Investor survey: uncertainty reigns

Fitch Ratings and KangaNews have been conducting the Fixed-Income Investor Survey since the first half of 2014. The 2020 iteration combines a deeply negative outlook with vast areas of uncertainty to produce the survey’s most worrying set of data ever.

By Helen Craig and Laurence Davison

In the rapidly changing environment of the COVID-19 crisis, timing is everything. The 2020 investor survey was conducted 2-20 March, just as the virus’s impact and measures to stop it were ramping up – seemingly by the hour.

This unusually febrile period undoubtedly had an impact on the survey responses. For instance, investors who responded toward the beginning of the period might not yet have fully processed the enormity of the situation and the economic consequences of a protracted period of social distancing. Projecting outcomes would have been uniquely challenging during the whole survey period.

The survey response rate dropped somewhat on 2019 levels, no doubt due to the extreme nature of market circumstances. Having approached 50 responses in some recent iterations, the number of investors filling in the 2020 survey was closer to 30. The responses still represent the bulk of institutional fixed-income funds under management in Australia.

The results provide a fascinating and illuminating portrait of a market coming to terms with a massive negative shock but perhaps without its impact yet fully priced in. Some of the data may be inconclusive, but the clear expectation is for severely weaker conditions across the economy and markets. The silver lining is that investors have started to see signs of real value in credit spreads – arguably for the first time in years.

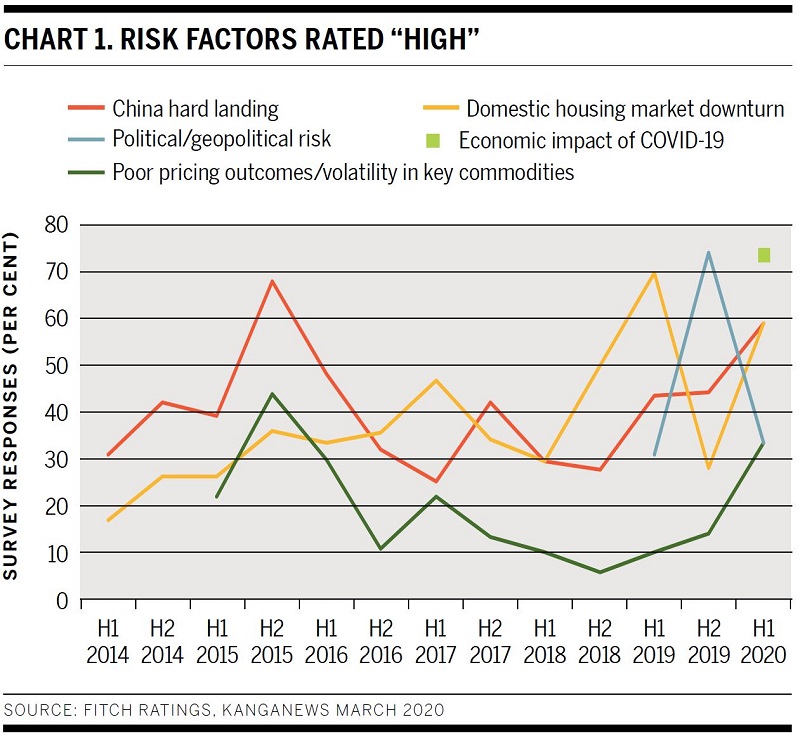

Unsurprisingly, the ramifications of COVID-19 are, by some distance, the biggest risk factor investors identified (see chart 1). There is also growing concern about the Australian housing market and the potential for a downturn in China; COVID-19 is probably a significant driver of these concerns, too.

This concern is no surprise. By mid-April, Fitch was forecasting global growth of negative 1.9 per cent for 2020. Its analysts write: “The global health crisis sparked by the outbreak of COVID-19 is taking an extraordinarily heavy toll on the world economy. Global GDP is falling and, for all intents and purposes, we are in global recession territory.”

