The stimulation game

Corporate treasurers in Australia and New Zealand clearly believe their local economies are in downturn mode and expect further monetary easing, according to the sixth annual KangaNews-Moody’s Investors Service (Moody’s) Corporate Borrowers Intentions Survey. Cheap money may be having some impact on corporates’ desire to borrow, but probably only at the margin.

By Helen Craig and Laurence Davison

This year’s survey was conducted by KangaNews in September and received responses from more than 70 capital-markets-relevant nonfinancial corporate issuers in Australia and New Zealand. This is the largest response ever to this survey, which has been published every year since 2014.

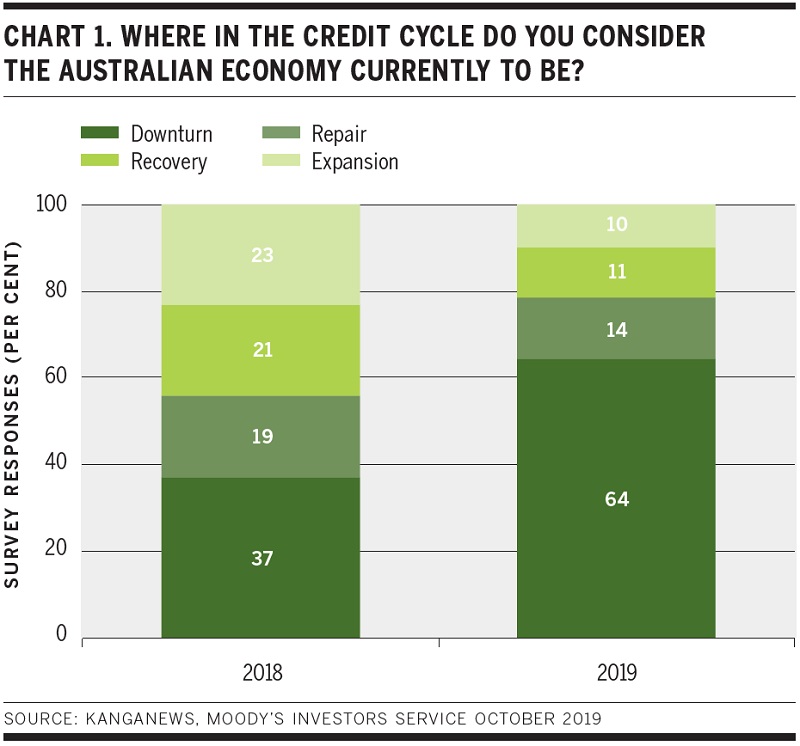

Corporate borrowers’ economic outlooks have noticeably declined in the past 12 months. Nearly two-thirds of survey respondents in 2019 say their local economy is in a downturn phase – almost twice the proportion who held this view a year ago (see chart 1).

