La Trobe Financial takes the plunge with greater volume

La Trobe Financial tested the waters for greater volume in its latest residential mortgage-backed securities (RMBS) deal. The issuer achieved its record deal size and says improving credit quality and structural tweaks designed to meet specific demand helped increase the transaction’s appeal.

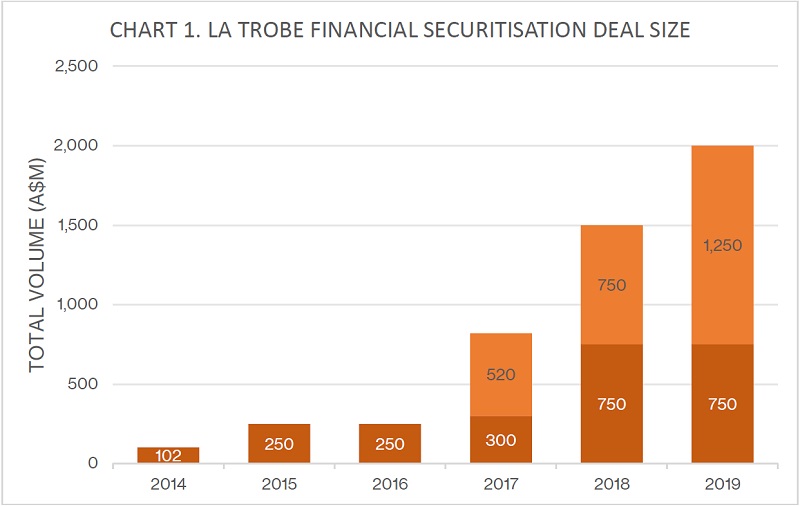

On 10 October, La Trobe Financial Capital Markets Trust 2019-2 (La Trobe Financial 2019-2) printed with total volume of A$1.25 billion (US$848 million), making it the issuer’s largest-ever RMBS. The deal was arranged by National Australia Bank (NAB), which was joined as lead manager by Commonwealth Bank of Australia, HSBC, Macquarie Bank, Natixis, United Overseas Bank and Westpac Institutional Bank.

Each of the issuer’s previous three deals had been for A$750 million (see chart 1). Martin Barry, chief treasurer and strategy officer at La Trobe Financial in Sydney, says the firm wanted to test the waters with a larger deal on the back of ongoing strong book growth.

La Trobe Financial had three asset pools – of A$750 million, A$1 billion and A$1.25 billion – rated before soft-sounding the market, initially for a A$750 million deal. “There was strong interest from repeat investors and indication of appetite for larger volume. We also received interest from new local and offshore investors, which gave us confidence to launch the deal at A$1 billion,” says Barry.

Barry says a handful of investors placed large orders following the launch while demand was strong across the capital stack. He says final bids in excess of A$2 billion from 31 investors allowed La Trobe Financial to print its maximum volume of A$1.25 billion.

Source: KangaNews 14 October 2019

The issuer split its triple-A rated, junior A2 notes into short- and long-dated tranches for La Trobe Financial Capital Markets Trust 2019-1 in April and did so again for the latest deal. It has taken this approach for its A1 notes in all transactions since the beginning of 2018 with the goal of hitting specific pockets of demand.

Barry says doing the same in A2 notes dials in further to demand for triple-A notes from investors that have particular appetite either to avoid call risk or take duration while gaining a yield pickup relative to the senior A1 notes.

Paul Kok, Melbourne-based director, capital markets and advisory at NAB, tells KangaNews: “The structuring of the A2S and A2L tranches is unique to La Trobe Financial and is designed to meet specific real-money investor demand. While investors in the short-dated tranche have the benefit of being paid relatively quicker, the long-dated tranche acts like a soft bullet and places investor confidence on La Trobe Financial’s willingness and ability to call.”

While La Trobe Financial maintained 30 per cent initial credit enhancement on its senior notes in La Trobe Financial 2019-2, Barry reveals that the level required from S&P Global Ratings for a triple-A rating has come down – to 11 per cent from 12.5 per cent.

Barry says this has been driven by an increase of the quality of loans the issuer is making to traditional bank customers and a corresponding decrease in the pool’s loan-to-value ratio reflecting the higher levels of equity these customers hold.

Demand picture

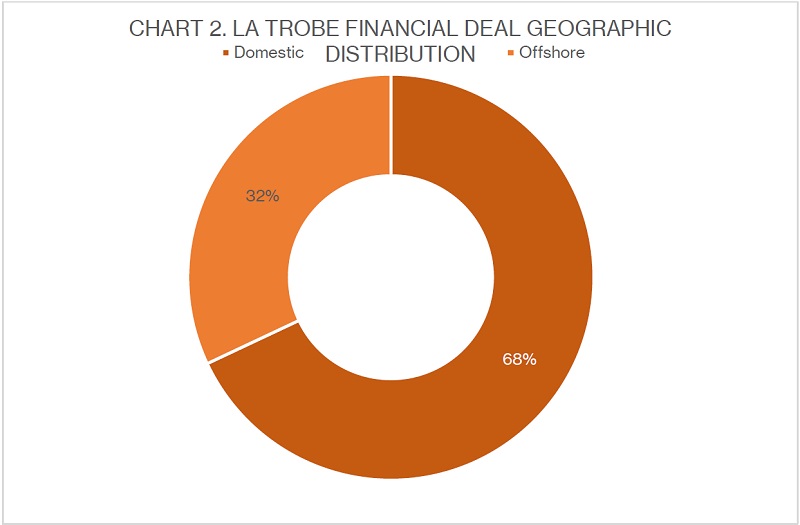

La Trobe Financial 2019-2 was distributed primarily to domestic accounts though there was also robust offshore participation, which Barry says was broad-based across jurisdictions (see chart 2). 76 per cent of the transaction was distributed to real-money accounts.

Kok says offshore demand was focused on Europe and Asia, which was aided by the fact it met EU and Japanese risk retention standards.

Barry adds: “Australian nonbank RMBS is still providing good yield and very good performance. Furthermore, the clouds that were on the horizon at the beginning of 2019 regarding the federal election and the housing market downturn have parted, giving renewed impetus for investors to look at the asset class.”

Source: National Australia Bank 14 October 2019

Kok agrees that Australian nonbank RMBS continues to present a good opportunity for global investors, particularly given the level of credit enhancement provided on triple-A senior notes is rare in other jurisdictions. While the offshore bid will ultimately often be determined by relative value, he says the technical factors supporting RMBS persist.

The Australian dollar market is also ready to absorb more supply, according to Kok. According to KangaNews data, by 11 October there had been more than A$33 billion of total issuance in Australia in 2019, eclipsing all post-financial-crisis year-end totals except 2017.

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

Related news