On the up?

At the start of 2017, New Zealand’s economy and bond market are playing a role that has become increasingly familiar when it comes to the comparison with Australia: the same, but different. Both countries are on high alert for the impact of global developments on their trading status, but New Zealand’s rates environment is starting to swing towards a potential upwards cycle.

Laurence Davison Managing Editor KANGANEWS

“Relatively speaking, both Australia and New Zealand are viewed as safe havens – but this is even more true for New Zealand because of Australia’s greater reliance on China,” suggests John Bishop, treasurer and general manager, transaction services at Auckland Council. “The feedback we have received from overseas investors, even prior to the US election, is that New Zealand continues to be perceived as having a very solid economy that has performed really well relative to other global markets even following the financial crisis.”

New Zealand may have been put in the shade by its nearest neighbour at the start of the decade as Australia enjoyed the benefits of an unprecedented resources-sector investment boom. But its consistent performance has enabled it to emerge as an outperformer as the commodity sector cooled.

Global support

Asked about how international investors view New Zealand in the new atmosphere of global uncertainty, local issuers tend to express cautious optimism. They certainly do not believe New Zealand will be immune to upheaval, but they tend to be confident that the impressive local economic story is becoming better known offshore.

Mark Butcher, Wellington-based chief executive at the New Zealand Local Government Funding Agency (LGFA), tells KangaNews: “I wouldn’t call New Zealand a safe haven in the sense that I would not expect a rush here from global investors during periods of uncertainty. I think it’s more accurate to say global investors are comfortable with their current positions and are happy to hold as New Zealand still looks very attractive compared with other jurisdictions.”

Demand for New Zealand dollar bonds may in fact be growing internationally, looking across the broadest spectrum of issuers. For instance, 2016 saw the first supply from Korean borrowers in the Kauri market. Although the scale of issuance was small – two deals for a total of NZ$600 million (US$434.8 million) – lead managers say they found a largely international investor base including accounts new to the New Zealand market.

“Demand for New Zealand dollar product increased over 2016,” suggests Murray Jones, Wellington-based head of portfolio management at the New Zealand Debt Management Office (NZDMO). “We expect investors to continue to look for diversification and alternative investment opportunities, and New Zealand government bonds [NZGBs] are likely to continue to look attractive on this basis.”

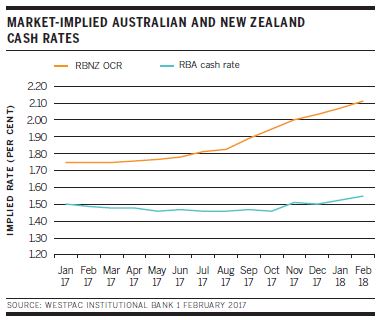

By the start of 2017, New Zealand’s expected rates direction is more akin to that of the US than Australia. Analyst forecasts for New Zealand’s official cash rate (OCR) have started to make cautious predictions of a resumed hiking cycle, while the expectation for Australia tends to be of ongoing flat rates or further cuts to come. A relatively weak employment data outcome on 1 February took some of the momentum out of rate-hike expectations, but implied cash rates continue to suggest the market sees an upwards direction for New Zealand well ahead of any move in Australia (see chart). The degree of the expected upturn is small at this stage – amounting to just a single OCR increase of 25 basis points by the end of calendar 2017 – but it marks a clear point of difference with Australia.

Butcher is also optimistic about ongoing support for New Zealand dollar product from global investors for as long as it offers an attractive yield pickup over other sovereign curves. He explains: “With the New Zealand dollar continuing to perform well against other non-US dollar currencies we expect to retain offshore investor confidence in New Zealand given our political stability, economic and fiscal strength, and strong currency."

The resilience of the New Zealand dollar was notable in 2016. The currency traded in a relatively narrow range with the US dollar for most of the year, not falling below US$0.65 after February and spending most of the second half of the year valued at US$0.70-0.75. The New Zealand dollar also established a competitive position with its Australian equivalent, often trading at more than A$0.95 and on one occasion coming close to flirting with parity (see chart).

