Illiquidity bites New Zealand credit market

The New Zealand dollar corporate market appears to have battened down the hatches as COVID-19 has impinged on global markets. The specifics of local demand have shielded New Zealand from global volatility on occasion but market participants say the low-rate environment now leaves it more vulnerable to global moves.

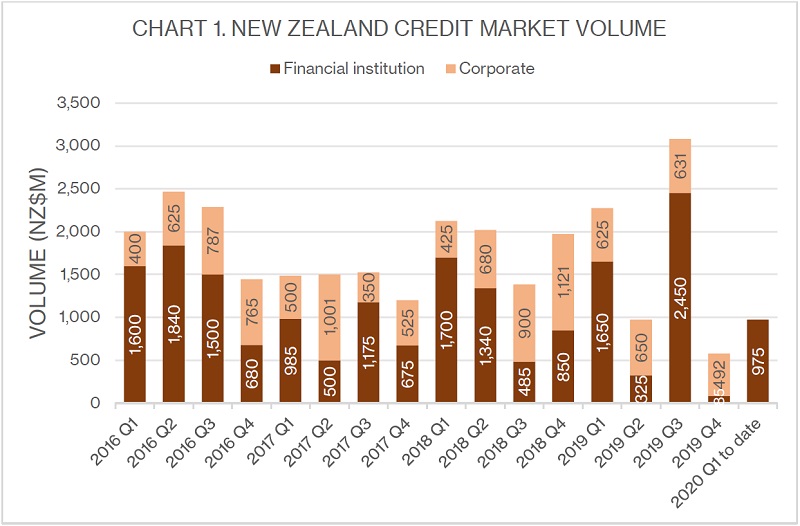

New Zealand credit was already off to a slow start in 2020. Just two new deals – from Bank of New Zealand (BNZ) and Westpac New Zealand – have come to market so far. In late February, Transpower New Zealand expressed its intent to bring a tap of its March 2025 line to market in mid-March.

Corporate supply is typically limited in the first quarter of the year, but New Zealand issuance looks set for back-to-back slow quarters (see chart 1).

Mat Carter, Auckland-based director, debt capital markets at Westpac Banking Corporation New Zealand Branch – which is mandated to lead the Transpower deal – says he remains confident of a pickup in primary supply over the rest of this year, provided a more stable and conducive backdrop emerges.

When that might happen remains to be seen. Intermediaries say primary deal flow offshore is probably a prerequisite for the market reopening in New Zealand.

In the meantime, Dean Spicer, head of capital markets New Zealand at ANZ in Wellington, tells KangaNews corporate issuers are unlikely to be forced into volatile markets. “Most of New Zealand’s corporate borrowers have come into this period with healthy maturity profiles and good funding diversity. They are well positioned and can weather some extended volatility,” Spicer says.

Source: KangaNews 12 March 2020

Liquidity issues

Secondary marks suggest New Zealand is outperforming its global peers – as tends to be the case during negative market moves. But local participants say this does not necessarily reflect a robust environment.

Mark Brown, Wellington-based head of fixed-income portfolio management at Harbour Asset Management, says little actual trading is happening. “Price makers are being defensive and marks are likely best-endeavours estimates, rather than true reflections of any market appetite,” Brown comments.

Fund managers gain a practical benefit from the lack of trading, explains David McLeish, head of fixed income at Fisher Funds Management in Auckland. “If assets are less volatile because they simply stop trading, this can help keep things from getting out of hand,” he says. “Less volatility reduces the risk of panic, which should reduce redemptions from funds, allowing managers to maintain positions without having to liquidate.”

This dynamic also has risks, though. McLeish notes that if fund managers do need to sell out of positions, the bid for those assets could be depressed or there might be no buyers at all.

But a sell-off does not appear likely, at least in the near term. Brown says Harbour made some changes to its positions when initially analysing the potential fallout from COVID-19. However, prices have moved sufficiently that the firm thinks the risks to specific companies are not evident enough to justify selling at current levels.

