Global collaboration critical to banking sector goals

The way Australian companies, especially in the financial sector, are responding to environmental and social risks is becoming more sophisticated and more prominent. Siobhan Toohill, group head of sustainability at Westpac Banking Corporation (Westpac) in Sydney, says collaboration between industry participants is taking progress to a new level.

The collaborative mindset that is increasingly emerging in the local and global banking community marks a sea change that is unique to the sustainability sector, Toohill says. “There has been a realisation that if we are going to get this right, we have to work collectively to address this substantial problem.”

The new mentality, Toohill adds, is that of “a rising tide lifts all boats”. Whether it is around climate change in Europe or the response to modern slavery in Australia, a spirit of collaboration is on the rise.

In Australia, for example, the Australian Banking Association now has a sustainability working group which includes the heads of sustainability from the big four as well as regional banks. This group comes together several times a year to discuss key issues affecting the industry such as climate change and Australian banks’ work around the Modern Slavery Act. The banks are also looking at how they can collaborate better around ways they can help stakeholders – including customers (see box on p56) – better compare sustainability performance.

“I’m really excited about this openness and willingness of banks to adopt common fundamentals and a common way to engage with regulators around environmental, social and governance (ESG) risks, such as the Task Force on Climate-related Financial Disclosures (TCFD) framework,” Toohill continues. “It’s powerful that multiple banks have adopted the TCFD – it will really lift the Australian banks to have a more common approach to measurement of climate risk.”

Origin of collaboration

A growing need to measure and disclose the material nature of risk and response has been at the heart of the growth of collaboration in the financial sector. According to Toohill, the role played by the TCFD since its conception in 2015 has had a profound effect across financial markets in this context.

The TCFD laid out an expectation that companies should be reporting on climate risk. This means quantifying and measuring it, setting targets, putting in place relevant governance mechanisms and a general significant increase in focus on the topic.

The TCFD principles initially gained traction in the EU but have now spread globally. In some jurisdictions they are regulated but in others – like Australia – the process remains principles-based. This is not to say TCFD lacks power, though: the mood of ‘if not, why not’ comes from regulators, the stock exchange and also – perhaps most strongly – from shareholders and other investors.

“We are now seeing the mainstreaming of climate-risk awareness and response happening in lots of different ways,” Toohill says. “Within businesses and from investor engagement, the level of maturity in the conversation is increasing as the level of assessment of private risk improves.”

The market has not yet reached its final form. Institutions are still working through different models while the capacity to measure and quantify risk varies. But, Toohill says, one of the most interesting things to observe through the process of TCFD adoption has been the discussions that have emerged within the financial sector.

