Fixed-income investor survey: downtempo notes

The H2 2019 iteration of the Fitch Ratings (Fitch)-KangaNews Australian Fixed-Income Investor Survey suggests asset managers have a relatively negative outlook on the Australian economy. Geopolitical risk is top of the agenda, while investors anticipate further monetary stimulus and a weak operating environment for local business.

By Helen Craig and Laurence Davison

The survey was conducted by KangaNews over a two-week span in late August and early September. A total of 47 investors responded to the survey, all of them institutional fund managers based in Australia. This is the 12th edition of the twice-yearly survey.

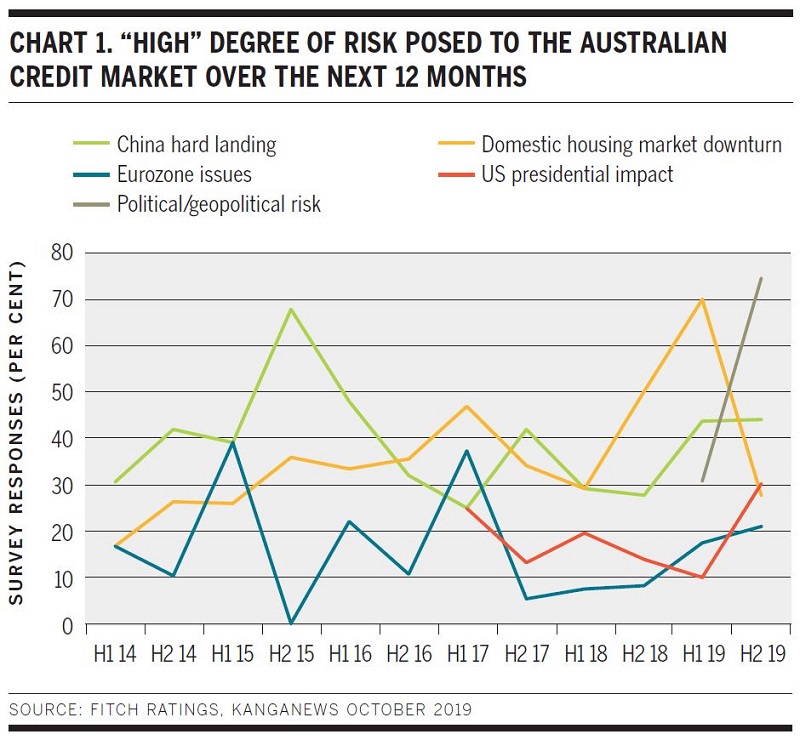

Political and geopolitical risk has been included as a risk factor for just the past two surveys. But trade tension and other global factors caused it to leap up investors’ list of concerns in the second half of 2019. Almost three-quarters of survey respondents rated it a “high” risk factor for the coming 12 months – a record for any risk factor assessed in the survey going back to its introduction in H1 2014 (see chart 1).

Fitch’s analysts say Australian fund managers are right to be concerned about geopolitical tension even if the headline noise dies down. They add: “Trade policy disruptions – including the recent sharp escalation in the US-China trade war and significant risks of a ‘no-deal’ Brexit – are darkening the global economic outlook. In a September update of its global economic outlook forecasts, Fitch made significant downward revisions to China and Eurozone GDP growth forecasts over the next 18 months.”

