What the buy side wants in ESG

As the sustainable debt market evolves at a quickening pace, the most important factor for issuers to keep abreast of is what investors want from them – what is considered best practice on a transaction basis and as ongoing environmental, social and governance (ESG) commitments. In December, KangaNews polled Australasian investors to ascertain their up-to-the-minute thinking.

Helen Craig Head of Operations KANGANEWS

Laurence Davison Head of Content and Editor KANGANEWS

KangaNews designed the survey with one goal in mind: to uncover information issuers can use to help guide their alignment of debt funding and ESG principles. More than 40 institutional investors responded, covering the Australian and New Zealand institutional fixed-income funds-management community.

As well as the quantitative results, KangaNews spoke to a number of investors to hear their perspectives on the responses and to learn more about the strategic thinking behind contemporary buy-side preferences.

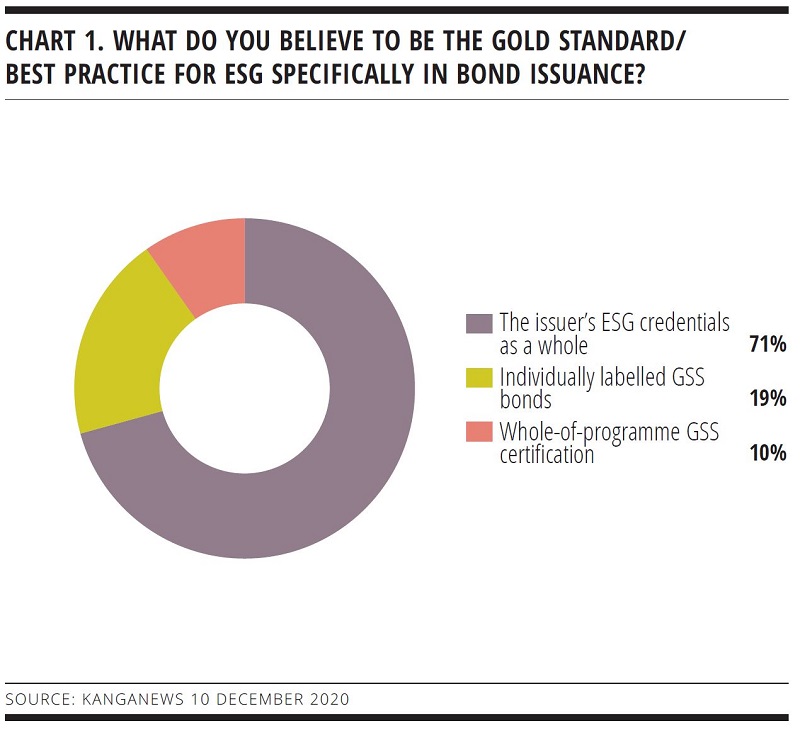

One of the clearest findings from the survey is that investors are more focused on issuers’ ESG behaviour as a whole than on the specifics of debt programmes or securities. More than 70 per cent of survey respondents name issuers’ ESG credentials as a whole as the “gold standard” for ESG in the bond market (see chart 1).

