Decoding GSS in Australian fixed income

In May, Commonwealth Bank of Australia (CommBank) and KangaNews undertook a ground-breaking research project to learn more about Australian fixed-income investors’ green, social and sustainability (GSS) strategies. The results of the Fixed-Income Investor GSS Survey shine the spotlight on a market that has evolved significantly but remains a work in progress.

By Helen Craig and Laurence Davison

To see coverage of the investor roundtable discussing the survey results please click here.

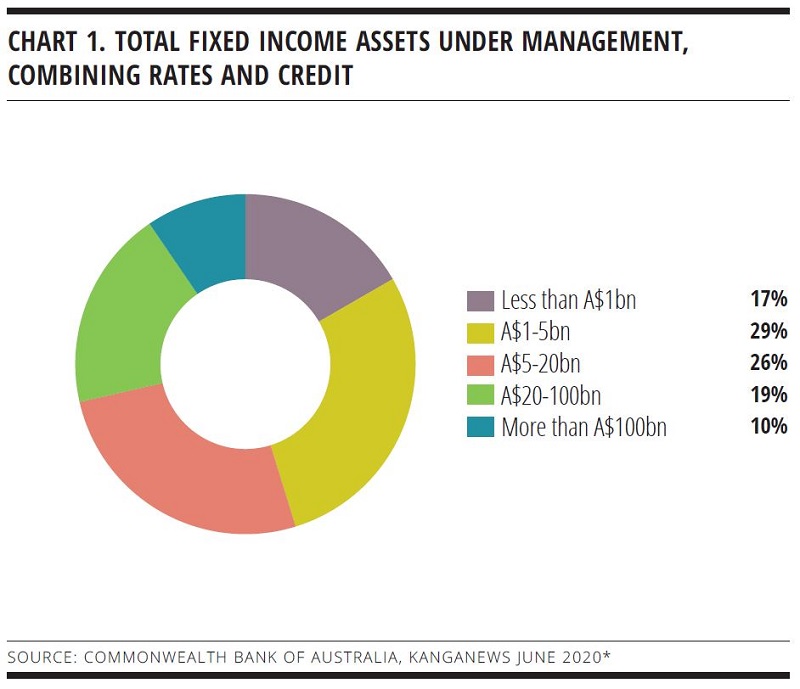

More than 40 investment firms completed the survey. All are Australian-based fixed-income investors, representing the full swathe of the institutional market from boutique funds to the local operations of global investment behemoths (see chart 1).

This is more than a representative sample: KangaNews is confident the bulk of Australian domestic fixed-income real money is represented in the survey.

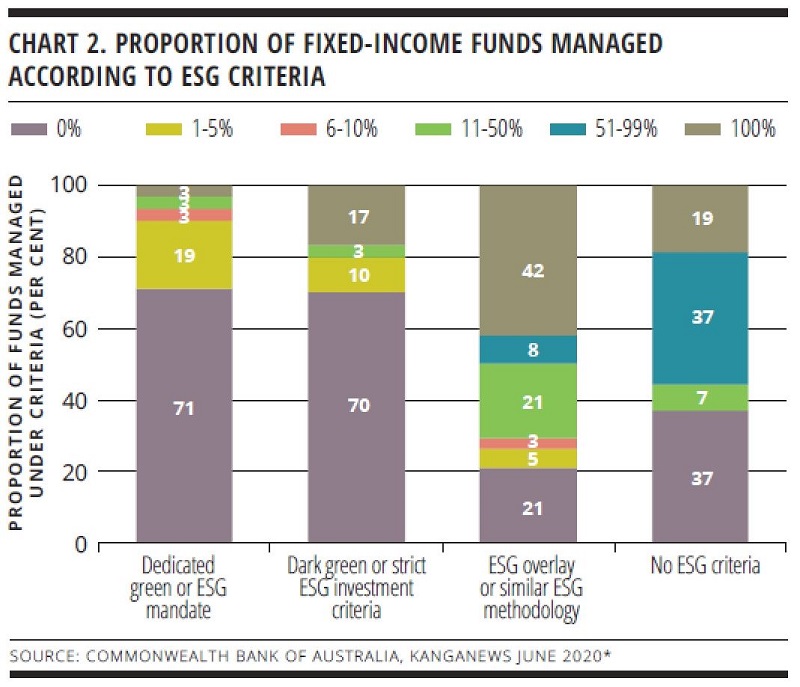

Unlike many environmental, social and governance (ESG) surveys, the CommBank-KangaNews project does not focus on specialist investors. The Australian investor base includes ESG focused funds but the survey’s aim is to incorporate these with views from mainstream fixed-income managers.

More than 90 per cent of survey respondents say their firms manage less than 5 per cent of their fixed-income assets under specific ESG mandates. On the other hand, more than 70 per cent of respondents indicate they apply an ESG overlay to more than 10 per cent of assets under management and more than 40 per cent have this approach across all their funds (see chart 2).