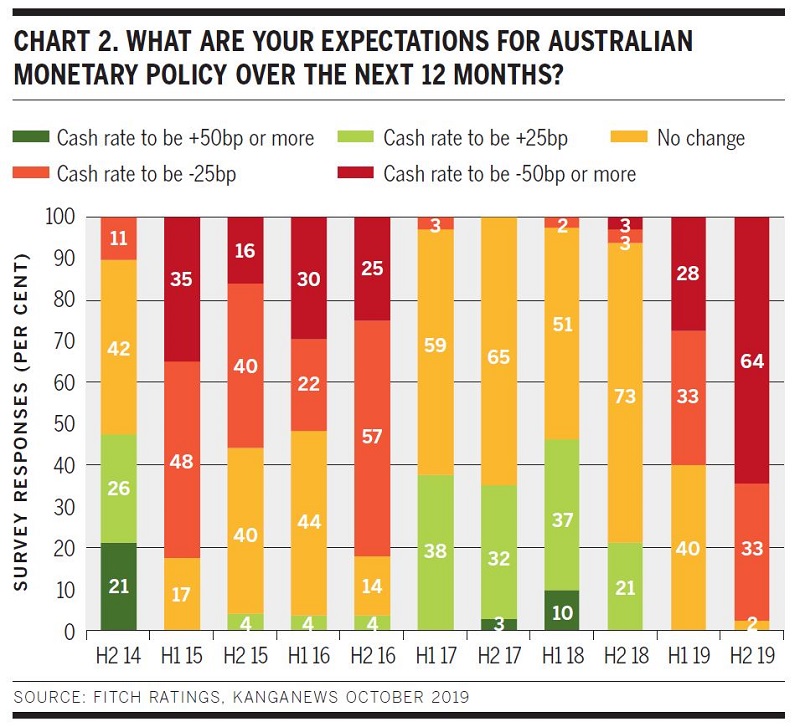

Investors also anticipate a weakening Australian economy. The survey was conducted prior to the Reserve Bank of Australia (RBA) cutting the Australian cash rate in October. Virtually every survey respondent anticipated at least one cut in the year ahead and nearly two-thirds expect two or more (see chart 2).

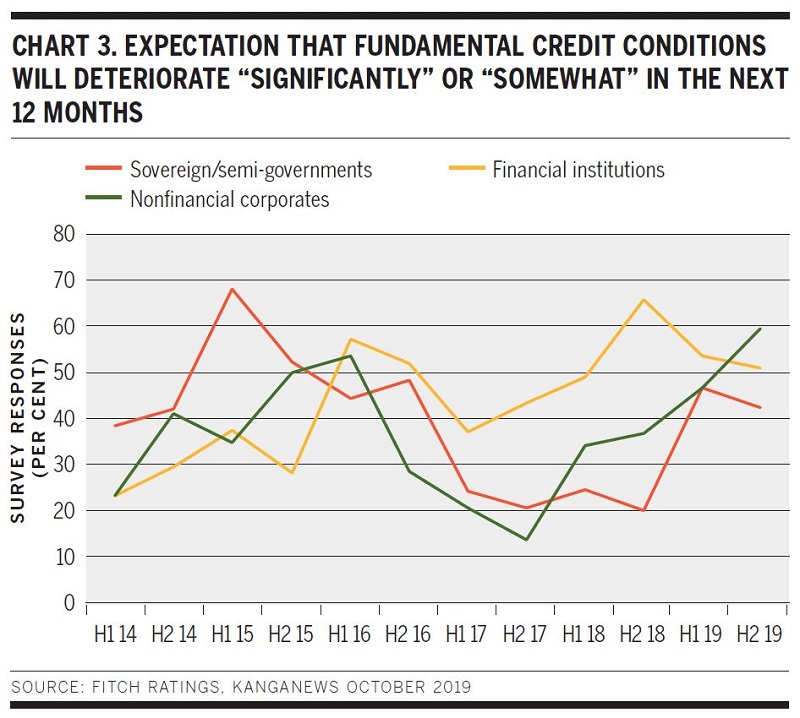

Views on credit conditions suggest the Australian fixed-income investor base believes difficulties are taking root in the real economy. For the first time in the Fitch-KangaNews survey’s history, the greatest expectation of deteriorating credit conditions is for the nonfinancial corporate sector (see chart 3).

Expectations of weakening credit conditions for financial institutions have eased, though more than half the survey respondents still expect this outcome over the coming 12 months.

Fitch’s analysts suggest the credit outlook is the product of slower growth in Australia, and that the slowdown also explains the views on corporates. “The Australian economy had another quarter of tepid growth in Q2 2019. The sharp slowdown since H2 2018 is domestically driven and has been triggered by a protracted downturn in the housing market. Declining house prices have dragged down construction activity and weighed on household spending against a backdrop of sluggish income growth, a low savings ratio and high household debt.”