LABELLED BONDS

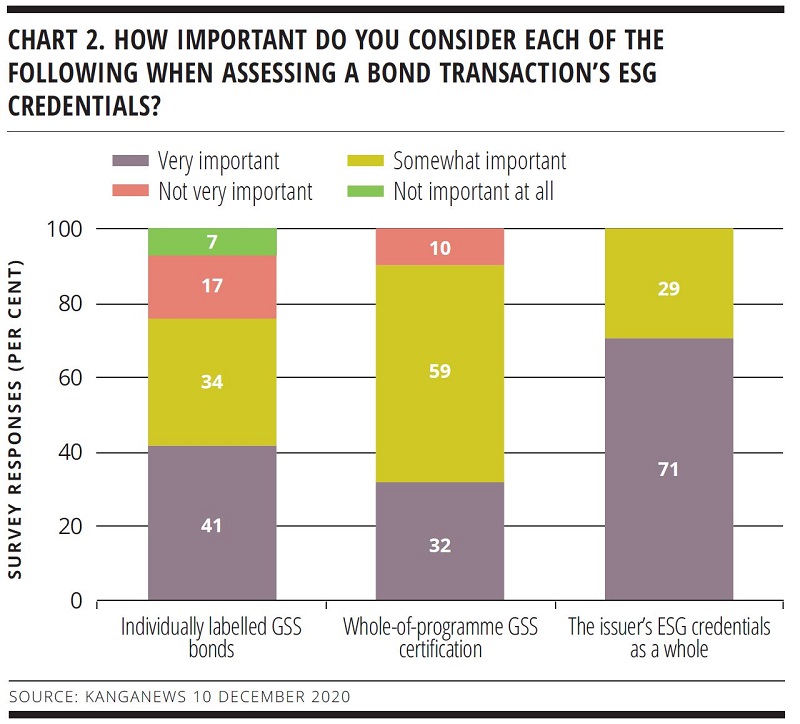

This holds true even when investors are looking at a specific debt transaction. Again, more than 70 per cent list issuer credentials as a very important factor in assessing individual deals – significantly more than place the same importance on security-level or whole-of-programme labelling (see chart 2).

Darren Langer, head of Australian fixed income at Nikko Asset Management in Sydney, comments: “To us, the issuer is the primary concern. The only reason for considering a label is if there is a special purpose for the funds. We can get comfortable if we’re certain the money is ringfenced for a particular project, but what we don’t want is issuers using ESG as a marketing tool.”

More than one investor mentions the potential for greenwashing as a major reason why issuers’ overall credentials are the most important factor in ESG analysis. The view seems to be that labelled green, social and sustainability (GSS) issuance is good as far as it goes, but the rest of the borrower’s assets should be relevant even so.

“The issuer’s ESG credentials as a whole remove any suggestion of greenwashing and cut to the core of what an investor is looking for,” explains Simon Pannett, director and senior credit analyst at Harbour Asset Management in Wellington. “We want to know what an issuer is actually doing and get a good sense of its corporate behaviour more generally. It is more important to know what is behind the label than it is to focus on the label itself.”

In fact, Pannett says Harbour would actually be just as, if not more, concerned about an issuer’s poor ESG behaviour outside the asset pool for a GSS bond even when it has assets suitable for this type of issuance.

Investors also have to keep an eye on their own portfolio-level allocations in a more dynamic way than just holding some labelled bonds. Marayka Ward, Brisbane-based senior credit and ESG manager at QIC, explains that research and guidance from Europe suggests that while it is appropriate for investors to report on the emissions avoided or the impact of GSS bonds they invest in, it is not appropriate to use this to offset the carbon emissions of the rest of their portfolios.

For investors to help clients achieve their Paris Agreement commitments, they need organisations across the portfolio to focus on reducing their overall emissions. For this reason, Ward says she favours the sustainability-linked style of bond – because it makes the targets company-wide.

“This is not to say we don’t see value in labelled bonds,” she continues. “If we have carried out credit work on the company and it has a vanilla bond as well as a green or social bond, like-for-like we probably prefer the labelled bond. We also think there is a technical reason to hold labelled bonds as our research shows they either outperform, or perform in line with, vanilla bonds. But, at the most basic level, the company issuing GSS bonds must pass our credit requirements first.”

This speaks to the wider trend of ESG integration with the credit-risk analysis process, which is becoming more prevalent across the Australian market.

In QIC’s case, the firm’s analysts incorporate ESG considerations into their credit work and ESG transgressions can trigger a decision not to invest – any of environmental, social or governance issues can be the driver of an investment decision. Ward says it would therefore be unusual to find a company with very poor ESG practices from the outset in one of QIC’s investment portfolios.

It is not a set-and-forget screen, either. QIC has a dynamic exclusion list that can come into play if a transitory ESG issue is identified that the firm believes is temporary but needs to be addressed. “This can cause us to put the company on a short-term investment ban – until such time as the issue is addressed,” Ward reveals. “For us, first and foremost, it is the issuer’s own credentials that drive the initial credit assessment.”

