Global FIs step into Australia’s big-four bank supply void

The Australian dollar market hit a sweet spot for global financial institution (FI) borrowers in the second half of May despite the ongoing absence of the biggest local issuers. Intermediaries say the supply gap has caused a technical pricing squeeze that attracts issuers, while offshore FI pricing remains attractive to real-money investors relative to local names.

The Australian dollar FI market has steadily returned from the COVID-19 crisis and issuance has progressed down the capital structure since April. A clutch of Canadian banks reopened the market with covered bond deals. Suncorp and Bank of Queensland followed with their own covered bonds.

More recently, benchmark senior-unsecured issuance has returned. The second half of May saw a consistent flow of deals from bank borrowers either through local entities or in Kangaroo format (see table).

Table. Australian dollar FI deals since 12 May

| Pricing date | Issuer | Format | Tenor (years) | Volume (A$m) | Margin (bp) | Leads |

|---|---|---|---|---|---|---|

| 12 May 20 | UBS Australia Branch | Senior unsecured | 2.5 | 1,500 | 105/3m BBSW | ANZ, CBA, NAB, UBS, WIB |

| 19 May 20 | Credit Suisse Sydney Branch | Senior unsecured | 3 | 1,750 | 115/3m BBSW | ANZ, CBA, CS, NAB, TD, WIB |

| 21 May 20 | Macquarie Bank | Tier two | 10NC5 | 750 | 290/3m BBSW | ANZ, CBA, MB, NAB, WIB |

| 26 May 20 | Groupe BPCE | Senior preferrred | 5 | 650 | 160/swap | NAB, Natixis, Nomura, TD |

| 27 May 20 | BNP Paribas | Senior nonpreferred | 5 | 250 | 210/s-q | BNPP, CBA, NAB, WIB |

Source: KangaNews 1 June 2020

Adam Gaydon, Sydney-based head of syndicate at ANZ in Sydney, tells KangaNews the Macquarie Bank tier-two transaction on 21 May was the final piece of the puzzle for Australian FI market recovery, as it demonstrates that investors are willing to engage across the capital spectrum.

“It has been important that every primary deal that has come since the market was reopened in April has performed in the secondary market. This has given investors confidence and there are now very few accounts that have yet to re-engage with primary issuance,” Gaydon tells KangaNews.

Pricing dynamics

The Australian dollar FI market has been reshaped by the COVID-19 crisis – in particular in pricing dynamics. Traditionally, issuance has been dominated by major bank supply which offered other FIs – local and global – a clear and consistent benchmark for their pricing when coming to the market.

Substantial prefunding at the start of calendar 2020 and increased deposit flows since the COVID-19 crisis began has effectively nullified the major banks’ call on wholesale debt capital markets. Whatever funding gap that remains for the major banks can be filled using the Reserve Bank of Australia’s low-rate term funding facility (TFF), though even this has not provided substantial volume to date.

In fact, the TFF does not appear to have been a major drain on the Australian dollar market’s FI supply. By 27 May only A$5.8 billion had been drawn from the facility since it became operational in late March.

Market participants still expect the major banks will remain absent from the market for the time being, though. As a result, major-bank senior-unsecured bonds have rallied in secondary markets since April. Offshore FI names have rallied in turn in response to the lack of supply and relative to major-bank spreads.

Apoorva Tandon, head of Asia syndicate at TD Securities in Singapore, says this has made pricing in Australia attractive for issuers relative to offshore markets. At the same time, some international credits now offer investors a much larger spread pickup to the major banks than was the case before the crisis.

Josh Sife, Sydney-based director, capital markets origination at National Australia Bank, says the UBS Australia and Credit Suisse Sydney deals, like the Canadian bank covered bonds in April, launched with pricing in line with global markets. But he adds: “The senior-unsecured deals were able to generate strong demand through the bookbuild and were able to eventually price well inside these levels, both achieving a 15 basis points price tightening from launch.”

Liquidity returns

The first phase of FI issuance, which focused on Canadian bank covered-bond deals, was driven by demand from bank balance sheets. Measures taken by the RBA, such as its government bond purchasing programme and expansion in repo operations, have created a huge amount of liquidity for repo-eligible securities, says Sife.

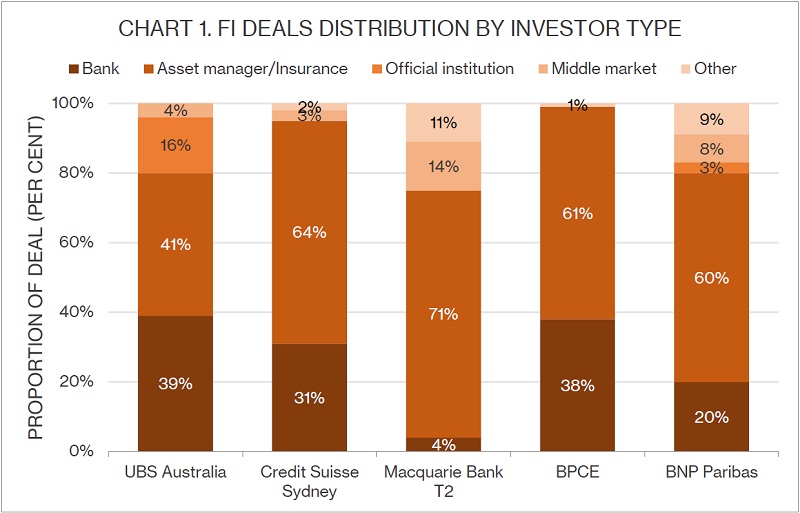

The buying base for FI deals broadened as the market moved through May, however, with the majority of all transactions taken by investors outside the bank sector (see chart 1).