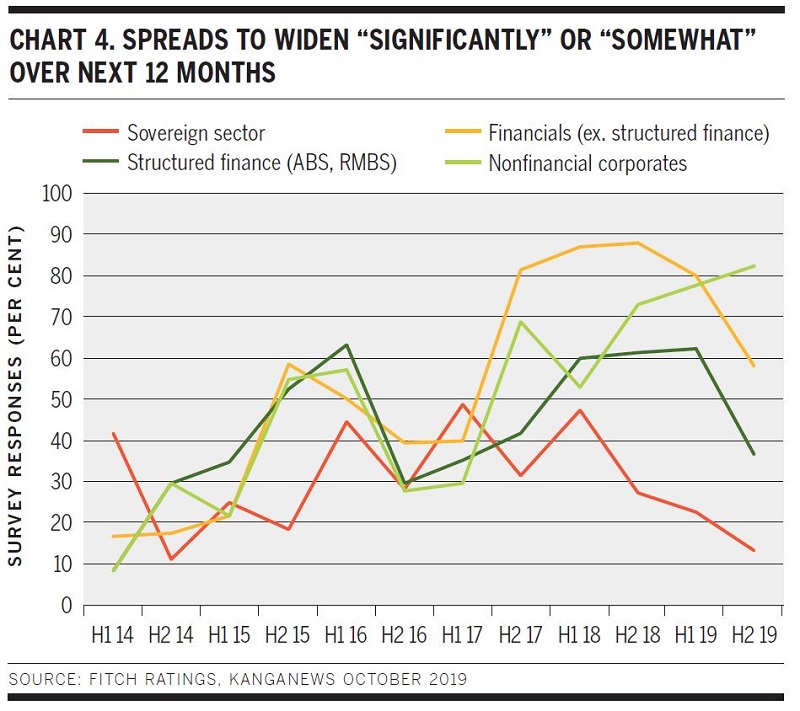

Perhaps unsurprisingly, asset managers expect spreads to follow the path of credit conditions. More than 80 per cent of survey respondents forecast wider nonfinancial corporate spreads in the coming year – a record for this sector – while the proportion of investors anticipating wider bank spreads has fallen (see chart 4).

