various investor sets. Deal distribution statistics show that issuers are receiving demand from an array of different sources.

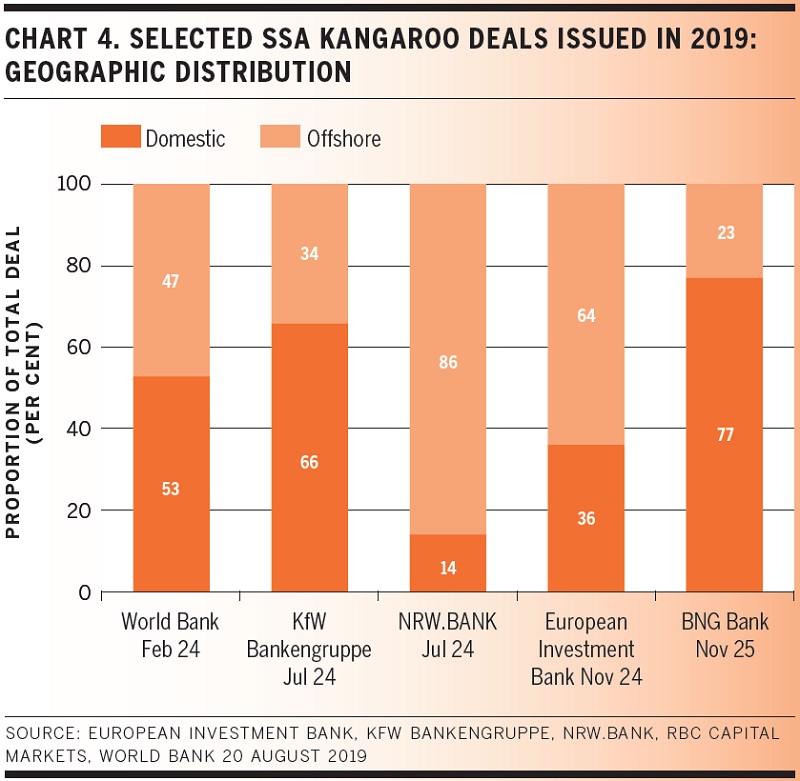

In the past, mid-curve SSA issuance has attracted the widest on- and offshore bid for the sector while the long end of the curve has been primarily the domain of Japanese and other offshore interest. The recent flurry of mid-curve SSA Kangaroos has also focused on domestic and offshore investors, although some of the transactions have been placed predominantly outside Australia (see chart 4).

Marayka Ward, senior credit manager and ESG champion at QIC in Brisbane, says despite the influx of issuance, SSA paper with 2024 maturity has been the least attractive point on the curve relative to semi-government bonds.

The addition of green, social or sustainability overlays has tended to augment Australian fund-manager demand for SSAs in recent years. This appears to be the case with regard to BNG Bank and KfW’s recent deals. NRW.BANK’s deal, on the other hand, had only a 14 per cent allocation to domestic investors – although Beuer told KangaNews at the time of pricing that some of these investors were new to the issuer.

Darren Langer, Sydney-based senior portfolio manager at Nikko Asset Management, comments: “For a manager like us with a composite mandate the SSA sector does not stack up, as pricing has not been attractive relative to other sectors in 2019 at any tenor.”

He continues: “The SSA sector is always a play relative to semi-government bonds. Recently, we have seen more reason for semi-government spreads to come in relative to government bonds compared with for SSAs, given we believed the banks will have more demand to buy semi-government paper into financial year-end to balance their high-quality liquid-asset requirements.”

In theory, the large forthcoming funding requirements for many of Australia’s semi-government borrowers could change relative-value dynamics in favour of SSAs. However, Ward says increased semi-government issuance has been well flagged and is thus priced in. For now, relatively low supply in the near term and a recalibration of the RBA’s committed-liquidity facility in June should stoke balance-sheet demand for semi-government paper.

Bogdanovic adds: “The uplift in semi-government borrowing requirements means these issuers are likely to extend their maturities. As a result, relative value for the long end of the SSA curve could benefit.”