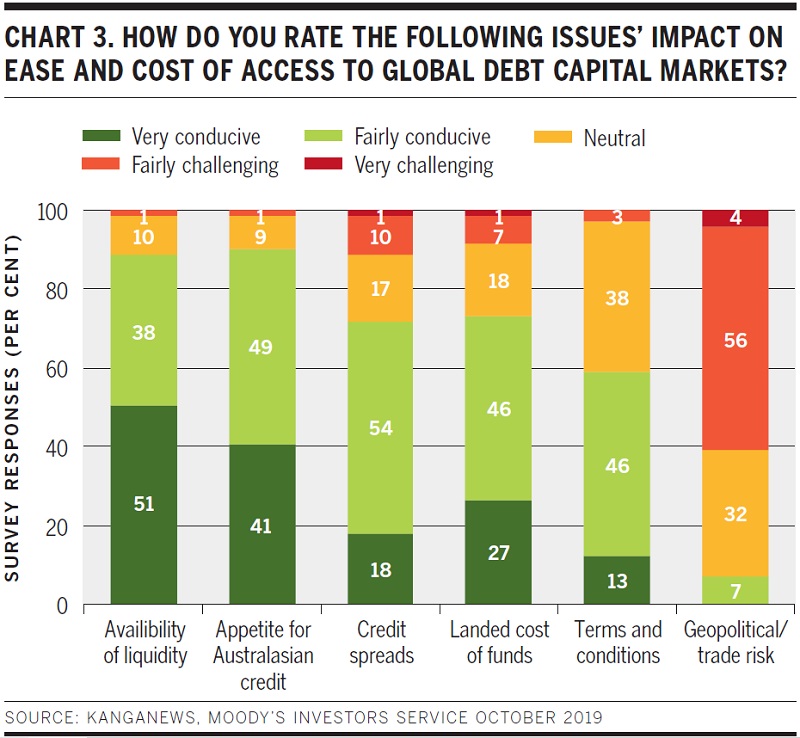

Unsurprisingly, therefore, the vast majority of corporate borrowers expect further monetary easing in the year ahead. The survey was conducted prior to the Reserve Bank of Australia cutting the cash rate by 25 basis points in October, but more than half of Australian corporates surveyed predict at least one more cut in the next 12 months (see chart 2).

The picture is if anything even more bearish in New Zealand, even though the Reserve Bank of New Zealand made its 50 basis point cut in August – before the KangaNews-Moody’s survey was conducted. Despite the already lower official cash rate, nearly three-quarters of Kiwi corporates expect a further 50 basis points or more of cuts in the year ahead.

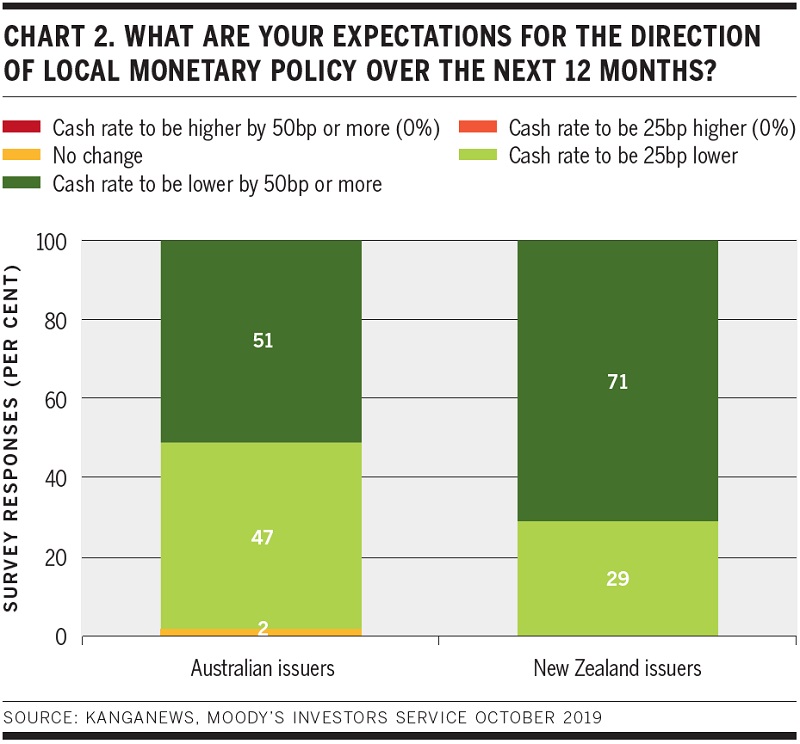

Borrowers confirm that most factors are already conducive for capital-markets issuance – and the main headwind is beyond the control of local central banks anyway. Availability of liquidity and appetite for Australasian credit both seem set fair, while most corporate issuers are at least satisfied with the cost of issuance and with terms and conditions (see chart 3).

The main concern when it comes to accessing capital markets is geopolitical and trade risk, which 60 per cent of Australasian issuers assess to be challenging – albeit most of these only “fairly” challenging. No other factor comes close to having a majority of corporate issuers suggesting it is a challenge to issuance in the second half of 2019.

