Leading from the front

European Investment Bank is one of the EU’s primary vehicles for achieving its sustainability goals and is therefore at the vanguard of European and global sustainable debt markets. The supranational tells KangaNews it aims to use this position to provide a blueprint for itself and others to implement ambitious sustainable-finance strategies.

European Investment Bank (EIB) has been one of the world’s largest financiers of renewable-energy projects for more than a decade. Its climate-awareness bond (CAB) programme, historically allocated to these projects, has grown in tandem with this role.

In 2018, EIB added the sustainability-awareness bond (SAB) programme to its suite of products, broadening the pool of assets that may receive allocations from issuance of dedicated bonds as its sustainability financing expands beyond climate action.

The EU’s bank is ramping up its commitments to funding transition to a low-carbon, resilient economy in conjunction with the increasing urgency of the task and escalating European government commitments to meeting it.

In November 2019, EIB announced a four-pronged approach including aligning all financing with Paris Agreement targets by the end of 2020, the phase-out of new unabated fossil-fuel industry lending by the end of 2021, increasing the share of new EIB lending to climate and environmental outcomes, and mobilising €1 trillion (US$1.2 trillion) for climate and environmental purposes by 2030.

In November 2020, EIB’s board of directors approved the Climate Bank Roadmap 2021-25, which enshrines these commitments in bank operations with a focus on accelerating transition, ensuring a just transition, supporting Paris Agreement-aligned operations and building strategic coherence and accountability.

Dominika Rosolowska, sustainability funding officer at EIB in Luxembourg, says the commitments and roadmap are indicative of the EU’s desire for EIB to strengthen its role as the union’s climate bank, putting the supranational at the forefront of sustainable finance in a region that is widely acknowledged as the global leader in the field.

“EIB has been asked to reinforce its role as a financier for climate and sustainability outcomes in the context of the European green deal. While we have already built vast expertise and experience in this area, it has now become increasingly relevant with the EU’s focus on transition and the introduction of the EU taxonomy,” she explains.

IMPLEMENTING AMBITION

Making bold commitments is just the first step in the process. The rubber hits the road in the bank’s lending activities, but its funding book is increasingly aligned with the task at hand, too.

This is where the EU’s taxonomy for sustainable activities comes into play. It codifies a range of environmental, social and sustainability objectives, activities and technical screening criteria. This is designed to help market participants understand if the activities underlying investments are sustainable – and why.

EIB contributed to various expert groups in the development of the EU taxonomy, including the high-level expert group on sustainable finance, the technical expert group on sustainable finance and the current EU platform on sustainable finance.

Rosolowska says, as the EU’s bank, EIB follows guidance from the EU and is therefore bound to align its activities with the taxonomy. “In practice, this means we need to apply the taxonomy lens in the first instance to our lending – to look at how we can align definitions and measurement criteria for projects with the definitions of the taxonomy.”

This alignment will be reflected on EIB’s funding side through eligibility criteria for use of proceeds of the CAB and SAB programmes. EIB has been issuing CABs since 2007 to link funding to the lending it provides for climate-change mitigation. It has been issuing SABs to link funding to its lending for other environmental and social objectives.

The SAB programme launched in 2018 but only included water-related projects at the time. In 2019, the programme expanded to health and education, and in 2020 the health component further broadened to include emergency-response measures – which EIB has been prominent in providing during the COVID-19 pandemic.

Rosolowska explains: “This is possible because the documentation we devised for the bonds is like a shell, to which we can add components as long as they are devised in line with the EU taxonomy or, where the taxonomy is not yet available, with its structure and logic. We need to identify an objective, the economic activity that contributes to it and the technical screening criteria used to assess the substantiality of the contribution to the objective.”

EIB intends to continue mapping its lending to the taxonomy including further expanding its CAB- and SAB-eligible asset pools. For SABs, this could include areas like social housing, biodiversity and gender. For CABs, EIB would like to broaden eligibility to cover a larger portion of its climate action financing, Rosolowska reveals.

The implementation of this strategy is a process not an event, she adds, reflecting the schedule for implementation of the EU taxonomy. While the taxonomy regulation entered European law in July 2020, the technical details and screening criteria for assessment of activities and their contribution to objectives are still to be finalised.

On climate, the European Commission is expected to announce legislation by the end of 2020, that will come into force by the end of 2021. Criteria for other environmental objectives are to be implemented at the beginning of 2023. Social objectives are expected to be tackled, too – but at a later date.

