Rocky road ahead

The 2020 iteration of the KangaNews-Moody’s Investors Service Corporate Borrower’s Intentions Survey highlights the response of corporate Australia and New Zealand to COVID-19. The results show treasury teams are anticipating a rocky path out of the crisis and a heightened domestic focus to their funding plans.

Matt Zaunmayr Deputy Editor KANGANEWS

The survey, now in its seventh year, was conducted in September and received more than 60 responses from capital-markets-relevant nonfinancial corporate borrowers in Australia and New Zealand.

The makeup of respondents is relatively consistent with previous years and broadly reflects the shape of Australian and New Zealand debt capital markets issuance. The vast majority of responses – more than 85 per cent – come from investment-grade firms and the dominant sectors are infrastructure, general corporate, real estate and construction, and regulated utilities.

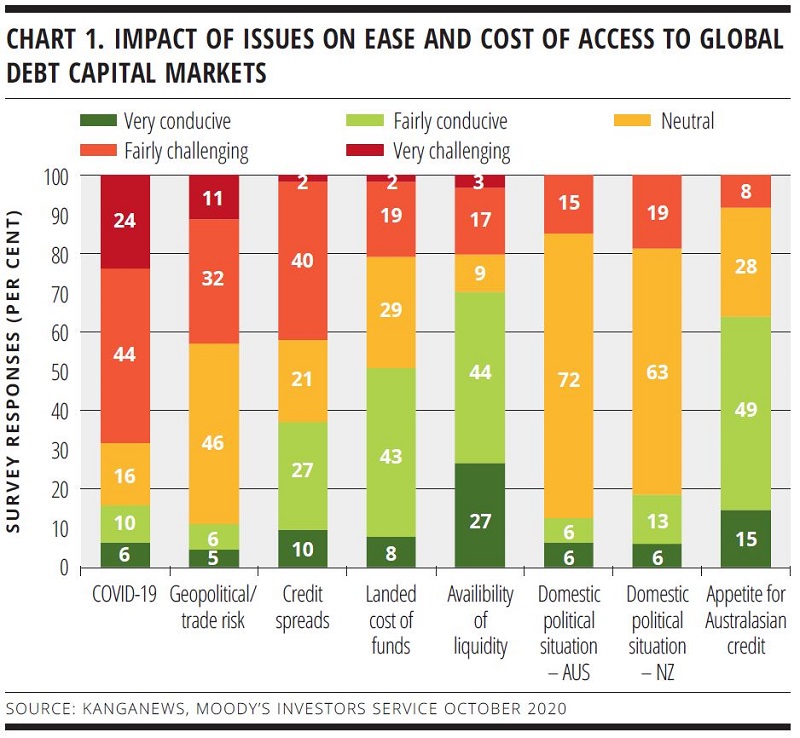

The economic and health crises wrought by COVID-19 in 2020 are, unsurprisingly, survey respondents’ key concern related to capital-markets access in 2020. More than two-thirds note that the pandemic represents a challenge in market access (see chart 1).

Notably, despite the severe economic impact of the pandemic, corporate borrowers continue to find liquidity conditions highly conducive to market access and remain confident in the appeal of Australasian credit.