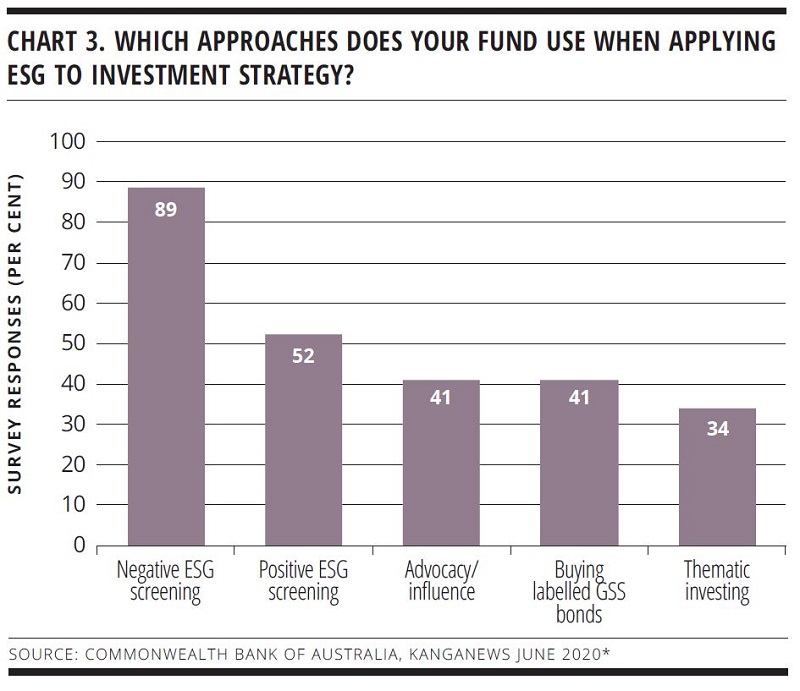

Despite representing the views of mainstream institutional investors, the survey suggests the Australian buy side is deploying a wide range of ESG practices. Negative screen remains the most widely used – nearly 90 per cent of survey respondents indicate they use this approach – but there is also significant takeup of positive screening, advocacy and influence, participation in labelled GSS bond deals and thematic investing (see chart 3).

