Issuer profile: Bluestone Mortgages

Key company and debt-issuance information on Bluestone Morttgages. Uploaded 15 October 2018.

| Size of loan book | A$1.75bn |

| Makeup of loan book | Near-prime and nonconforming residential mortgages: 84% Reverse mortgages: 16% Commercial mortgages: <1% |

| Geographic distribution of loan book | Australia: 96% New Zealand: 4% |

| Outstanding debt issuance | RMBS: A$1.2bn |

Source: Bluestone Mortgages September 2018

About Bluestone Mortgages

Bluestone Mortgages (Bluestone) provides solutions to borrowers who fall outside bank criteria with

mortgage products spanning near-prime through to specialist in Australia and New Zealand.

Bluestone was established in Sydney in early 2000 and has expanded to become a significant lending and asset-management business employing more than 200 staff with in excess of A$8.4 billion of assets under management.

The business has developed a suite of industry-best-practice systems and processes. This has seen Bluestone consistently originate quality assets at equity-accretive margins.

In Australia, the group has operated a successful mortgage-lending platform for more than 15 years with no loss to any institutional investors.

Ownership and capital structure

In March 2018, entities associated with Cerberus Capital Management completed a transaction with Bluestone Group to purchase Bluestone’s Asia-Pacific operations. As a result, Bluestone Asia Pacific is no longer related to Bluestone UK. The executive management team of the Asia-Pacific business

continues to run the operations with additional management positions being added to support growth.

The strategic focus of the group will de-risk on both sides of the balance sheet, shifting lending focus towards lower-credit-risk assets and reducing structural leverage. Bluestone has no debt at corporate level.

Asset performance

Bluestone maintains a disciplined underwriting and pricing policy to generate superior risk-adjusted returns. Bluestone’s cumulative loss over 18 years of operating is less than 1.5 per cent.

Bluestone’s portfolios are built on conservative security criteria with a maximum loan-to-value ratio of 85 per cent, a focus on higher-population-metropolitan securities, and a majority of owner-occupied principal and interest borrowers.

Funding strategy

Bluestone has a broad investor base. It has warehouse facilities from Commonwealth Bank of Australia, National Australia Bank and Macquarie Bank with additional facilities being added, while the Sapphire securitisation programme has issued in excess of A$7.2 billion of bonds domestically and offshore.

Bluestone expects to issue 3-4 securitisations per year, in increasing size as the business continues to grow.

Business performance

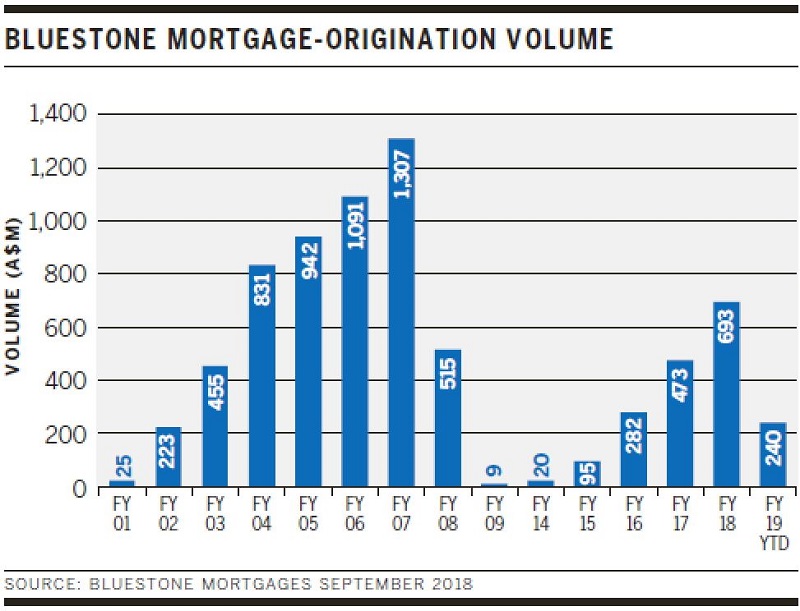

The Bluestone business is performing strongly after re-entering mortgage origination in Australia in 2013 and New Zealand in 2017. Having invested heavily over the last five years, Bluestone is generating strong financial performance with significant uptake of product by brokers. Bluestone maintains strict discipline around pricing, ensuring all products deliver the required risk-adjusted returns. Bluestone will continue expanding its product range and operational jurisdictions, continuing the growth it has seen since returning to the market.

For further information please contact:

| Campbell Smyth Chief Executive Officer |

+61 2 8115 5167 |

| Tim Miller General Manager, Operations |

+61 409 313 845 |

Sponsored by

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

Related news