Trio of factors aid demand for ADB’s record Kangaroo green bond

Kangaroo deal flow in benchmark volume started coming through on 8 January, when Asian Development Bank (ADB) priced a A$1 billion (US$718 million), five-year green bond. Despite ongoing headwinds for supranational, sovereign and agency (SSA) issuance in Australian dollars, the deal achieved record volume based, deal sources say, on the boost the year’s first issuer typically receives, improving technical factors and the green overlay.

ADB’s transaction, led by Deutsche Bank, Nomura and TD Securities, is the largest-ever SSA Kangaroo green bond, surpassing European Investment Bank’s A$750 million five-year climate-awareness bond, which was the first deal priced in 2018 (see table).

Top-five SSA Kangaroo green bond deals by volume

| Pricing date | Issuer | Volume (A$m) | Tenor (years) |

|---|---|---|---|

| 8 Jan 19 | Asian Development Bank | 1,000 | 5 |

| 3 Jan 18 | European Investment Bank | 750 | 5 |

| 26 Mar 15 | KfW Bankengruppe | 600 | 5 |

| 28 Aug 18 | Kommunalbanken Norway | 450 | 5 |

| 25 Jan 18 | European Investment Bank | 400 | 10 |

Source: KangaNews 11 January 2019

The deal is also the largest single-tranche SSA Kangaroo transaction since World Bank’s A$1 billion five-year deal in June 2014 and ADB’s equal largest single-tranche Australian dollar deal – ADB achieved this volume in several transactions in 1998, 2010, 2011 and 2014, according to KangaNews data.

The transaction is ADB’s first green bond in Kangaroo format, having previously issued around US$5 billion equivalent under the programme in currencies such as US dollars, euros, Swedish krona, Hong Kong dollars and Indian rupee. The programme focuses on funding projects which support mitigation of greenhouse gas emissions and adaptation to the consequences of climate change.

Volume bump

Lead managers reveal that the transaction launched with minimum volume of A$300 million, however they were always confident the final print would be larger.

The first transactions of a calendar year typically derive a benefit from the demand that builds up over the Christmas and New Year break, but the leads and borrower suggest that in ADB’s case the green overlay provided an additional volume boost.

Anthony Ruschpler, Manila-based treasury specialist at ADB, says much of the interest surrounding the transaction was because of the green label. “We do not think we would have achieved the same outcome for a regular outing. Not only did most of the key domestic SRI [socially responsible investment] buyers participate but so did several offshore accounts which have been absent from the Kangaroo market for a number of years.”

Yuriy Popovych, Singapore-based director, international fixed income, origination and syndication at TD Securities, says that the transaction began to fuel itself once it was announced to the market that it would be upsized.

“At A$300 million some accounts were waiting on the sidelines because green-bond transactions typically are less liquid in secondary markets, with accounts tending to buy and hold. But as the transaction grew, first to A$500 million and eventually to A$1 billion, most of these accounts came in to the deal and a lot of others increased their orders.”

Craig Johnston, Sydney-based director, Australian and New Zealand dollar syndicate, says it is difficult to exactly pinpoint the level of additional demand coming from the green overlay. However, he says the advantage is certainly there, with investors eager to buy the product for more reasons than a simple desire to add to their green portfolios.

“Some are buying on expectations that their dedicated green funds will grow or because they expect the product to perform well,” Johnston tells KangaNews.

Oliver Holt, Nomura’s head of Australian dollar syndicate in Singapore, says ADB’s deal gave investors the best of both worlds. “The funds are purely focused on the darkest-green projects which is the preference for ESG [environmental, social and governance] investors, while also allowing traditional investors into the order book,” Holt says. “This resulted in a materially larger deal than ADB’s peers. As such this is likely the most liquid green Australian dollar SSA to date and this will help cultivate further interest.”

Since the beginning of 2018, three of the four largest-volume, five-year SSA Kangaroo deals have been in green format (see chart 1). Jeff Grow, executive director at UBS Asset Management in Sydney, tells KangaNews it is encouraging for the market to see large-volume deals being printed.

Source: KangaNews 11 January 2018

“We are not particularly worried about liquidity as there is always a bid for green bonds in the secondary market,” says Grow. “But we would rather get set in the primary market so that we can fulfil the wishes of our clients, rather than having to chase the bonds in secondary.”