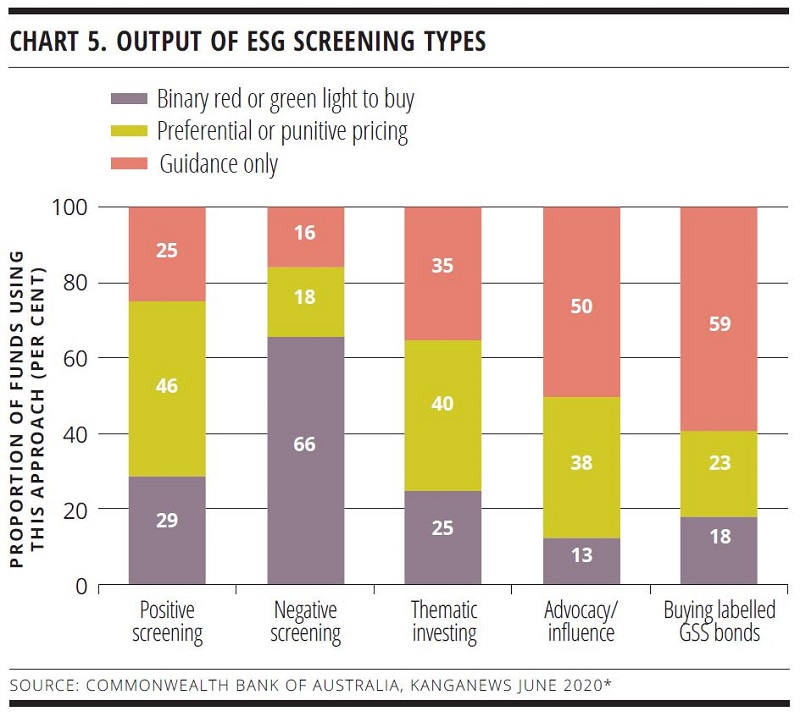

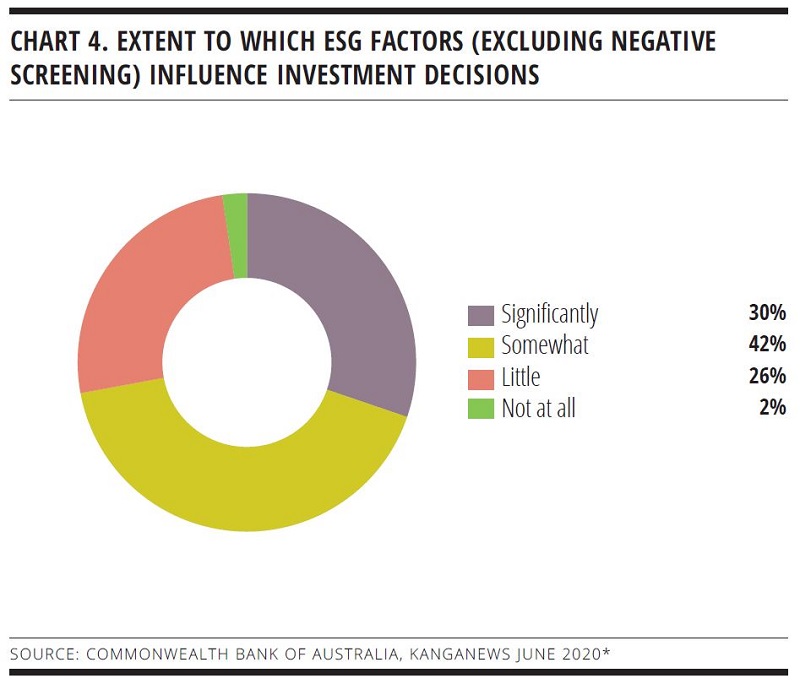

Investors also insist they do more than pay lip service to ESG factors. Nearly three-quarters of survey respondents say they play a “significant” or “somewhat” of a role in the investment process. Most individual ESG practices influence fund managers’ pricing decisions or produce outright red or green lights to buy (see charts 4 and 5).

The techniques most likely to produce a pricing output are positive screening and thematic investing: 40 per cent or more of investors say these approaches result in preferential or punitive pricing. It is harder to judge the precise impact of ESG approaches on pricing, however: the survey does not show how widely specific practices are deployed across an investor firm’s portfolios or suggest the proportion of aggregate funds that use each technique.

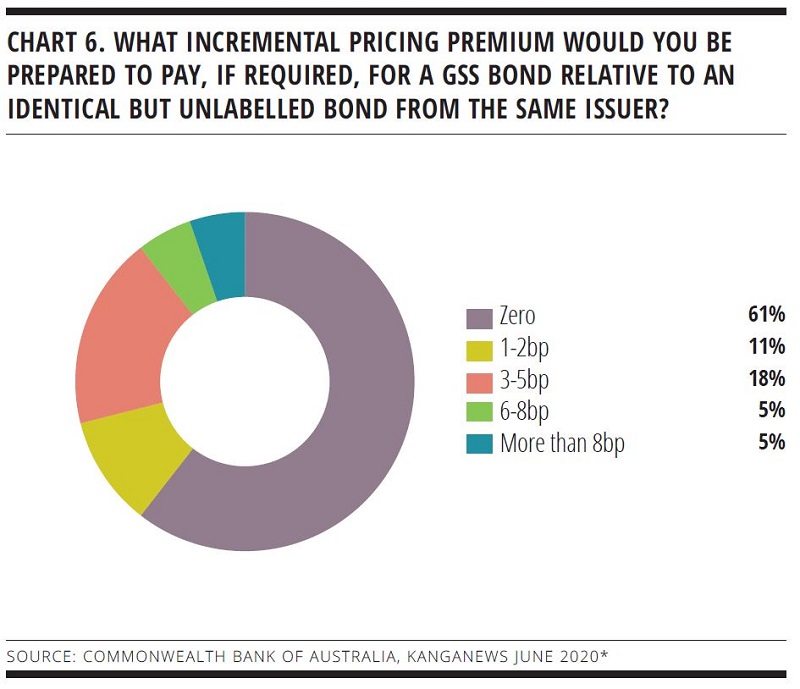

While the majority of survey responses indicate an unwillingness to pay a premium for GSS bonds, there are signs that a growing number is becoming willing to do so – at least at the margin.

At times, Australian market participants have suggested GSS bonds perform better in the secondary market and they may also print at tighter levels in the euro market in particular. Roughly 40 per cent of Australian fixed-income investors say they would contemplate paying some premium for labelled issuance, though 90 per cent would not offer a discount of more than 5 basis points (see chart 6).

Interrogating the data more deeply sounds another relatively positive note. While the subset of funds willing to pay a really significant premium for GSS bonds tends to comprise ESG specialists or boutique operations, the 29 per cent of funds willing to pay a 1-5 basis point increment are overwhelmingly large, mainstream asset managers.

Seeking preferential pricing does not appear to have been a major motivating factor for issuers of GSS bonds in Australia so far, though. Anecdotally, most if not all issuers say their reasons for coming to market with labelled issuance are not primarily economic and only one transaction has demonstrated a superior pricing outcome for green notes. Other issuers believe they have reduced the new-issue premium by using GSS format, though.