ISSUER SECTORS

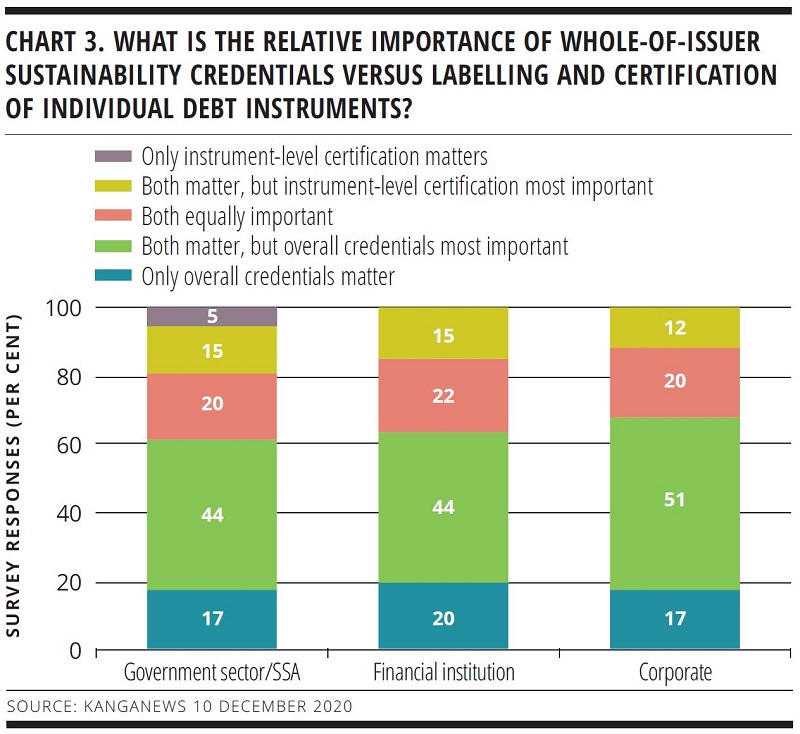

There is also no apparent difference in investors’ preferences by issuer sector. Whether they are looking at a government sector issuer – including supranational, sovereign and agency (SSA) names – a financial institution or a corporate borrower, investors place significantly greater weight on a borrower’s overall credentials than the characteristics of individual deals (see chart 3).

In this case, though, the data may not tell the full story as several investors report that they consider the context of an issuer’s purpose. For instance, Pannett argues that ESG considerations are baked in to “the whole raison d’etre of an SSA”. As a result, he adds: “We prioritise our time and effort where we have greater concerns, which is predominantly industrial corporates.”

Ward adds: “SSAs have a natural advantage in the ESG space because they are predominantly focused on funding the social good. These issuers are therefore the one exception we make when looking at green- or social-bond deals in relation to requiring independent certification.”

It may not be the majority opinion, but at least some investors take this view as far as a conclusion that government-sector issuers would be better issuing on a whole-programme basis than focusing on GSS asset pools.

“While I acknowledge issuers have taken time and effort to create an ESG framework, it is far better if the organisation as a whole seeks to have ESG credentials,” says Terry Yuan, credit analyst at Antares Capital in Sydney. “Rather than packaging up and issuing particular assets it would be better if governments as a whole were to make it clear that it is about all their activities. In my view, this would make more of an impact – and it would make their bonds more attractive.”

MEASURING COMMITMENTS

The KangaNews survey also asked investors for detail on what type of ESG credentials they want issuers to display. There is no universal preference but it is clear that an articulated plan to meet measurable, externally defined targets is crucial.

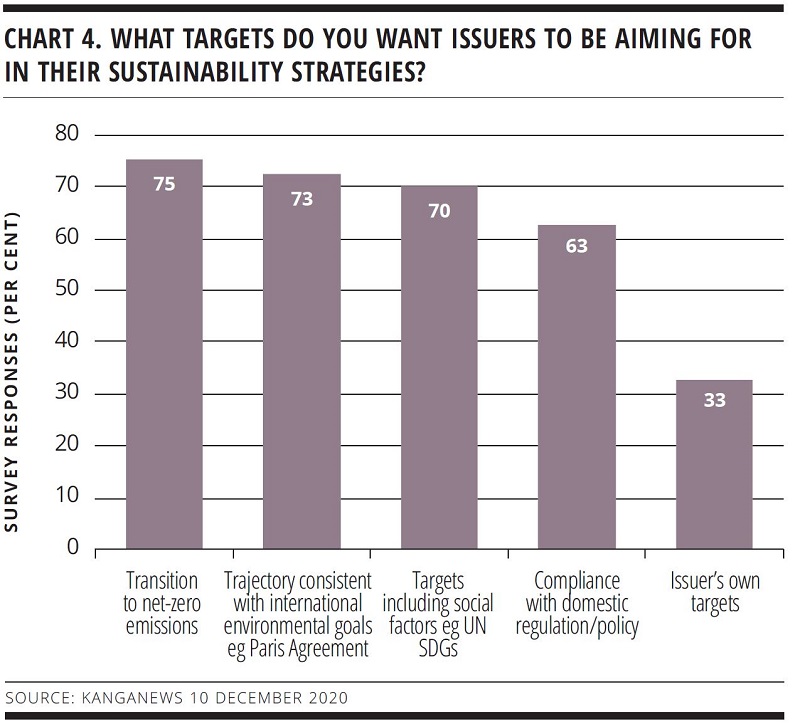

The most commonly named single target is a net-zero emissions transition plan, while meeting international-agreement targets or specific goals with a social component – including the UN Sustainable Development Goals – also features heavily (see chart 4). By contrast, there is relatively little interest in issuers’ self-set targets.