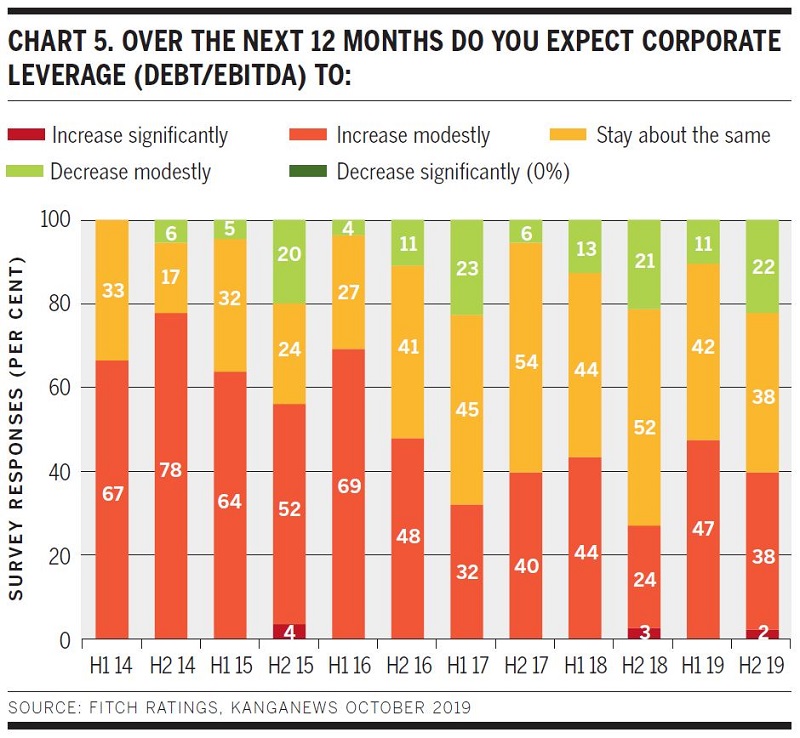

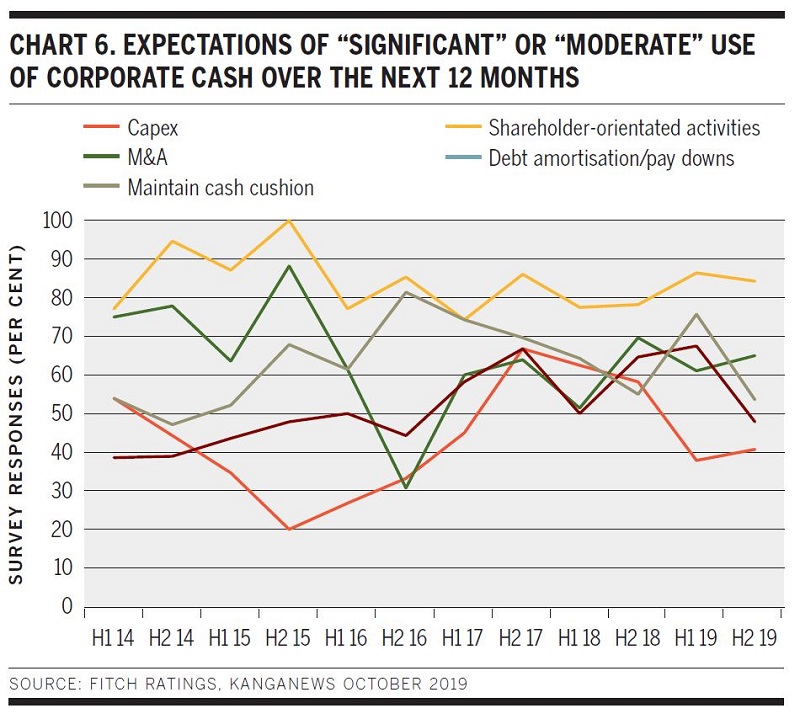

On the other hand, there seems to be little expectation of a significant change in corporate behaviour. Barely a fifth of survey respondents expect corporate leverage to reduce over the next 12 months – none of them significantly (see chart 5). Almost twice as many investors anticipate increased corporate leverage. More than 80 per cent of survey respondents also expect corporates will continue to return profits to shareholders, in some cases apparently at the expense of maintaining cash cushions or paying down debt (see chart 6).

The impact of a low cash rate on corporate investment will be marginal if Australian fixed-income fund managers are correct. Capex expectations remain puny, with barely 40 per cent of investors projecting investment will be even a moderate use of corporate cash in the year ahead.

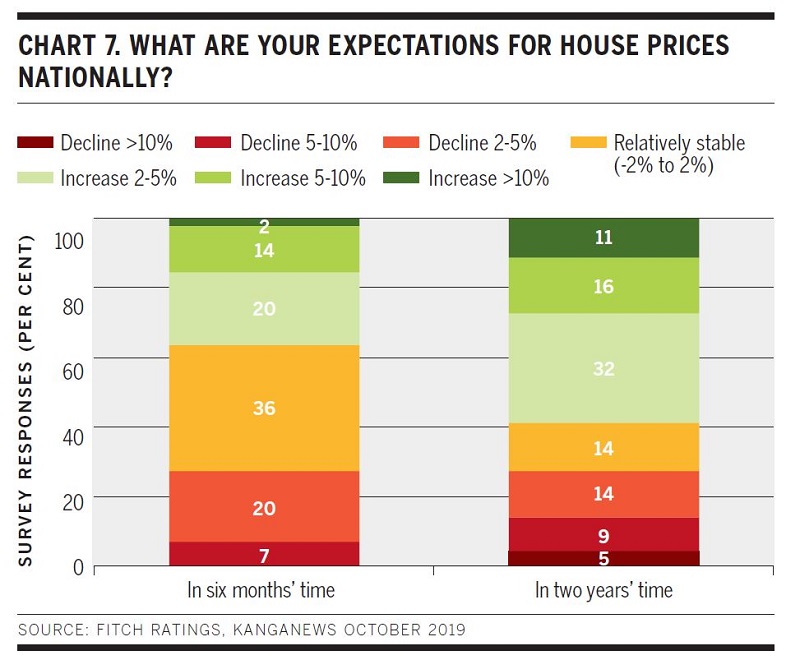

On a more positive note, investor concern about the Australian housing market appears to have abated significantly. A housing downturn was the top risk factor in the Fitch- KangaNews survey just six months ago, with more than 70 per cent of survey respondents ranking it a high risk. Not only has this figure fallen right back – to around 30 per cent – but the majority of investors now expect house prices to climb over the next two years.