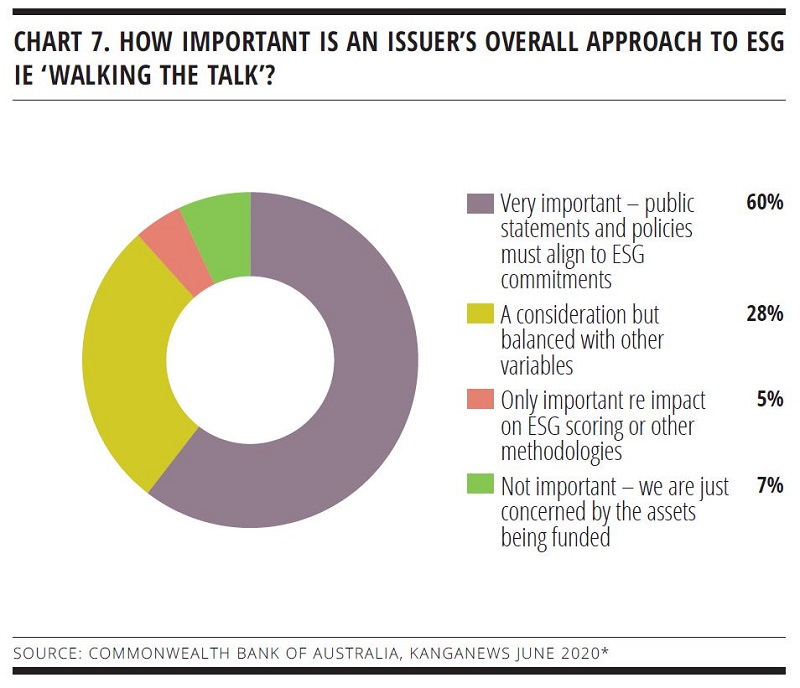

It has been suggested that labelled GSS issuance should be regarded as an interim step, bringing ESG to the forefront but eventually being superseded by a broader deployment of tools and practices by issuers and investors. Taken together, the survey data suggest the Australian fixed-income buy side is moving towards a broader application of ESG principles. Investors certainly report that they expect issuers to demonstrate a genuine commitment to their own ESG strategies (see chart 7).

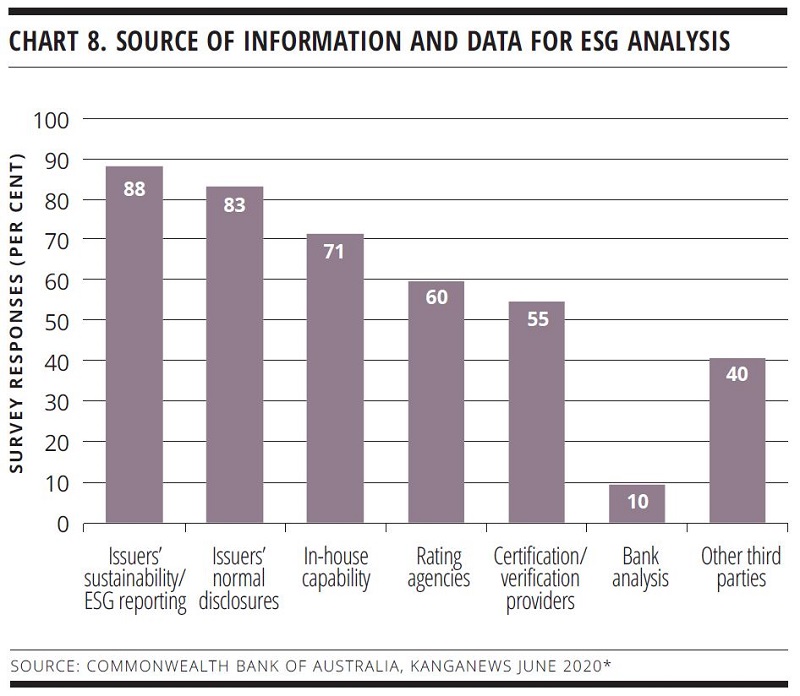

Investors are also asking for a wide range of information to support their ESG analysis: more than half of those surveyed use all of issuers’ sustainability reporting and normal disclosures, their own in-house capabilities, rating agencies, and third-party certification and verification providers to inform their ESG analysis (see chart 8).

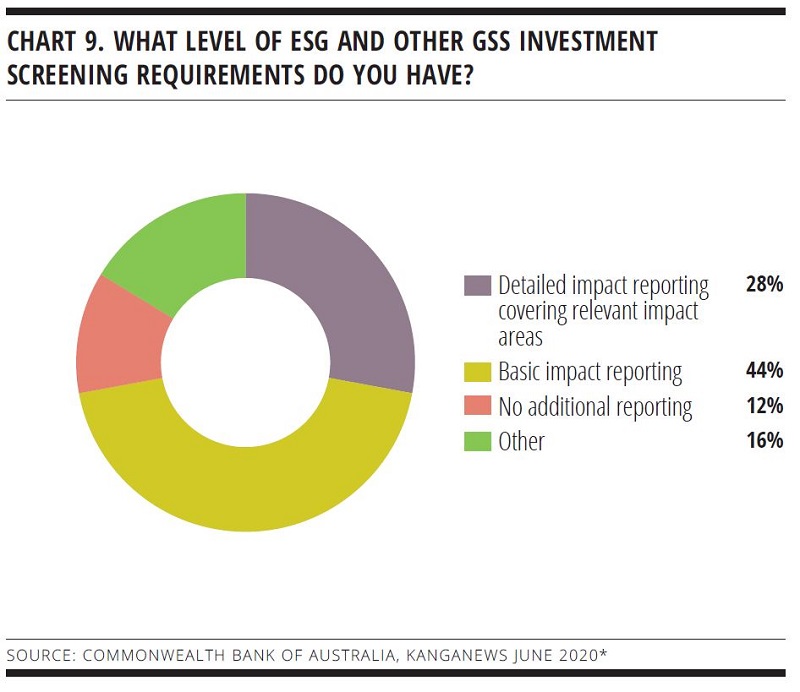

On the other hand, only 28 per cent of investors demand “detailed impact reporting covering relevant impact areas” – the majority requiring only basic impact reporting or no additional reporting at all (see chart 9).

