Mutual sector primer

Mutual banks are soundly capitalised but lack of market access may be holding up their growth aspirations. Only a handful are active in debt capital markets.

After the Council of Financial Regulators announced its intent to adjust the timing of regulatory measures for authorised deposit-taking institutions (ADIs) on 17 March, Michael Lawrence, Sydney-based chief executive at the Customer Owned Banking Association (COBA), said the mutual sector was in a strong position to cope with the disruption from COVID-19.

The sector is well capitalised, he noted, with an average capital ratio of 17 per cent – substantially higher than the “unquestionably strong” benchmark of 10.5 per cent the Australian Prudential Regulatory Authority (APRA) announced in 2017.

Mutuals also have an average liquidity ratio of 16 per cent, compared with APRA’s minimum of 9 per cent for liquidity holdings.

The number of mutual and customer-owned banking institutions in Australia has been declining for a long time – almost halving to 66 in the decade ending December 2019, APRA states. The sector’s combined assets are A$129 billion (US$79.3 billion), which pales in comparison with the major banks’ combined asset value of A$3.7 trillion.

The sector did, however, receive a boost from recent negative publicity for the majors. The final report of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry was released on 4 February 2019. The headline-grabbing admissions throughout the inquiry lured some major-bank customers to switch to the mutual sector.

Indeed, growth data from 2019 shows the mutual sector outstripping the majors by a substantial amount across three key categories, for a total asset growth differential of 9.4 per cent.

But the mutual sector has not made much headway with increasing its overall market share in the wake of the royal commission. APRA’s statistics show mutuals’ portion of the market in their core residential mortgage business was 4.5 per cent as of 31 December 2019, up just slightly from 4.4 per cent in December 2018 and 4.2 per cent in December 2017.

Moreover, the share of deposits the mutuals sector holds was 3.5 per cent as of 31 December 2019, unchanged from December 2018 and only 0.1 percentage points higher than in December 2017.

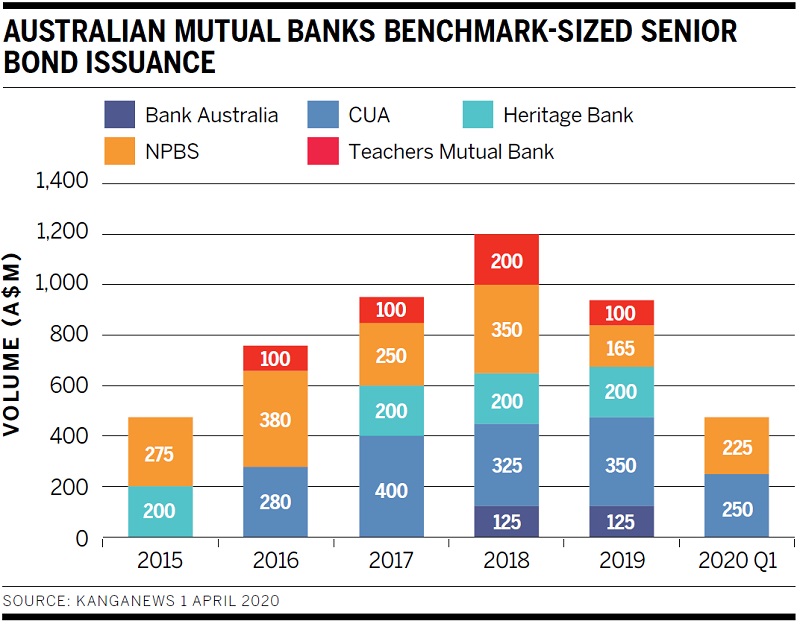

Accordingly, not many institutions are capital-markets relevant. Only Bank Australia, Credit Union Australia (CUA), Heritage Bank (Heritage), Newcastle Permanent Building Society (NPBS) and Teachers Mutual Bank have issued benchmark-sized senior deals in the past five years (see chart).

Beyond Bank, IMB, P&N Bank and People’s Choice Credit Union (PCCU) are the only other sector issuers of benchmark size to feature in debt capital markets, all of them having issued securitisation deals.