Diminished retail

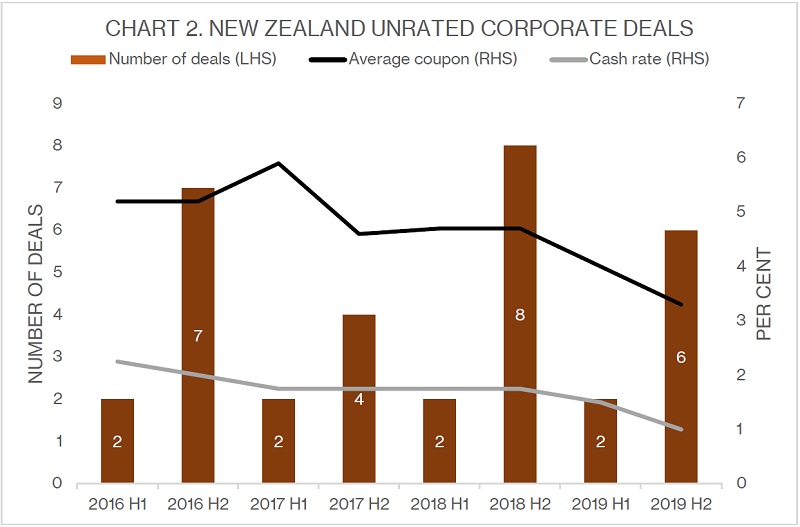

The large contingent of retail investors buying New Zealand corporate bonds has sheltered the market from global volatility in the past. Even in the shadows of the financial crisis in 2009, the market was open for business. However, New Zealand was in a fundamentally different yield environment then. The average coupon on unrated corporate deals in New Zealand has come down sharply in the last two years as the cash rate has fallen to 1 per cent (see chart 2).

Mike Faville, head of debt capital markets at BNZ in Auckland, tells KangaNews that retail investors will probably show less demand for unrated corporate bonds with rates at historic lows and the cash rate expected to be lowered further.

Source: KangaNews 12 March 2020

Shaun Roberts, head of debt capital markets at Forsyth Barr in Wellington, says unrated deals could come to the market with a yield of less than 3 per cent, although he acknowledges margins have widened to offset the fall in rates. Argosy Property successfully priced a deal at less than 3 per cent in late 2019 but that was in less-volatile conditions. One possibility that could push yields higher would be a sell-off in swap rates, Roberts notes.

Historically sticky bank deposit rates in New Zealand provide stiff competition for retail corporate bonds, particularly in times of market stress. Unrated corporate debt with potential coupons at about 3 per cent would have to compete with major banks offering 12-month term deposits at 2-2.6 per cent.

Still, intermediaries predict a corporate deal – even an unrated one – will be possible when market stability returns. Most of the market expects highly rated names to reopen offshore markets, but Westpac’s Carter asserts that there is retail cash available to be put to work in New Zealand for unrated corporates if coupon hurdles can be met.

“The key consideration is achieving an appropriate balance between the minimum coupon and the credit margin,” he comments. The Reserve Bank of New Zealand is expected to lower the official cash rate at its next meeting and Carter says this may crystallise investor acceptance of a lower-for-longer rates environment.

Forsyth Barr’s Roberts adds that when conditions do stabilise, the current bout of volatility may encourage more corporate treasurers and boards to reconsider the structure of their debt funding. In that case, the efficiency, diversification and tenor benefits of capital-market transactions could bring them into favour.

This could be particularly relevant in sectors where major banks may be less willing to lend because of tougher regulatory capital requirements the RBNZ imposed at the end of 2019.

Facilitating funding

In the near term at least, BNZ’s Faville says, if companies have funding needs or maturities to refinance, they would probably be inclined to access bank lines rather than risk a public debt capital markets transaction.

Bank liquidity could, therefore, become important, Faville tells KangaNews. BNZ and Westpac New Zealand were both able to price benchmark senior deals early in the year at 83 basis points over mid-swap. There were other transactions from the New Zealand major banks in offshore markets.

Vicky Hyde-Smith, Wellington-based head of New Zealand fixed income at AMP Capital, says measuring the spread movement of major-bank senior paper typically gives the best indication of market moves. These bonds have been marked about 20 basis points wider in recent days but Hyde-Smith thinks they could trade even wider than this.

She notes there is an extra layer of complexity for the New Zealand banks resulting from RBNZ’s increased capital requirements. “The major banks will likely begin to raise capital later this year and this should be a technical positive for major-bank senior pricing. However, in a risk-off environment, major-bank senior paper is typically the first to move wider, as it is the most liquid and the largest part of the credit market.”

