Flux capacity

New Zealand market participants gathered virtually on 20 August for the ANZ-KangaNews New Zealand Capital Markets Forum (NZCMF). New Zealand’s economy, politics and COVID-19 response are setting the market’s parameters, and discussion focused on managing through and beyond the current rocky patch.

Matt Zaunmayr Deputy Editor KANGANEWS

The 11th NZCMF was originally due to take place in March. The onset of COVID-19 meant it was rescheduled to August, when the country’s successful elimination of COVID-19 would have enabled the market’s first chance to gather in person since the crisis began. However, days out from the event a new, locally transmitted, outbreak of COVID-19 emerged in Auckland. This threw New Zealand back into lockdown mode and the conference into the virtual sphere.

Organisers, participants and delegates manoeuvred quickly to deliver the agenda as planned via the KangaNews virtual event hub. The conversation remained unchanged, with the focus on the post-COVID-19 economic outlook, fiscal policy heading into an imminent election, and the Reserve Bank of New Zealand (RBNZ)’s ever-expanding market intervention. The new outbreak of COVID-19 in the country and its return to lockdown measures added a further layer of uncertainty to the mix.

Despite acknowledgement of the obvious challenges, a consistent theme running through the panels and presentations was the possibilities New Zealand’s capital markets and economy have in front of them.

In his opening address, Andrew Allan, head of global markets, New Zealand at ANZ, told the audience at the online event: “The impact of the pandemic is a recurring theme, as is the impact of the unprecedented policy response of the government and the RBNZ. However, we also want to highlight innovation and the ways in which New Zealand companies can continue to be successful in global markets.”

“Over time, we need a way to ensure our borders are open. This will rely as much on what is happening in other countries as here. We will be following progress on vaccines and continue to explore the possibility of travel bubbles. However, our border policy has been crucial to our COVID-19 control.”

“Markets were very dislocated in March and liquidity was very challenging. Those of us that went through the financial crisis in 2008 thought we had seen the worst markets could throw at us, but this period was reminiscent of that – although with a different cause.”

SETTING THE SCENE

New Zealand’s economic situation is inextricable from its COVID-19 response. New Zealand is one of only a couple of countries around the world pursuing outright elimination of the virus instead of suppression. Until mid-August, this was going well as the country recorded more than 100 days without local transmission.

Sharon Zollner, chief economist at ANZ in Auckland, said at NZCMF that countries which have successfully controlled the virus have shown a better rebound in economic activity. This still means less bad, rather than outright good, performance: Zollner said the only reward for dealing well with the health crisis is a recession.

“The economy had a surge immediately after the first lockdown ended as there was pent up spending capacity,” she added. “But we are going into a recession due to the loss of tourism. Alhough this will not be fully felt until the end of the year, businesses know it is coming and are reflecting it in their intentions and expectations for investment, employment and profits.”

The response of the RBNZ and central government has been unprecedented stimulus. The former expanded its large-scale asset purchase programme (LSAP) to NZ$100 billion (US$66 billion) from NZ$60 billion in the week prior to NZCMF.

The latter’s fiscal response has seen New Zealand Debt Management’s 2021 financial-year borrowing requirement rise to NZ$60 billion with more expected in the government’s delayed pre-election fiscal update, due on 16 September. The election itself has been postponed by four weeks to 17 October.

New Zealand’s minister of finance, Grant Robertson, told conference delegates New Zealand’s finances remain relatively stable despite the record spending. “New Zealand is in a strong position with a robust balance sheet, which means we can manage higher levels of debt. We will bring this down over time but at the moment the spending is important to manage the crisis.”