Outlooks are more mixed for the next six months (see chart 7), but over the medium term the balance of probabilities presented by fixed-income investors appears to be gradual, u-shaped recovery in the housing market.

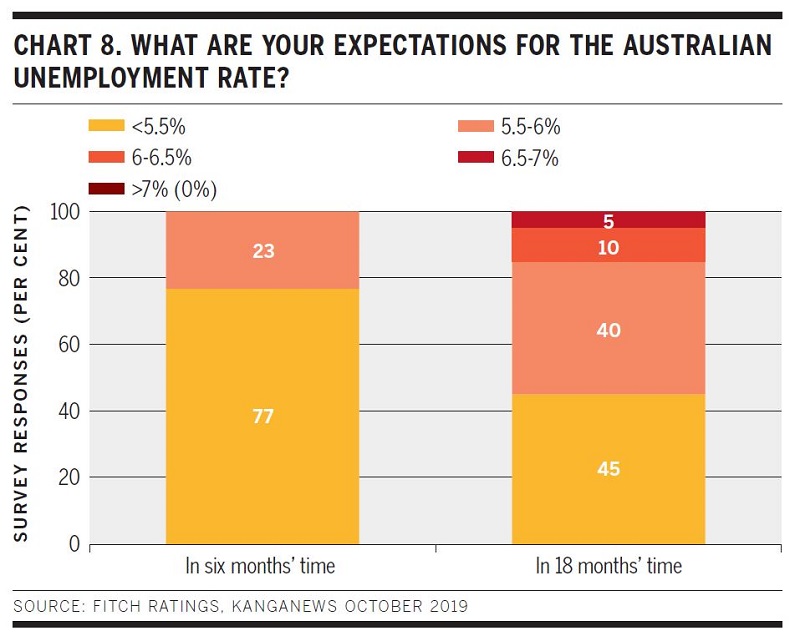

As well as the low cash rate, investors seem to believe ongoing subdued unemployment will support a benign housing-market outlook. Three-quarters of investors expect unemployment to remain lower than than 5.5 per cent for at least the next six months (see chart 8). The outlook is slightly less positive for the next 18 months, but even here 85 per cent of investors do not foresee unemployment climbing to more than 6 per cent.