In early May, the RBA expanded its criteria for repo-eligible securities to include investment-grade corporate bonds. Tandon says this could provide a further demand tailwind for offshore FIs that are not Australian authorised deposit-taking institutions as the repo criteria could be broad enough to include such names under a corporate designation.

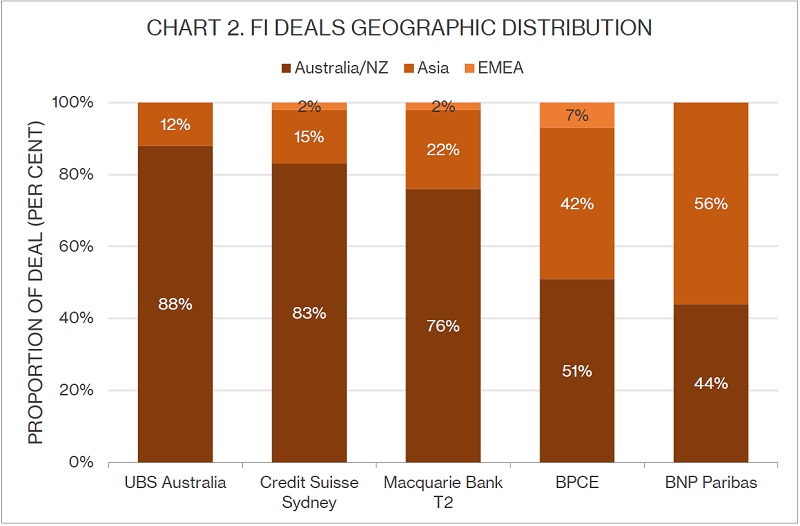

Demand from investors in Australia and Asia has been robust for the recent FI transactions (see chart 2). Tandon says there Australian dollar liquidity has build up among the Asian investor base, driving some bank demand for the recent transactions.

DCM candidates

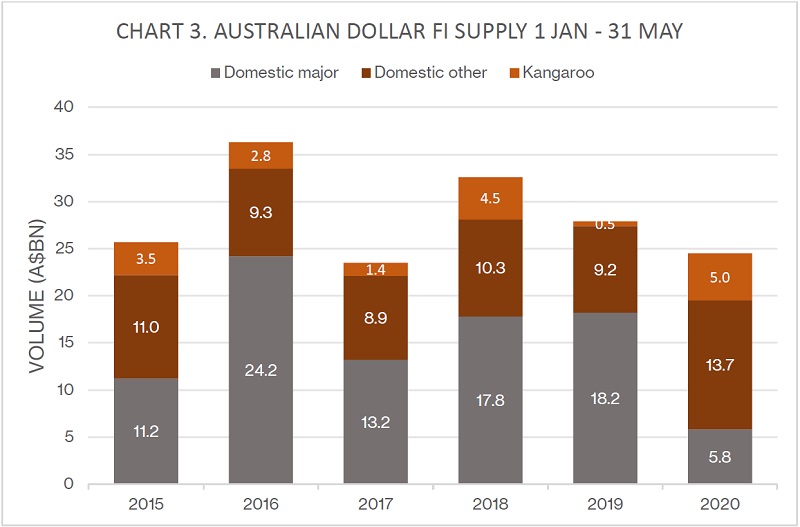

Australian dollar FI supply remains still well down on previous years – but not to the extent that may have been expected with the absence of major-bank supply (see chart 3). Meanwhile, KangaNews data show A$10.9 billion of Australian FI maturities between 20 March and 31 May.

The global banks that have issued through their local branches, UBS and Credit Suisse, are eligible to draw from the TFF through those branches. However, ADIs are only able to draw 3 per cent of the volume of their loans outstanding at 31 January 2020 through the TFF.

According to Australian Prudential Regulation Authority (APRA)’s monthly ADI statistics for April 2020, Credit Suisse has A$4.7 billion of outstanding loans and finance leases to Australian residents while UBS has A$5.5 billion. This would allow A$141 million and A$165 million of funding through the TFF.

APRA statistics show other banks that frequently fund through Australian branches, such as Bank of China, Bank of Communications, Royal Bank of Canada and others would have access to similar volumes or less, when their Australian dollar debt capital markets funding volumes are typically much higher.

Source: ANZ, National Australia Bank, TD Securities 1 June 2020

Source: ANZ, National Australia Bank, TD Securities 1 June 2020

Source: KangaNews 1 June 2020

The utility of the TFF for these banks is therefore likely limited. By comparison, Commonwealth Bank of Australia could access A$20 billion of through the TFF if it needed it, according to APRA.

Sife adds that liquidity conditions have been so strong in recent months that most banks have not started drawing on their TFF allowance. “The fact that most issuers are holding off drawing down on three-year funding at 0.25 per cent is an indication of how well funded the local bank market currently is. This dynamic is creating opportunities for global FI borrowers to step in and fill the void.”

KangaNews is your source for the latest on the COVID-19 pandemic’s impact on Australasian debt capital markets. For complete coverage, click here.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news