Corporates find more crisis funding options

The economy-wide impact of COVID-19 has affected Australian corporate borrowers in a host of ways. But access to funds has generally remained in place as issuers navigate a path back to some type of normality – even for those in the most affected sectors.

Chris Rich Staff Writer KANGANEWS

Social-distancing measures, travel restrictions and the enduring potential for outbreaks have wrought havoc across the Australian economy. While the country appeared by the mid-way point of the year to be in a better place than many from a health standpoint, the worst of the economic impact may still be to come.

Unemployment jumped to 7.1 per cent in May from 5.2 per cent in March – when the lockdown restrictions were introduced, toward the end of the month. The increase was kept in check by people dropping out of the labour force altogether: the underutilisation rate, which combines the unemployment and underemployment rates, hit a record high of 20.2 per cent in May.

The federal government’s A$70 billion (US$48.6 billion) JobKeeper programme – designed to keep employees attached to their workplace by providing A$1,500 per employee per fortnight – is scheduled to end on 30 September with no transition plan in place, by 1 July, for the estimated 3.5 million employees covered.

There is growing commentary that the end of JobKeeper could represent an economic cliff, where support – and thus the relatively buoyant level of economic activity during the mid-part of the year – falls away vertiginously.

On the other hand, the volatility from the first few weeks of the crisis has seemingly been all but forgotten as equity markets have regained most of their losses since the Q1 sell-off.

Likewise, offshore debt markets were replete with corporate issuance even in the weeks after the immediate shock of COVID-19, as wider spreads and – later – central-bank support for the credit market in key global jurisdictions attracted investors back to the sector. In a 24 June research note, S&P Global Ratings estimates a total of US$1.6 trillion in new debt had been issued in 2020, a rise of 60 per cent over the same period in 2019.

Relatively early in the second quarter, Australian corporates waded back into global bond markets – particularly euros – and the bank debt market for their pressing refinancing needs. Meanwhile, an 18 May Westpac Institutional Bank research note says capital raising on the Australian Securities Exchange excluding IPOs topped A$9.2 billion (US$6.4 billion) in April 2020 – the most since May 2009.

QBE Insurance was the first Australian domiciled issuer to access the US 144A market since the escalation of the crisis, executing a US$500 million additional tier-one capital transaction on 5 May. It was later followed by Scentre Group, which issued a senior 144A deal.

The Australian corporate market took longer to adjust to new valuations and, market sources say, to clear an overhang of paper that was effectively blocking new issuance. With no corporate asset-purchase programme to assist, the market had to clear this backlog itself to prepare the path for new issuance.

However, Australia’s corporate deal pipeline was relatively robust in May and June. The number of deals was low but outcomes suggest volume is available to trusted names.

Woolworths Group was the first corporate to execute a transaction in Australian dollars since the COVID-19 crisis commenced, on 13 May. Investor sentiment had improved by then, with key breakthroughs including a settled sovereign yield curve and liquidity, and successful bank transactions.

