Competition at risk as fintech lenders potentially slip through the cracks

COVID-19 has thrown up challenges even for the most established capital markets borrowers. The crisis is particularly acute for newer financial institutions with shorter track records and smaller asset books. Government support should help, but a protracted downturn could make survival of the fittest a best-case scenario.

In recent years the fintech lending sector has been championed for its technological innovation and for the competitive challenge its advocates claim it will bring to the lending market. Unencumbered by legacy systems and with the ability to focus on narrow lending subsectors, fintech lenders have started to make market-share gains – albeit still at the margin of the overall market.

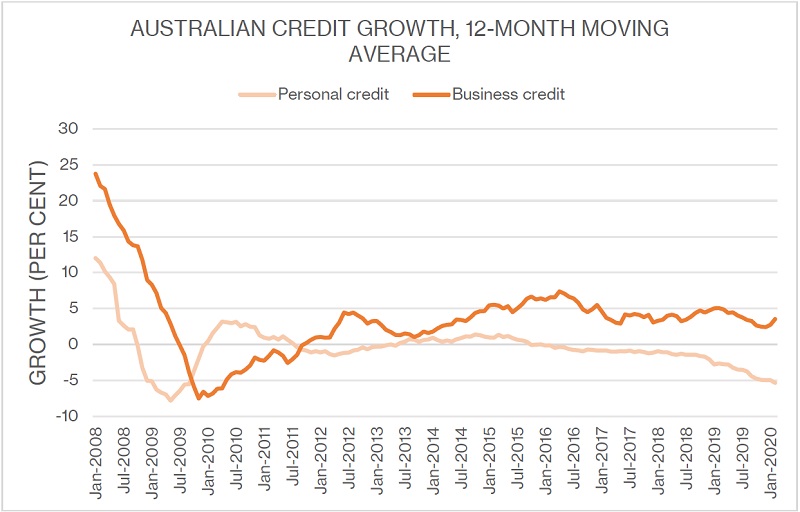

Operating in a challenging environment will not be new to fintech lenders, all of which have come into being in a period of low growth across Australian business and personal credit (see chart).

Having competitive provision of credit, especially in the SME space, may be critical to Australia’s recovery from the COVID-19 crisis. Fintech lenders have created competition in their respective sectors and arguably improved the range of financing options available to small businesses, consumers and households. If many fail during or after the crisis period, the Australian lending landscape could lose competitive challengers before they have had a chance to make their mark.

The timing of the COVID-19 crisis poses specific challenges for many new lenders. Few are cashflow positive and even fewer have the scale or track record to have access to a diverse range of funding options, even in a more conducive market.

Source: Reserve Bank of Australia 29 April 2020

Relatively narrow sources of funding potentially mean less ability to withstand negative changes to operating conditions.

“The fintech lending sector in Australia is developed but relatively immature,” says Daniel Teper, Sydney-based partner, corporate finance advisory at KPMG. “Owners and shareholders have historically been hesitant to dilute themselves too early so many only have capital that will last 6-12 months. Meanwhile their cash burn rate has likely increased.”

Several government stimulus programmes have been designed to help lenders bridge the gap between the onset of the crisis and the economic recovery, Lenders welcome these while saying eligibility problems may hinder their efficacy (see box).

Some observers believe any winnowing of the fintech field may be no more than the acceleration of a natural selection process that would likely have happened anyway. But others say the survival of a healthy group of new lenders will be important for the future state of competition in Australian lending.

Government support lauded but not the whole solution

The Australian government has moved to provide support for businesses and borrowers – both of which could assist the fintech lender sector. Market users welcome the government programmes but say they cannot be the whole answer.

The government stimulus includes measures designed to protect consumers – JobSeeker and JobKeeper. These should help put a ceiling on the eventual peak in arrears and are also potentially available to fintechs themselves to bolster cash flow. Regulators have also moved to shield the creditworthiness of lenders from arrears related to COVID-19 hardship.

Meanwhile, Australia’s securitisation market has flickered with the help of Australian Office of Financial Management’s structured finance support fund (SFSF) but it is unclear how much support this will . Therefore, nonbanks reliant on warehouse funding may be at the mercy of their banks to extend or expand these.

The government’s response has been substantial, decisive and targeted. It has done a lot to provide support for the financiers of small business and should be congratulated for this.

Pressure points

Fintech lenders have emerged in every sector of lending in Australia. Some seek to fill gaps being left by major banks in personal and SME lending. Others are challenging the banks by lending prime residential mortgages.

Australian fintech lenders have mostly adopted a similar approach to funding that evolves and broadens in line with loan-book growth. This approach starts with venture capital, then adds bank warehouse funding – potentially including specialist debt investor mezzanine funds – and eventually progresses to public securitisation.

Firms are at different points in the funding journey, though. Some – such as Zip Co – have already issued public asset-backed securities deals. Others are yet to reach even the warehouse phase.

There are also contrasting strategies when it comes to seeking authorised deposit-taking institution (ADI) status. A clutch of ‘neobanks’ believe having access to deposit funding, among other benefits, makes entering the regulated arena a worthwhile step. Most are operating as more conventional nonbank entities.

Whatever funding strategy new lenders have adopted, access to funds is clearly harder now than it was before COVID-19. Those that have taken the ADI route have access to deposit funds, but market participants say this space has become much more competitive and is especially challenging for banks without an established lending product on the other side.

For those that have begun lending, the same operational uncertainties exist as with most businesses during the COVID-19 crisis. A massive and sudden rise in unemployment is likely to affect their customers and their asset quality, and therefore their balance sheets.

Funding is naturally harder for entities with a less well-established track record of credit quality. The concern around many fintechs is less about access to funds in the immediate future but how well ballasted they are to withstand a more protracted – or wholly diverted – route to profitability.