Looking forward

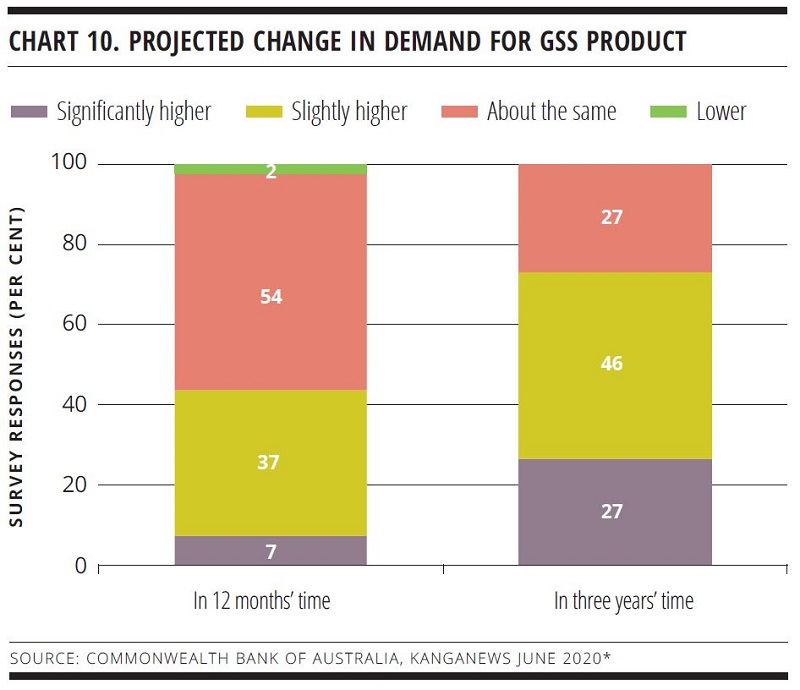

Australian investors clearly believe ESG is here to stay in the debt market. Despite the suggestion that differential pricing may be hard to come by, none expect labelled GSS issuance to be a flash in the pan. A healthy majority expect demand to grow over the next three years (see chart 10). The nearer-term outlook is somewhat less positive, however – and pricing may be critical here.

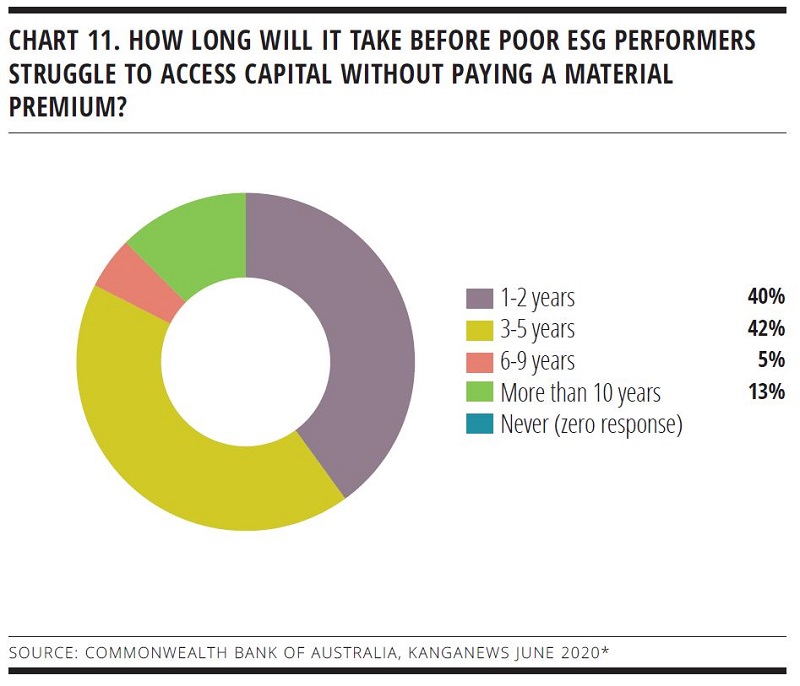

The key issue may be time, in the sense that price-based preference for good ESG performance will still take a number of years to assert itself. This perhaps chimes with the idea that the market is already moving towards a broader – and hence likely more complex – understanding of ESG risk on an entity level.