The role of the PRB

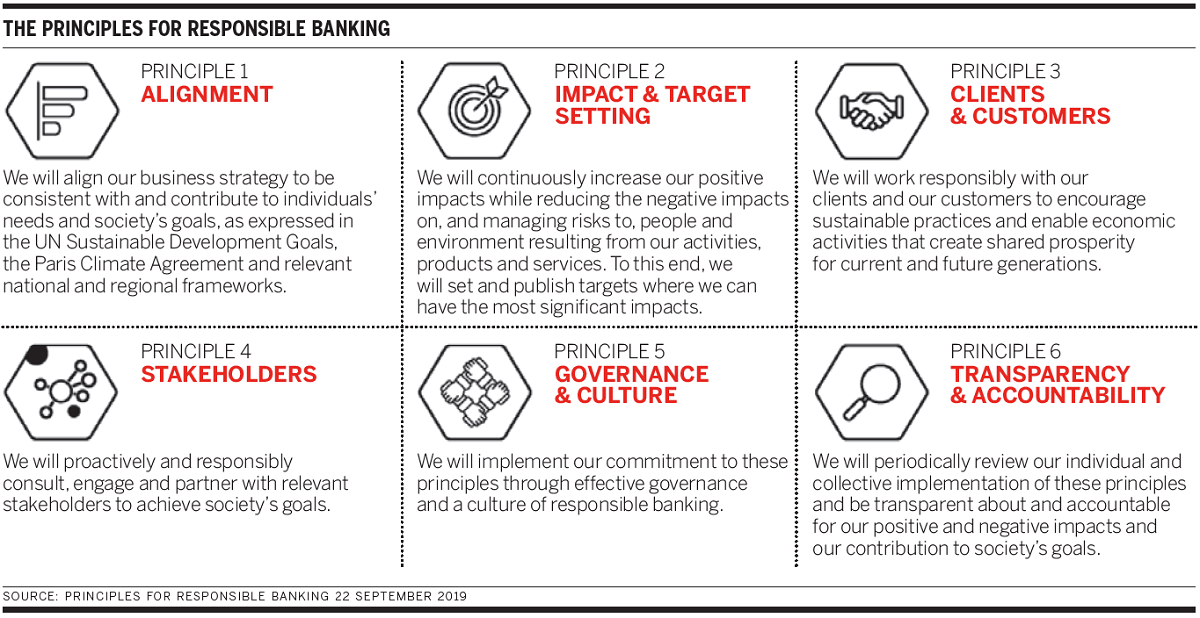

Globally, the UN Principles for Responsible Banking (PRB) is a key initiative for collaboration between banks. These principles were established at the start of 2018 with 11 banks from around the world involved – a list that included Westpac. The number of participating institutions had grown to 30 by the end of 2018. By the official launch of the PRB in September 2019 there were 130 participating banks from 49 countries – representing more than US$47 trillion in assets or approximately a third of the global banking system.

The first of the six PRBs (see table) covers alignment of banks’ strategic purpose with the Paris Agreement and the UN Sustainable Development Goals (SDGs). Other principles cover impact and target setting, working with clients, customers and other stakeholders to achieve sustainability goals, governance and corporate culture, and transparency and accountability.

Integral to all these principles is the idea of progressing together, as an industry, to achieve specific targets. The PRB and the collaborative environment around them can also support banks at different stages on their journies.

Toohill explains: “There was initially concern, as we were developing the principles, that they would play well for a bank that’s quite mature in its sustainability journey but not be so helpful for banks that are just starting out. In designing the principles, we have worked with the expectation that they are about where you are today but also your ambitions for the future. The expectation of the principles is that you are constantly demonstrating improvement and lifting ambition.”

The expectation is that banks should constantly be pushing themselves and also – by engagement through initiatives like the UN Environment Programme (UNEP) Climate Initiative and UNEP Finance Initiative (UNEP FI) – that there should be a significant degree of collaboration and learning from each other. “The ability to connect and engage with international banks – to learn from them – has been quite an extraordinary by-product of participating in the PRBs,” Toohill confirms.

This outcome was not a central component of the original conception of the PRB. Toohill tells KangaNews: “I don’t think we realised when drafting the principles that this kind of global collaboration would emerge. But what we have seen is that learning about global best practice is a key means of delivering the goals we have set ourselves. This can be formally, via UNEP FI, but also informally – we pick up the phone to our international counterparts to work together to drive change.”

Global leadership

Toohill notes, for example, the positive experience of working with some European banks that have developed a longer-term approach to finance that factors in climate risk. Westpac has had the opportunity to look at the methodologies these banks are using to examine their own portfolios.

Two examples that have been relevant to banks in Australia both relate to European banks working to develop a better understanding of the environmental impact of their balance sheets.

One is ING’s ‘Terra’ approach, which deploys an innovative means of measuring the climate impact of the sectors in the bank’s loan book that are responsible for most greenhouse gas emissions: power generation, fossil fuels, automotive, shipping, aviation, steel, cement, residential mortgages and commercial real estate. ING has rolled out Terra on the basis that it wants more entities in the financial sector collaborating and improving data quality to drive greater change.

The other is Natixis’s ‘green weighting factor’. The bank’s representatives visited Australia within weeks of the September 2019 launch of this initiative to spread the word about how Natixis is attempting to monitor and manage the climate impact of its whole balance sheet.

“The work itself is really interesting but what’s almost more encouraging is the openness these banks are displaying around sharing their methodologies,” Toohill comments. “They have taken the view that leadership is about sharing what they do and supporting more banks to progress.”

Bringing customers along on the ESG journey

Banks’ drive to incorporate environmental, social and governance (ESG) factors in their strategies and day-to-day operations is accompanied by a desire to help their customers’ ESG journeys. For the most part, this means facilitating transition rather than outright divestment.

“Our view is that any bank that is quite practised in sustainability has an important role in supporting customers to develop their transition strategies, and to work with customers to use sustainable finance to achieve these outcomes,” says Siobhan Toohill, group head of sustainability at Westpac Banking Corporation (Westpac).

This may mean withdrawing support for certain industries or sectors. For example, Westpac cannot see an acceptable transition path for tobacco to achieve a better sustainability outcome so it no longer lends to tobacco companies.

On the other hand, the bank is much more focused on working with companies to incentivise positive transition when it comes to climate change and risk. It has prioritised working with companies that have significant carbon exposure to progress towards a positive transition trajectory.