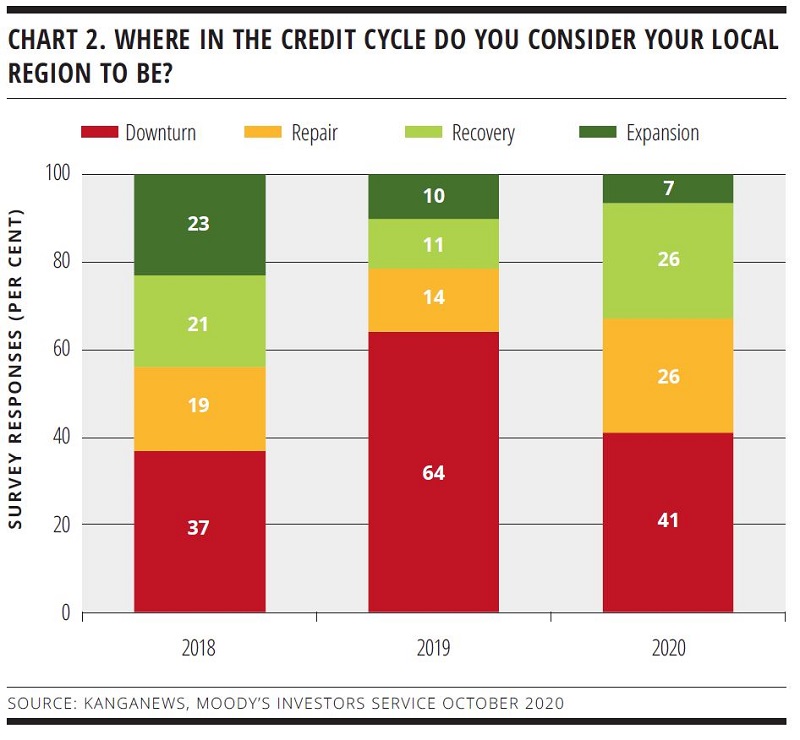

The pandemic has undoubtedly hammered corporate operating conditions – albeit not equally for all borrowers – but corporates appear to believe the worst of the economic consequences may be over. More respondents indicate that the credit cycle is in repair or recovery than did in 2019, while fewer think the trajectory is still downward (see chart 2).

The question is relative, though – so responses may simply indicate how far things fell in H1 2020. Patrick Winsbury, associate managing director at Moody’s in Sydney, says 2019 was characterised by weak investment and consumer spending, mediocre growth and US-China trade tensions.

“At this point in 2020, after likely seeing the worst of the downturn in the second quarter, the outlook is probably looking better,” he comments. “Respondents may also be identifying a move to the recovery phase because of the large amounts of government stimulus undertaken in 2020.”

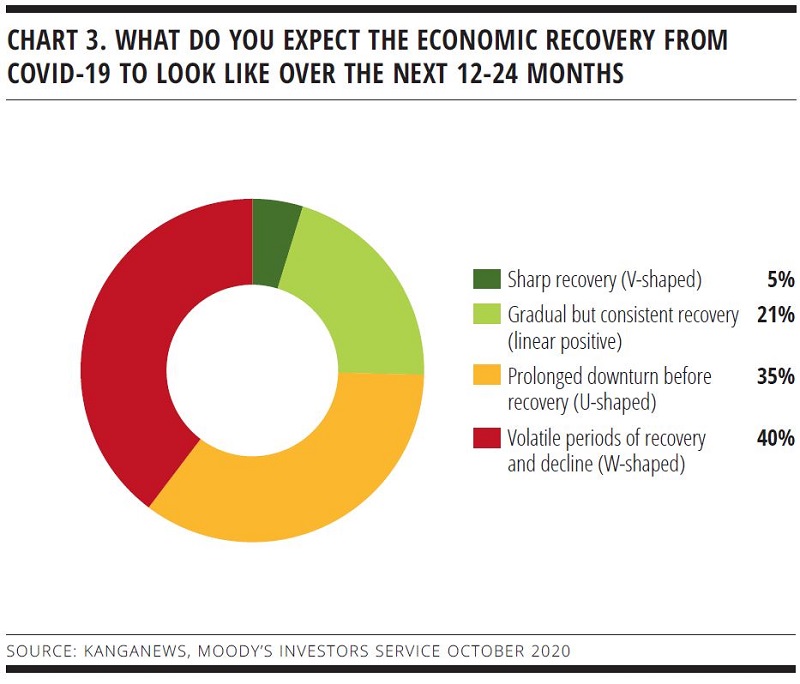

The majority of borrowers still foresee a long road ahead for recovery rather than swift resolution of macroeconomic woes (see chart 3).