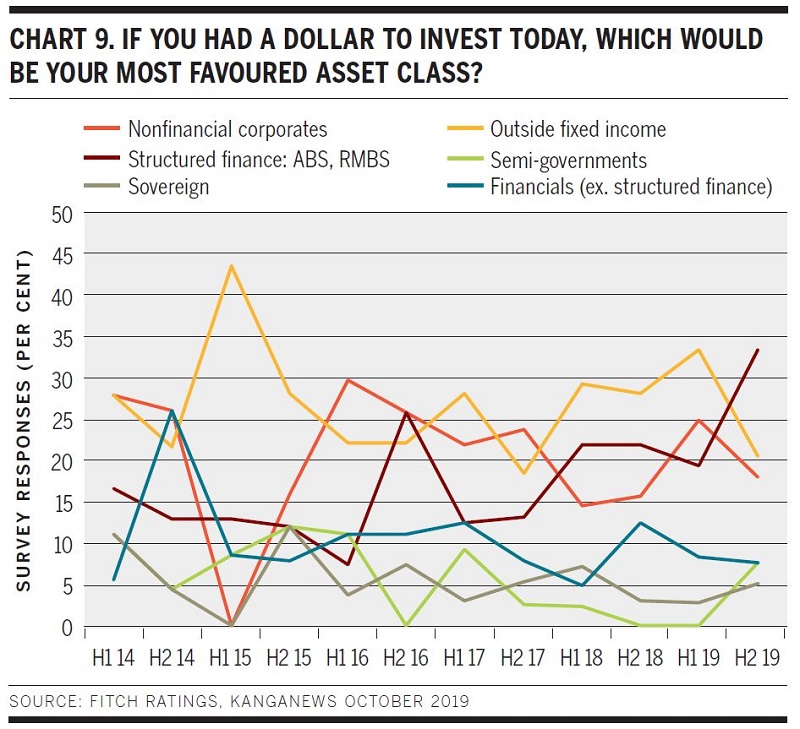

On balance, the investment outlook suggests Australian fixed-income investors are cautious but not in a full-blown flight to quality. For instance, for the first time in the Fitch-KangaNews survey’s history structured finance – asset-backed securities and residential mortgage-backed securities – are the most preferred asset class for marginal investment (see chart 9).

This might suggest fund managers are looking for high-quality product with a yield pickup and are prepared to sacrifice some perceived liquidity to get it. At the same time they are, as the survey question on the housing outlook implies, relatively comfortable with allocations to underlying collateral sourced from the Australian housing market.

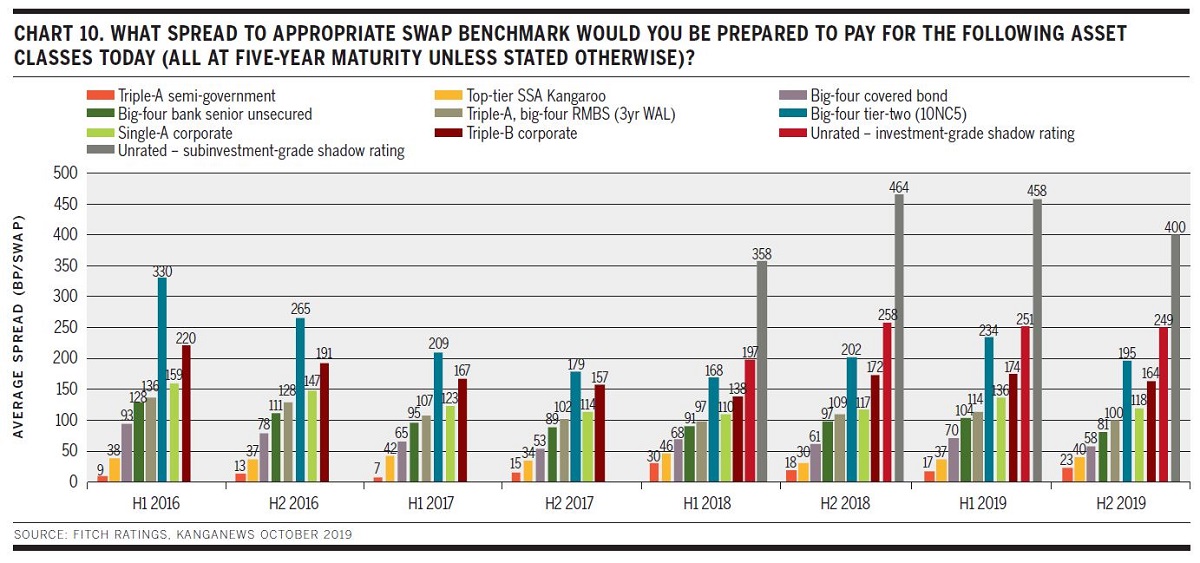

Neither have fund managers’ spread expectations blown out. In fact, the average spread investors say they would pay for most asset classes is at or inside all-time tight levels for the Fitch- KangaNews survey (see chart 10).