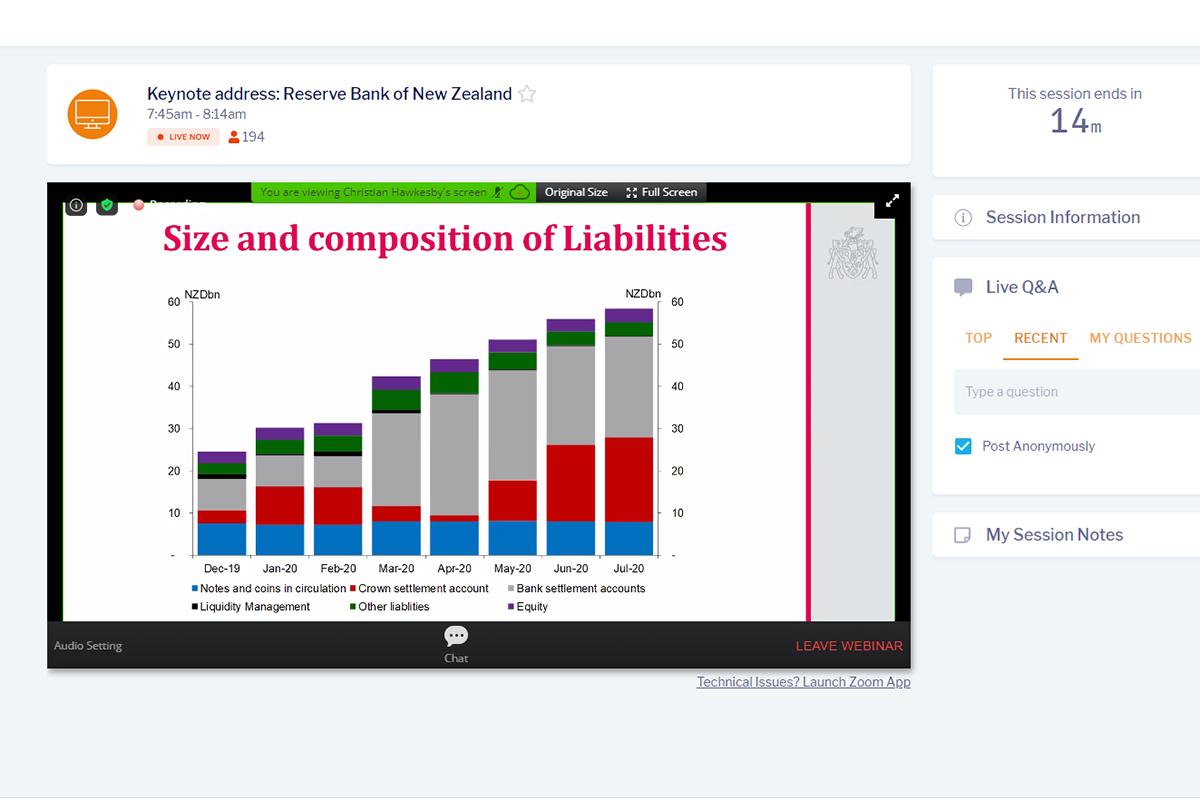

The New Zealand government bond (NZGB) market has functioned well so far during the crisis, with significant support from the RBNZ’s LSAP programme. At the time of the conference the central bank had bought more than NZ$25 billion of NZGBs as well as New Zealand Local Government Funding Agency bonds in the secondary market.

RBNZ assistant governor, Christian Hawkesby, said in the opening keynote: “We are not using the reserve-bank balance sheet to maximise profit or minimise risk. We are using it to achieve our policy objectives.”

The central bank has flagged further measures to help buttress the economy against imminent recession, including telling banks to prepare operationally for the possibility of negative interest rates in 2021 and contemplating the purchase of foreign assets to push down the New Zealand dollar exchange rate.

Hawkesby reiterated in his NZCMF speech that the RBNZ is preparing the market for further policy measures. He responded frankly to questioning on whether the RBNZ would specifically seek to influence the exchange rate more than other monetary policy channels with its policies.

“The New Zealand dollar fits into the picture as it always does. We assess all the moving parts in the New Zealand economy including the exchange rate and its implications for inflation,” he replied. “It is an important channel and interest-rate differentials matter, but no more or less than before the crisis.”

“We will be fighting for every basis point. But neither of the two levers we can pull to get greater returns in fixed income – increasing credit risk or extending duration – are necessarily great ideas as we bridge ourselves, hopefully, to a vaccine and the end of this crisis.”

“It is hard to see yield rising in the near term, but for the first time in a while we have procyclical fiscal and monetary policy at the same time. At some point this should lead to a meaningful steepening of yield curves as issuers extend duration. This is more likely in five years than one, though.”