In response to the survey results, Fitch says: “Domestically, the COVID-19 outbreak has dented consumer sentiment, which was already on a downward trend in 2019 against a backdrop of elevated debt and muted real-income growth. The spread of the virus will hit consumer spending as people self-isolate. The Australian economy is also being challenged by the pandemic fallout through its trade linkages with China and exposure to commodity exports.”

As well as gobal growth contraction in 2020, Fitch forecasts the Australian economy to contract by 2.2 per cent and Chinese growth to fall below 2 per cent.

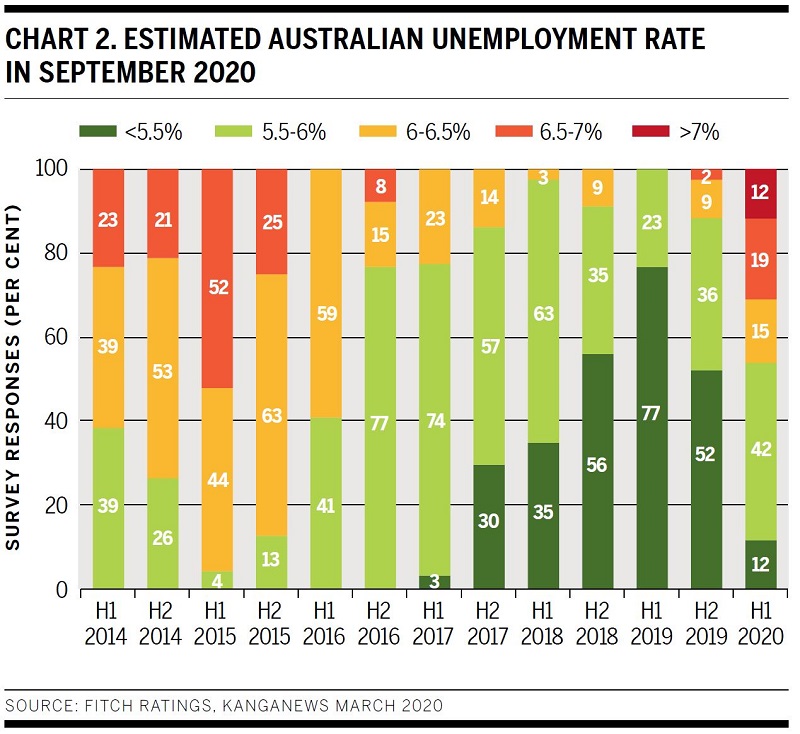

A sign that the survey was conducted during an earlier phase of the ramping up of social distancing is investors’ unemployment outlook (see chart 2). The full impact of business closures may not yet have been factored into investors’ thinking by mid-March.