“We want companies to tell us what they are doing and we want as much data as possible,” Langer says. “The more quantitative data the better, because in the end we’re trying to understand whether the company has a policy it is adhering to. This information should be coming through in the annual report but also external standards and reporting.”

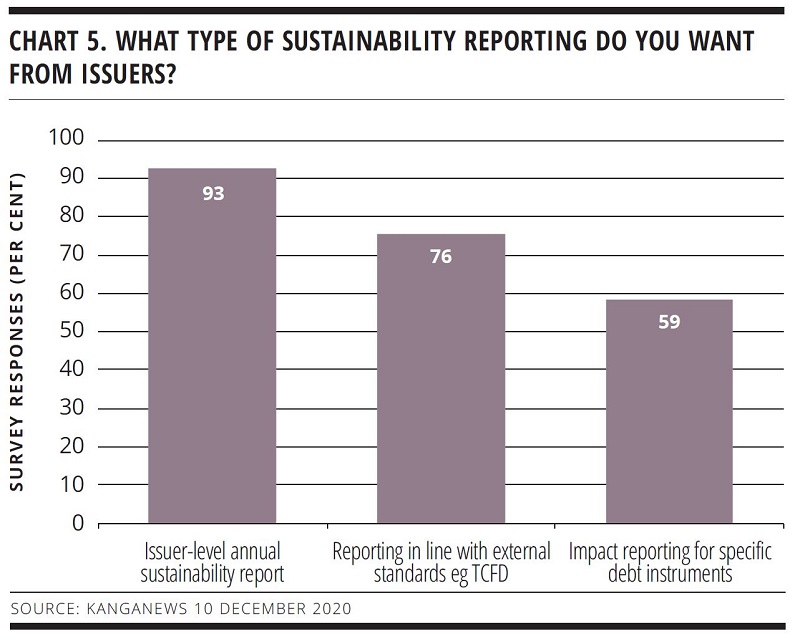

Three-quarters of investors responding to the KangaNews survey agree that reporting in line with external standards – such as the Task Force on Climate-related Financial Disclosures (TCFD) – is desirable. Even more want to see issuers producing annual standalone sustainability reports (see chart 5).

“Our clients want to know about TCFD metrics, modern slavery and a number of other external regulatory requirements they need to comply with,” Ward reveals. “Some countries – including New Zealand, the UK and Switzerland – are mandating TCFD reporting over the next few years. The regulatory environment is driving our response and causing us carefully to consider what our clients are asking us to provide and why.”

