Fixed-income investor survey: betting the house

In September 2018, Fitch Ratings (Fitch) and KangaNews conducted their biannual Australian Fixed-Income Investor Survey for the 10th time. Survey data collected over the past half decade show the changing patterns of investor outlook – and the latest iteration zeroes in on the domestic housing market as a key risk factor.

By Laurence Davison and Matt Zaunmayr

Once again, the survey received responses from fund managers collectively representing a large majority of the sector in Australia in assets under management. Nearly 40 investors submitted their views – close to a record for this survey.

With more than four years of historic data now available, the Fitch-KangaNews survey provides an illuminating snapsot of fixed-income-investor sentiment. One of the key trends over this period is the gradual rise to the forefront of buy-side concerns about domestic economic considerations over global dynamics.

At the same time, the survey’s historic data show sentiment gradually improving through the middle of the decade but suffering a notable, if not extreme, reversion in the current year. A larger proportion of investors expect to see spreads widen in the coming months than has tended to be the case in this survey. The focus is on the financial sector in particular, where fund managers see pressures building around residential-mortgage exposures and a consequent impact on credit spreads.

The tone of the survey is moderate but cautious. The overall expectation appears to be of a weakening Australian economy without necessarily a collapse in fundamentals. This is perhaps best summed up by investors’ perspective on the domestic housing market.

The measured tone of the survey is highlighted by the fact that even where investors expect sectoral weakness, specifically in the financial sector, they do not anticipate any significant issues with access to funding in the period ahead. There is a clear gap between what can loosely be described as market impacts – developments like wider credit spreads and tighter lending standards – and the broader macro backdrop, which investors generally see as weaker but not problematic. There is still, for instance, only very limited expectation of much higher unemployment in Australia or of the reserve bank shifting back to an easing rates bias.

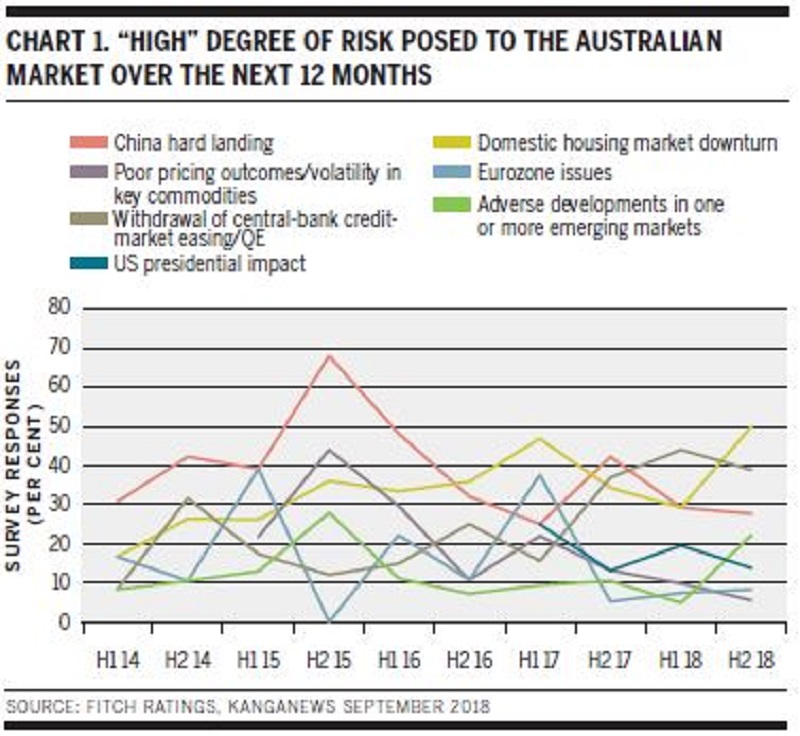

For just the third time in the survey’s history, the housing market ranks as the leading risk factor for Australian fixed-income investors (see chart 1). With exactly half the survey respondents ranking domestic housing a “high” risk factor for the coming year, the issue attracts the second-highest level of concern of any included in the survey throughout its history.