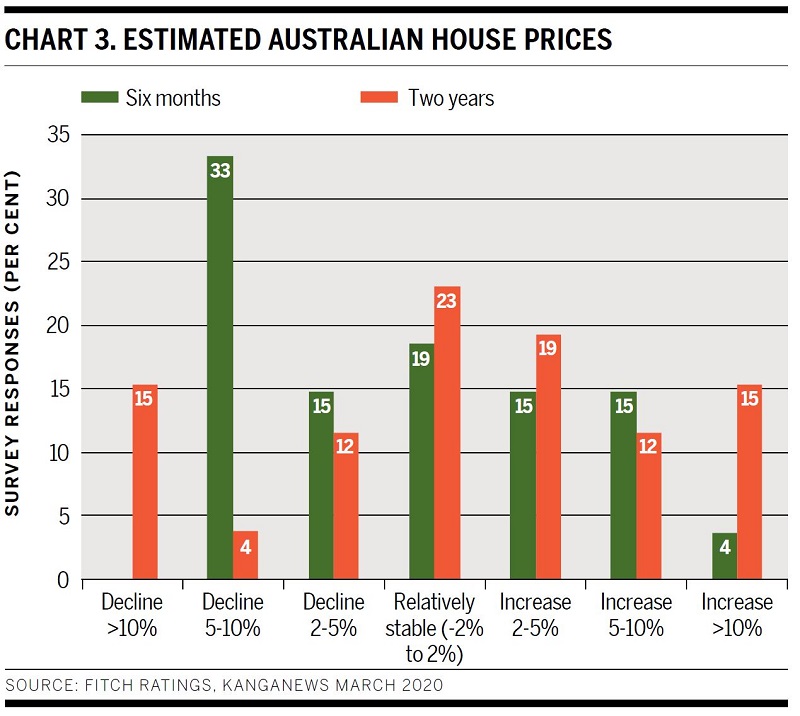

The outlook on house prices tells a slightly different story. Here, investors are relatively sure of a sharp decline in prices over the course of 2020 (see chart 3). In contrast, there is a wide disparity of views on the longer-term outlook. As many investors – 15 per cent of respondents – expect a hard rebound as the proportion forecasting a protracted house-price decline.

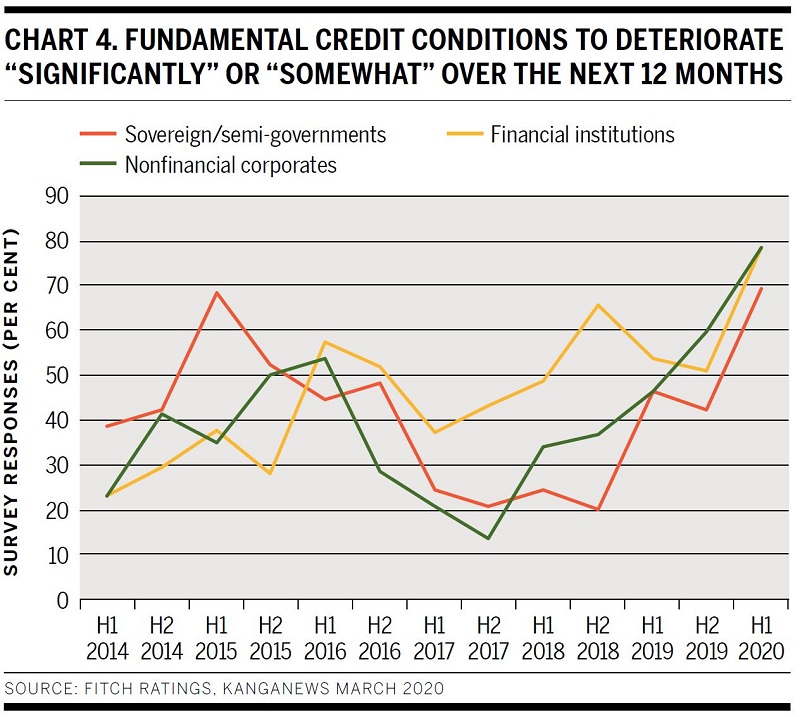

There is a clear consensus that credit conditions are going to be tighter and weaker. Expectations of such deterioration are at a record high for the government sector, financial institutions (FIs) and nonfinancial corporates. About 80 per cent of investors anticipate weaker conditions for credit issuers (see chart 4).

