Fixed-income investor survey: neighbourhood watch

The domestic housing market has soared as a risk factor in the minds of Australian fixed-income investors according to the latest Fitch Ratings (Fitch)-KangaNews Australian Fixed Income Investor Survey. A deeper look at the data suggests investors believe risk is contained, but the survey as a whole points to expectations of a slowing economy.

By Helen Craig and Laurence Davison

The survey was conducted in March this year and received responses from 43 Australia-based institutional fixed-income investors. This represents a comfortable majority of domestic assets under management in the sector. This is the 11th iteration of the survey, which has been conducted on a half-yearly basis since the start of 2014. As such, the survey provides a unique timeline of Australian fixed-income investor sentiment.

The proportion of investors assessing the domestic housing market as a “high” risk factor for local credit is, at 70 per cent, the greatest for any risk factor since the survey’s inception (see chart 1). Only once before – around QE withdrawal, in the second half of 2015 – has a risk factor been rated high by more than half of survey respondents.

Fitch’s expectation is that Australian house prices will drop by 5 per cent in 2019, a similar pace to 2018 and enough to take the total peak-to-trough correction to 12 per cent by the end of this year. “Weakness is being driven by tightened credit conditions following regulatory enforcement of stricter lending standards. Investor demand has also been hit by an increase in stamp duty for nonresidents and macroprudential limits on interest-only and investment lending,” Fitch’s analysts conclude.

Investors seem to agree with the rating agency on most of this analysis and if anything to be more bearish at the margin. Nearly two-thirds of survey respondents expect house prices to fall by at least a further 5 per cent in the next six months. While the majority expect the correction to be worst in the near term, there is little hope of a significant rebound in the next two years (see chart 2).

If Fitch’s analysts are right to identify tighter credit conditions as a main cause of the housing-market decline, Australian fixed-income investors offer little succour for those hoping for a reversal of credit rationing. Nearly two-thirds expect retail lending conditions to tighten further while fewer than 15 per cent anticipate any degree of loosening (see chart 3).

The last time a majority of survey respondents expected retail lending to become looser was in the second half of 2014. In a further contrast with the latest retail-sector credit expectations, barely a third of investors responding to the H1 2019 Fitch-KangaNews survey believe banks’ lending to investment-grade corporates will tighten in the next 12 months.

None of this means investors are necessarily anticipating a major economic downturn in Australia. Three-quarters are comfortable that unemployment will remain below 5.5 per cent for the next six months. While there is some expectation that it will creep up over the coming 18 months, more than 80 per cent of survey respondents still expect unemployment to be 6 per cent or less by the second half of 2020 (see chart 4).

Solid employment numbers will not be enough to stay the Reserve Bank of Australia’s hand when it comes to cutting rates, investors believe. Exactly 60 per cent of survey respondents now expect cuts in the next 12 months, nearly half of them by at least 50 basis points (see chart 5). This is the most widespread expectation of rate cuts since H2 2016.

Credit conditions

Even if it is not accompanied by a downturn in employment, investors expect the housing-market decline to have an impact on bank credit.

Nearly two-thirds – a record for this survey – expect credit conditions to deteriorate for financial institutions over the next 12 months (see chart 6).

Fitch’s analysts write: “Sluggish wage growth has slightly increased 90-day plus past-due loans. Impairments are likely to rise from historical lows due to the cooling property market and high household leverage, which makes households more susceptible to shocks from higher interest rates and unemployment. The ongoing tightening of banks’ risk appetites and underwriting standards should, however, support asset quality in the long term."

The bulk of the Australian fixed-income investor base predicted wider bank spreads in the previous two iterations of the Fitch-KangaNews survey and it is little surprise to see the same forecast in the new survey (see chart 7).

Perhaps more surprisingly, while only 37 per cent of investors expect fundamental credit conditions to deteriorate for nonfinancial corporates, nearly 80 per cent anticipate wider corporate spreads.

Fitch is seeing the housing market malaise start to have a wider impact across Australia. The rating agency has reduced its 2019 GDP growth forecast for Australia to 2 per cent, from 2.7 per cent as recently as December last year. However, Fitch expects growth to recover to 2.5 per cent in 2020.

“The housing downturn is having larger negative effects on the real economy than we envisaged, while the agricultural sector is suffering from the effects of a prolonged drought,” Fitch’s analysts write. “Construction activity has also declined in the previous two quarters, while consumption has been slowing against a backdrop of sluggish household income, a low savings ratio, high debt and adverse wealth-effects from falling house prices.”

On the flip side, Fitch acknowledges that the labour market has remained strong while buoyant bulk-commodity prices have lifted export receipts and company profits.

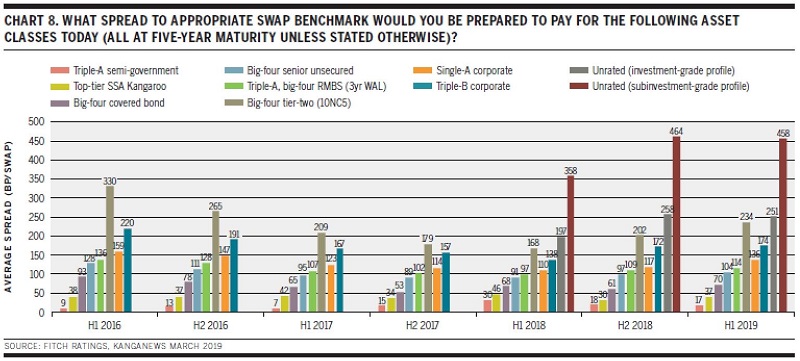

Investors have already recalibrated their pricing expectations in light of softer credit-market conditions. Asked what margin they would pay for a range of asset types, survey respondents on average suggest high-grade spreads – for local government-sector issuers, international supranational, sovereign and agency names and covered bonds – have held up reasonably well. Meanwhile, credit asset class pricing expectations have widened commensurate with their risk status (see chart 8).

Conservative corporates

In this environment, it is perhaps unsurprising that already low expectations of corporate credit growth have receded yet further. The proportion of investors anticipating even “moderate” use of corporate funds for capex is at its lowest level since late 2016. Meanwhile, M&A is the second least-expected use of corporate funds in the Fitch-KangaNews survey (see chart 9).

As ever, a large majority of investors expect “shareholder-orientated activities” to be the primary focus of corporates’ use of cash. Building and maintaining cash cushions and paying down debt are also widely anticipated behaviours from corporate Australia.

Investors therefore have little expectation of an uptick of corporate bond supply. Barely 20 per cent of survey respondents expect corporate issuance to increase at all and all those that do only expect it to do so “somewhat” (see chart 10). This is less than half the proportion that expect to see more issuance from the financial sector and from unrated credits.

One area where investors responding to the Fitch-KangaNews survey are optimistic about supply is in the sustainable-debt sector. More than 85 per cent of survey respondents flag an expected increase in this type of issuance in the year ahead, including nearly 20 per cent that believe this will be a “significant” increase.

Investment outlook

While the overall tone may be bearish, Australian investors do not appear to be withdrawing from markets nor to have any expectation of doing so in the coming months. Most expect to maintain credit exposure in the next 12 months. The proportion expecting to increase exposure – 28 per cent – is nearly twice as large as that forecasting a decrease (see chart 11).

The picture on duration is not dissimilar where, again, the majority of investors expect to be in a holding pattern in the coming 12 months (see chart 12). Survey respondents have not forecast a major change in credit exposure since H2 2016 nor in duration since H1 2017.