Buy side on hold

The Reserve Bank of Australia (RBA) jumped into the fog of dislocated debt capital markets in March with an unlimited government and semi-government asset purchase programme. Local investors are contemplating a cascade of market consequences.

Matt Zaunmayr Deputy Editor KANGANEWS

COVID-19 has brought a health crisis, an economic crisis and a funding crisis. The combination and its scale are unprecedented and all the factors are weighing on the minds of local fund managers. But with investment flows shifting rapidly in recent weeks, liquidity has been the pre-eminent concern.

In the early days of crisis acceleration, even the most reliable markets came under pressure as it became clear just how deep and broad the economic impact would be. Chris Rands, credit analyst, global fixed income at Nikko Asset Management in Sydney, says: “Liquidity in the government bond market was bad and bid-offer spreads were extremely wide. It was even difficult to execute switches where there was no addition of risk.”

He adds that the semi-government market was even worse, with price makers sitting on as much stock as they could handle with no-one to sell to. In credit, Rands says, the situation was almost impossible in bonds outside major banks. Nikko AM opted to stay out of the market entirely.

Amid the escalating COVID-19 crisis, on 19 March the RBA announced it would undertake unconventional monetary policy to restore normal market function.

The cornerstone is the unlimited asset purchase programme, with which the RBA is targeting a three-year Australian Commonwealth government bond (ACGB) yield of 0.25 per cent. It is buying bonds across the ACGB curve and in the semi-government market to achieve this. The RBA also wants to promote good functioning across the bond market.

Australian fund managers say the purchases have had the desired effect of pushing government bond yields down, at least at the target tenor, and stabilising the market. But fund managers remain extremely cautious as the crisis sails on into uncharted waters.

Carte blanche

The RBA has focused its attention primarily on the government bond market so far. By 7 April, it had purchased A$33 billion (US$20.3 billion) of ACGBs. It has been explicit that it will buy as many government bonds as is necessary to keep three-year yield at 0.25 per cent. By 1 April, the reserve bank had beaten this goal as the three-year ACGB was sitting below the target.

The RBA’s blank cheque for the federal government to print money allowed confidence among fund managers to get up off the floor, at least in the government bond market.

Stephen Cooper, Sydney-based head of Australian fixed income at First Sentier Investors, says: “The RBA has deliberately not constrained itself by balance-sheet limitations and this gives the market confidence it will do whatever it takes.”

Rands adds: “We saw liquidity come back as soon as the RBA began buying bonds. The government bond market out to 10 years is becoming liquid again. It is not where it was prior to March, but it is trading.”

The RBA is not acting alone. Central banks around the world have gone headfirst into larger monetary policy expansions than ever. The US Federal Reserve has made its purchasing programme free to do whatever it takes to keep the world’s largest economy afloat.

Beverley Morris, director, fixed income and absolute return at QIC in Brisbane, says the Fed’s move has supported liquidity and trading in sovereign bond markets globally.

As of 7 April, the RBA has purchased only as far out on the curve as the November 2029 ACGB. Even here, it has only transacted in minute quantity relative to the outstanding volume of bond lines around the 10-year point and to purchases in the three-and seven-year maturity buckets.

Accordingly, long-end ACGB yields have been less responsive so far to the asset purchases and the spread between the three-and 10-year ACGB remains wider than it was prior to the crisis. This has caused some consternation among fund managers, given the AOFM is expected to issue at least some of what will be a massive funding task into the longer end.

Whether market skittishness will require further intervention is a point of conjecture. If anything, the RBA is flagging tapering purchases rather than an expansion of its QE programme. The reserve bank stated following its April monetary policy meeting that if market conditions continued to improve it would probably be purchasing fewer government securities. This caused a spike in 10-year ACGB yield.

Sources familiar with the RBA’s purchase programme indicate it is unconcerned with the yields of government bonds away from its three-year target per se but will intervene to ensure the market is functioning.

Tim Hext, Sydney-based portfolio manager at Pendal Group, says the reserve bank will probably remain wary of dislocation in the market but that it also likely values the considerable freedom it has generated by avoiding metrics for success in the government bond market outside the three-year yield.