Regional factors are also relatively prominent among the risk factors. Fitch’s report on the survey notes: “While regulations and tighter lending standards have played their part, external threats posed by trade wars also loom and are reflected in other related risks, namely a China hard landing, adverse emerging-market developments and US presidential impact.”

Fitch also notes: “Withdrawal of QE by central banks has slipped to second on the list of risks to Australian credit markets over the next 12 months, with 39 per cent of investors ranking this as a high risk, down from 44 per cent in H1 2018, even though the withdrawal of QE could put upward pressure on global bond yields.”

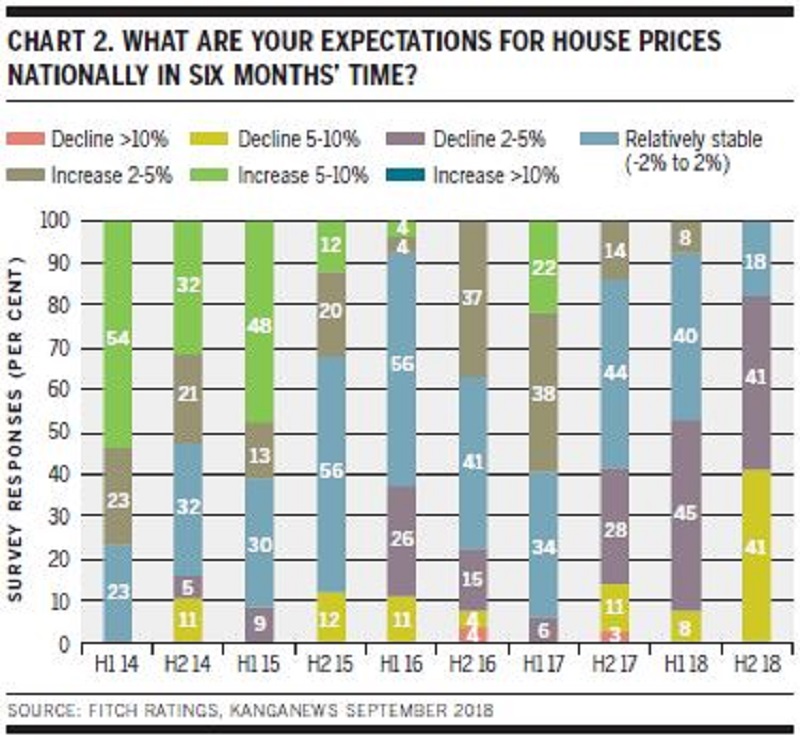

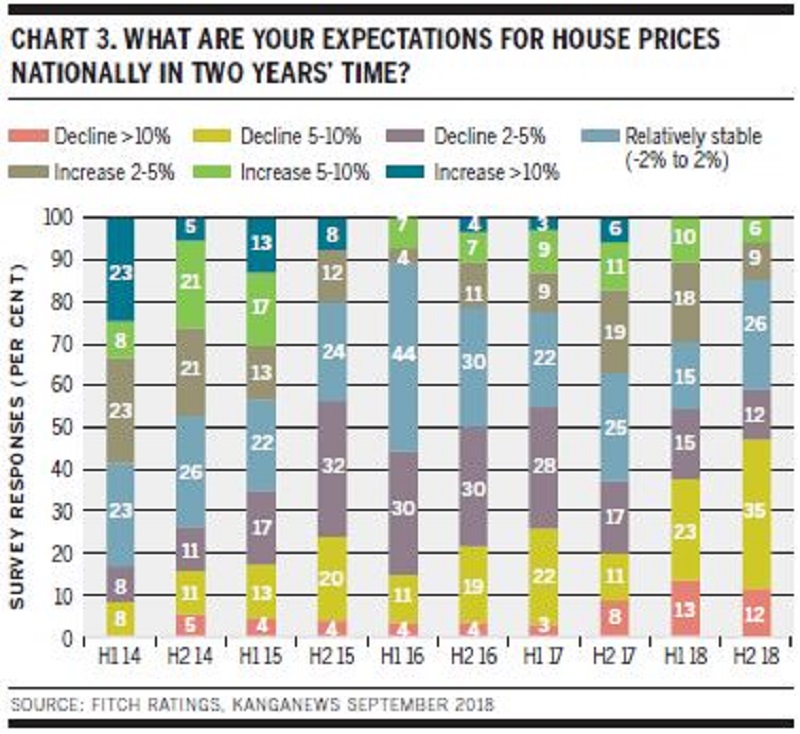

Unsurprisingly given the risk outlook, more than four-fifths of the investors surveyed expect house prices to continue falling over the next six months – while none anticipate a rebound (see chart 2). The outlook is somewhat more mixed when the horizon is extended to two years, though more than half expect prices still to be lower in late 2020 than they are now (see chart 3).

