KEC talks funding strategy after Australian dollar debut

After establishing its Australian debt issuance programme in late July, Korea Expressway Corporation (KEC) issued its inaugural Kangaroo transaction on 26 August. The issuer tells KangaNews the deal priced inside its US dollar secondary curve.

The A$450 million (US$331.5 million) transaction was split equally between fixed and floating-rate note tranches. It priced at 72 basis points over swap benchmarks after launching and taking indications of interest at 78-80 and 80-85 basis points area over swap benchmarks having attracted a final book in excess of A$1.05 billion.

Keunwook Kang, senior manager, finance at Korea Expressway, shared deal insights with KagnaNews.

Why did KEC establish an Australian debt issuance programme in Kangaroo format?

One of our key goals was to establish a relationship with, and garner demand from, Australian onshore investors. We believed Kangaroo format to be an optimal choice.

Can you provide an overview of your funding programme and issuance by currency?

The mandate announcement said Korea Expressway was considering 3-5 year tenor for the deal. Why was Korea Expressway looking to execute a deal in the short end of the curve, and why was three-year tenor ultimately chosen? Would you like to return at the longer tenor?

What were your pricing expectations going into the transaction and how did Australian dollar pricing stack up on an international basis?

We achieved arbitrage by swapping the proceeds into Korean Republic won, leveraging the current basis as well as Australian dollar denominated bond-market conditions, given our base funding currency is Korean Republic won.

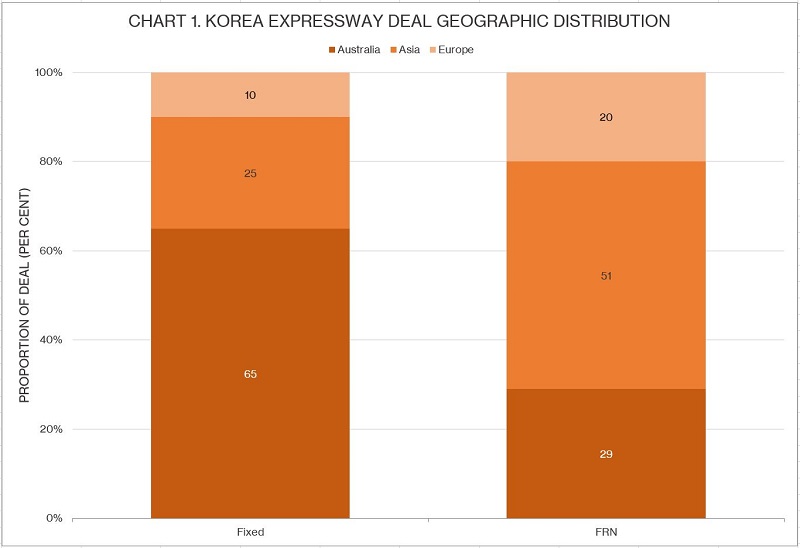

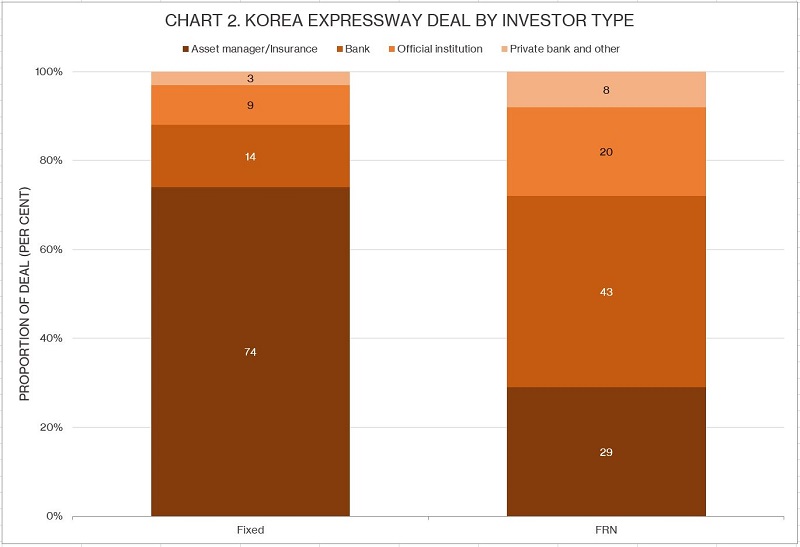

In addition, we’re extremely satisfied with the breadth of investor demand we could accommodate through our three-year fixed and floating dual-tranche formats, as shown by the distribution statistics [see charts 1 and 2].

What about plans for future Kangaroo issuance by Korea Expressway?

Source: Korea Expressway Corporation 31 August 2020

Source: Korea Expressway Corporation 31 August 2020