“One cannot put an economy in stasis for three years and expect to be able to wheel all the businesses out again. The unfortunate reality is that some business models are not viable in this period and they cannot be supported forever. The focus needs to shift to retraining for industries that can successfully operate in this environment.”

“Wholesale funding is far more expensive than deposits at the moment so it has been crowded out. This is similar to what has happened in Europe in recent years, meaning some banks have been using markets for capital transactions and to keep their name fresh rather than for funding. The same may happen in New Zealand.”

“Capital is not static. We need more capital to fund growth and to help meet new requirements when they come in from 1 July 2021. The market for redeemable perpetual preference shares in New Zealand will need to develop and we look forward to issuing these in the future.”

PARSING THE MESSAGE

New Zealand rates have been on a rollercoaster ride since April, as market participants digest the various interventions and messaging from the central bank and government. The RBNZ’s recent LSAP expansion and more emphatic language around negative rates has seen NZGBs rally to new lows, well inside the Australian sovereign curve.

David Croy, senior interest rate strategist at ANZ, pointed out that the rally is not new. “New Zealand 10-year bond yields have fallen every year since 2013. What is new is the synchronous nature of global policy easing and the strength of forward guidance here and abroad. And, of course, QE is now a key feature of the New Zealand bond market.”

New Zealand seems set for low interest rates for many years. Diana Gordon, head of fixed income at Kiwi Invest, said this has significant implications for Kiwisaver and for local fund managers. Investors will not be able to rely on the same assets they have historically used to provide their clients with acceptable retirement income.

“The Kiwisaver mix has to change to provide the retirements people want,” Gordon said. “We as an industry need to be looking at private debt, venture capital, forestry finance and other avenues of risk, but they all should of course be looked at on their individual merits. Mandates have been slow to change in the past, but I expect they will change much faster to adapt to this world.”

So far, demand for government bonds and recent corporate deals in New Zealand has remained robust as bank balance sheets and fund managers are extremely liquid but face limited supply. The RBNZ’s backup bid is undoubtedly helping support market confidence especially in the rates sector.

Dean Spicer, ANZ’s head of capital markets New Zealand, cautioned that while the turbulence of March and April is past it would be premature to suggest the worst is behind markets given prevailing uncertainty around the virus and the economy.

Jared Barton-Hills, head of credit trading Australasia at ANZ, added that lack of issuance is likely to become an issue for the New Zealand market. Negative rates will not influence this story; as rates go lower, Barton-Hills continued, offshore selling can be expected though it should be offset by RBNZ intervention.

By the time of NZCMF, there appears to have been negligible impact from the crisis on offshore demand for NZGBs, according to Kim Martin, acting director, capital markets at New Zealand Treasury. In fact, the sovereign borrower’s increased borrowing requirement may even see increased interest from offshore investors.

“Previously, some offshore investors told us they liked New Zealand’s sovereign fundamentals but considered our bond market just too small to invest in. This may be changing. We have seen a wider range of offshore investors participating in our recent syndicated deals,” Martin said.

On the other hand, low rates are already causing a shift for some domestic institutional investors. Gordon said: “We are going further out on the curve right now. We think these are ‘fictitious markets’, in that central banks are dictating the curves they want in New Zealand and will crush the long end of curves overseas if they see long rates rise. While we are happy to play into this, we know it may not hold forever.”

Meanwhile, Vicky Hyde-Smith, head of New Zealand fixed income at AMP Capital, said her firm was underweight credit before the crisis due to tight valuations but is now more comfortable adding credit because of the RBNZ’s effective underwriting of liquidity premia.

New Zealand dollar corporate bonds have historically competed with stubbornly high term-deposit rates for retail investors. Deposit rates are now tumbling and retail investors too are having to adjust their return expectations. Andrew Parsonage, head of debt capital markets at Jarden Securities, told conference delegates retail investors are becoming used to low rates and are typically adjusting their maturity spectrum to find higher-yielding assets.

“Sustainability always comes up in our investor engagement and views are changing rapidly. Investors see our debt as low risk but sometimes have specific and challenging questions, particularly on reporting benchmarks, which help focus our attention on how we can improve our efforts.”

