GSS capital a diversifier for ANZ in support of TLAC requirements

ANZ Banking Group (ANZ) intends to maintain its commitment to green, social and sustainability (GSS) bond issuance, having printed its first such deal in tier-two format in the euro market. The issuer says use-of-proceeds deals are as applicable to capital issuance as senior debt and can even help diversify the investor base as the bank fulfils an increased tier-two requirement.

ANZ’s €1 billion (US$1.1 billion) 10-year non-call five tier-two sustainable development goals (SDG) deal priced on 15 November. ANZ, Barclays, BNP Paribas, HSBC and Societe Generale led.

The transaction is the first-ever euro-denominated GSS bank-capital transaction. It is also ANZ’s second SDG bond, following a €750 million five-year senior-unsecured deal priced in February 2018. The funds raised by the transaction will finance or refinance projects in accordance with ANZ’s SDG bond framework in areas such as health, education and clean energy.

GSS capital

The Australian Prudential Regulation Authority (APRA) announced in July that Australia’s major banks will be required to hold more additional - likely tier-two – capital to meet total loss-absorbing capacity requirements. All else being equal the major banks expect to issue less senior-unsecured paper as their tier-two requirements grow.

Until ANZ’s tier-two deal, all Australian bank GSS bond deals had been in senior format. Mostyn Kau, Melbourne-based head of group funding at ANZ, says the bank’s focus on GSS issuance has not diminished even though it will be raising more tier-two capital and less from senior-unsecured funding.

Although the deal was the first subordinated GSS issuance by an Australian bank, no structuring innovations were required. “The structure of the transaction is exactly the same as any other TLAC-eligible tier-two deal and the use-of-proceeds layer is no different from a senior-unsecured deal,” Kau says. “Bank capital is still also funding for the bank. With ANZ now requiring more tier-two and less senior-unsecured funding, it made sense to explore a SDG tier-two transaction.”

Kau adds that the emphasis on maintaining a commitment to SDG issuance is driven partly by ANZ’s new targets for lending to environmentally and socially sustainable projects. In October, ANZ surpassed its 2020 target for A$15 billion (US$10.2 billion) of lending in this space and it has now set a new target to lend A$50 billion by 2025.

“There is a lot of motivation to facilitate funding in this space. While ANZ has in no way been funding-constrained over recent years, SDG bonds increase diversification into a growing investment pool of funds and they increase the prominence of lending to projects which are environmentally sustainable. Even though the product mix of our funding requirement has changed, the focus on SDG issuance remains,” says Kau.

Broad base

APRA’s TLAC requirements for major banks have spurred the big four into action since July. The domestic and US markets have been the choice destinations so far, but the banks have acknowledged that they expect to broaden their horizons for tier-two issuance to fulfil the requirement.

Kau says ANZ had not issued a euro tier-two deal in the last decade. “The new requirement makes access to the broadest possible range of markets and investors critical. We therefore wanted to re-establish a presence in tier-two with European investors.”

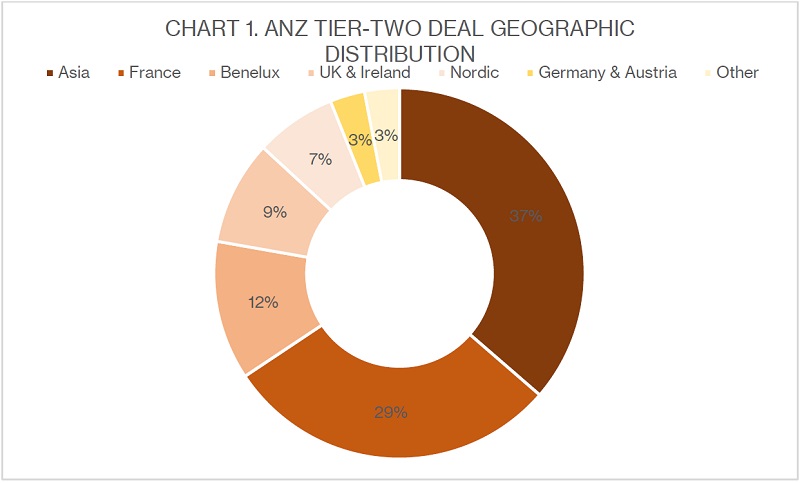

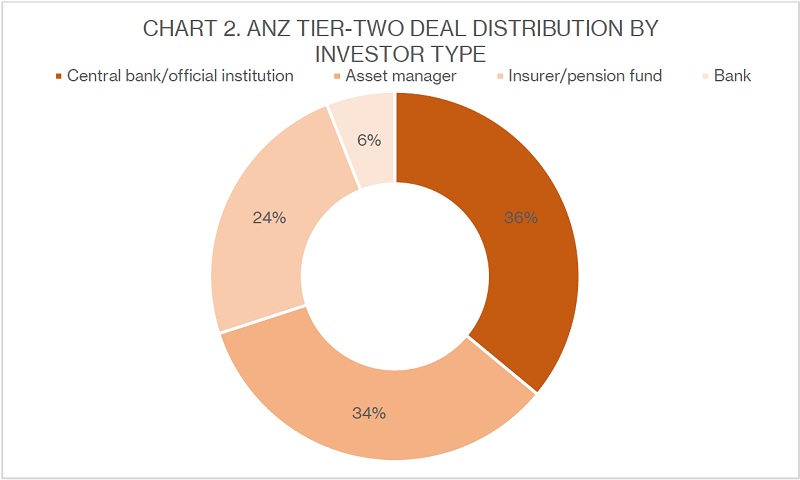

The deal was broadly distributed in Europe and more than a third was allocated to investors in Asia (see chart 1). Central bank and official institution investors, asset managers and insurance and pension funds were all substantial participants (see chart 2).

Source: ANZ 21 November 2019

Source: ANZ 21 November 2019

Europe has been at the vanguard of GSS innovations in debt capital markets and has the deepest pools of GSS funds. Issuers have consistently been hesitant to ascribe any pricing benefit to a GSS bond over a vanilla bond, but Europe is the market where this has been most likely to occur.

This could potentially be enticing for the major banks given the potential cost of meeting the new TLAC requirements. Kau says, however, that this was not a motivating factor and, while it likely increased the size of demand, it did not result in an obvious pricing benefit.

ANZ’s deal attracted €2.7 billion of bids at the final pricing of 140 basis points over mid swap. Pricing tightened by 20 basis points from launch. Kau says the pricing was 10-15 basis points wide of levels in Australian dollars but says this premium is well worth paying for the diversification of its tier-two investor base.

Kau tells KangaNews that there is scope for issuing tier-two or senior-unsecured SDG bonds in Australian dollars.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news