Rapid renaissance

Asian demand has been a consistent component of the Australian dollar credit market in recent years and – to the surprise of some – has emerged from the first phase of the COVID-19 crisis as a still-reliable bid. Yield and credit quality factors are crucial, as the relative stability Australian credit offers attracts consistent demand.

Matt Zaunmayr Deputy Editor KANGANEWS

Demand for Australian dollar credit assets in Asia has been driven over the past decade by the Australian market’s combination of relatively high yields and high credit quality, as well as by growth in the volume of Australian dollar savings being accumulated by Asian fund managers, banks and insurance companies.

The relative yield story has eroded significantly since 2018 and this has caused some challenges to Australian dollar demand. But the other drivers of Asian investor interest were strong enough for this bid to remain a consistent component of the Australian dollar credit market until the COVID-19 crisis struck.

When the crisis hit, intermediaries say most international investors’ focus turned primarily to liquidity. This meant net selling for most markets around the world, including Australian dollars. In fact, even those regional investors that maintained significant Australian dollar risk in March-April may have done so due to inability to sell at cost-effective levels rather than preference for these assets.

On the up side, according to Owen Gallimore, Singapore-based head of credit strategy at ANZ, there was relatively limited panic selling from the Asian investor base during the crisis. In fact, he says demand from Asia – which often fluctuates in line with yield differentials – has been reassuring in its consistency throughout 2020.

Nervousness about the possible liquidity and price performance of the Australian dollar market that flared in the brief period of market dislocation appears to have dissipated by early August. Investors in Asia have been contributing a consistent portion of the books of corporate and financial-institution (FI) transactions, and intermediaries say their representation in deals continues to outstrip final allocation.