This is broadly in line with the Moody’s house view. Martin Petch, vice president at Moody’s in Singapore, says: “We expect growth to pick up to moderately above trend in 2021, albeit reflecting the low base for activity following the downturn in 2020. We expect government infrastructure spending to support growth as well as some mild recovery in employment, which will help lift consumer spending. Business investment is likely to remain soft until the momentum of recovery picks up.”

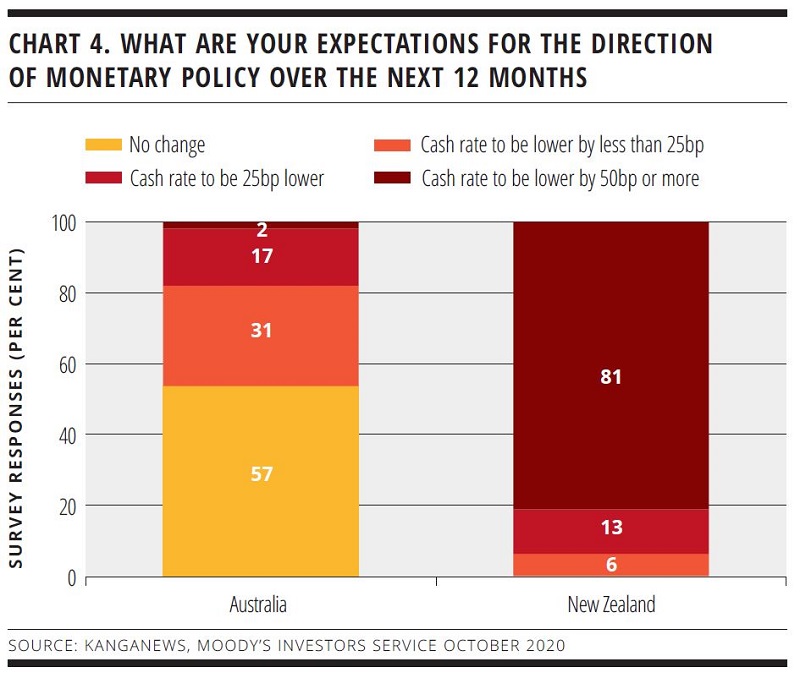

Respondents’ forecasts for monetary policy in Australia and New Zealand broadly reflect market expectations in September. In Australia, the market is gradually moving toward expectations of an unconventional cash-rate cut – of 10 or 15 basis points. In New Zealand, there is a clear expectation of negative rates within the next 12 months (see chart 4).

CRISIS RESPONSE

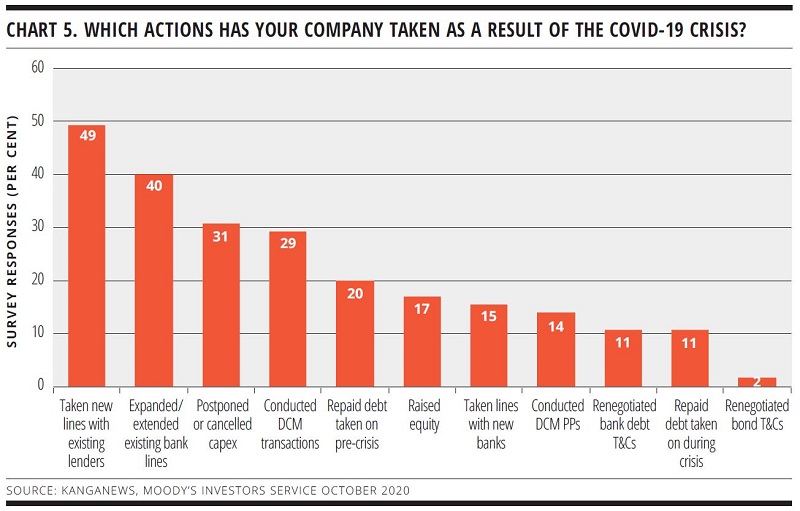

Corporate borrowers have responded to the crisis in a range of ways when it comes to debt funding. The most popular were taking on new bank lines or extending existing ones, followed by the postponement or cancellation of capex plans (see chart 5).