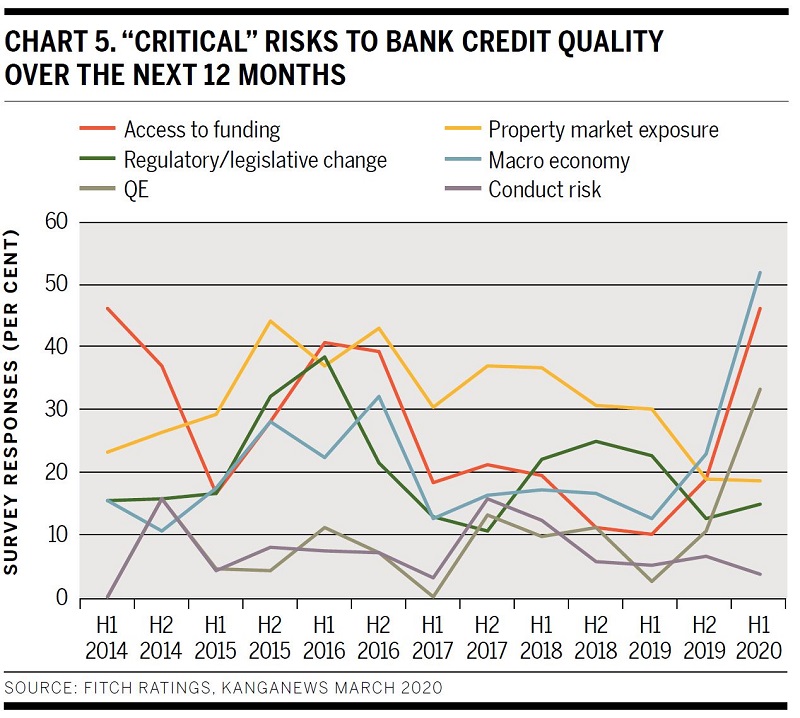

Investors are increasingly concerned about the impact of economic conditions on banks and the potential for a funding squeeze. More than half the survey respondents say the economic situation is a “critical” risk to bank credit quality over the next 12 months, and more than 40 per cent highlight access to funding as a critical risk (see chart 5).

Fitch downgraded the big-four Australian banks, to A+ with negative outlook, on 7 April. Its analysts say the majors remain “adequately capitalised” with “sufficient liquidity to weather the disruption, at least in the short term”.

The pandemic will pressure the operating environment for Australian banks, particularly with asset quality and earnings. Fitch’s base case is for a sharp economic contraction in H1 2020, with a modest recovery beginning in H2. Unemployment is likely to remain elevated relative to pre-pandemic levels.

Significant government and bank support should assist business and household borrowers. Nevertheless, Fitch expects a portion of businesses will not resume after lockdowns end and many households will be unable to resume repayments when loan holidays finish. This will drive impairment charges higher at the same time as lower interest rates pressure net interest margins, while credit growth is likely to remain low.

The banks are generally well capitalised, which will help to offset some of these risks – although there remains a substantial downside threat to Fitch’s base case.

In funding markets, the Reserve Bank of Australia announced its term funding facility (TFF) for banks on 19 March – right at the end of the Fitch-KangaNews survey period. It is possible knowledge of this facility may have reduced investors’ concern about access to funding.