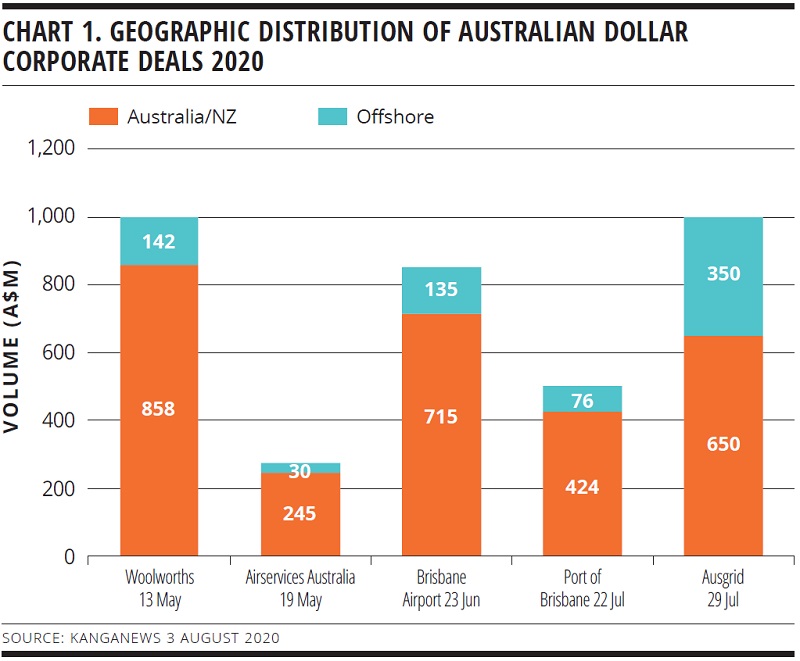

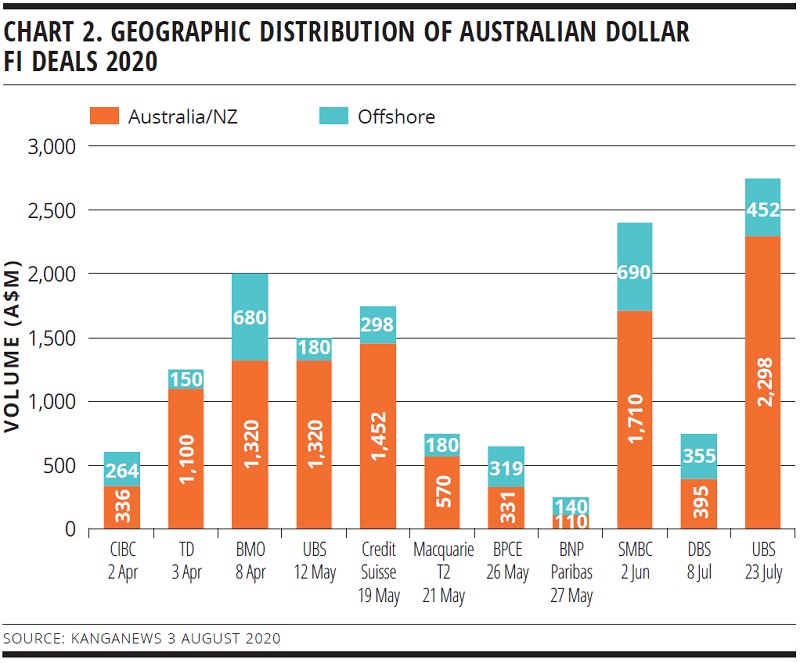

Most credit deals have tapped an excess of Australian domestic liquidity but offshore demand, made up mostly of Asian accounts, has also been a consistent feature since the market’s restart (see charts 1 and 2).

MARKET RELATIVITY

Part of the motivation for Asian investors re-engaging with the Australian dollar market may be necessity. Like investors in most regions, whether they are banks, asset managers or insurance funds, those in Asia have seen cash inflows resume in force since the depths of the COVID-19 market crisis.

Unlike buy-side counterparts in the US and Europe, Asian investors do not have a booming local market to invest in. Supply from Asia-Pacific borrowers in the Asia-focused US dollar Reg S market is down compared with 2019, while there has been a small increase in issuance in combined Reg S and US 144A format.

Lorna Greene, director, debt syndicate and origination, Asia at National Australia Bank (NAB) in Hong Kong, says Reg S pricing continues to be favourable. But she adds: “Execution certainty has been a key determining factor for issuers amid the backdrop of heightened volatility in the post-COVID-19 environment and this has led some Asia-Pacific borrowers to issue in Reg S and 144A combined format to maximise their potential investor base.”

Issuance in local currency markets such as Singapore and Hong Kong dollars is also down in 2020. Carman Lau, director and head of fixed income, North Asia, at HSBC Private Bank in Hong Kong, confirms that the US dollar market has been the main recipient of demand since the COVID-19 crisis. The challenge is that US investors are typically given preferential treatment in transactions with US domestic documentation – leaving a supply shortage for accounts in Asia.

Greene explains: “There are fewer options than before the crisis while liquidity remains strong. This is compelling investors to be open to doing credit work on more borrowers and to be active across more regional currency markets as they look to put money to work.”

In another sign of how readily markets have adapted to a socially distanced world, intermediaries in Asia report that the demise of in-person investor updates has been little or no impediment to the process of spreading the net (see box).

Even so, dealers say the fact that many regional investors are already familiar with the Australian dollar market can only be positive for demand in these unusual conditions.

The biggest challenge is the same as it has always been. The opportunity set in Australian dollars is limited compared with US dollars in particular. Daniel Leong, director, debt syndicate at Mizuho Securities in Hong Kong, says it is likely most investors in Asia will continue to favour US dollars as their economies are more tied to the currency, as well as for liquidity reasons.

Engaging the region

Closed international borders have not been an impossible obstacle for investor relations as markets have further embraced technology to stay in touch. However, in a maturing region such as Asia there is likely to be impetus for issuers to hit the road again once it is possible to do so.

There have been two key tenets for Australian issuers seeking liquidity from investors in Asia: patience and presence. The oft-repeated mantra has been that investors in the region may require several in-person meetings over multiple years before finally engaging in a deal. Once they do, though, they tend to be loyal and consistent buyers.

Australian companies undertaking extensive deal and nondeal roadshows in Asia and further afield may be off the table for the foreseeable future. But the buy and sell side have embraced virtual methods of engagement.