Fitch’s view is that Australian banks are well positioned to handle an ongoing housing-market correction, based on its study of the capital impact of a point-in-time stress across a range of scenarios, with house-price declines of 20-60 per cent and default rates of 10-20 per cent. However, the rating agency’s central scenario is not a sharp or substantial correction.

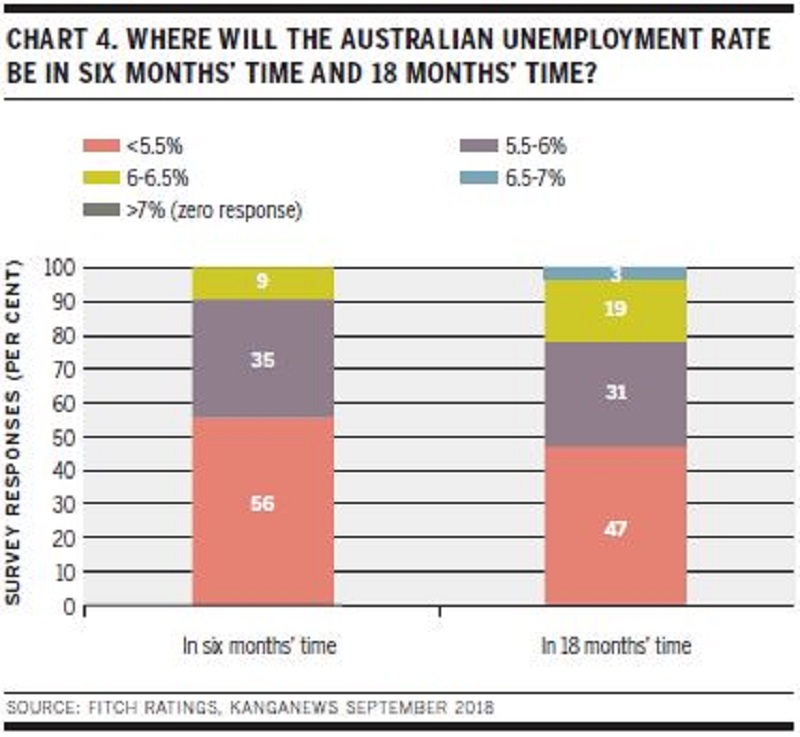

The most likely causes of an accelerated market downturn are well known. “A rapid rise in unemployment is the most likely driver of a significant housing-market correction, although sharply higher interest rates would also pressure some borrowers in light of the high level of household debt,” Fitch adds.

Australian fixed-income investors do not appear to anticipate either. Their outlook on unemployment is very benign: fewer than 10 per cent of survey respondents anticipate an increase of 0.5 per cent or more from the current 5.6 per cent unemployment rate in the next six months, while only just more than 20 per cent have this expectation for the next 18 months (see chart 4).