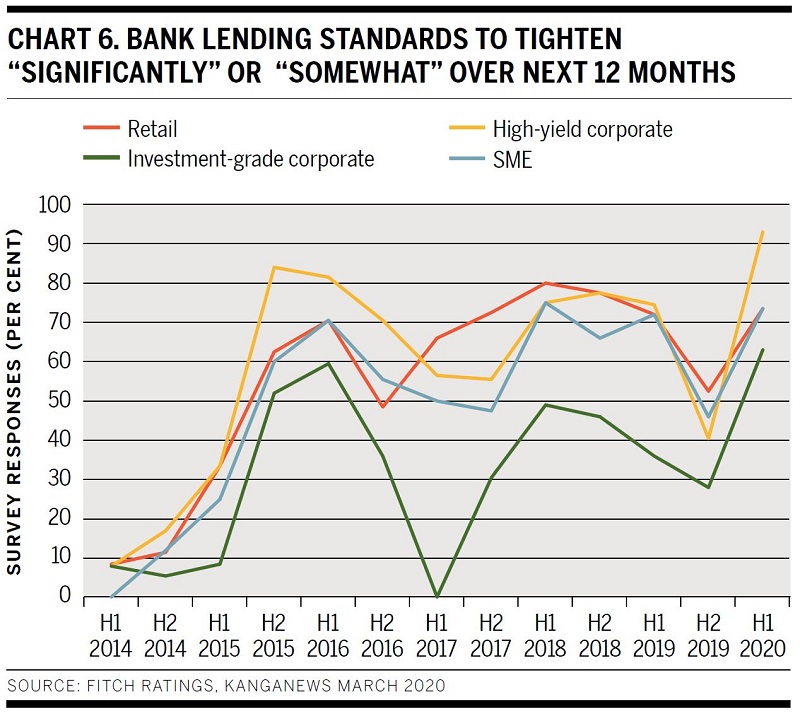

The purpose of the TFF is to free up credit for businesses and households via the banking sector. Again, its existence might have mitigated investor concern about a funding squeeze in the real economy – concern that was clearly elevated during the survey period (see chart 6).