Patrick Winsbury, associate managing director, corporate finance and financial institutions groups at Moody’s in Sydney, says: “From an Australian perspective, a transmission mechanism for geopolitical risk into credit is via a bond issuer’s fundamental credit profile. This could be direct – for example if sales revenue or cash flow declines as a result of declining exports – or second order, being a generalised decline in consumer and business sentiment as a result of uncertainty.”

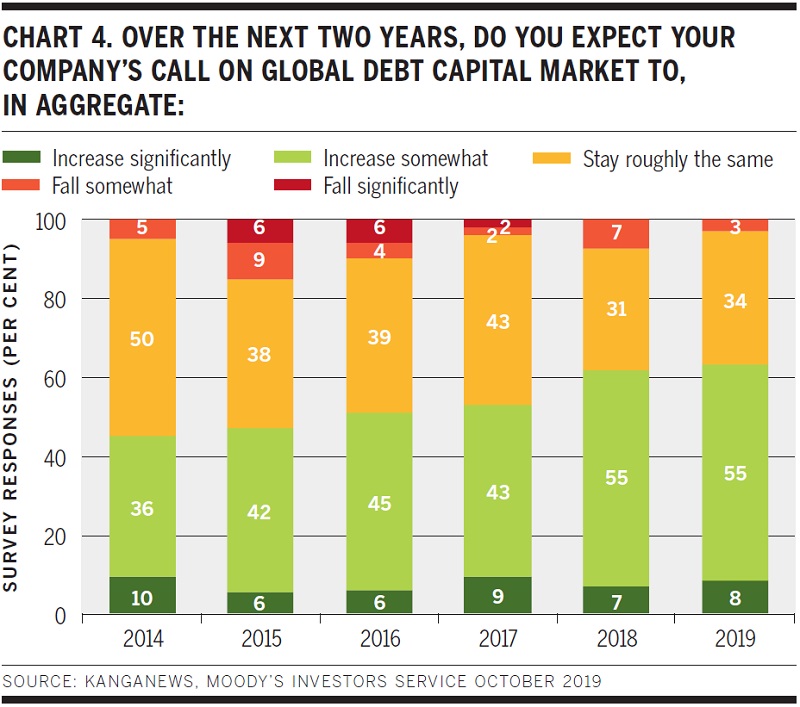

The availability of relatively supportive capital markets might be inducing corporates to be more active. A record proportion of survey respondents – 63 per cent – say they expect their companies’ call on debt capital markets to increase over the next two years while just 3 per cent say they expect to be less active (see chart 4).

For context, in 2019 roughly half the responses to the KangaNews-Moody’s survey came from companies that say they issue in debt capital markets on average at least once each year. A further third say they issue every 2-3 years and the remaining 20 per cent say they are less frequent issuers or do not currently have debt-market securities outstanding.

Whether an increase in projected capital-markets activity means corporates will be borrowing more overall is hard to determine. More than 40 per cent of survey respondents also indicate they expect their companies to have a greater proportional use of capital-markets funding in their debt books in the foreseeable future, suggesting more issuance may in many cases reflect rebalancing rather than additional debt.