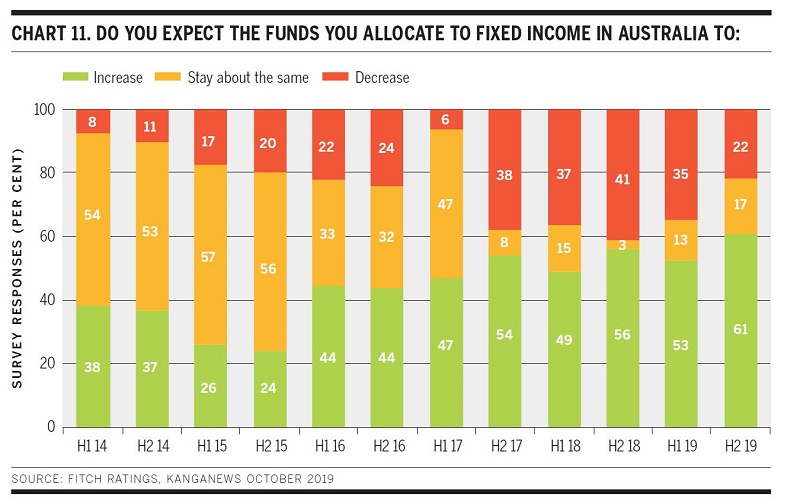

Perhaps the reason for the continued path tighter in spreads lies in the ongoing imbalance between investment funds and investable assets. For the first time in this survey’s history, more than 60 per cent of fixed-income investors expect their funds under management to increase (see chart 11).

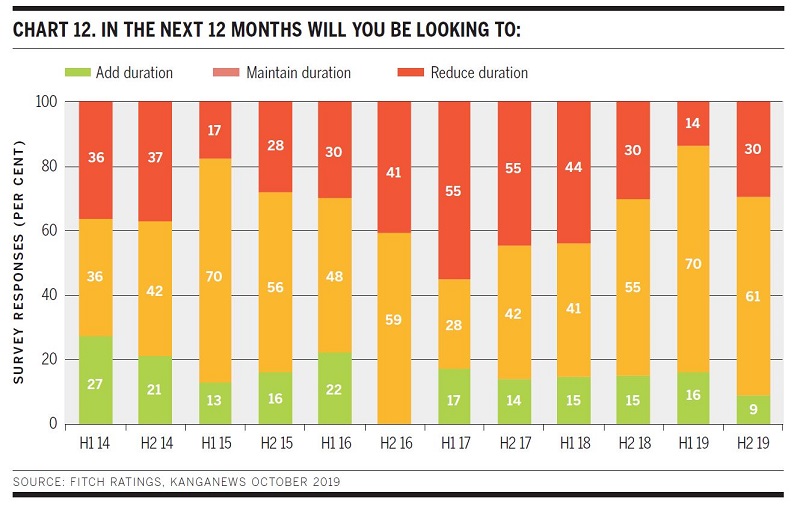

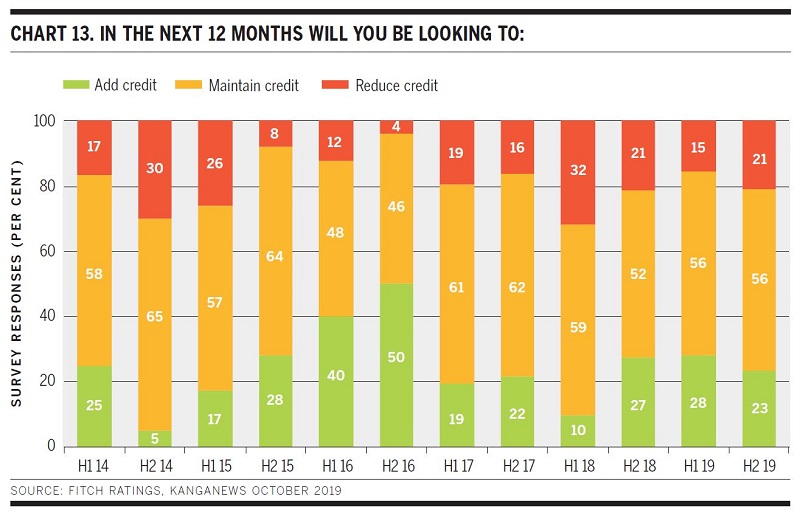

This is more of a hunt for assets than a hunt for yield, however. Only a handful of survey respondents expect to extend duration in the next 12 months, though most expect to maintain rather than reduce it (see chart 12). Expectations of adding and reducing credit over the same period are roughly even, again with the majority of investors planning to maintain exposures (see chart 13).