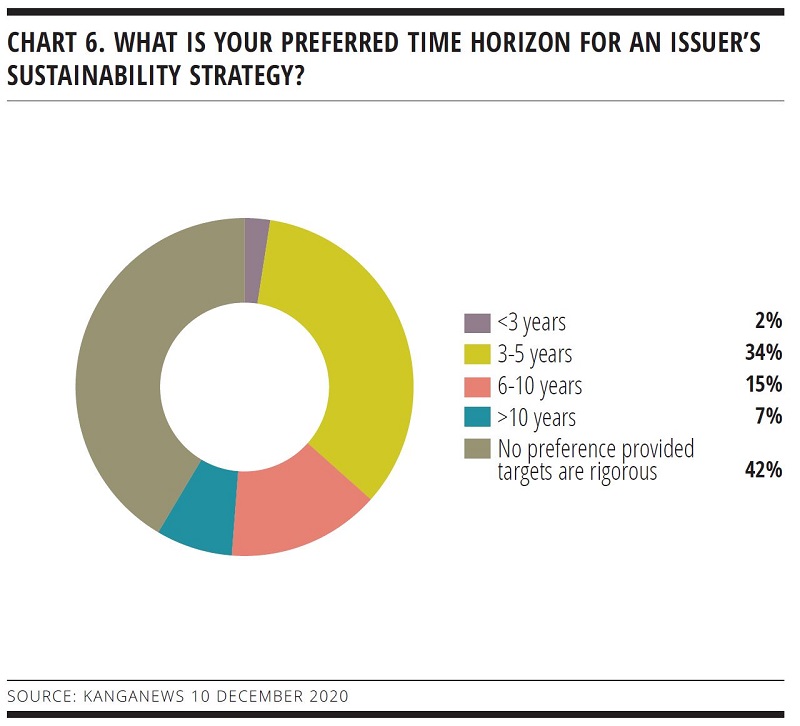

The survey uncovers at least one area where investor views appear to diverge. While the buy side clearly prefers issuers to have rigorous and measurable targets in place, its view on the horizon for achieving them is less uniform. A third of investors responding to the KangaNews survey want issuers to be working to a medium-term horizon, but slightly more say they do not require a timeframe at all “provided targets are rigorous” (see chart 6).

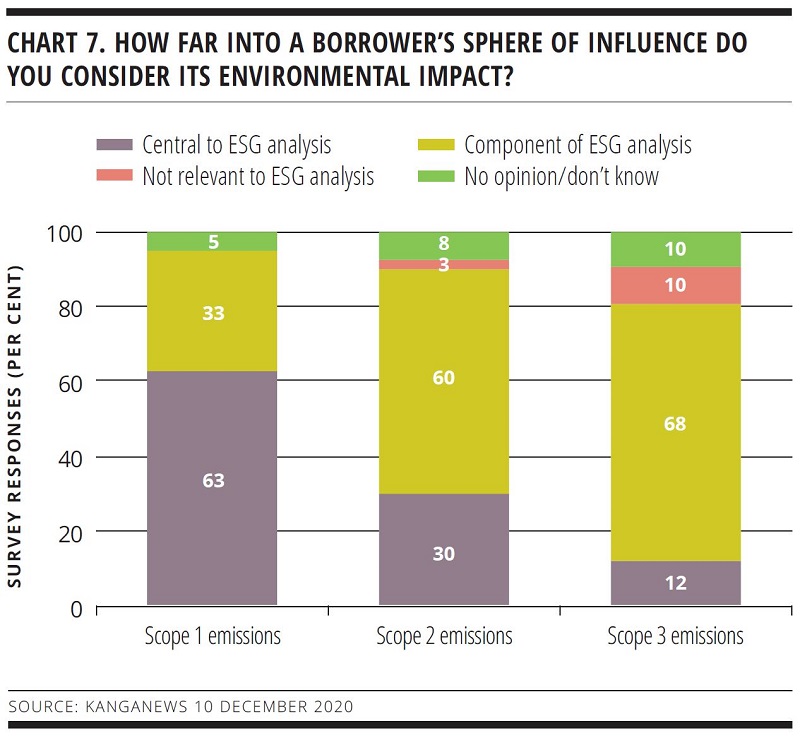

There may be scope for future evolution in this area. The same can be said for investors’ view on sphere of influence. At present, only scope-one emissions – the ones most directly created by an entity, including fuel consumption and company vehicles – are considered “central to ESG analysis” by a majority of investors (see chart 7).