DUST SETTLES

Rates and credit spreads have rallied around the world in response to monetary and fiscal stimulus. Australia’s cash rate and three-year Australian Commonwealth government bond (ACGB) yield target of 0.25 per cent make it one of the few places where positive yield is still on offer in the short end for high-grade product. Meanwhile, the Reserve Bank of Australia (RBA)’s light touch in the long end of the ACGB market has meant a relatively steep sovereign curve.

Still, global investors hunting for yield had reason to turn away from the Australian dollar market in 2018 and 2019 as Australian dollar yields went below those of US dollars.

Lau tells KangaNews the effect has been a 90 per cent decline in HSBC Private Bank’s Australian dollar investment base over the past year. She adds that the Australian dollar performing well provides further impetus for offshore investors to exit the currency and she expects investable Australian dollar funds to continue declining in the near term.

Intermediaries believe this view is not widespread, however. Leong says: “The proportion of Australian dollars held in Asia continues to increase so natural demand for the currency is still there. Investment in the Australian dollar market will be determined by investor comfort on the economy, rates, liquidity and currency. At the moment these are proving resilient.”

Meanwhile, the credit quality of borrowers coming to the Australian dollar market has remained strong. For instance, with notable exceptions the bulk of corporate issuers in 2020 have been credits experiencing limited impact from the pandemic.

Gallimore says: “Marketing Australian dollar corporate deals to offshore investors has always been a case of pointing to ratings arbitrage. Not only are Australian borrowers often conservatively rated but they also usually offer a greater spread than international comparisons with similar ratings.”

The supply backdrop should see Australian dollar credit continue to perform. A confluence of factors has essentially eliminated major-bank supply since Q1, creating a technical tailwind for price tightening.

This could have positive and negative consequences for regional demand. Near-term performance may make the assets attractive, but Lau tells KangaNews the absence of major-bank supply, usually by far the largest source of Australian dollar credit, has further limited HSBC Private Bank’s participation in the market as it means a shortage of substantially sized primary-market opportunities.

The supply void has resulted in opportunities for global bank primary issuance in Australian dollars. Global bank spreads have rallied to levels competitive with offshore markets, while the spread offered to major banks means they are still relatively attractive to the Australian dollar investor base.

Global banks have taken advantage of this pricing sweet spot. Nonmajor bank Australian dollar issuance is up this year – though not to the extent that it fully replaces major-bank supply – and some banks have been able to issue in greater volume. Examples are Sumitomo Mitsui Banking Corporation Sydney Branch, which priced A$2.4 billion (US$1.7 billion) of three- and five-year notes in June, and UBS Australia Branch, which printed A$2.75 billion at the same maturity points in July.

Such names tend to be familiar to Asian investors, which can allow for greater regional investor participation in their Australian dollar deals – particularly those that are total loss-absorbing capacity-eligible or from holding-company borrowers.

Apoorva Tandon, head of Asia syndicate at TD Securities in Singapore, tells KangaNews the volume bump available to banks in Australian dollars provides something of a virtuous circle. It means a broader spectrum of investors in Asia can participate, including new and some returning investors from the region.

Major-bank supply is not expected meaningfully to return in 2020, which could pave the way for further spread tightening. UBS Australia priced Australian dollar deals in May and July. Its May deal was a 2.5-year floating-rate note (FRN) deal that priced at 107 basis points over three-month bank bills. Its July three- and five-year transaction printed at 67 and 87 basis points over swap benchmarks.

Will Gillespie, director, frequent issuer coverage and syndicate, Asia at NAB in Hong Kong, says if this rally is sustained it may end up with all-in levels that are no longer attractive to investors in the region. So far, though, he adds, demand remains robust.

The lack of bank supply is not just an Australian dollar phenomenon, though. Globally, banks are taking advantage of government support and thus have less need for senior funding. Tandon says this affects the Australian dollar market in two ways.