According to Popovych, the pick-up offered by the SSA sector over government bonds has been more attractive for investors in Asia, with central banks and commercial banks particularly active in transactions. Deal statistics reflect this, as bank-balance-sheet and official-institution investors have played a large part in recent deals (see chart 5). Australian dollar demand from this investor set in 2019 has been resolute despite Australian dollar yields plummeting. Deal sources have told KangaNews that growing natural holdings of Australian dollars are coming to the fore with investors in Asia.

Kauri Developments

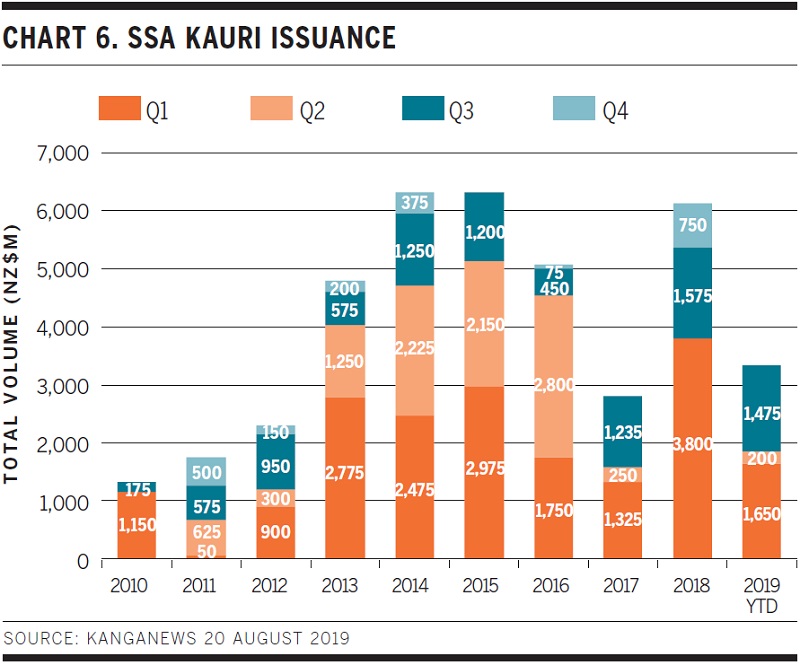

Kauri issuance from supranational, sovereign and agency (SSA) borrowers has lagged the long-run average so far in 2019 (see chart 6). Demand is evident but swap levels have not made issuance possible even for some of the market’s more consistent borrowers.

Given the Kauri is a noncore market for SSA borrowers, the weighting towards the front end of the year that is evident in the Kangaroo market tends to be less consistent. Deal flow comes if and when pricing makes sense. For most of 2019, it seems pricing has not been favourable for issuers.

Having said this, International Finance Corporation (IFC) printed a NZ$600 million (US$377.4 million), five-year deal in July – the market’s first deal since early April. At the time, senior financial officer at IFC in Washington, Marcin Bill, told KangaNews that the New Zealand dollar deal priced inside five-year US dollar levels on an asset-swapped basis.

With the US dollar curve pushing out, more opportunities may open in the Kauri space.

Shift permanence

How long supportive technical factors will remain in place to steer borrower and investor preferences towards mid-curve Kangaroo SSA issuance is difficult to ascertain.

Some factors – such as the effect of offshore major-bank tier-two issuance on cross-currency basis swaps and relative value to semi-government bonds – will play out over the medium and long term. Popovych says the expected tenor of offshore tier-two issuance from Australia’s major banks is also likely to provide more impetus for long-end Kangaroo deals from SSA borrowers going forward. However, investors from Japan which have supported this tenor in Australian dollars in recent years have become less involved in Australian dollar deals.

The back end of the year is often quieter for SSA supply, with the majority preferring to front-load issuance. However, in the current environment this does not necessarily mean Australian and New Zealand dollar (see box on this page) SSA issuance will be muted for the rest of the year. In fact, if pricing remains favourable there are reasons to foresee continued strong levels of supply.

“Given geopolitical instability currently and going forward, it is possible that some borrowers will look to undertake a significant amount of their funding sooner rather than later – and away from US dollars where the possibility of volatility is currently higher,” Popovych tells KangaNews.

During the volatility which hit global markets early in August, Australian dollar spreads in all asset classes followed the global trend wider albeit to a lesser extent than most other markets. This bodes well for attracting further issuance from offshore.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news