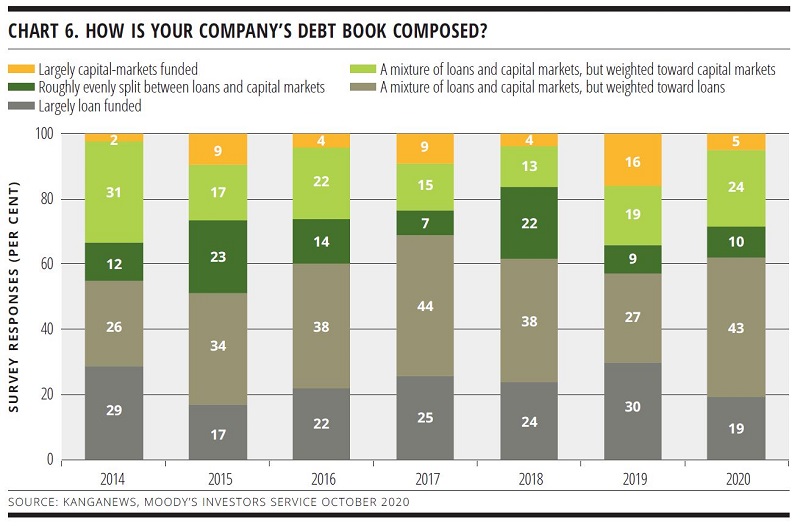

Fewer borrowers issued bonds as a result of COVID-19 than the number that added or extended bank lines. But there is no sign of a widescale return to complete reliance on bank funding. In fact, issuers overall continue to build the capital-markets proportion of their debt books at the margin (see chart 6).

Arnon Musiker, vice president and senior credit officer at Moody’s in Sydney, says Australian Bureau of Statistics data also show firms are expecting to scale back capital investment, and this could influence future borrowing requirements.

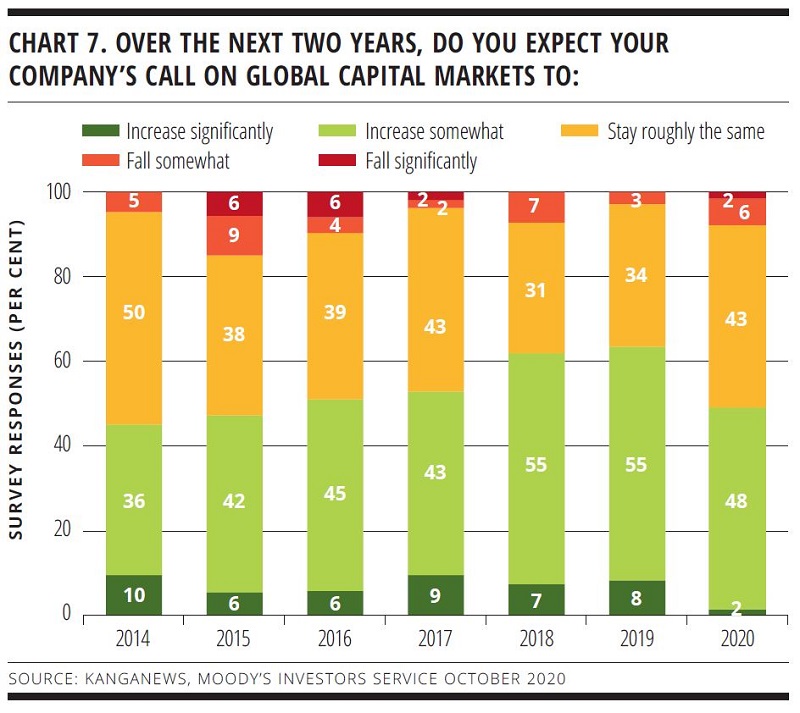

The proportion of borrowers expecting their call on debt capital markets to increase over the next two years is at its lowest level since 2015 (see chart 7). However, half the issuers still expect to increase their call on global bond markets while just 8 per cent expect it to fall.