Australia’s contribution

European banks are the acknowledged market leader in environmental transition in particular. But this does not mean the Australian banking sector can only be a follower. The social component of the ESG universe is notably underdeveloped and Toohill believes the opportunity exists for Australia to take global leadership in this area.

To take just one example, the social-bond market is tiny compared with green-bond issuance. Environmental Finance data indicate that global green-bond issuance reached around US$170 billion equivalent in 2018, while there was less than US$15 billion equivalent of social-bond volume. Sustainability bonds – which combine environmental and social projects – added US$18 billion equivalent to the total.

One of the biggest reasons for the limited supply of social bonds is the relative complexity of measuring and assessing social outcomes. In the environmental space, it is relatively easy to measure reduced emissions once a baseline standard has been agreed. The same cannot be said for social projects.

Toohill says one of the goals of the Australian Sustainable Finance Initiative (ASFI), which was launched in March 2019 (see p34), is to provide leadership on social impact assessment. Toohill notes that ASFI’s co-chair, Jacki Johnson, has said the EU taxonomy is focused on green and climate factors. Australia is somewhat behind the curve in developing a green or climate taxonomy, Toohill acknowledges – but it can make a lead contribution on adding social-impact dimensions to its taxonomy.

“The whole world is still learning how to quantify, measure and set standards around social impact,” she says. “It’s really significant that Australia is having this conversation and looking to how to build its taxonomy across the SDGs and not just focus on climate.”

It is, of course, also critical to have positive impacts to measure. Westpac itself has done a lot of work in the past year in the area of customer vulnerability. The bank has established a customer vulnerability position statement and action plan to set out its approach to providing support to customers experiencing vulnerability. This includes customers who are experiencing domestic violence or elder abuse, or who have fallen victim to scams.

Westpac now has specialist teams across different parts of the organisation to support bankers with complex customer queries. This includes a dedicated Priority Assist line staffed by specialists where customers experiencing vulnerability can access dedicated support and have their issues dealt with appropriately and – just as importantly – promptly.

Toohill explains: “We have uncovered that with vulnerability comes complex claims that can get stuck in the system. We are trying to flip this on its head, to make sure these people are assessed and supported and we can close out their complaints as quickly as we can. To do this we have people who have specialist training to assist people experiencing vulnerability.”

Westpac has also introduced a substantive focus on indigenous customers, particularly those in remote areas. Initiatives introduced over the past year include pop-up branches in remote locations.“Members of some communities in remote areas rarely make it into a town, they may not have access to cars, they can have problems around identification and verification, and even a mobile phone might be shared by various people,” Toohill explains.

“By taking a pop-up branch into remote areas, we are able to offer banking services and also improve people’s financial capabilities by having conversations in the moment around banking basics. While this might seem quite a small offering, the impact can be incredibly significant.”

Also in the past year, Westpac has set up dedicated customer support teams for indigenous Australians living in remote areas. These customers can now ring a dedicated number and access a specialist team to assist them with their banking needs. The teams are tuned in to the specific types of requirements these customers have, Toohill explains. They will often use a local language and they understand that phones might be shared. The goal is to support these customers in a timely and culturally appropriate way.

“This is one of the things I am most proud of being associated with during 2019. It’s the simple things – like helping customers reset pin numbers and checking that customers have the right bank account for their needs – that are having a very profound effect,” Toohill comments.

Unique challenges

The nature of Australian banks’ business models also gives them a slightly different perspective from some of the global ESG leaders. “The Australian banks have a particular a focus on social issues, including financial capability,” Toohill suggests.

This feeds back into the theme of international collaboration between banks. For example, UK banks also tend to have a focus on customer vulnerability and, according to Toohill, there was significant engagement on the topic between the Australian and UK banks during 2019.

There can be little doubt that the collaborative approach will become even more crucial as the time horizons for a massive increase in action around climate change in particular shrink.

Toohill notes the progress global banks have already made on sustainability product development – including, on Westpac’s part, the work the bank did in 2018 on green deposits, which was a world first. In November 2018, Westpac launched a green tailored deposit certified by the Climate Bonds Initiative. It is designed for investors who want investments that genuinely contribute to addressing climate change.

The pace of work on transition is accelerating. Westpac issued its most recent climate-change position statement in 2017 and is due to update this in 2020.

“The more we learn, the more we strengthen our approach,” Toohill claims. “As we collaborate more, understand more and undertake more research, the more action we’re taking towards the ambitions of the Paris Agreement and the SDGs – not only about managing the risks, but also in new financing opportunities. I am already seeing an acceleration in engagement rippling through the finance sector globally.”

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news