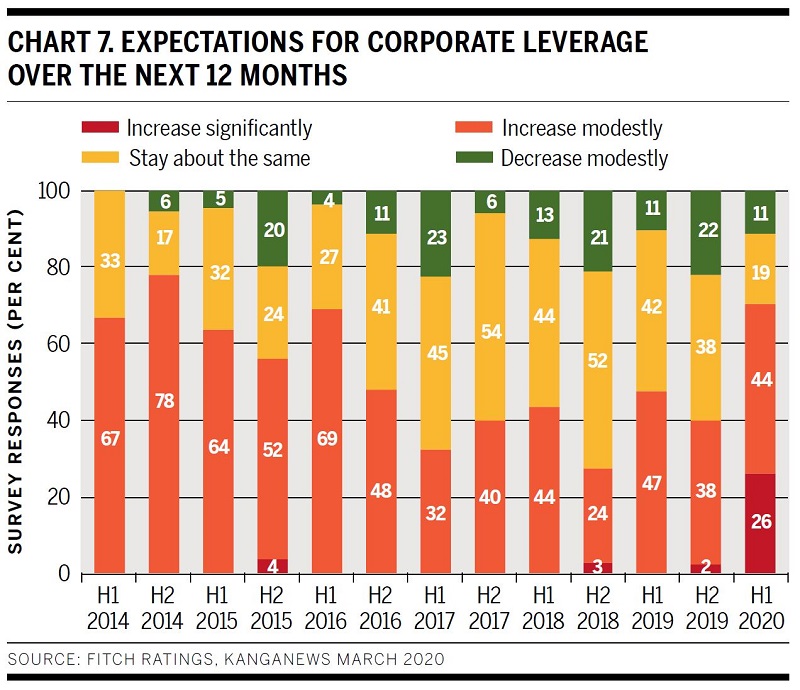

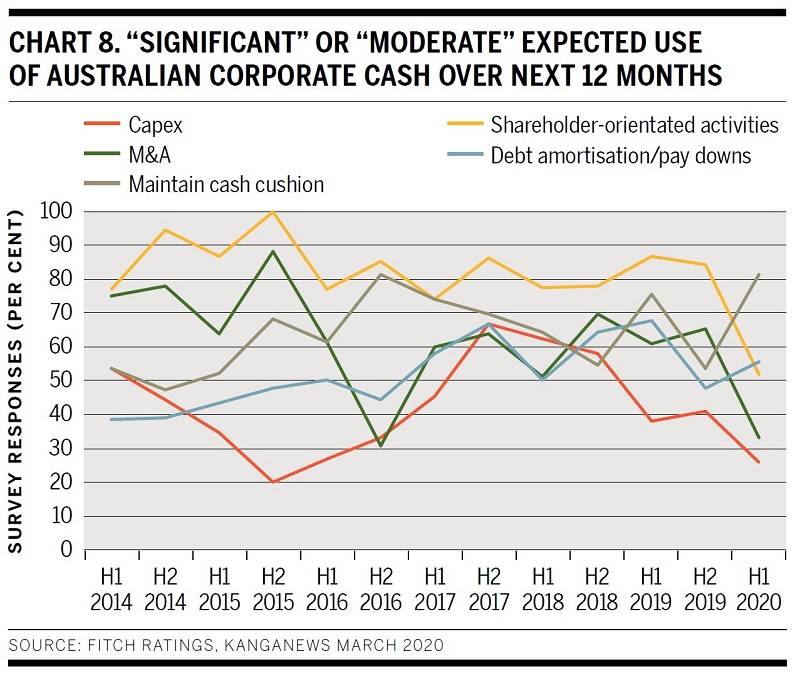

On the other hand, it seems unlikely that any support measures would have significantly changed the investor outlook on corporate Australia’s weakening position. The survey shows a jump in expectations about corporate leverage (see chart 7) that is not driven by a positive view on investment – far from it. To the extent that corporates have cash to deploy in the coming year, fixed-income investors predict maintaining buffers will be the main priority, over investment and even shareholder compensation (see chart 8).

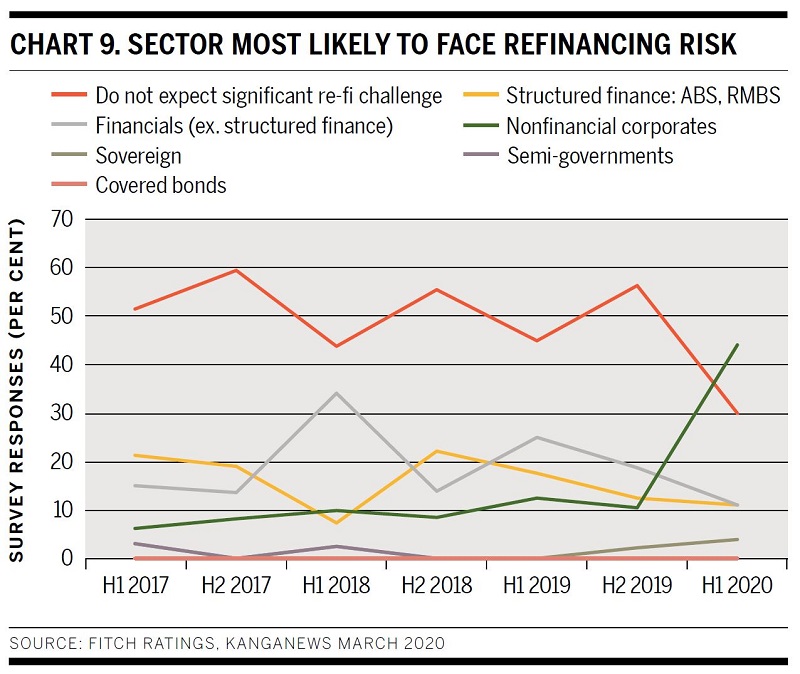

With these factors in mind, investors will probably be keeping a close eye out for any signs of stress in the corporate loan and capital markets. For the first time in the history of the Fitch-KangaNews survey, more investors foresee refinancing problems for a specific sector than predict no significant refinancing issues. The buy side thinks nonfinancial corporates will be the ones in the firing line (see chart 9).

Australian corporate issuers have been all but silent in debt capital markets since the explosion of the COVID-19 crisis, with just two deals printing – both in the euro market. Domestic banks have also been all but silent, and the TFF is likely to keep a lid on issuance by Australian FIs across the globe. The sovereign and semi-government market, meanwhile, has started ramping up to a new phase of issuance growth.