The phenomenon of New Zealand having a somewhat divergent economic trajectory to Australia is a relatively new one, and the countries’ proximity in cultural, economic and geographic terms means many global investors continue to regard them as near proxies. However, New Zealand issuers believe they should be immune to most direct consequences of an Australian sovereign downgrade (see Australia feature).

The most likely impact would be to the local banking sector. New Zealand’s four largest banks are all subsidiaries of Australian institutions, and a sovereign downgrade in Australia would see all four parents lose their coveted double-A ratings – including in New Zealand.

“An Australian sovereign downgrade would likely have an impact on the credit ratings of the local banking sector, but whether it would affect the New Zealand government’s ability to issue bonds is unlikely,” Jones suggests. “Even so, it is something we would watch carefully. Any impact would very much depend on the investment environment and global sentiment at the time.”

Bishop adds: “The only potential flow-on effect is if an Australian sovereign-rating downgrade led to the Australasian banks also getting downgraded. This would affect New Zealand banks, but as far as Auckland Council is concerned there would be very little, if any, immediate impact.”

Economic background

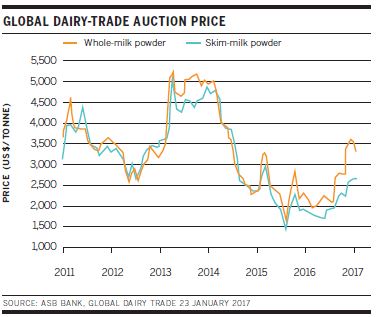

The background to the supportive global investor story is a New Zealand domestic economy that has continued to perform well. Prices for the country’s key commodity, dairy, have climbed steadily since mid-2016 (see chart) – although they are still well below their recent cyclical peak in 2013-14 – and net migration remains high. This latter factor is helping keep a potential inflation resurgence in check, leading some analysts to expect a flatter future OCR curve than markets imply. But there is no doubt that the overall economic picture is a relatively healthy one.

An obvious similarity to Australia’s economic situation when it comes to the investor-relations task is the way New Zealand issuers say investor focus continues to be on commodities and the local housing market. But issuers report slightly different experiences when it comes to the extent to which the dairy rebound has influenced the degree of investor focus.

Bishop reveals: “The key economic query investors have for Auckland Council is regarding dairy prices and the impact on council activities. We point to the fact that this effect is actually quite small, while dairy prices have recovered over the last 6-9 months. Aside from this, Auckland house prices are of course widely discussed. We assure investors that our revenue is not subject to any impact even if there is a housing-price bubble.”

Jones says the topics of conversation with investors remain the same, but their content has perhaps changed tone. “Dairy has been a long running point of conversation with investors and the recent rebound in prices has been encouraging,” he tells KangaNews.

Elsewhere, Jones points to positive economic outcomes as a strong framework for investor-relations work. In particular, he points to tourism as a key driver in recent years, with China accounting for much of the growth. He also mentions the impact of strong immigration over the last 2-3 years on construction, house prices and spending.

Meanwhile, Butcher suggests the dairy-price rebound has quelled investor concern to at least some extent. “We get fewer questions on the dairy sector but continue to receive questions on the potential effect of a housing-market downturn on the banking system and real economy,” he comments.

Investor conversations will inevitably follow the economic topography of New Zealand, adds Andrew John, funding manager at Auckland Council. “The main thing to bear in mind is that when we sell our paper to investors we are to some extent also selling them the New Zealand story,” he explains. “When you look at what the global media reports on, dairy and housing prices appear regularly. So for international investors this is the dialogue they will come across more frequently than anything else.”

Political developments

One relatively new – if second-order – subject of interest for international investors is New Zealand’s political situation. The National Party has been in government since the general election of 2008, but the resignation of prime minister John Key in late 2016, with an election already scheduled for September 2017, took most observers by surprise.

The political landscape remains relatively stable, however. The new prime minister, Bill English, was a long-serving deputy prime minister and minister of finance, while prediction markets suggest the National Party has at least an 80 per chance of retaining power as of early February.