“The capacity for any lender to lend is diminished at the moment and net-interest margin, revenue and profitability are all likely to be down. For some this will mean an extended time period to break even. This is a big issue and the question for many will be how long they can continue to operate when their capital does not stretch as far and the credit quality of their loan books, both new and existing, is under pressure,” Teper tells KangaNews.

Being on the right side of the scale chart is likely to be crucial. Cameron Rae, Melbourne-based managing director at Laminar Capital, says lenders which have found a niche and begun building a book of high-margin loans will likely be coming into the crisis in better standing.

The type of lending a fintech is targeting may also have an impact on its resilience. Rae adds, for instance, that lenders trying to compete with the major banks in prime mortgage lending may have to contemplate diversifying their business models. With low overall demand for home loans, the path to profitability for lenders taking this route has likely become much longer.

On the other hand, sector advocates say the credit quality of the prime space could make it a better place to be. Michael Starkey is cofounder and chief operating officer at Athena Home Loans in Sydney, which has quickly built a book of super-prime mortgages in the last 24 months. He says Athena’s focus on high-quality borrowers, strict credit criteria and low-cost digital offering allow it to maintain pricing relevance and credit quality even in a weaker operating environment.

Exactly how challenging the operating environment proves to be for fintech lenders in specific sectors remains to be seen. Sarah Samson, head of securitisation origination at National Australia Bank (NAB) in Melbourne, says early hardship trends are starting to emerge. It appears that buy now, pay later is faring better than traditional personal lending and home loans. This is mainly, Samson says, because the repayment amounts are very low. In residential mortgages, NAB is beginning to see more hardships in nonconforming than in prime lending.

The real impact on credit books is yet to play out, though. Samson adds: “It is what happens at the end of the hardship period, when repayments either return to normal or go into default, that will be the real test for the whole lending industry.”

Traditional avenues

This sums up the nature of the fintech funding challenge. The cloud looming over Australian consumer credit makes access to funds, including in capital markets, especially challenging and costly for lenders with smaller books and limited track record of navigating downturns – doubly so if they are not consistently generating capital through profitable operations.

Options outside government support channels do still exist for fintech lenders, says Teper, though capital raising and debt funding will need to be undertaken at revised volume and pricing ambitions. A few neobanks completed capital raising just prior or while the crisis has been unfolding: 86 400 raised A$34 million in April, Xinja raised over A$400 million in March and Volt Bank brought in A$70 million in January.

Debt investor risk appetite is likely fundamentally altered. Anecdotally, KangaNews has heard that some institutional investors that have held mezzanine notes in warehouses have sought exits and are willing to take a haircut to achieve them.

Starkey tells KangaNews there was a short period at the beginning of the crisis when wholesale funding was closed and Athena slowed its pace of loan origination in this period. However, he says increasing market confidence and the support of the structured finance support fund means funding in these lines is opening up again. As a result, he says Athena is looking to pick up its lending once more.

Samson says NAB is in general seeing good support for fintech lenders from warehouse providers. She adds that positive signalling from the Australian Office of Financial Management around warehouse support for fintech lenders is contributing to a willingness to maintain lines of credit to the industry.

Many fintechs with existing warehouses are likely to have diminished need for further funding at the moment, Samson continues, given the volume of origination is likely to be down. “There is funding out there, but it will come at a risk-adjusted price. All lenders at the moment need to make decisions on how much they are willing to pay to expand their lending and should only be writing the loans that fit a credit appetite which has been revised for the current environment.”

Competition consolidation

While some funding appears to be available, market participants agree that some fintech lenders will not emerge on the other side of the bridge. This will likely create opportunities for established market players to acquire fintechs.

This may always have eventuated and for some it has likely been the end goal all along – although founders stand to sell for much less now than they might have done absent the COVID-19 crisis. Teper tells KangaNews acquisitions are probably not imminent but he reports that some players are getting their ducks in a row in case of opportunities.

An outright failure of a neobank would be noteworthy. No Australian ADI has technically failed since Australian Prudential Regulation Authority (APRA) was formed in 1998. There have been mergers large and small to avoid such a catastrophe, but COVID-19 is an unprecedented crisis and the neobanks, as new market entrants, are especially vulnerable.

Capital raisings will insulate neobanks in the near term but they will need to get lending products off the ground and into the market as soon as possible to minimise cash burn. In the meantime, their number will not increase any time soon. APRA has ceased granting ADI licences for at least six months from April.

Those fintechs that have established a presence in the Australian lending landscape are backing themselves to get through the crisis and even to attract new business. David Hornery, co-chief executive at Judo Bank in Melbourne, says Judo is well capitalised and liquid so the current environment actually presents a growth opportunity.

He says: "It is times like these that true relationship banking really comes to the fore. One thing that is absolutely central to supporting customers is being available and being proactive, which because of our high banker-to-customer ratios we can consistently be. We want to set the bar for what the true relationship banking of small businesses looks like in this country.”

At the consumer end, Zip Co is confident its technology platform stands it in good stead. Peter Gray, Sydney-based co-founfer and chief operating officer at Zip says the investments it has made in its credit and decision-making platforms have led to just 1 per cent of its customers being late with payments – a rate he says is substantially lower than for most credit card receivables.

In prime mortgages, Athena expects to continue to build a strong loan book. “We are set up for digital distribution so we are mitigated from the physical restrictions which might affect lenders dependent on brokers. Our customer acquisition has always been more focused on customers refinancing rather than new lending, so we are also insulated from a downturn in new home loan demand,” says Starkey.

KangaNews is your source for the latest on the COVID-19 pandemic’s impact on Australasian debt capital markets. For complete coverage, click here.