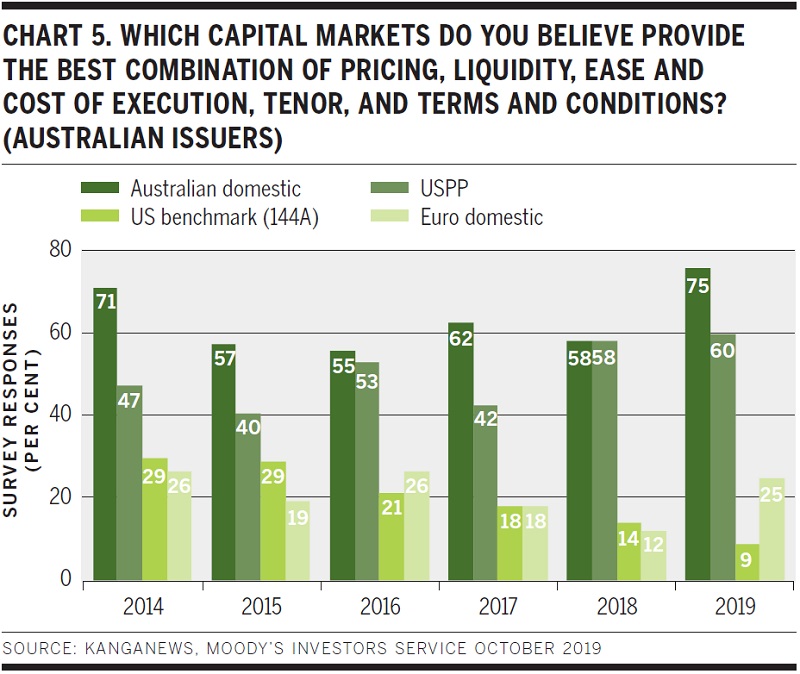

When it comes to market selection, Australian corporates appear to be increasingly comfortable with the value proposition of their domestic issuance option. Three-quarters of survey respondents from Australia indicate that the local market is among the best debt-funding options available – again, a record response (see chart 5).

US private placements (USPPs) also score for Australian corporates, while supportive euro pricing throughout 2019 has seen this issuance option rebound in popularity among a select group of issuers.

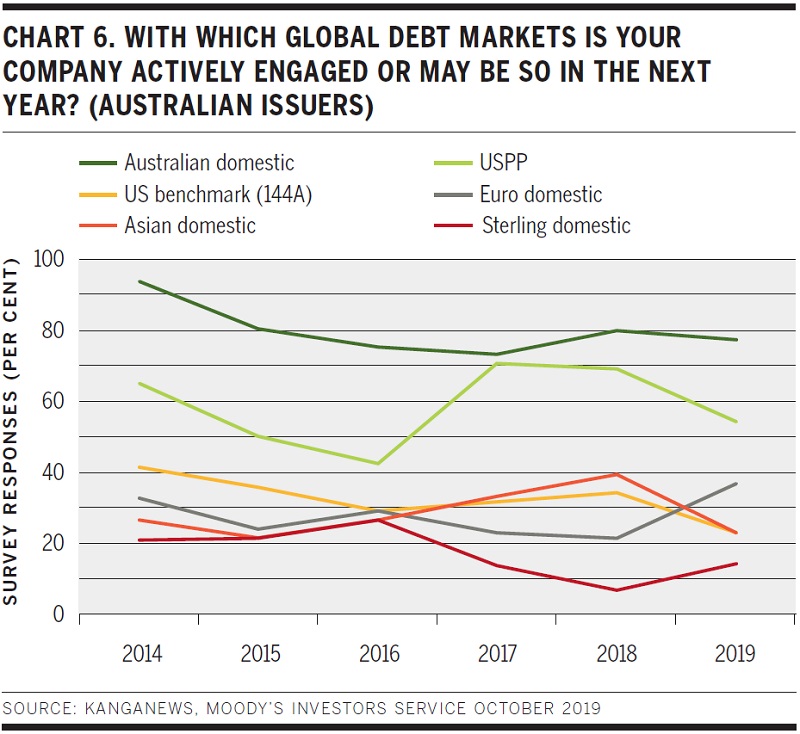

A similar picture emerges when it comes to the markets Australian corporates think they may be engaged with in the year ahead. Domestic issuance continues to be the most likely approach, euros has rebounded from a low level and there are slightly reduced expectations of USPP activity (see chart 6).

Winsbury says Australian borrowers may have come to look on their domestic market as a fallback funding option to be used when other debt sources are less appealing. “While the Australian dollar corporate bond market may be strategically important, other funding markets may offer a lower spread or longer tenor, or have greater certainty of funding for particular issuers,” he comments. “Many issuers will regularly tap the Australian dollar market in smaller amounts to maintain access if foreign markets experience dislocations in future.”