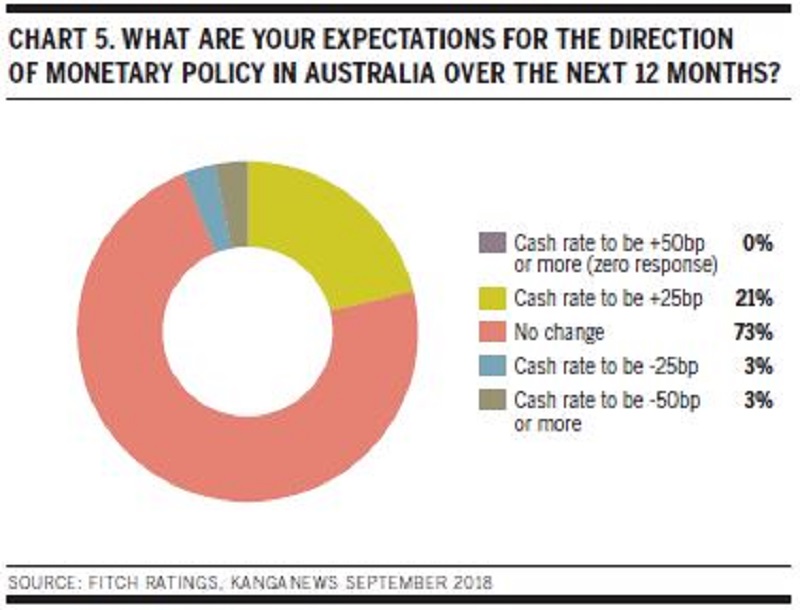

Investors have more or less capitulated on expectations of rate hikes. As recently as six months ago, nearly half the responses to the Fitch-KangaNews survey anticipated at least one cash-rate increase from the Reserve Bank of Australia (RBA) in the next 12 months; that figure is now down to barely 20 per cent (see chart 5).

“Fitch anticipates strong labour markets to persist with the unemployment rate drifting lower from 5.4 per cent in 2018 to 5.2 per cent by 2020 on the back of above-trend GDP growth and a less rapid rise in participation rates,” the rating agency writes. “We expect the RBA to undertake a shallow interest rate-tightening cycle given that, despite tightening labour markets, we forecast only gradual wage-growth and inflationary pressures.”

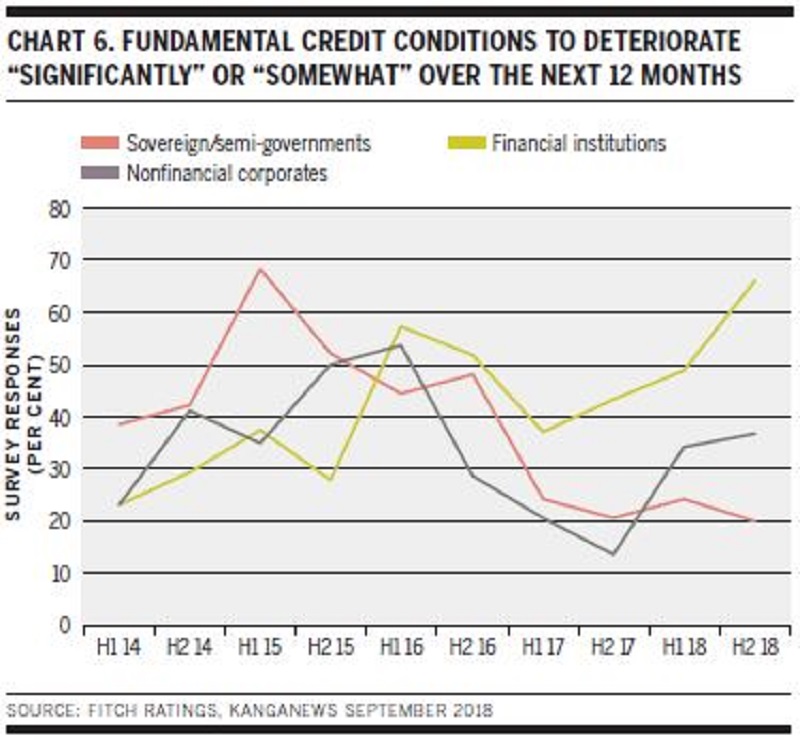

In the minds of Australian fixed-income investors, weakness is more likely to come through in deteriorating fundamental credit quality – most notably in the bank sector.

Two-thirds of survey responses forecast “significantly” or “somewhat” worse bank credit conditions in the year ahead, compared with just 20 per cent with the same outlook on the sovereign sector (see chart 6).