Analysts point out that the longer part of the curve is particularly susceptible to moves in the 10-year US Treasury bond and that this could make RBA intervention at the long end less successful – a fact that could stay the reserve bank’s hand.

Cooper says central bank policies regarding the long end of sovereign bond curves will have an impact on demand. “I suspect the RBA wants the curve to be positively shaped, but just how positive is a big question,” he suggests. “Other central banks, such as the RBNZ [Reserve Bank of New Zealand], appear to be targeting a very flat curve. Policymakers will have great influence over this but it will be interesting to see how conflicting goals between central banks play out.”

Work to do

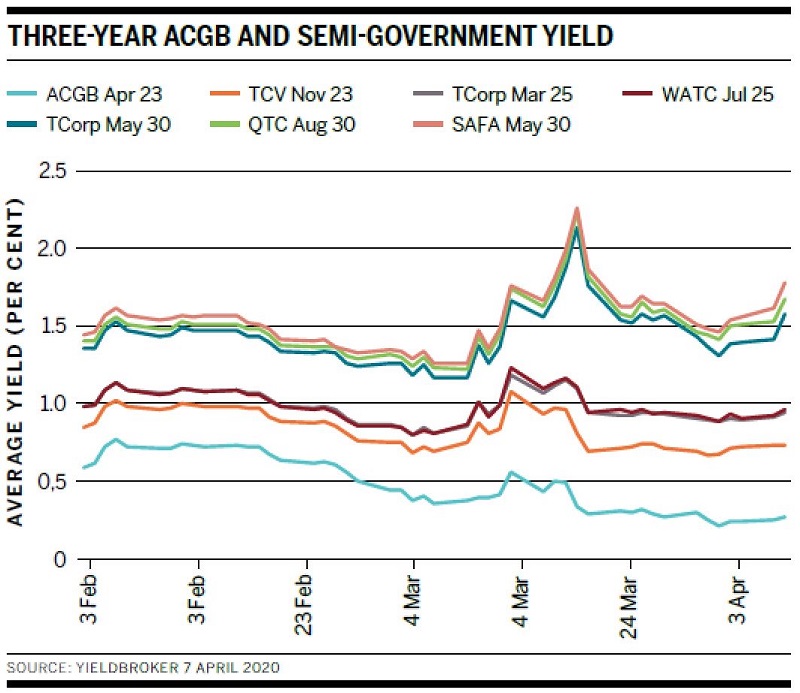

The RBA has dipped its toes into the semi-government market more cautiously, with A$5 billion of purchases in the first two weeks of the programme across all states and territories. The RBA’s initial focus has been on semi-government bonds maturing between 2026 and 2030.

The semi-government bond market came under more severe stress than the government bond market during early March volatility. State government budgets are expected to be hard hit by the economic fallout from COVID-19, given their reliance on property-related taxes and goods and services tax returns.

Compounding the downside risk, semi-government borrowers’ issuance tasks were already on the rise to meet massive infrastructure requirements. The sector took care of the majority of its pre-existing 2019/20 issuance task in January and February but those tasks are likely to be much higher now.

Semi-government yields rallied on the announcement that the RBA would purchase bonds in the sector (see chart). However, yields generally have risen even on days when the RBA has purchased semi-government bonds. As with the ACGB market, 10-year yields spiked when the RBA indicated it was prepared to pare back purchases.

Despite the RBA intervention, QIC’s Morris says the buy side remains cautious on semis due to the volume of additional issuance set to come. A flood of supply came from the sector at the end of March and start of April. Demand appears to be primarily from bank balance sheets with minimal participation from asset managers.

Morris says short-dated floating-rate note issuance and long-dated taps from some issuers illustrate that demand for the asset class remained patchy in early April, although most fund managers appear relatively confident that it should re-establish itself in due course.

Anne Anderson, head of fixed income and investment solutions, Australia, at UBS Asset Management in Sydney, tells KangaNews counterparties have become more selective in the bids they make, but over time a rhythm seems to be emerging that gives fund managers more confidence the RBA intervention is working to smooth the market.