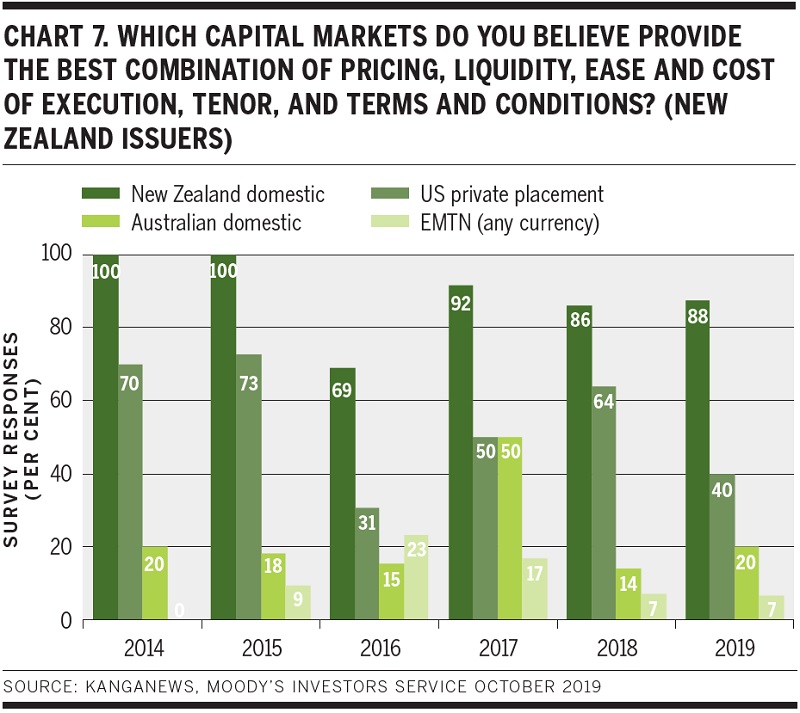

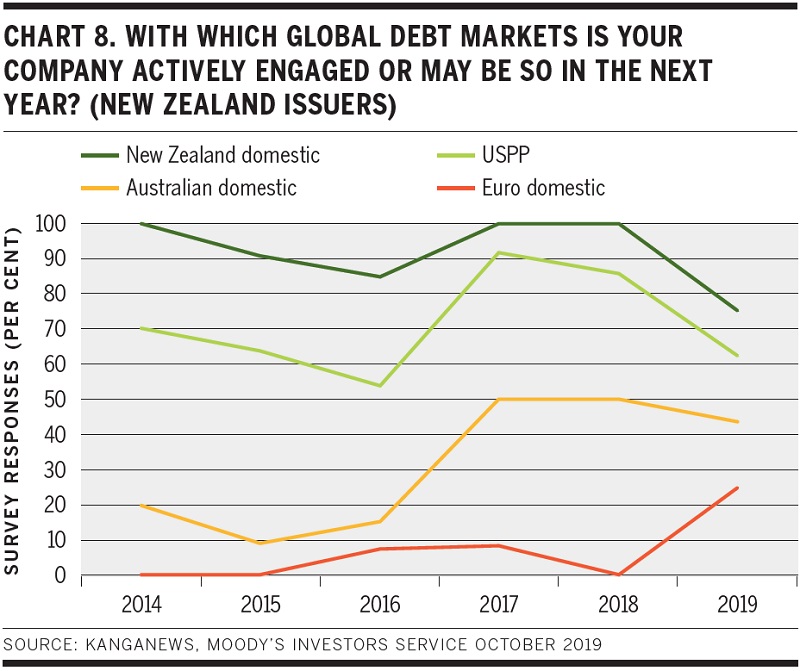

New Zealand corporates, meanwhile, have historically been more tightly focused on their home market – and the 2019 KangaNews-Moody’s survey suggests little change in this outlook. Issuance in New Zealand remains the clear best option for most local corporates (see chart 7) and reduced expectation of future market engagement almost across the board (see chart 8) may represent nothing more than a lower refinancing period ahead.