EYES ON THE FUTURE

Market participants have tended to focus on the near term since the start of the crisis. However, there is also a sense that the events of 2020 offer a once-in-a-lifetime opportunity to reset the New Zealand economy to be more innovative, sustainable and inclusive, and that capital markets have a role to play. With so much change afoot, it may be possible to reimagine the economy in a more sustainable fashion.

In an NZCMF keynote address, New Zealand’s former chief science adviser, Sir Peter Gluckman, said: “COVID-19 does not change the range of issues we are facing but it does offer an inflection point that we must not squander. This is a chance for deep discussion and engagement to shape the future of the economy and society.”

New Zealand’s international borders will remain closed for the foreseeable future, so the immediate viability of some of its companies may rest on their ability to operate and thrive domestically. Conference delegates heard from Ian Taylor, founder of Animation Research, which had its entire pipeline of sports-graphics projects scrapped at the beginning of the pandemic.

“We began looking at what we needed to do to keep the day-to-day business running. This was essentially what we could do in New Zealand to keep money coming in. Meanwhile, we also began planning for what would happen as the crisis unfolded and for a scenario where life begins to return to normal but New Zealand’s borders remain closed,” Taylor said.

Live sport has returned much quicker than Animation Research initially predicted and Taylor told attendees of the company’s pivot to deliver its contracts, which are mostly for coverage of sporting events in the US, remotely from its headquarters in Dunedin.

New Zealand’s business leaders see capacity for domestic improvement and innovation in developing a sustainable, low-carbon economy. Jane Taylor is a director of entities including Port Otago and Orion New Zealand, and a guardian of Aotearoa Circle. She told delegates this may be the only chance left to address the risks posed by climate change.

Ensuring a sustainable economic recovery is an area in which capital markets can have an immediate impact. At NZCMF, Auckland Council’s treasurer, John Bishop, said the council still hopes the majority of its future borrowing will be in green format. “Our issuance of green bonds has been well received by investors and councillors alike. Investors are engaging with the topic more than they ever have, and investors that are not holders of our green bonds are asking questions on sustainability.”

Conference speakers insisted there is much more interest in the market than the range of current green, social and sustainability bond issuers in New Zealand indicates, though this number is also rising. Mercury mandated a debut green bond on 21 August, for example.