“Many borrowers have also brought forward issuance plans for the next couple of years, to raise liquidity in response to COVID-19-related uncertainty and to strengthen their liquidity position as much as possible in view of an economic downturn,” Musiker explains.

The survey also shows that when corporate issuers have a call on debt markets they are increasingly likely to view domestic issuance as their first option. This applies on both sides of the Tasman Sea.

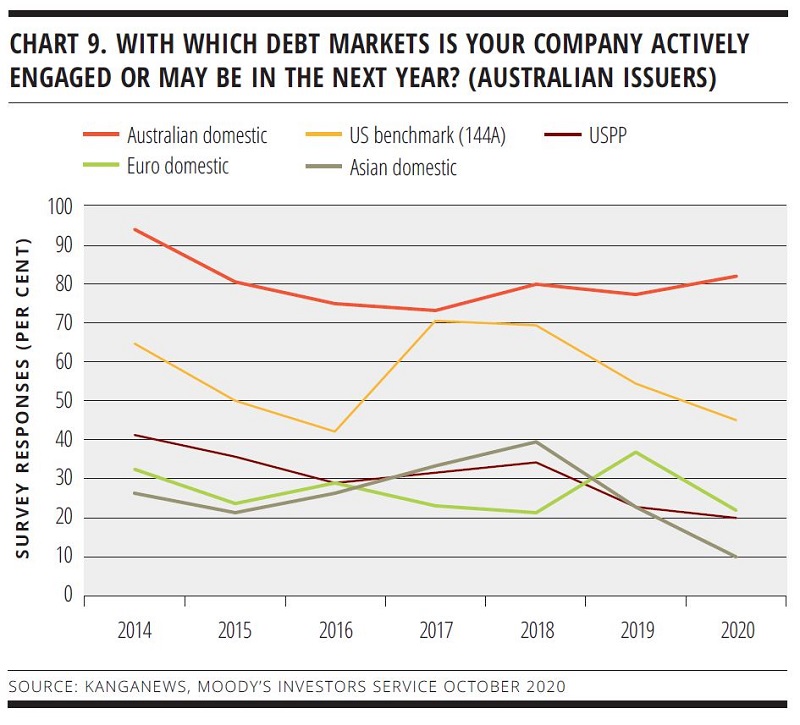

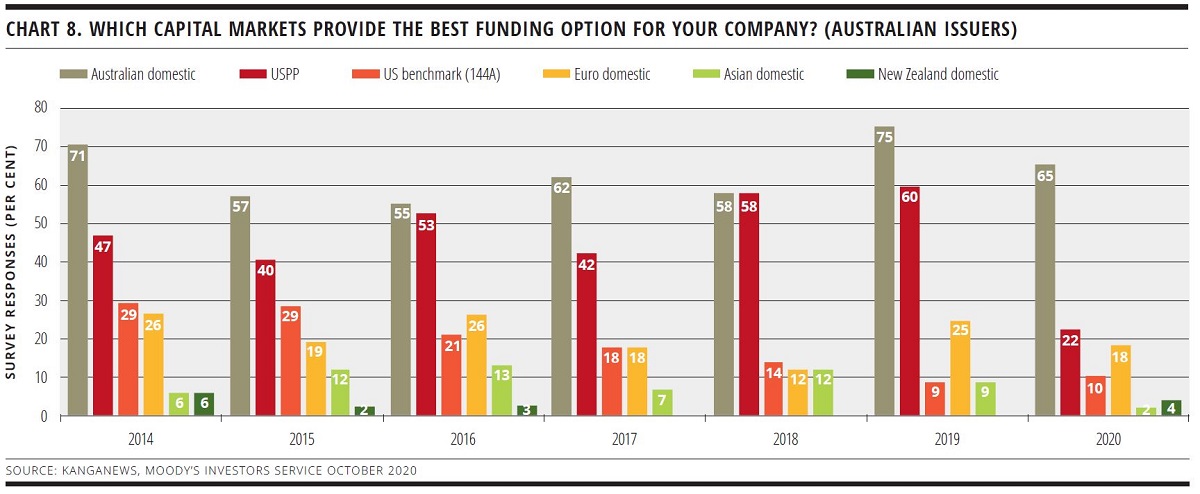

For Australian borrowers, the most notable change in views on ease of market access is a precipitous drop in appeal of the US private placement (USPP) option (see chart 8). Traditionally a close competitor to domestic issuance – if not the preferred option – just 22 per cent of issuers believe USPP is among the best issuance avenues in 2020 compared with 65 per cent naming the domestic market.

Australian borrowers say they have increased or intend to increase engagement with their domestic market in 2020 and the coming year (see chart 9).