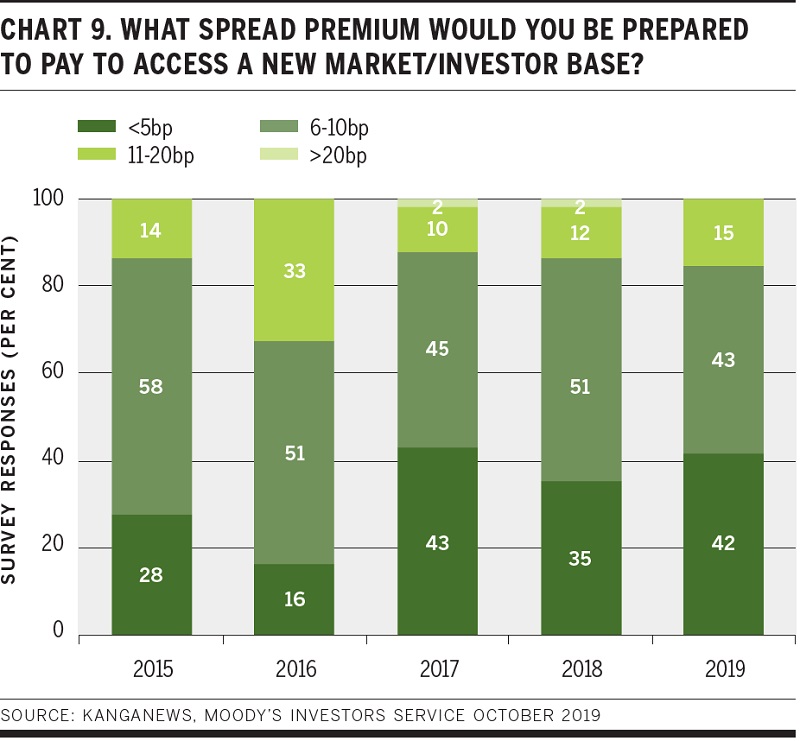

While the range of markets into which Australian and New Zealand corporates, taken as a whole, plan to issue may be relatively narrow, the KangaNews-Moody’s survey indicates an ongoing willingness to offer at least some premium to gain access to a new liquidity pool. More than half of all survey respondents say they would pay at least a 6 basis point premium for this sort of funding diversity and 15 per cent would pay as much as 20 basis points (see chart 9).

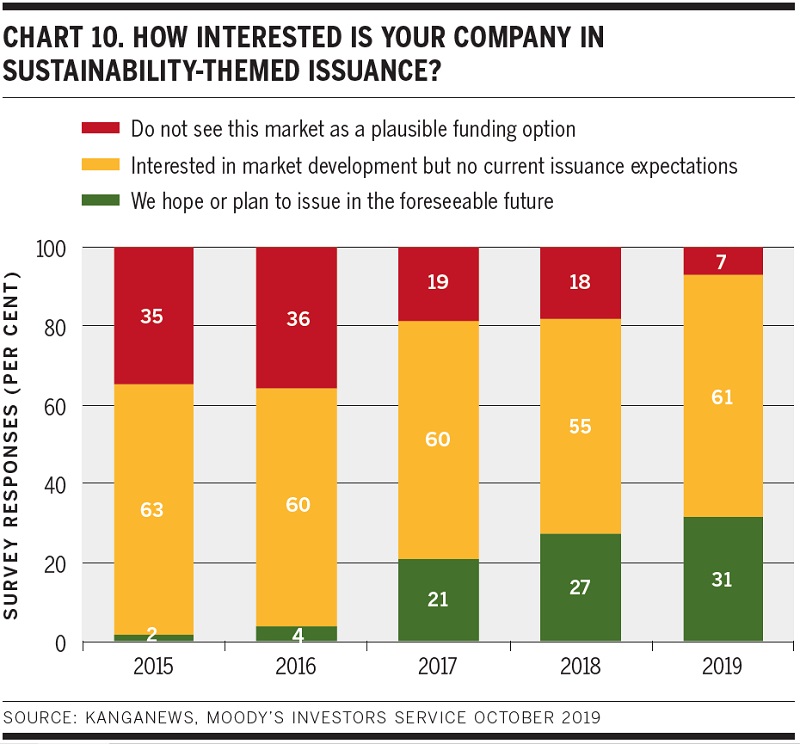

The KangaNews-Moody’s survey also suggests notable growth in interest in environmental, social and governance (ESG) factors and products in the debt-funding universe. While not quite a third of borrowers say they hope or plan to issue sustainability-themed debt in the foreseeable future, the number saying they do not see ESG-linked debt in any format as a plausible funding option for their company is – at 7 per cent – also at its lowest-ever level in this survey (see chart 10).

