WATC debut provides the prelude for sovereign green-bond bow

Australian government-sector syndicated green, social and sustainability (GSS) bond issuance was steady rather than spectacular in 2023, though the year did produce an equal-record sized deal and a first-time transaction from a state issuer.

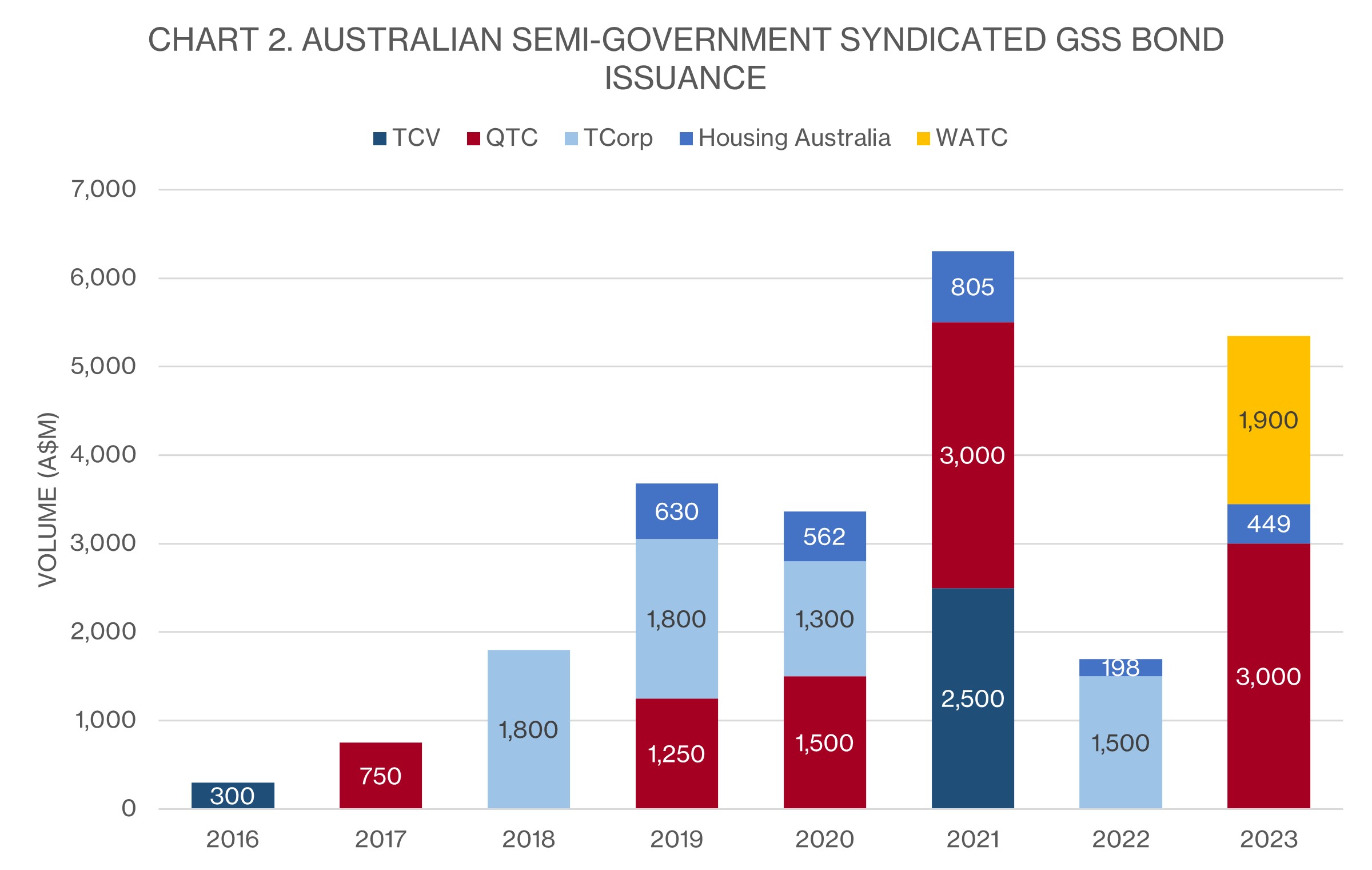

The record-sized deal came from Queensland Treasury Corporation (QTC), in the form of a A$3 billion (US$2 billion) March green-bond print that matched its own largest deal in the format, from 2021 (see chart 2). Three months later, Western Australian Treasury Corporation (WATC) debuted its own green-bond programme with a A$1.9 billion transaction.

Syndicated supply does not tell the full story of issuers’ willingness to print in GSS format. In June, Daniel Chandler, head of funding and sustainability at New South Wales Treasury Corporation, said:

Source: KangaNews 31 December 2023

“We have done about A$2.25-2.5 billion in reverse enquiries and tenders in [the GSS] space in the past 12 months, which has added liquidity to existing lines… We also carefully think about when we issue into these programmes: we do not want the market to go stale or enter a period of inactivity where no issuance happens.”

WATC noted particularly strong support for its deal, which was able to revise price guidance from 55-59 basis points over EFP at launch to 53-55 basis points at the first update, finally settling on a margin at the tight end of the updated range. The issuer said, however, that it was hard to unpick the bid for a WATC green bond specifically from general demand for an issuer with notable scarcity value given Western Australia’s limited debt requirement.

“It is hard to know the extent to which the support is green-bond related, though there were certainly a number of investors with a specific green lens,” Kaylene Gulich, chief executive at WATC in Perth, told KangaNews after pricing. “Others, though, responded positively to the detail we were able to provide on delivering broader ESG [environmental, social and governance] outcomes and the positive economic story. We are fine with both – we weren’t looking for demand that was ‘just’ green.”

WATC roadshowed in Australia, Japan, Asia and Europe ahead of pricing, to what Gulich described as a highly receptive response. “In my experience these were the most positive conversations we have had with investors across jurisdictions. My sense is that they were impressed with the breadth of the conversation we were able to have about the state government’s ESG credentials and economy – including a lot of interest in the look-through to the mining sector.”

The potential game-changer for government-sector GSS issuance is the arrival of the Australian Office of Financial Management (AOFM) as a green-bond issuer, which is expected to happen before the sovereign funding year ends in June 2024.

Such is the interest in the project that KangaNews surveyed Australian fixed-income 20 investors in May 2023 to gauge their preferences for local sovereign green-bond issuance. A key takeout is that investors will be paying close attention to the credibility of the transaction and the policy backdrop supporting it, even in light of significant progress on climate policy since the change of federal government in 2022.

Adrian Janschek, portfolio manager at First Sentier Investors in Sydney, acknowledged that Australia’s “well-known environmental perception issues” make labelled issuance “somewhat of a political novelty in the first instance”. But he also believes progress is being made at the policy level including a clear direction being set, such that the AOFM should not be afraid to sell a positive story.

Tamar Hamlyn, Sydney-based principal and portfolio manager, interest rate strategies and macroeconomics at Ardea Investment Management, has a greater level of concern. He explained: “The credibility issues are unfortunately significant. There is a risk that the domestic market underappreciates the extent of international negative perception about Australia’s enabled emissions.”

There could be a two-way effect here, whereby a sovereign programme either helps improve investor perception of Australia’s environmental commitments or suffers because of that perception. If the former outcome is to be achieved, investors say, it is vital that the programme be regarded as impactful and that GSS funding provides additionality.