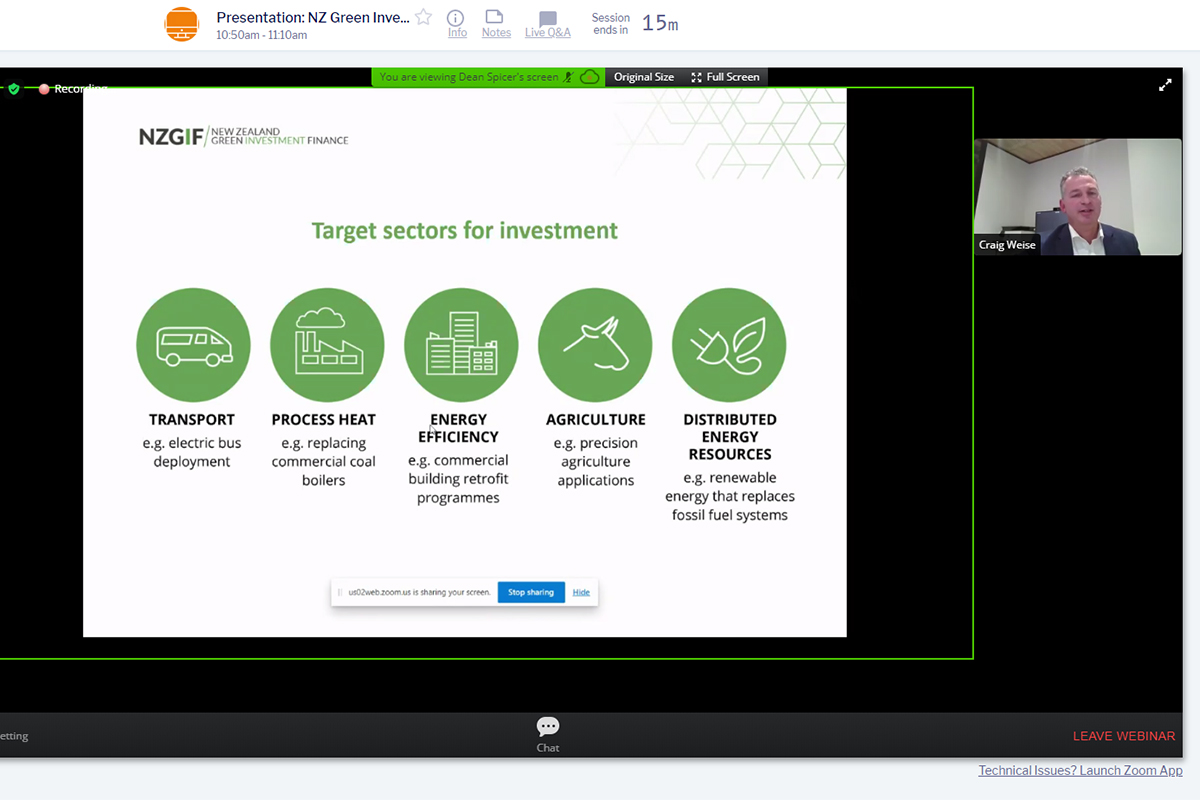

At NZCMF, Craig Weise, chief executive of New Zealand Green Investment Finance (NZGIF), a new publicly owned green bank, told delegates NZGIF’s mandate already includes the development of products that are investable by the wider market, which includes debt capital market issuance.

Meanwhile, David Hall, co-director of Mohio’s climate innovation lab, briefed the online audience on the development of forest-finance instruments, designed to channel investment funds into projects that would increase New Zealand’s forest cover. “The key question in climate finance is how exposed New Zealand is to the risks and opportunities of the low-emissions transition. The financial system has a role in directing capital towards novel and innovative solutions,” he said.

The New Zealand government, with its increase in fiscal spending, is also exploring investment opportunities to scale up its renewable-energy capacity, potentially to 100 per cent of output by 2035. However, some in the business community say the government’s fiscal-policy approach may run the risk of crowding out private investment.

Tim Brown, a member of the Infratil management team and chair of Wellington Airport, told conference delegates Infratil’s New Zealand investment plans remain in place for areas that have continued to experience demand growth through the COVID-19 period. These tend to be technology projects like data centres and 5G infrastructure.

However, investment is on hold in areas such as electricity and airports because of a combination of weak demand and uncertainties resulting from government policies. “Sustainable economic growth requires investment by private enterprise in productive assets and, in general, this is not getting a lot of encouragement from either the market or the government,” Brown said.

Taylor added: “A lot of the excess capacity and unemployment in the economy is in the private sector and it is very important that the private sector is included in any reforms for the recovery. Stimulus must be boosted by private investment and the most obvious places are in energy, transport and food production. This should be underpinned by increased investment in science and technology.”

New Zealand’s relatively low sovereign debt coming into the crisis allowed the government to provide massive levels of fiscal support, but Zollner made the point that this cannot continue forever. If there is no vaccine or other fix that allows a rapid return to normality, at some point the focus must turn to reskilling the workforce rather than propping up nonviable businesses, she argued.

Robertson said the government is investing significant amounts in job creation and this is already producing results – for example a doubling of the number of construction industry apprentices.

The business leaders’ panel discussed New Zealand’s labour market self-sufficiency as an issue for the present and future of the economy. Debbie Birch, director of New Zealand businesses including Fonterra Co-operative Group and IWIinvestor, emphasised the need for a nimble labour market. “We need to be prepared for continuous change because businesses will need to be ready to scale up immediately with skilled staff as and when borders open.”

“Last year was the first in which we made a profit, which came in handy because it became our reserve and allowed us to ensure no-one would lose their job this year. We wanted to ensure staff knew that part of their new job description was to look after themselves and their families. It has been an incredible journey, and we have seen productivity go through the roof.”

“The New Zealand and Australian markets are key investor bases for us and we will aggressively support both over the next few years. This is not to say we would not consider opportunistic issuance in other markets where it makes sense.”

Sponsored by

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news