Technicals supportive

The Australian market proved to be challenging for SSA issuance in the second half of 2018, with unfavourable basis-swap levels curtailing potential supply. Ruschpler reveals that pressure on Australian dollar spreads towards the end of 2018, owing to selling coupled with a tightening bias in the US dollar market, made new mid-curve Kangaroo issuance very challenging. The opportunity for ADB’s new Kangaroo deal came from the fact that spreads have stabilised, and US dollar spreads have moved wider.

Johnston says the market may not be as conducive now as it was in the first months of 2018, when a whopping A$4.8 billion of SSA issuance was priced according to KangaNews data. However, he says SSAs currently look attractive compared with semi-government paper and are pricing at a level that is historically wide on an asset-swapped basis.

Holt says the deal represents good long-term relative value against Commonwealth government bonds. “This is a function of US dollar swap spread contraction over the last few months and the opposite effect in the Australian dollar swap spread,” he says.

Holt continues: “For the last 18-24 months investors have looked to the US as rates have risen and Australia’s have fallen. The change in tone from the Federal Reserve in the final quarter of 2018 has seen a number of the rate hikes priced out in the US, so investor attention is beginning to return to other currencies, including to Australian dollars.”

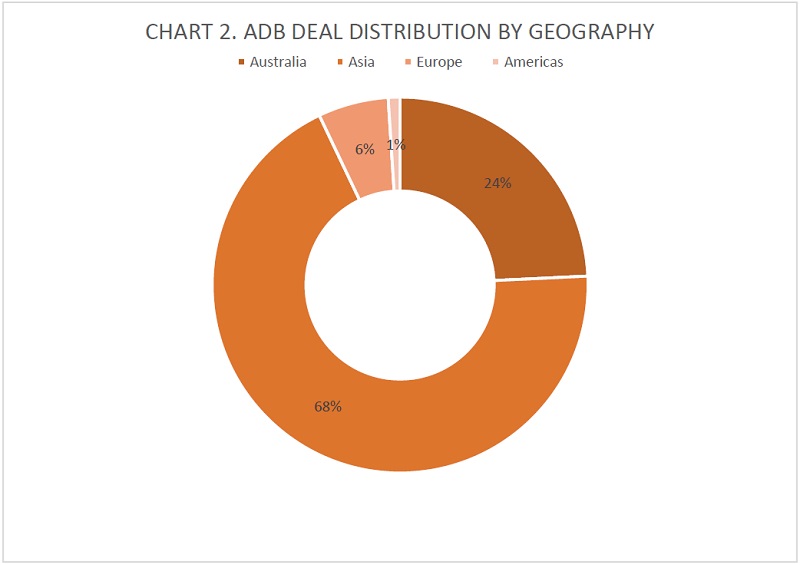

This dynamic led to a larger than expected participation from Asian accounts. Typically, mid-curve SSA Kangaroos – particularly green bonds – have been targeted at domestic investors, and leads say these were the initial focus of the transaction.

However, deal statistics provided by TD Securities show that the majority of the transaction was allocated to Asian-based investors (see chart 2).

Source: TD Securities 11 January 2019

Challenges remain

Despite these improving technical factors challenges remain for the SSA Kangaroo market, with leads revealing that other global options are currently proving more cost-effective.

Popovych says: “Australian dollars do not currently represent a pricing arbitrage opportunity. The secondary curve has pushed out in recent months, and pricing compared with euros, sterling and US dollars is a bit expensive.”

Added to this, Holt points out that sterling and euros have been particularly competitive recently, with some deals in sterling saving issuers 6-8 basis points compared with other global markets.

However, he also reveals that demand in sterling appears to be petering out with deal sizes decreasing. And in euros, higher new-issue concessions are beginning to be built in as the market reprices. “Australian dollars are currently a bit wider, but not significantly,” he tells KangaNews.

Popovych says the Kangaroo market is open for borrowers that are prepared to take a strategic view. “The pipeline of the usual suspects is there, but some are struggling to get to their funding-cost targets at the moment.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news

Quantum leap for Canadian provinces as Québec smashes Kangaroo record

Investor diversity, relative value and the growing status of the Australian dollar market lined up for Province of Québec as it shattered the record volume for a Canadian province Kangaroo transaction. The A$1.35 billion, 10-year print was nearly four times larger than any previous deal from the sector – a record that had stood for a decade.