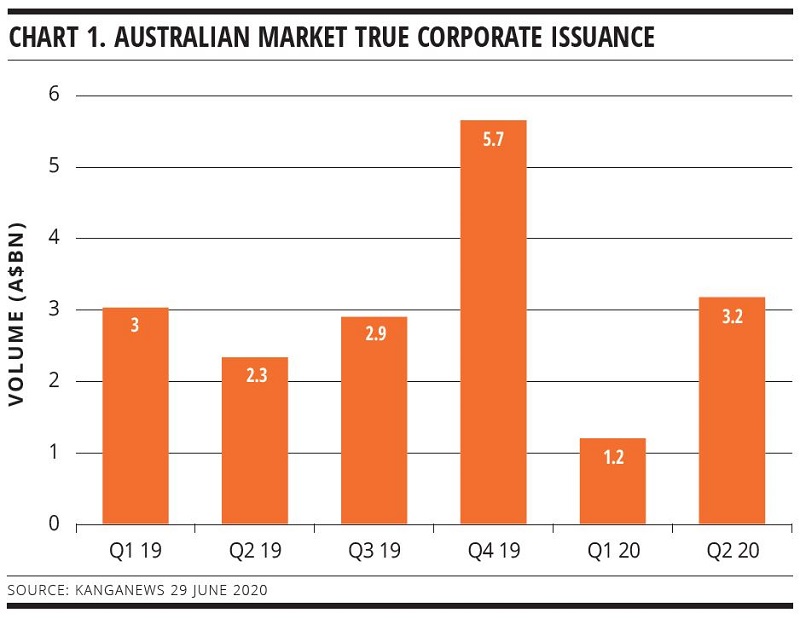

The final full week of June saw corporate issuance pick up strongly, with just less than A$1.9 billion printed in transactions from Brisbane Airport Corporation, Optus Finance and WSO Finance. In the end, the second quarter of 2020 actually saw more corporate issuance in Australian dollars than the same period a year earlier (see chart 1).

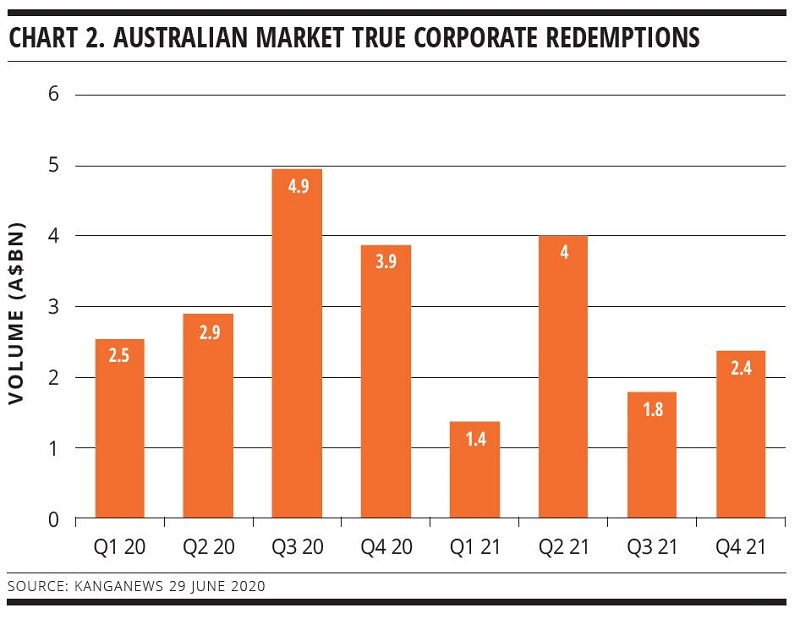

There should also be plenty of money to be put to work by investors as redemptions reach close to A$9 billion in the second half of the year (see chart 2).

Bank debt

Perhaps the biggest trend of the COVID-19 crisis in corporate funding has been the ability of most investment-grade companies to come through the initial maelstrom without major liquidity stress. In this sense, lessons from the last crisis appear to have been learned – assisted by the initial stickiness and relatively quick snap-back of liquidity across debt funding options.

The global financial crisis left many corporate borrowers in a tricky spot as bank liquidity dried up, including some international banks dropping out of the Australian dollar market altogether.

While COVID-19 saw equity capital issuance spike up across corporate Australia, the local loan market has not seen large-scale facility establishment and drawdown announcements akin to the trend among investment-grade corporates in the US and Europe, according to a 29 June Westpac research note.

Companies are refinancing and extending committed facilities, however. The Westpac research suggests sizeable corporate cash balances are available to provide support if needed – “a result of strong balance sheets and relatively limited capex programmes being undertaken by Australian corporates relative to historical levels”.

A flight of bank liquidity does not appear to have eventuated in the latest crisis, either. This is even the case for growth companies. For instance, Oskar Tomaszewski, chief financial officer at NEXTDC in Sydney, is optimistic about the firm’s ability to raise funds in the bank market.

“In part my confidence is because of our strong business, but it is also because I think banks are more mature, as a result of the financial crisis, in how they deal with a challenging credit environment,” Tomaszewski explains. “Banks have built relationships and do not want to throw them out the window over something that will ultimately pass.”

