Eyes on Australia: Zurich Insurance Group

With a significant market share in the Australian individual life-insurance market after recent acquisitions, Zurich Insurance Group (Zurich) is going on a roadshow to Australian and Asian investors towards the end of April. Mathias Meisel, head of capital markets in Zurich, talks to KangaNews about the issuer’s Australian business and its funding plans.

KangaNews Zurich has incrementally increased its presence in Australia in recent years, with the acquisition of Macquarie Group’s life-insurance business in 2016, Cover-More Group in April 2017 and ANZ’s OnePath in December. What is so attractive about the region?

Australia has attractive long-term fundamentals. The country ranks among the top 15 global economies and is well-positioned to benefit from the broader growth in the Asia Pacific region. The country also has a stable and well-established legal and regulatory framework.

KangaNews To what extent has the opportunity to increase Zurich’s presence in Australia been created by the divestment of insurance assets by Australian banks?

The decision of some Australian banks to divest some of their insurance assets as part of their efforts to increase their own focus has provided the opportunity for Zurich to increase our presence and bring our global knowledge of working with banks to our new local partners.

KangaNews Do you see growth in Australia as a chance to increase Zurich’s presence in the Asian region?

KangaNews What plans, if any, does Zurich have for further opportunistic or strategic acquisitions in Australia?

Given our overall scale in the Australian market we don’t see any need to strengthen the business through further acquisitions. However, as with all our core markets, we will assess new opportunities as they emerge against both our strategic priorities as well as the strict financial criteria we apply.

KangaNews The three acquisitions give Zurich a 19 per cent individual life-insurance market share, making it Australia’s largest life insurer. What effect does this have on the financial footprint of the global business?

KangaNews What does the acquisition mean for Zurich’s Australian funding plans? You have scheduled a non-deal Australian roadshow towards the end of April. Presumably this means you are at least exploring the idea of funding the local business in the local currency?

For the roadshow we are interested in a two-way dialogue where we present the investment proposition Zurich has to offer and understand investor interests.

We are very interested in the local Australian market and would like for the local market to reciprocate by embracing us and the quality and global diversification that we bring.

KangaNews How has Zurich’s Australian business been funded historically?

KangaNews The OnePath acquisition isn’t expected to complete until November this year – subject to regulatory approval. What does this mean for your funding plans specifically in terms of the timeline?

KangaNews How large is Zurich’s funding need likely to be on an annual basis for the Australian business and with what frequency are you likely to come to market?

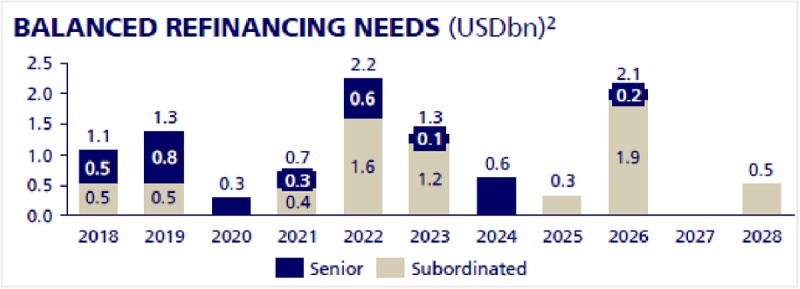

CHART 1: ZURICH INSURANCE GROUP DEBT MATURITY PROFILE

2 Maturity profile based on first call date for subordinated debt and maturity date for senior debt

Source: Zurich Insurance Group 17 April 2018

As for the Australian business, we do not expect to require further funding beyond what we are considering for OnePath. However, we will maintain a certain gearing related to our capital deployed in Australia. This will make a recurring refinancing of debt instruments very likely, also if sensible in the AUD debt market.

It’s hard for us to commit to a specific frequency in terms of future issuance because we fund on a global basis for the entire group. But very roughly speaking, if we would enter the local market, investors could expect to see us in that market every few years.

KangaNews What are your thoughts on the value of establishing an Australian dollar domestic issuance programme? We have seen a number of global financial institutions issuing AUD off EMTN programmes in recent times – is it necessary to have a domestic programme?

We have looked at the advantages and disadvantages of setting up a new Australian wholesale debt-issuance programme, as opposed to issuing off an existing EMTN programme using a long-form pricing supplement. Recently, we added an Australian issuer to the EMTN programme, which provides us with sufficient flexibility to be issuing in Kangaroo format using a long-form pricing supplement, at relatively short notice, should the need or opportunity arise.

KangaNews QBE very successfully issued US dollar AT1 securities in and Asian-focused deal last year. What role do you see Asian investors playing in funding the expanded Zurich Australian business? Is additional-capital issuance likely to be on the cards?

As a group we also issue capital instruments in debt format. This is done on a group level. It’s a possibility we may contemplate this type of issuance in Australia but initially we would like to focus on the senior market.

We think we offer real value in terms of credit quality and global diversity. There are not many non-bank names in the financial industry with a Swiss home base and such a diversified global setup as the Zurich group. Given the rather concentrated and bank-weighted nature of the Australian debt market, we hope Australian investors appreciate the very rare diversification opportunity that we bring combined with the high franchise and credit quality that they expect.

KangaNews The other notable facet of the QBE AT1 deal was that it was a green bond. Zurich is a market leader in sustainable finance including as an investor – but could green and/or social bonds be an option for funding the Australian business?

KangaNews What does the growth in scale mean for Zurich as a fixed-income investor in Australia? Will the firm be more prominent, including as an active investor on its own account?

KangaNews Does Zurich have any plans to acquire any life insurance businesses in New Zealand and if so what does this mean for its capital markets footprint in the New Zealand dollar market?

As a matter of course we continuously scan the market globally to assess if there are potentially interesting opportunities, which we would explore in our usual disciplined manner. Any opportunities would have to be aligned to our strategic priorities and fit culturally within the Zurich group, while also adding value to our shareholders by achieving our group hurdles.

KangaNews Do you have any final message for Australian and other investors you will be meeting on your upcoming roadshow?

Related news