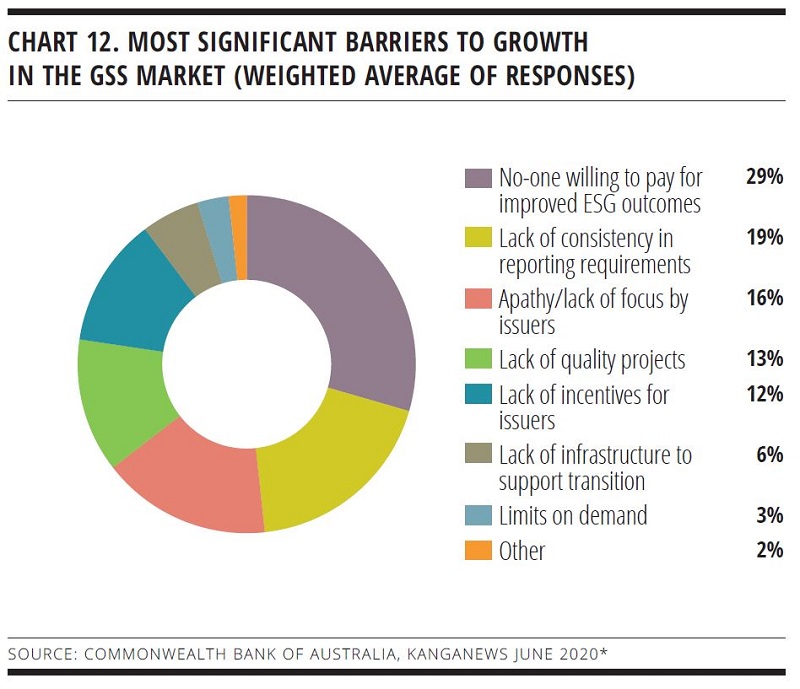

Only 40 per cent of survey respondents believe borrowers with poor ESG performance will need to pay a material premium to access capital in the next two years, though more than 80 per cent believe such a premium will emerge in the next five years (see chart 11). Meanwhile, “no-one willing to pay for improved ESG outcomes” is the most frequently named barrier to the growth of the ESG market (see chart 12).

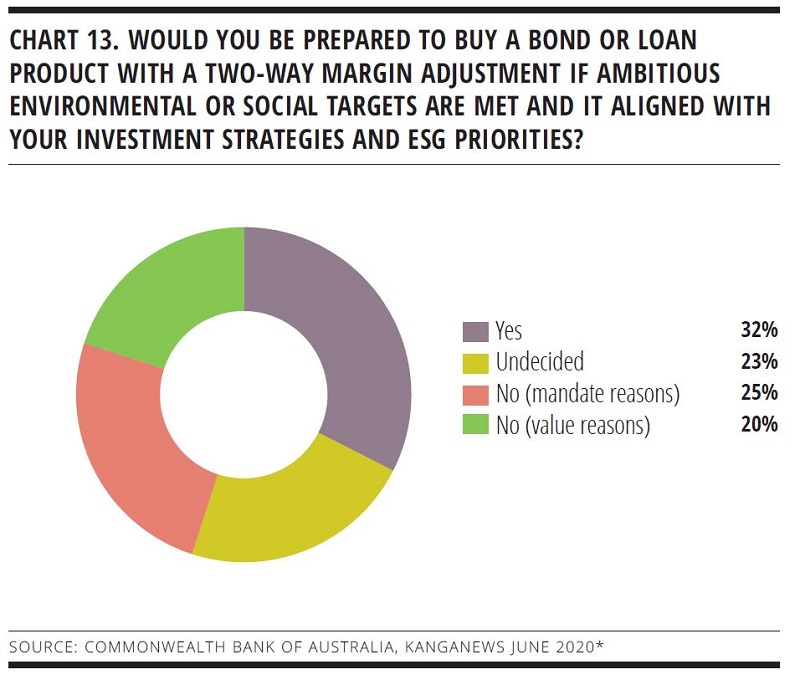

One solution might be two-way pricing on debt instruments that measure issuers’ ESG performance. Such securities are in their infancy, but Sydney Airport became a global leader by printing a sustainability performance-linked bond in the US private placement market at the start of 2020. More than half the respondents to the CommBank-KangaNews survey indicate they would at least consider purchasing this type of bond, and mandate change could take that number to 80 per cent (see chart 13).

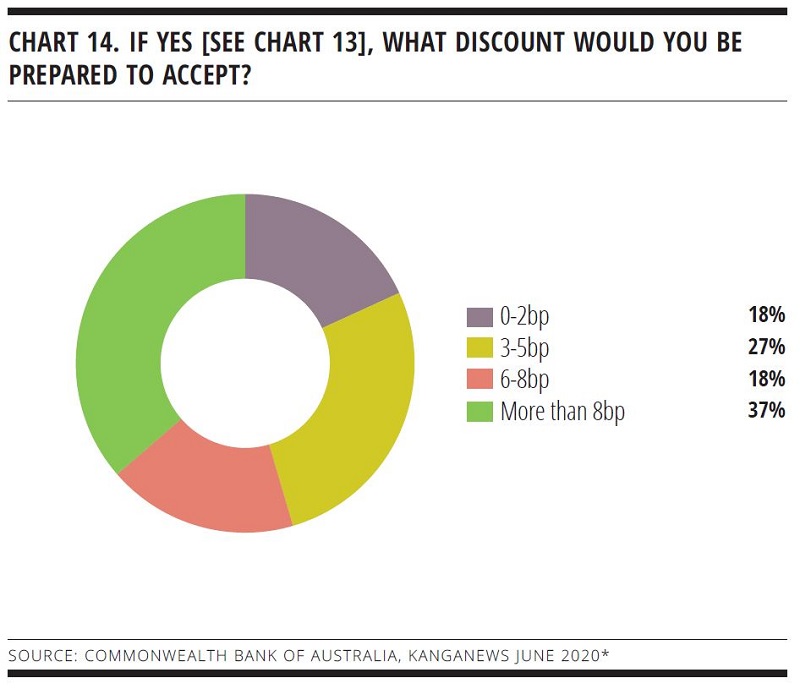

Importantly, those investors that would contemplate buying sustainability performance-linked product with two-way pricing incentives suggest they would consider offering a solid discount for positive ESG outcomes. Unlike standard GSS bonds, the survey suggests more than half of Australian investors would consider a pricing discount of 5 basis points or more for this type of security (see chart 14).