Airlines and airports

The airline and airport industries have faced the brunt of the COVID-19 fallout as international and even domestic travel has been effectively banned under Australia’s lockdown. However, debt has been available to most borrowers even in this most challenged of sectors.

Virgin Australia has to date been the highest-profile casualty of the crisis as it entered voluntary administration on 21 April. Qantas disclosed extensive staff layoffs in late June, demonstrating that Australia’s largest airline is far from out of the woods itself. Even so, Qantas was able to secure A$1.1 billion in additional liquidity in a bank facility issued on 25 March.

Sydney Airport also established A$850 million of new two- and three-year bank debt facilities, on 20 April. This is despite provisional data indicating a 96 per cent decrease in international passenger traffic and a 97 per cent decrease in domestic passenger traffic in the first 16 days of April versus the prior corresponding period.

The company has said it expects to see similar reductions in traffic for as long as restrictions on travel remain in place. Qantas announced on 25 June that it does not expect to fly international routes until mid-2021.

Michael Momdjian, Sydney Airport’s group treasurer, tells KangaNews accessing liquidity was relatively straightforward as relationship banks remain supportive. He says the competitively priced deal was oversubscribed without onerous terms and conditions given the borrower’s strong credit fundamentals.

Brisbane Airport demonstrated that capital markets debt, including in the Australian dollar market, can also be available to airport issuers. The company printed A$850 million of new bonds in late June with a healthy oversubscription.

Warren Briggs, Brisbane Airport’s treasurer, tells KangaNews the company had more than A$450 million of undrawn bank lines going into the crisis but “there was clearly a level of concern about how we would manage our liquidity requirements over the next 6-12 months”.

Before the bond deal, the airport secured an A$840 million, 18-month bank facility. “This ensured we had a strong liquidity buffer to get through whatever would come out of the pandemic,” Briggs adds.

Entering debt capital markets seems to be off the table for Sydney Airport for the time being, despite Brisbane Airport’s success. The reason is its relatively secure liquidity position.

At its AGM in May, Sydney Airport revealed it had a current liquidity position of A$2.7 billion comprising A$360 million in cash, A$1.8 billion of undrawn bank facilities, including the A$850 million of two- and three-year debt raised in April, and approximately A$600 million of new US private placement (USPP) bonds priced in February and settled in June.

Trevor Gerber, chairman of Sydney Airport, said after A$1.5 billion of debt maturities the remaining A$1.2 billion of liquidity is “more than enough to sustain operations for an extended period of time, even if the current operating environment were to persist for some time”.

Momdjian says Sydney Airport is comfortable with its liquidity position since establishing its additional bank facilities and receiving the funding from a USPP deal that priced as COVID-19 jitters were intensifying. He explains the additional liquidity buys the airport time to assess bond markets and provides a better story to tell investors.

Momdjian adds: “The uncertainty caused by COVID-19 has seen investors across our sector demand an additional spread on longer-dated bonds for what is expected to be a temporary event.”

Retail impact

Along with the airline, tourism and hospitality industries, the property sector has been one of the hardest hit. But, again, whatever is happening on the business front does not appear to have radically weakened access to markets or debt funding strategy.

David Rowe, treasurer at Stockland in Sydney, tells KangaNews the crisis has not changed the way the borrower thinks about its diversity of funding or its approach to market. Stockland’s debt book contains a mixture of USPP, EMTN, AMTN, bank debt and commercial paper. Rowe says COVID-19 highlights the importance of a diversified funding portfolio and access to a range of debt options.

On the other hand, Rowe adds: “Market disruption from COVID-19, and the the potential for further deterioration, compelled us to increase our liquidity position.”

As part of a market update on its third quarter results, Stockland announced an increase in available liquidity to around A$1.6 billion from A$850 million in February, after putting in place additional unsecured bank facilities totalling A$600 million and issuing a new 10-year HK$805 million (US$109.7 million) bond in February.

Moody’s Investors Service, in a 24 June research note, suggested most Australian real-estate investment trusts (REITs) have sufficient gearing buffers to withstand likely property-value declines during COVID-19, reflecting the sector’s overall conservative capital management. Declining property values, which are expected to drive up gearing for REIT portfolios, will largely reflect other credit metrics such as lower earnings and cash flow, the note says.