First, Australian dollars is primarily a senior bank market so there is less aggregate supply available. Second, the global supply void is resulting in the same tightening pressure in major markets that has been seen in Australian dollar credit – and typically to a greater extent. This could produce a disincentive to issuers as significant as the impact declining outright yield has on investors.

“The secondary market in Australia has been performing well. But if it does not perform in synch with the US dollar market it will be very difficult to attract supply from global banks,” Tandon explains.

He adds, though, that there is strong demand from Asia for Australian dollar FI product, particularly in private-placement format for long-dated, higher-yielding capital deals. This creates a good opportunity for issuers to extend curves and access capital funding at a competitive price.

Asian demand has been sufficiently strong to spur NAB’s treasury into executing three long-dated, tier-two Australian dollar deals from its GMTN programme in early August. KangaNews understands these to be the only deals executed by an Australian major bank between February and August, except for NAB’s domestic wholesale AT1 print in July.

DEVELOPED POSITION

Along with the yield and credit quality of the Australian dollar market, some further factors have emerged from COVID-19 relief measures that are likely to enhance Asian demand.

According to Gallimore, the Asian investor base appears to have overcome what has been a consistent roadblock in recent years – Australia’s absence from the J.P. Morgan Asia Credit Index Core. He says most credit flows in the region are passive so being off index has been an impediment.

Familiarity may have changed the story. Gallimore explains: “Over time, investors have come to understand the Australian credit landscape. They know the ports, airports, toll roads and utilities sectors after many years of engagement and are therefore happy to invest in these names through the cycle.”

The Australian dollar market is also potentially a beneficiary of the country’s ability to withstand the economic downturn precipitated by COVID-19. By early August, the spread of the virus in Australia remained relatively contained albeit with concern around an outbreak and second lockdown in Victoria. Crucially, the ability of the government to provide ongoing support stands Australia apart from many of the Asian region’s emerging markets.

Tandon says the consensus view is that Australia is well placed for economic recovery from the COVID-19 crisis and that this safe-haven status, along with the RBA’s accommodative policy, is likely to enhance the existing factors that have been drivers of natural demand for Australian dollars in the region.

OFFSHORE OPTIONS

For many investors in Asia, liquidity and currency mean the preference is still to access Australian-origin credit in regional or global markets. While the record volume on offer in the Australian domestic market may slow this impetus, its ongoing yield and liquidity considerations are drawing investors in different directions. It stacks up favourably for yield-driven buyers, while investors with a liquidity axe are still more likely to be enticed by the US dollar and euro options.

In this case, Australian dollar yield may not be sufficiently higher than other markets to offset its lower level of supply and liquidity, Lau says. “We do not see Australian dollar yields getting back to where they were a few years ago any time soon, so our investment preference is likely to remain away from the currency.”

Gallimore says investors that have been familiar with the Australian dollar market for a while, such as those in Japan and Korea, are more likely to be comfortable investing as long as the basis swap is favourable. Newer investors are more likely to be focused on liquidity and therefore drawn to US dollars.

At the beginning of the COVID-19 crisis, while the Australian dollar credit market was still closed, a steady flow of Australian corporates accessed the euro and, less frequently, the US dollar markets. In the past, Asian investors have often been large buyers of Australian corporates’ US dollar deals in particular – as well as those of the big-four banks.

However, the recovery of the Australian dollar corporate market has meant less impetus for corporate borrowers to go offshore, as larger-than-average volume was possible at home for much of Q2 and beyond. Meanwhile, the major banks have been absent from global markets for the same reason they have not been issuing at home.

Australian corporate borrowers have sporadically issued in US dollar Reg S format since 2017, and Greene says there are opportunities for issuers to access large pockets of demand. However, a lack of secondary-market turnover appears to be a stumbling block.

“Triple-B corporate issuers’ bonds have not been actively traded in the secondary market so they have remained relatively wide since the crisis. But these prices are not indicative of where a deal would be likely to price in the current environment. New primary deal flow post the initial COVID-19 market disruption has priced inside secondary levels and we continue to see investors considering a wider set of sectors when determining fair value,” Greene comments.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news