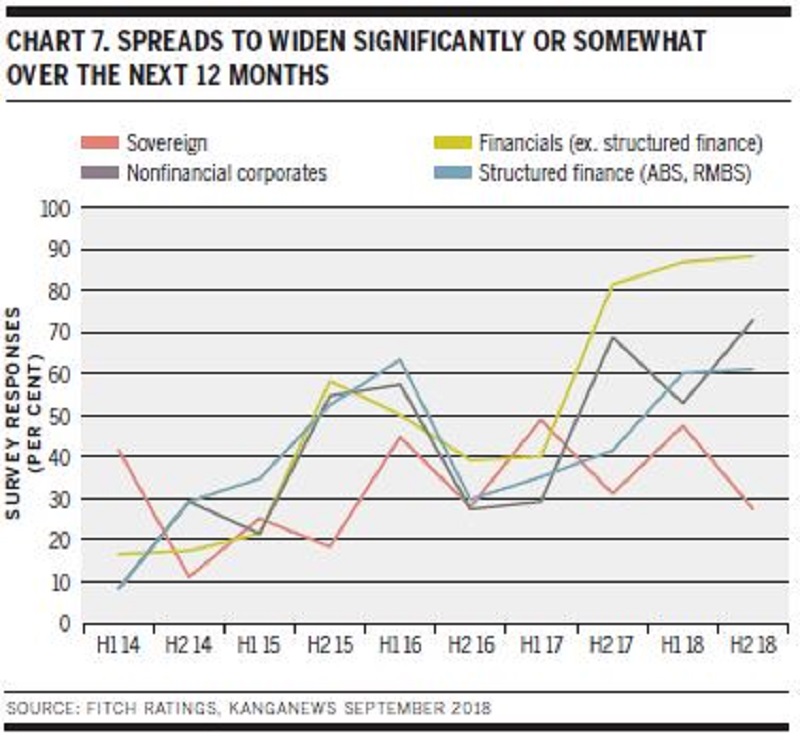

The same view comes through when it comes to expectations around the future direction of credit spreads. Again, investors see the financial sector deteriorating and the sovereign sector performing much better (see chart 7). There is also a noticeable uptick in expectations of wider corporate credit spreads in the year ahead: nearly three-quarters of survey responses hold this view.

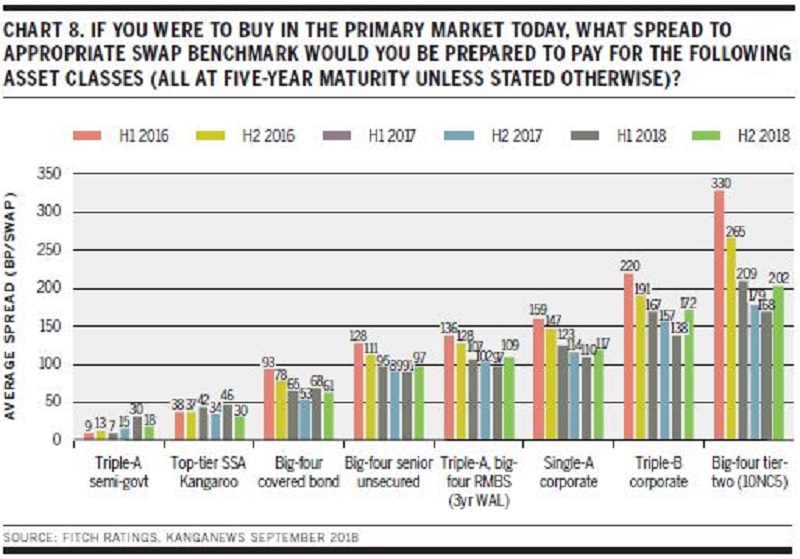

In fact, investors are already reporting their willingness to engage with various credit asset classes can only be induced by higher spreads. The average engagement point reported by investors responding to the Fitch-KangaNews survey has actually fallen for key high-grade asset classes – semi-governments, triple-A Kangaroos and major-bank covered bonds – but the same cannot be said for bank and corporate unsecured bonds (see chart 8).