The retail component has been the most severely affected within the property sector and Stockland has the largest exposure to retail among diversified property companies. Moody’s says, though, that Stockland has significant buffers within its covenants and will only approach its rating threshold if its retail property values decline by more than 30 per cent.

Releasing its third-quarter 2020 results on 13 May, Stockland acknowledged the numbers do not fully reflect the impact of COVID-19 on its business. But it added that there are signs of improvement in its April figures.

Stockland has A$250 million of bonds maturing in the next 12 months and expects to pay them out with its current liquidity. As a frequent issuer in the euro and USPP markets, Rowe says the company will continue to look for opportunities in these jurisdictions as they recover further.

Higher education

The university sector is another that has been hard hit by COVID-19. Increasing demand from offshore for Australia’s highly-regarded tertiary education system has led to a significant proportion of international students enrolling at universities around the country. In 2019, international student enrolments were just shy of a million according to the Department of Education, Skills and Employment. This is a roughly 50 per cent increase from 2009.

The closed national border has staunched this revenue stream. Meanwhile, the government excluded universities from the JobKeeper programme despite the international education sector contributing A$39 billion to the Australian economy in 2019.

Universities Australia, the peak body representing the sector, estimates universities could lose A$16 billion in revenue between 2020 and 2023. Australia’s prime minister, Scott Morrison, announced a pilot programme to enable the return of international students, on 12 June, but there has been little other movement on getting international students back into Australia.

Laurence Zanella, treasurer at University of Sydney, says uncertainty around when international students will return has changed debt strategies. “We are thinking about funding if we don’t return to normality and our real concern is next year rather than this one. While liquidity is tough this year, it could be tougher next year – depending on what happens with borders.”

Consequently, University of Sydney is ensuring it has adequate liquidity via stand-by bank lines. The positive note is that this type of liquidity is available to higher-education borrowers. “We added to our existing bank lines and put additional ones in place just to give us extra liquidity and flexibility for 2021,” Zanella tells KangaNews.

But he adds: “If you have an existing arrangement, it has been a lot easier to refinance or extend that facility. If you don’t have an existing facility it is more difficult to get one in place, even with a relationship bank. There is more credit work required than there was six months ago.”

University of Sydney has a A$200 million bond maturing in 2021, and Zanella says it is not looking to refinance it in debt capital markets at this stage.

Planning ahead

While Australia’s public-health outcomes during the COVID-19 crisis have been among the world’s best, at least in the first wave of the virus, events in June demonstrate that the path back to an earlier earnings profile is not guaranteed for most companies. A spike in cases of the disease led to a second lockdown in Melbourne at the beginning of July and slowed the process of reopening borders. While the initial phase was a short, sharp shock, companies are now confronting a longer-term change to their business profiles.

On the other hand, the crisis will produce winners. NEXTDC, a data-centre provider, says there has been no noticeable change to its sales pipeline as a result of COVID-19. In fact, the increasing use of online technologies during the pandemic is a tailwind.

NEXTDC raised A$863 million in equity over April and May, consisting of a fully underwritten A$672 million institutional placement of new shares and A$191 million through a non-underwritten share purchase plan.

In a 2 April Australian Securities Exchange announcement, NEXTDC said the funds raised will support its growth agenda, “including the proposed development of a new data centre in Sydney together with balance-sheet flexibility required to accelerate and expand a range of growth initiatives in line with recent and expected material contract wins”.

Tomaszewski tells KangaNews NEXTDC’s plans for expansion could not be serviced by issuing debt due to its capital requirements. It expects the equity raising will meet funding needs for the next two years.

Already, though, NEXTDC has turned its attention to extending its runway by upsizing its debt stack. But as an unrated corporate it faces a more challenging road. “We have seen investment-grade credit improving, and even almost back to pre-COVID-19 levels. The subordinated or noninvestment grade credit markets are starting to show stabilisation and the green shoots of recovery, but they are not yet as robust as where we see investment grade,” Tomaszewski says.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news