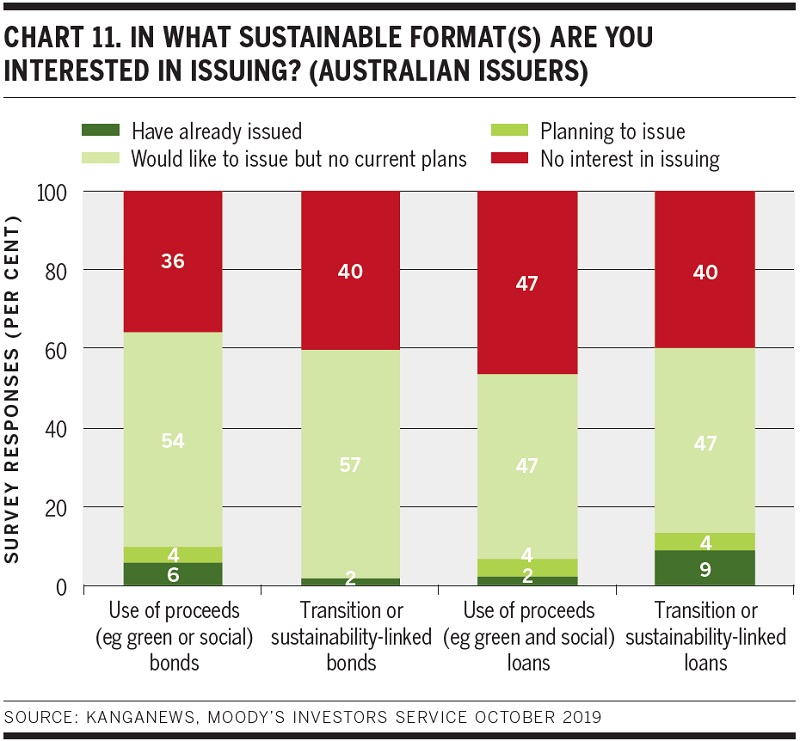

Interest may be growing in general terms, but the number of corporate borrowers with clear plans around deployment of ESG instruments remains small. Just 10 per cent of Australian issuers either have issued or have specific plans to issue use-of-proceeds bonds like green or social bonds (see chart 11). There is slightly more engagement with the emerging sustainability-linked-loan (SLL) asset class. But most Australian corporates appear to be open to various options in the ESG space.

Corporate green-bond issuance has yet to develop breadth or depth in Australia. According to KangaNews data, there have been just six domestic transactions since the first came to market in 2017 and only one of these has been from an issuer outside the property or higher-education sectors. Some market users have much greater hopes for SLLs and bonds deploying the same principles. This is based on the idea that borrowers do not need to have a large pool of qualifying assets to issue in this format – making the product more suitable for ESG transition.