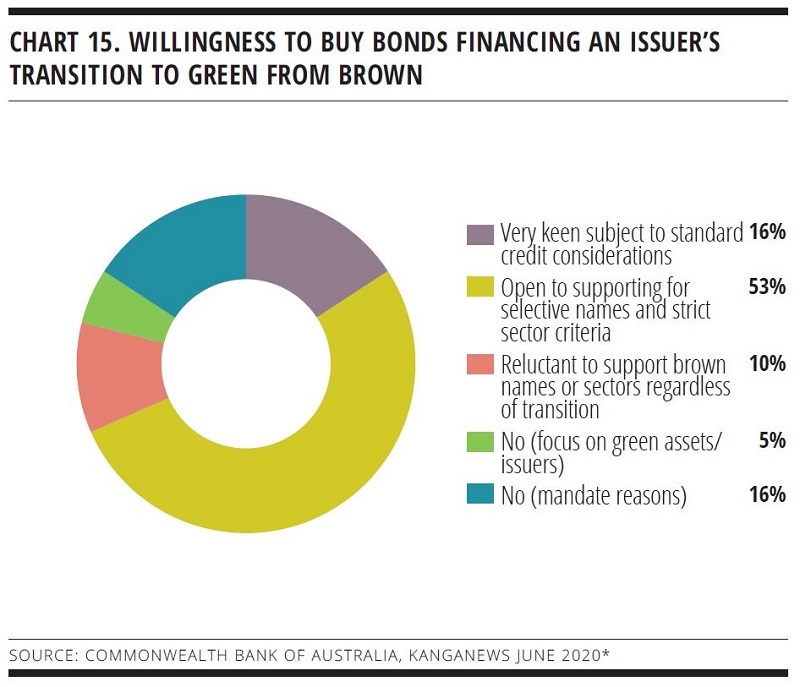

Investors are also generally willing to explore options for transition finance. While just 16 per cent of survey respondents say they are “very keen” to support brown-to-green transition instruments, a further 53 per cent say they would at least consider such issuance subject to credit and sector criteria (see chart 15).

In this case, virtually all Australia’s largest fixed-income fund managers say they are at least “open” to supporting transition finance, should issuers meet other ESG criteria. Perhaps surprisingly, most of the investors saying they are “very keen” to see this type of issuance are also large, mainstream asset managers. In fact, specialist ESG managers are more likely to be restricted to asset-level allocations.

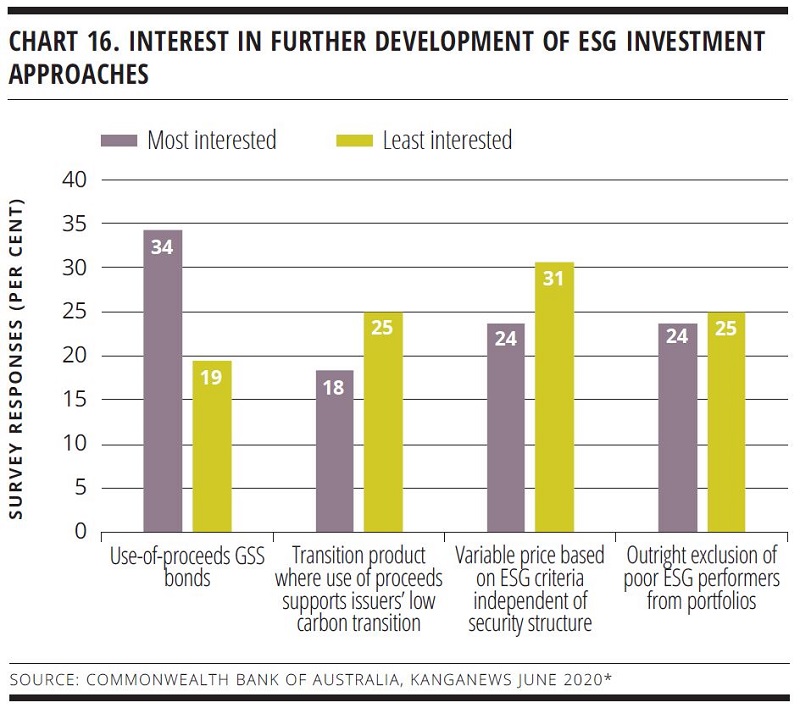

However, transition-based products do not feature heavily on the list of investors’ most preferred ESG approaches for further development. Fewer than 20 per cent name these as such, compared with the 30 per cent-plus that name use-of-proceeds GSS bonds as their area of most interest for further development (see chart 16). Meanwhile, 31 per cent of investors say instruments with variable price based on ESG performance are the area of ESG debt in which they are least interested in seeing development.