FUTURE EVOLUTION

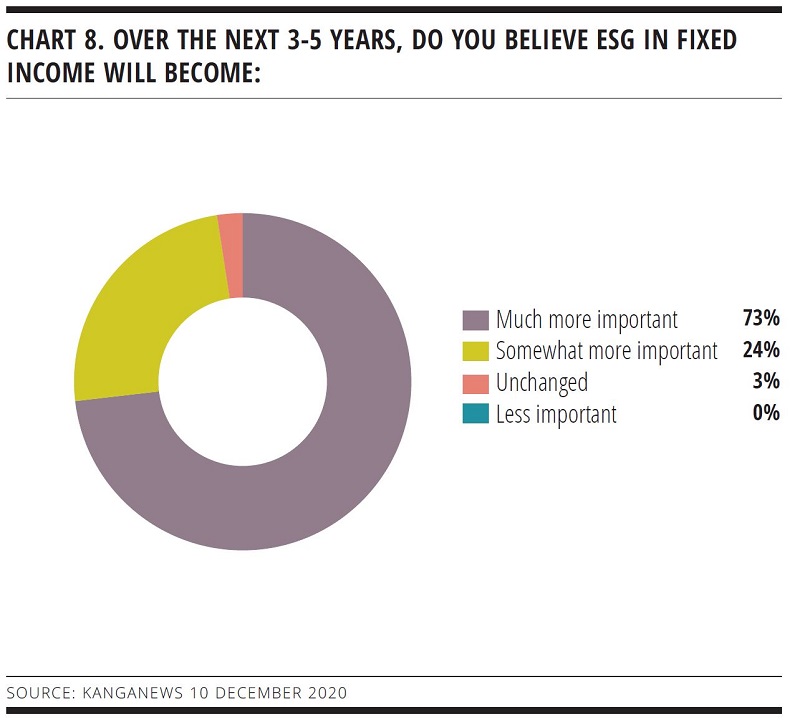

The survey paints a picture of an investor base that is evolving in its understanding and deployment of ESG principles. There is a strong belief that this trend will continue in the future, as nearly three-quarters of survey respondents say ESG will become “much more important” in fixed income over the next 3-5 years (see chart 8).

Yuan suggests ESG integration simply makes sense on the issuer side, as something with both a sound economic rationale and which provides a solid PR benefit. “Companies are aware that the ESG activities they are engaging in could ultimately result in cost savings, as well as boosting employees’ morale and offering reputational enhancement. There is not much down side to adopting ESG policies and actions,” Yuan suggests.

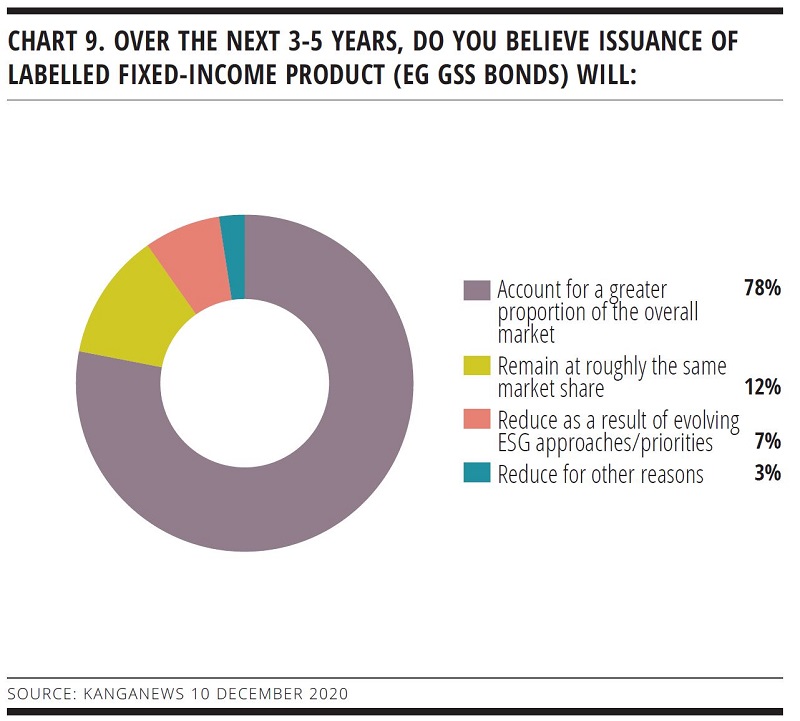

Despite all the talk about whole-of-issuer analysis, investors also still expect a growing role for labelled bonds. More than three-quarters believe this asset class will claim a greater share of the fixed-income market in the medium term – even when asked if evolving investor approaches could marginalise GSS product to at least some extent (see chart 9).

Fund managers seem to believe that the market as a whole may not have progressed as far toward holistic analysis of issuers as they themselves have. For instance, Pannett says: “My view is that the market will continue to favour labelled issuance in the medium term even though my own preference is for a whole-of-issuer approach. However, I think the whole-of-issuer approach will prevail further out along the horizon.”

Ward, meanwhile, suggests that over time the market could bifurcate. High-grade issuers will either issue GSS bonds or stand on their sustainability credentials as a whole, while private-sector issuers may in time migrate to issuance linked to overall sustainability performance.

“If the market can get comfortable with sustainability-linked instruments, this is where I think we’ll see growth in the next few years,” Ward comments. “My view is they will become a very good corporate-wide motivator and address the gap for companies that do not have a ready pool of assets or projects to fund.”

The main thing is that ESG evolution continues in some form. Langer explains: “We don’t think the market sees what is important in quite the same way as we do – in other words, issuer credentials versus individual bond credentials. Overall, though, our view is that ESG is becoming more important, full stop. How this eventuates is not as important as the fact that ESG is much more significant than it was even a year or two ago.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.