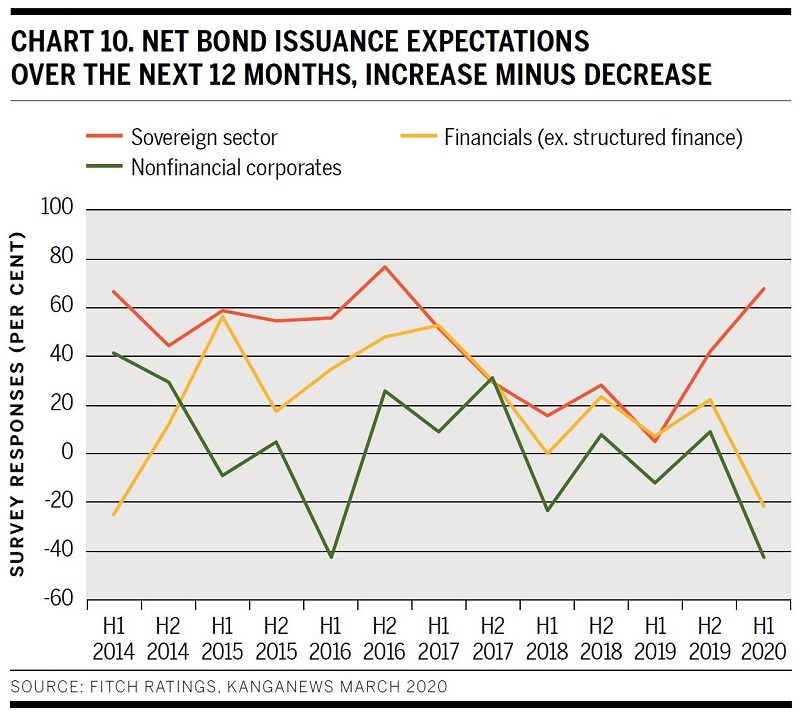

This pattern matches investor expectations. The survey shows a net 60 per cent-plus of fund managers expect growth in issuance from the government sector, while expectations around FI and corporate issuance are both in negative territory (see chart 10).

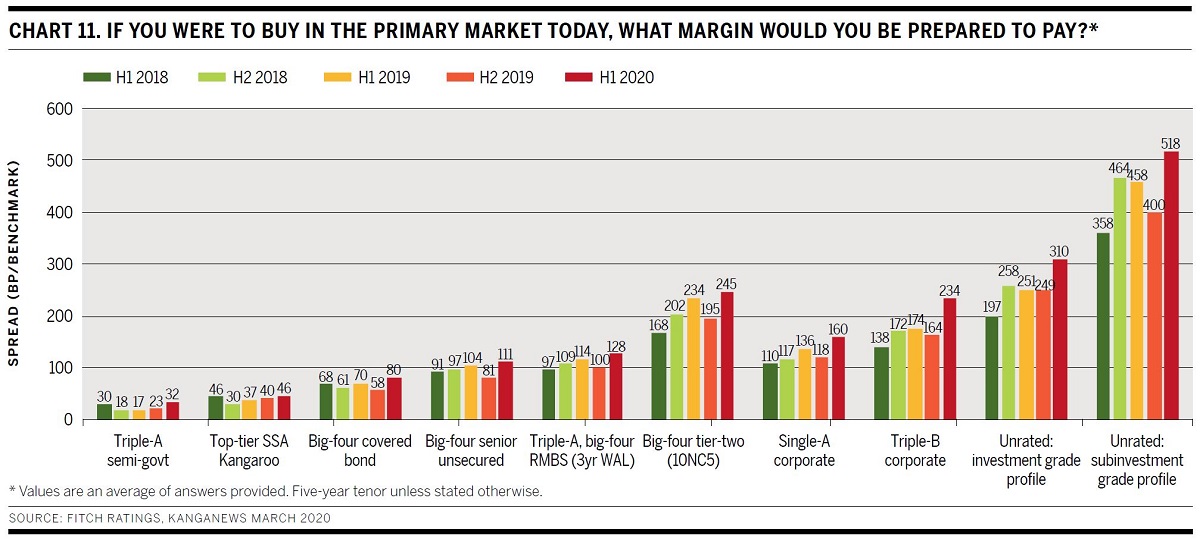

When it comes to investors’ own participation in markets, the spreads fund managers say they would be willing to pay for various debt asset classes have gone up across the board – though arguably not massively (see chart 11).