While the impact is only a few basis points for major-bank senior-unsecured bonds and single-A corporates, spread expectations widen more significantly for residential mortgage-backed securities, triple-B corporates and bank subordinated debt.

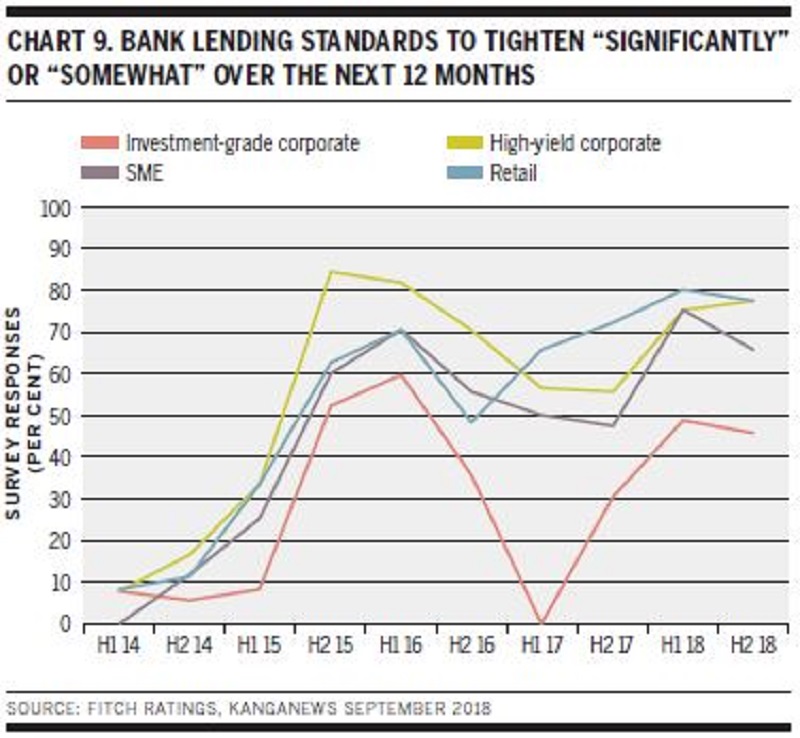

Investors expect banks to respond to weaker credit conditions by continuing to tighten their own lending standards. Again, the sectors most affected will be those bearing the highest risk: high-yield corporates, the retail market and – to a slightly lesser extent – SMEs (see chart 9).