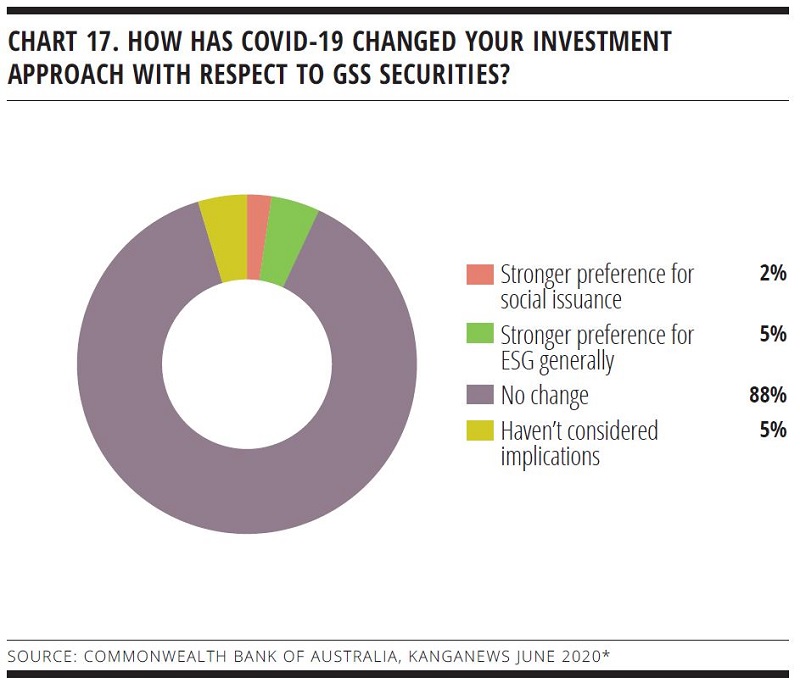

One area where the Australian investor base is clearly still working through the likely impact on capital-market practices and investment approach is the COVID-19 pandemic and its economic consequences. Global commentary has focused on the pandemic as a potential catalyst to expand social finance in particular – but the vast majority of Australian fixed-income investors say COVID-19 has not changed their investment strategy or that they have yet to consider its implications (see chart 17).

The timing of the survey may mean investors have yet to work their way through the implications of COVID-19 in full. The optimistic argument says the pandemic could make capital markets think about social issues in the same way as they have started to do about the climate crisis while simultaneously providing a real-world demonstration of what not taking sufficient climate action could mean for economies and markets.

On the other hand, even market leaders in the social-bond space say it carries complexities that have yet to be worked through in full. It should perhaps not be surprising to find that Australian fixed-income investors were not, as of May 2020, ready to draw conclusions about the impact of COVID-19 on their investment practices.

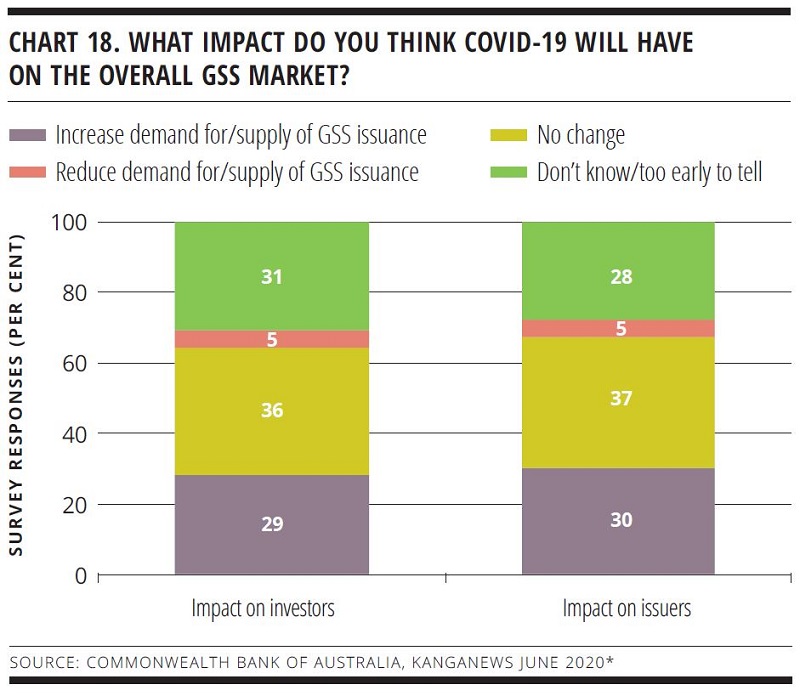

A reasonable number – around 30 per cent – of fund managers believe that COVID-19 will spark greater interest in GSS instruments on the part of issuers and investors (see chart 18). Hardly any expect the crisis will prove an impediment to further evolution of the market.

* All chart data compiled by KangaNews June 2020.

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.