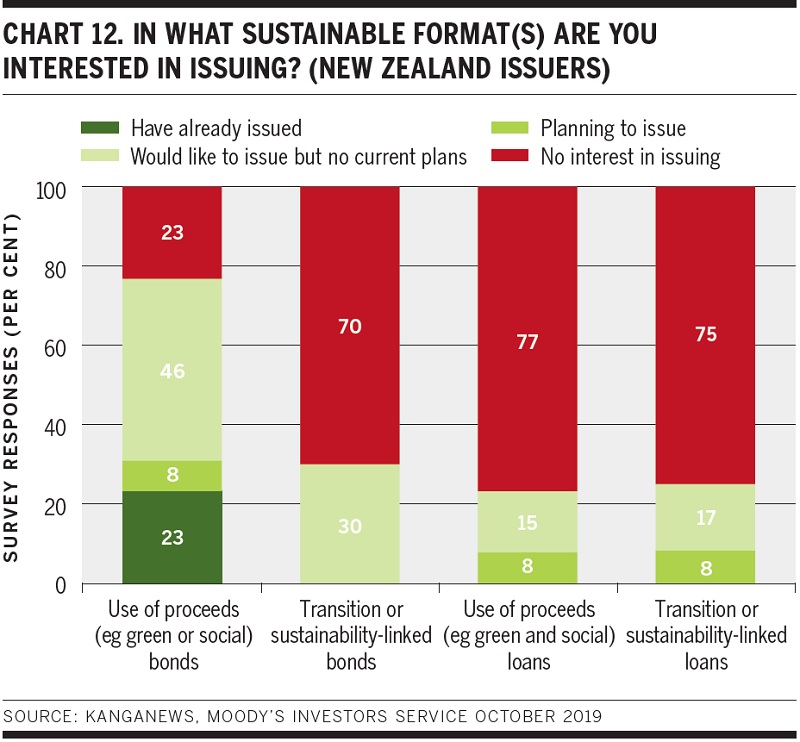

The only real difference in New Zealand is that use-of-proceeds bonds may have taken slightly deeper roots with corporate issuers. Nearly a third of those responding to the KangaNews-Moody’s survey either have issued these instruments or plan to do so (see chart 12). On the other hand, engagement with alternative forms of ESG funding like sustainability-linked products is relatively lower in New Zealand.

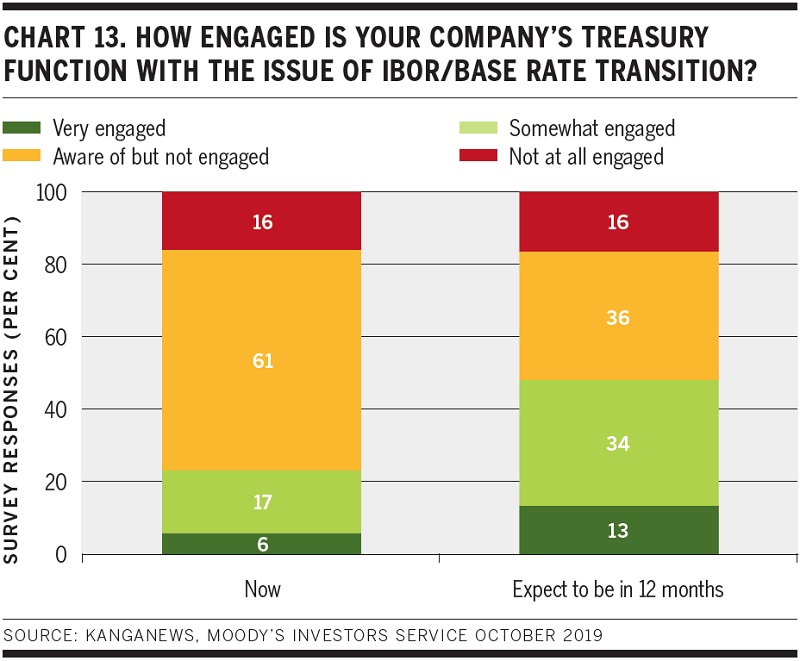

Australasian corporates also only have limited interest in another major issue in global capital markets: the end of interbank offered rates (IBORs) and their replacement with alternative benchmarks. Fewer than a quarter of survey respondents say they are engaged with IBOR transition in 2019 (see cart 13). While the number expecting to be engaged in a year’s time is higher it still amounts to less than half the corporate borrowers responding to the survey.

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.

Adelaide Airport rekindles investor relations in domestic return as it hits funding turning point

Following its first Australian dollar deal in seven years, Adelaide Airport says re-engaging with the local investor base was a top priority as it embarks on a new capex plan and plans for upcoming maturities. While issuance has slowed since a hectic end to Q1, the deal book demonstrates ongoing robust demand for Australian dollar corporate credit.