The RBA will probably hold a significant portion of the government bond market in the coming months and years. This will have various consequences, but one will be to keep interest rates low and thus make spread product – which in this case includes semi-government bonds – relatively more attractive, Morris tells KangaNews.

However, she adds: “Investors will likely need to see some stability before participating in large size and I think the market has not quite got the required confidence yet. Given the RBA is not targeting a level of spread [for semi-governments], it may take a while for market participants to feel comfortable that the RBA’s purchases can offset the weight of supply. But we think the sector is attractive over the medium term.”

Credit conundrum

Australian dollar credit represents a different problem altogether. Government debt is still theoretically risk free, even though the crisis will hit revenues and fiscal programmes will put unforeseen burdens on budgets. The entire sector received a shot across the bow on 8 April, when S&P Global Ratings revised its outlook on Australia’s AAA rating to negative.

Still, the indefinite economic shutdown creates much more plausible risk of declining credit quality – and even default – across various corporate sectors. Much of the fiscal stimulus seeks to allay this risk, and the central bank is chipping in to free up the flow of capital as much as possible.

Nowhere is demand narrower than in the Australian dollar corporate credit market, which remained, in effect, shut in early April. Anderson says there are still challenges around finding market clearing levels. Scheduled FX rolls exacerbated this at the end of March as the decline in the Australian dollar expanded cash calls while some parts of the fixed-income market were not functioning well.

Corporate credit was excluded from the asset-purchase programme, as the RBA preferred to incentivise commercial banks to lend to corporates supported by a term funding facility.

In a speech in November 2019, RBA governor, Philip Lowe, expressly stated the central bank’s aversion to purchasing private-sector assets. The two primary reasons he gave for this were that there was “no sign of dysfunction in our capital markets that would warrant the reserve bank stepping in”, and that buying private assets “would insert the reserve bank very directly into decisions about resource allocation in the economy”.

Lowe added: “While there are some scenarios where such intervention might be considered, those scenarios are not on our radar screen.”

Whether that scenario is now on the radar is up for debate among market participants. Morris says the risk of corporate default in Australia remains very real and market functioning is severely impaired, potentially mitigating the RBA’s moral-hazard concerns about buying corporate paper.

Anderson says reduced capacity and risk appetite on bank balance sheets reduces the ability for the secondary market to find a clearing level. “The scale, breadth and inherent uncertainty of this crisis are very different and more challenging than the global financial crisis,” she argues.

A corporate asset purchasing programme has been in place in Europe for several years. The Fed has now implemented its own in the US. These markets had record volume of corporate supply in March, even as the COVID-19 crisis intensified. Morris says there is clear evidence that corporate asset purchases improve market function.

First Sentier’s Cooper has doubts about the efficacy of such a programme in Australia, however, given the dynamics of local corporate funding – which remains largely intermediated by banks, and the local big four in particular.

The euro and US dollar corporate markets are much larger and deeper than Australia’s. Cooper points out that corporate bonds make up only about 10 per cent of the Australian composite index and, therefore, argues that providing support to the government and semi-government bond markets should naturally lead to greater corporate liquidity. But he adds that fixed-income investors have all learned to “never say never” when it comes to central bank policy.

With the Australian corporate market seemingly shut for the time being, some fund managers are likely tempted by the deal flow, coming at newly established wider prices, in Europe and the US. Cooper says First Sentier is dipping its toes back into these markets, but market conditions are still not conducive to wide-scale portfolio rebalancing.

Paradigm shift

Specifically, liquidity across markets appeared to be too stretched as of early-to-mid April for fund managers to jump back in wholesale, even if they are starting to view the yield on many asset classes as appealing.

For confidence to truly return to the market, some fund managers are looking for a turnaround in the health and economic crises as well as the liquidity crunch. Cooper says First Sentier is looking for “peak news flow” on the coronavirus before it will be confident about meaningfully participating in primary markets again.

“Markets will gain confidence once there are signs of the infection rate slowing,” Cooper comments. “At this point, I expect liquidity to return to normal and flows to normalise. This would be the appropriate time to be adding risk and we would probably be paid appropriately for that risk for the first time in quite a while.”

He adds: “It is a timing game and we have, thankfully, been underweight risk over the last month or so. But we are looking for the time when we want to reverse this.”