New Zealand corporates that need funding would be well served by a return to stability offshore. Carter says New Zealand will probably look for stability and green shoots in global markets – ideally in increased offshore primary supply.

ANZ’s Spicer says banks should be able to help with liquidity in the near term but opportunities in New Zealand debt capital markets will return once there is some stability in global markets. The debt capital markets will then have a large role to play in identifying windows of opportunity to facilitate bank and corporate deal flow.

Watching brief

Fund managers agree one prerequisite for comfort in the New Zealand credit market is probably offshore deal flow. Until this emerges, Harbour’s Brown says, managers will remain cautious.

McLeish says Fisher, which manages both domestic and global funds, is beginning to see some buying opportunities, as credit spreads are now close to where they were in the sell-off of early 2016, when concerns about a slowdown in China were reverberating through markets.

“To put this further into context, since early 1999 – when our data series begins – global investment-grade credit spreads have been higher than now only about 30 per cent of the time. After a period of extreme over-valuation, global corporate bonds are finally starting to offer some value.”

But Hyde-Smith says while credit pricing is heading towards 2016 levels, it is too early to be taking on risk. “We are trying to marry credit levels with the broader economy so where the market moves from here depends a lot on the growth outlook,” she comments.

It is still early days for assessing the human and economic cost of COVID-19 and actions taken in response could still be disruptive. New Zealand will be led by larger markets, McLeish says.

Furthermore, he argues, given New Zealand credit tends to outperform as global corporate bond prices fall, the local market may land at unattractive levels, compared with global options, once volatility stabilises.

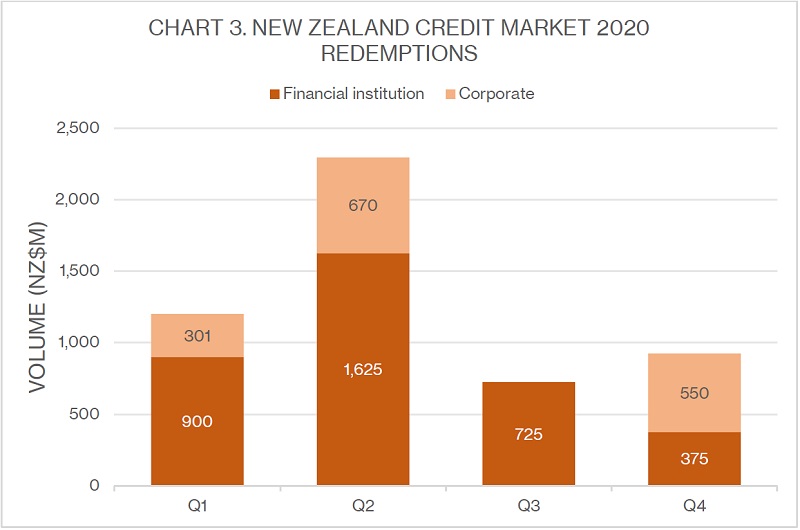

If there is a rebound for New Zealand credit, the second quarter appears to be the time when investors should have plenty of cash to put to work, as corporate and financial institution redemptions for the year will be peaking (see chart 3).

But judging the point when global markets might stabilise is difficult, given the nature of the crisis. Iain Cox, head of fixed interest and cash at ANZ Investments in Auckland, tells KangaNews the focus for now is on mapping the spread of COVID-19 and trying to assess the potential political and economic impact.

The likelihood of more government reactions such as in Italy – where the whole country has been put into lockdown – combined with self-imposed restrictions from businesses, creates a large and ongoing economic risk, Cox says.

Source: ANZ, borrowers 3 March 2020

In this environment, a flight to quality might be expected from fund managers and their end investors. The expected increase in supply from the high-grade sector might compound this, as could a relative widening in price for some of New Zealand’s high-grade names, Hyde-Smith asserts. Kāinga Ora – Homes and Communities and New Zealand Local Government Funding Agency have both recently indicated increased funding requirements.

Cox says it would be natural for some investors to move into more conservative portfolios, though this is not necessarily the right strategy if they are investing for the long term. He adds that the current environment provides vindication for taking a strategy with high-grade credit that treats bonds as the defensive assets they are designed to be, rather than as equity-like instruments.

KangaNews is your source for the latest on the COVID-19 pandemic’s impact on Australasian debt capital markets. For complete coverage, click here.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news