Even so, Butcher adds: “As we approach the general election later this year, and given both the recent change of prime minister and last year being the year of global political surprises, I would expect to receive more enquiry about the political environment from offshore investors.”

Margin direction

Like Australia, New Zealand saw the yield pickup offered by its sovereign bond curve over other government markets decline significantly in 2016. A September 2016 research note published by BNZ noted that NZGB spreads were “near a cyclical low point” relative to US Treasuries (USTs) and “well below 20-year average” relative to Japanese government bonds.

The BNZ note concluded that NZGB yields continue to “stand out in the low/negative yield world”, however – with relative yields to euro and sterling bonds especially attractive. Despite the relative tightening to the US and Japanese sovereign curves, BNZ’s analysts concluded: “We see narrower cash-rate spreads assisting compression when other fundamentals are also supportive. The market already prices further New Zealand-US cash-rate compression, but we anticipate further narrowing than is currently priced.”

Holders of New Zealand bonds have had a favourable experience in recent months – at least compared with other sovereign curves. But local borrowers say the types of global investors they engage with tend not to be looking for near-term gains.

“Investors have moved to diversify their own holdings over recent years. To the extent that this has resulted in a greater NZGB allocation, our experience to date is that the nature of these holdings have been relatively stable during times of volatility,” Jones comments.

Butcher adds: “Long-term, real-money accounts dominate our offshore investor base while short-term reserve managers and central banks don’t feature. Our offshore investors are happy with a steeper curve, higher yields and relative stability in the spread to USTs. Any selling we have seen we think is predominantly based on a stronger US dollar view – and has been more than offset by new buyers of LGFA bonds from offshore.”

A stable, consistent global investor base is likely to prove extremely helpful in the coming months and years as fundamental changes in trading dynamics make bond markets ever-more prone to volatility. Jones explains that changes in regulation mean intermediaries are less able to warehouse securities and will therefore be more likely to rapidly price changing investor sentiment.

He adds: “I believe we are going to see periods where credit and government curves will reprice quite quickly – the sharp sell-off near the end of the calendar year is probably indicative of this type of move. In this context, diversification of the investor base is something the NZDMO has been focusing on over the past few years. This will continue to be important going forward.”

Although Jones says NZGB spreads held up relatively well in the late-2016 correction he also suggests further tests are likely approaching. “We expect to see a general repricing across credits as curves move higher and investors that may have been targeting outright yields shorten duration and move back up the credit spectrum,” he explains.

In general, though, New Zealand issuers are looking at the future of their investor-relations task with a degree of confidence. The potential investor base has expanded in recent years, and the country’s economic performance stands it in good stead to attract investment dollars seeking diversification without sacrificing liquidity altogether.

“I think, provided New Zealand continues to offer a positive spread pickup versus USTs and Australian Commonwealth government bonds, the factors which have driven support for New Zealand in recent years will remain,” Butcher argues.

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

Related news

New Zealand's market ready to step up as degree of difficulty grows

With a substantial infrastructure requirement looming and a weak economic environment, the New Zealand capital market will have to be on top of its game in the years ahead. Participants at KangaNews’s annual women in New Zealand capital markets roundtable discussed the issues at hand and how they believe a constructive ecosystem can be developed.

New Zealand looks for the silver lining despite economic headwinds

Speakers at the ANZ-KangaNews New Zealand Capital Market Forum, which took place in Auckland on 21 March, believe the local market continues to offer opportunities despite the obvious challenges of an economy in recession. The everincreasing urgency of the energy transition, a significant infrastructure shortfall and the role of the fixed income market took centre stage in discussions.

Foundations for the future

The KangaNews Debt Capital Market Summit 2024 took place in Sydney on 18 March amid an unprecedented bonanza of new issuance and at what could prove to be an inflection point for the local market. The agenda covered a raft of topics centred on the theme of taking advantage of recent growth to deliver a market that is match fit for the demands that will be placed on it, with discussions ranging from the impact of geopolitics and global economic currents to the need to stay ahead of accelerating technological advances.