At the same time, flows out of fixed-income funds and into other asset classes are likely to leave fund managers with little room for rebalancing of portfolios, at least in the near term.

Hext says central-bank policy, rather than fund managers taking a view on pricing and rebalancing allocations, will drive market stabilisation. “We were positioned defensively so have been okay, but a lot were caught the wrong way around and are still trying to sell. Ultimately, fund managers will be driven by flows of investment and divestment.”

Future market

How closely the market that emerges on the other side of the COVID-19 crisis resembles the one that went into it will depend to some extent on how successful central banks are in coaxing fund managers back into the assets they have been seeking to sell in March and early April.

Europe and the US have had impressive deal flow through the worst of the crisis, but those markets were already accustomed to large amounts of central-bank intervention. How the Australian fixed-income market responds remains to be seen.

Nikko AM’s Rands says the impact on the local credit market may long outlast the effects of the virus. “A lot of investors were running with a lot of credit and that was a difficult position to get out of when liquidity dried up. If the index is going to be 90 per cent government bonds, we need to think about the appropriate amount of credit to hold in a portfolio. We don’t want to be lumped with it when there is another stress event.”

Irrespective of how much future demand there will be for Australian dollar credit, what proportion of the credit market remains in the public sphere is a separate question given the RBA’s term funding facility could potentially account for all of the major banks’ immediate wholesale funding needs.

However, Hext makes the point that the major banks can and will still come to market if spreads tighten sufficiently or they wish to access funding for tenor longer than three years.

There will be much greater supply of government bonds. The Australian Office of Financial Management (AOFM) is planning to issue about A$5 billion each week by tender and also to introduce two new lines by syndication before 30 June 2020. New supply dynamics will affect the Australian composite bond index, which is already weighted towards government bonds.

Cooper says: “We will engage with clients and question the appropriateness of the composite bond index for what they are trying to achieve. If it remains appropriate, we are capable of managing our funds actively against it in the same way we always have. If it isn’t, we can also be flexible and adapt.”

Fund managers are also now contemplating big-picture paradigm shifts. The European, Japanese and US experience of QE indicates that it is not easy to unwind. Fiscal policy dominance is likely to be a feature of the coming decade and central-bank policy now appears to be coordinated with government policy rather than independent of it.

Hext says any notions about the inability of central banks to print money are being demystified. “The expansion of the RBA’s exchange settlement balances is evidence of this,” he comments. He adds that central banks have inadvertently moved into what could be described as modern monetary theory.

Morris says while markets are rightly focused on the short-term recessionary outlook, this policy paradigm shift is likely to have long-run implications for all asset classes. It may take time for the full picture to become clear.

Related news

Input complexity clouds Australian debt strategy outlook

KangaNews hosted its annual roundtable discussion for Australia’s leading bank fixed-income strategists in March amid a fast-changing world. While inflation, interest rates and geopolitical risk are on the rise, financial markets are not yet in crisis territory. The strategists agree Australia is in relatively sound financial shape as the world moves into a higher rates regime.

ESG to the fore as New Zealand business emerges from the pandemic

The agenda at the KangaNews New Zealand Debt Capital Market Summit in December 2021 included a panel of high-level local corporate executives who discussed how business responded to the challenges of the pandemic and the future outlook. Sustainability is playing an increasing role in corporate strategy.

New Zealand’s banks resilient despite lingering uncertainty

New Zealand’s banks are returning to a more normal business environment but the spectre of the pandemic remains. At the KangaNews New Zealand Debt Capital Markets Summit in December 2021, Daniel Yu, senior analyst at Moody’s Investors Service in Sydney, broke down some of the key themes the rating agency expects the country’s banks to face over the next 12 months and their credit quality.

The economic arc of recent history

Having celebrated his 30th anniversary with Westpac Banking Corporation in 2021, chief economist Bill Evans is in a unique position to view the challenges facing markets and economies thanks to his deep understanding of how they have responded to comparable events in the past. Evans speaks to KangaNews about the economic outlook, the wealth trade-off between wage earners and asset owners, the risk of deglobalisation and how sustainability is factoring in to his forecasting.