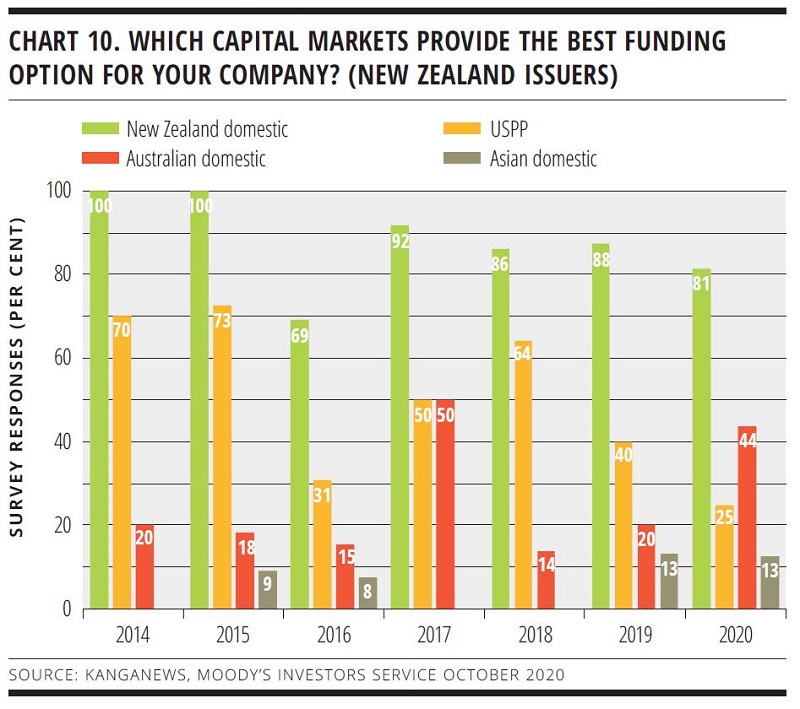

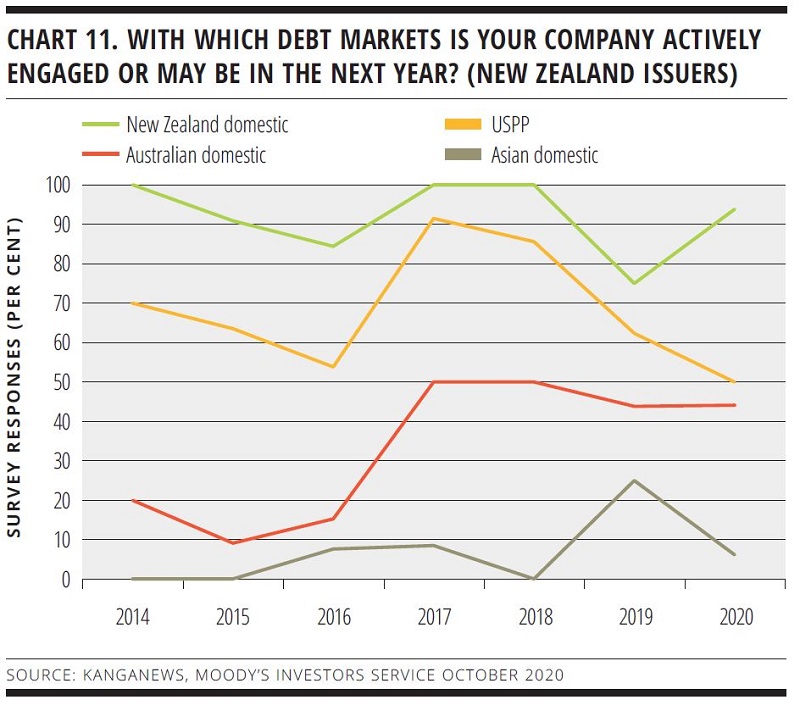

A similar trend comes through in the New Zealand market, where USPP has been replaced by the Australian dollar as the second-best issuance option (see chart 10). It is unclear whether this will translate into more trans-Tasman deals, though, as borrowers indicate that engagement with the Australian dollar market remains stable in 2020 from 2019 (see chart 11).

Despite the large take-up of virtual means for marketing and roadshows, corporate borrowers indicate in the survey that social-distancing restrictions are presenting challenges for investor relations. A small minority think the new paradigm has had a positive impact, but 55 per cent say there are minor challenges and 11 per cent note significant challenges.

ESG AWARENESS