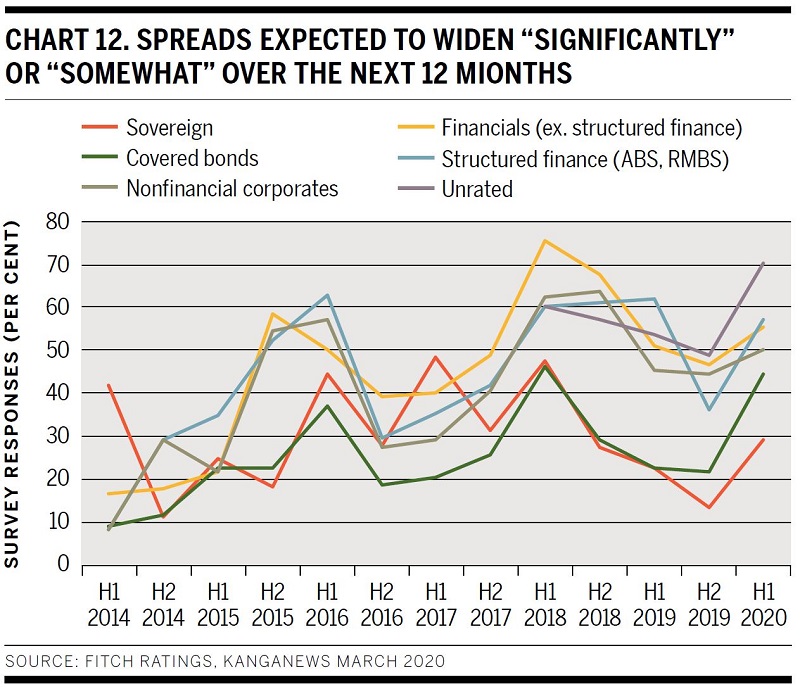

Most investors forecast further spread widening in all credit asset classes. Even the proportion anticipating cheaper sovereign debt and covered bonds grew significantly from the survey conducted in the second half of 2019 (see chart 12).

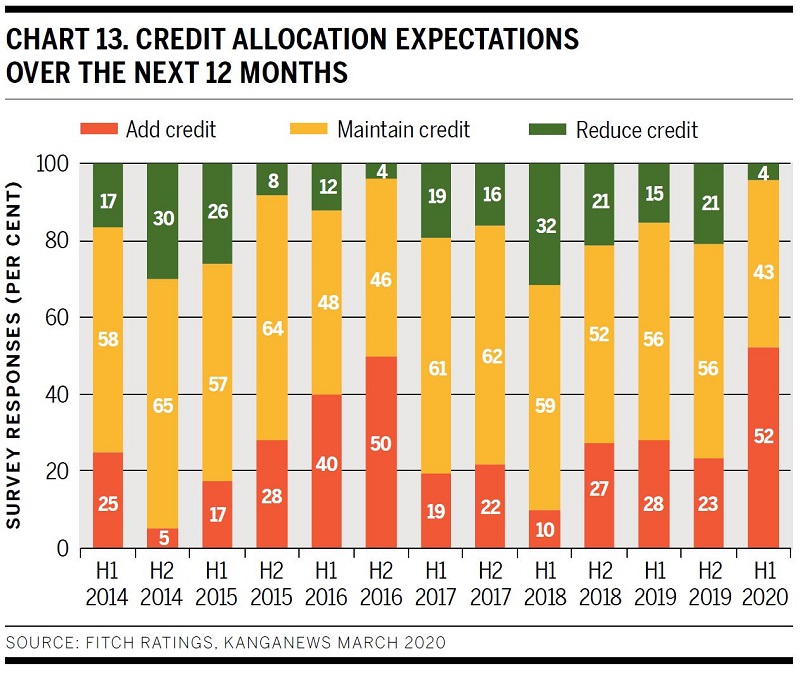

The most positive news from the survey is that investors appear to believe buying opportunities will emerge on the back of a wide-ranging repricing. At 52 per cent, the proportion of investors expecting to add credit in the coming 12 months is a record for the Fitch-KangaNews survey (see chart 13).

Sponsored by

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

Related news