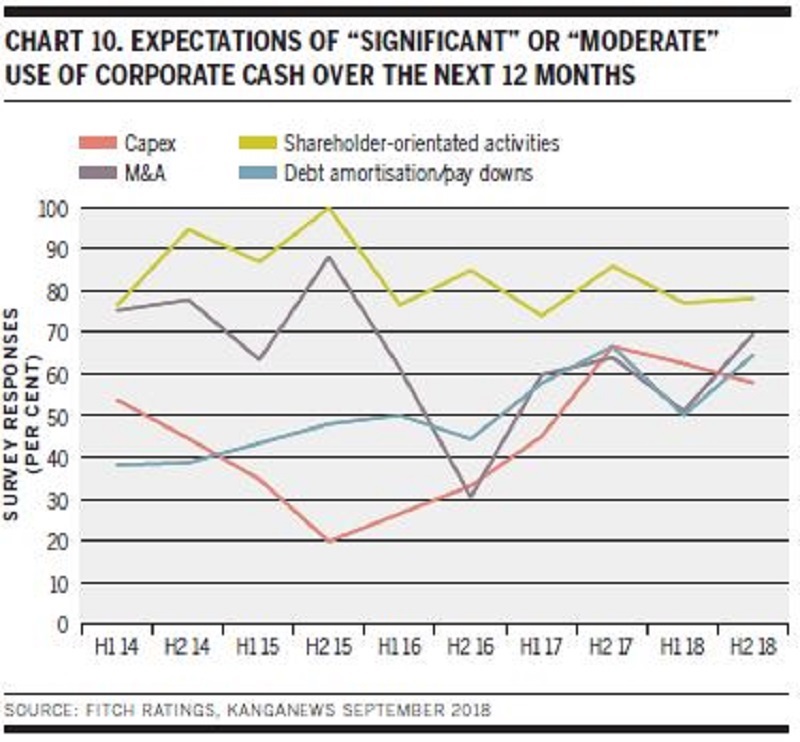

The Fitch-KangaNews survey also suggests investors believe Australian corporates will maintain their traditionally conservative approach. While there is some expectation of an M&A pickup, “shareholder-orientated activities” remains the most likely use of corporate cash in investors’ minds (see chart 10). The capex outlook sinks after a few quarters of more positive views, while expectations that companies will seek to retire debt have also crept up.

Australian fixed-income investors do not expect a significant shift in already-conservative corporate-leverage settings. Just 27 per cent believe Australian corporates will increase leverage modestly over the next 12 months, down significantly from 44 per cent in the previous iteration of the survey. More than half the investors do not foresee any change in leverage, a number which is also up slightly from the previous survey.

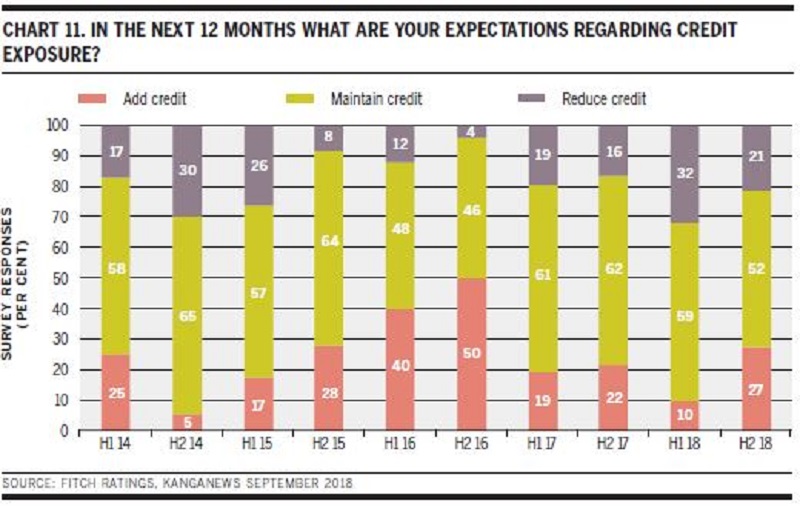

On the other hand, the investment outlook appears to have moderated. The proportion of investors saying they expect to reduce credit exposure over the coming year has eased, while expectations of higher credit exposure are at their highest level for two years (see chart 11).

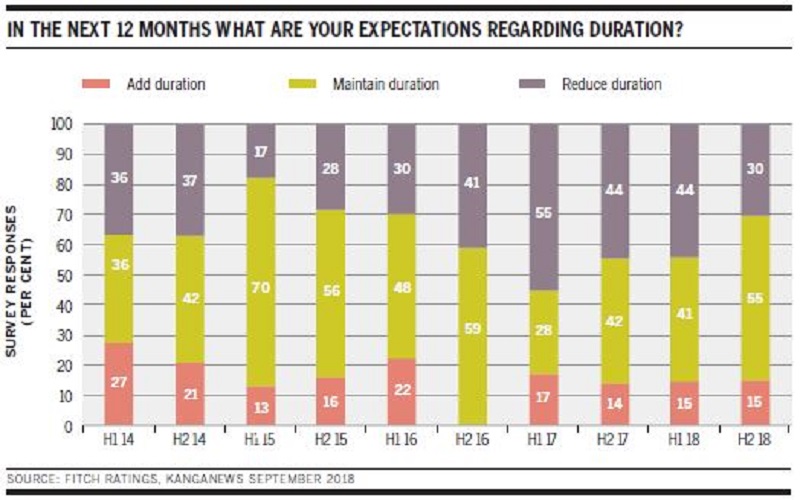

It is a similar story for duration. While there are still only a few fund managers that expect to add duration in the next 12 months, the proportion reporting plans to reduce duration is at its lowest level since the turn of 2015-16 (see chart 12).