Rosolowska says EIB will continue to be at the front line of adapting its lending and funding to the evolving criteria. “Until the technical screening criteria are available, EIB will rely on its project experts to apply the taxonomy lens, structure and intent to its balance sheet and map these to increase the eligible pools for CABs and SABs.”

FUNDING IMPACT

EIB is one of the world’s largest debt capital market funders, with an annual issuance requirement of €60-70 billion. As its lending to climate and other sustainability projects ramps up, it may be able to allocate an increasing portion of this volume to CABs and SABs.

Jorge Grasa, Luxembourg-based funding officer at EIB, says the bank’s approach to funding has not changed despite its greater sustainability commitments. To achieve such a large funding task, EIB needs to be active across all major and many supplementary markets, Grasa confirms. He adds that EIB has an increasing focus on building out CAB and SAB curves in various currencies to sit alongside vanilla curves.

“We want to service investors with specific demand for our CABs and SABs but also to continue providing regular issuance of vanilla bonds to fill investor needs for these. The products are complementary – and they help increase EIB’s presence in markets and diversify its investor base,” Grasa explains.

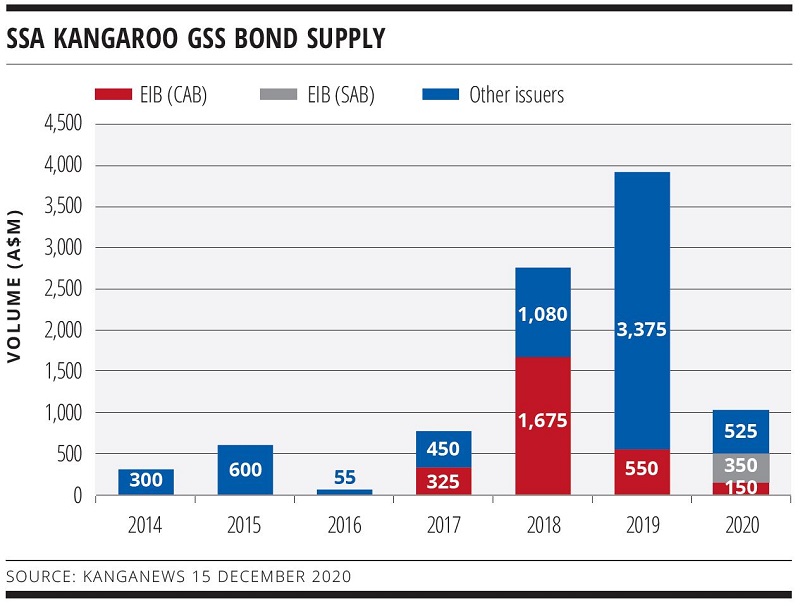

EIB has CABs outstanding in 11 currencies and SABs outstanding in four. Australian dollars became the fourth currency in which EIB issued SABs in May 2020, despite a challenging environment for supranational, sovereign and agency (SSA) borrowers in the Kangaroo market.

As well as unfavourable basis swap economics in the early months of the year, the various government and central-bank actions taken around the world in response to COVID-19 have made issuance for most SSAs more favourable in markets other than Australian dollars for most of 2020.

Even with diminished issuance possibilities EIB has remained one of the pre-eminent SSA Kangaroo issuers of green, social and sustainability (GSS) bonds (see chart). Grasa says EIB appreciates the support of its dealers and investors during a challenging 2020 and is keen to continue its commitment to the Australian dollar market in 2021 and beyond, in its vanilla, CAB and SAB bond curves.

Rosolowska says EIB is encouraged by investors in markets outside Europe buying into its CAB and SAB programmes, thereby subscribing to the robustness of EIB’s sustainability funding, its links to the EU taxonomy and its development of criteria.

She adds that EIB had strong engagement with Australian investors – that have been preparing for the release of a domestic sustainability roadmap – on the development of its CAB and SAB programmes when it undertook a virtual roadshow in the second half of 2020.

“We have been encouraged by the level of Australian investor interest and understanding of what is happening in Europe. There was reciprocity of thinking around sustainability while investors were particularly curious about how the taxonomy can translate into market activity. As more and more jurisdictions seek to classify what is sustainable, we are keen to exchange thoughts and experiences with market participants around the globe,” Rosolowska explains.

Sponsored by

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news