The pandemic has been described as a catalyst for environmental, social and governance (ESG) recognition in capital markets, while 2020 has seen significant progress in the development, if not the issuance, of transition and sustainability-linked instruments. Australasian corporate issuers’ plans are not changing, though.

Only 27 per cent of survey respondents say the pandemic has increased their engagement with ESG concerns related to their business, while 71 per cent indicate no change at all and a tiny minority say it actually decreased awareness.

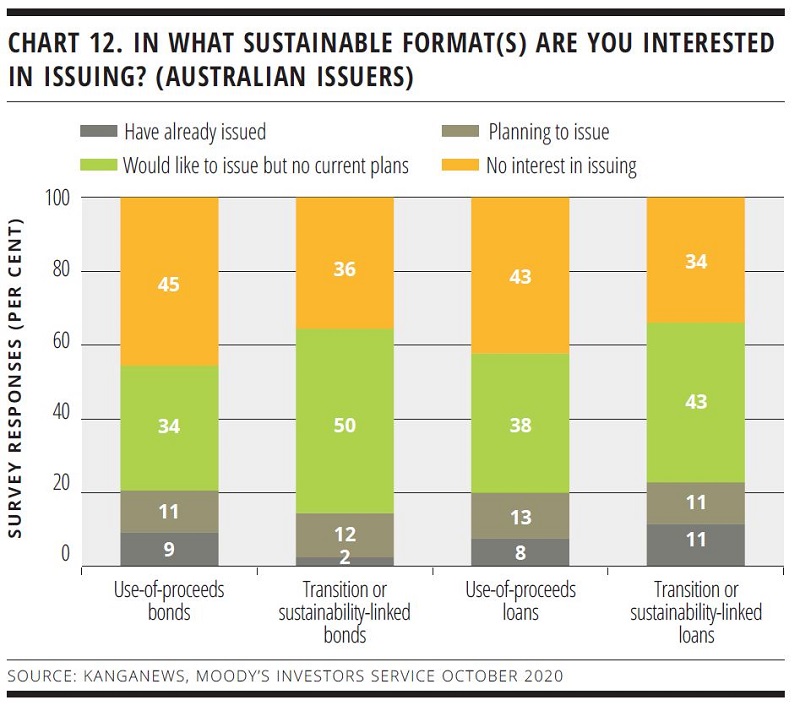

There is also little sign of an impending boom in ESG-themed debt issuance from the corporate sector. In Australia, the survey indicates a small pick-up in issuance or planned issuance for the various ESG formats, but more than three-quarters of respondents say they still have no firm plans or no interest in issuing sustainability-themed debt of any kind (see chart 12).

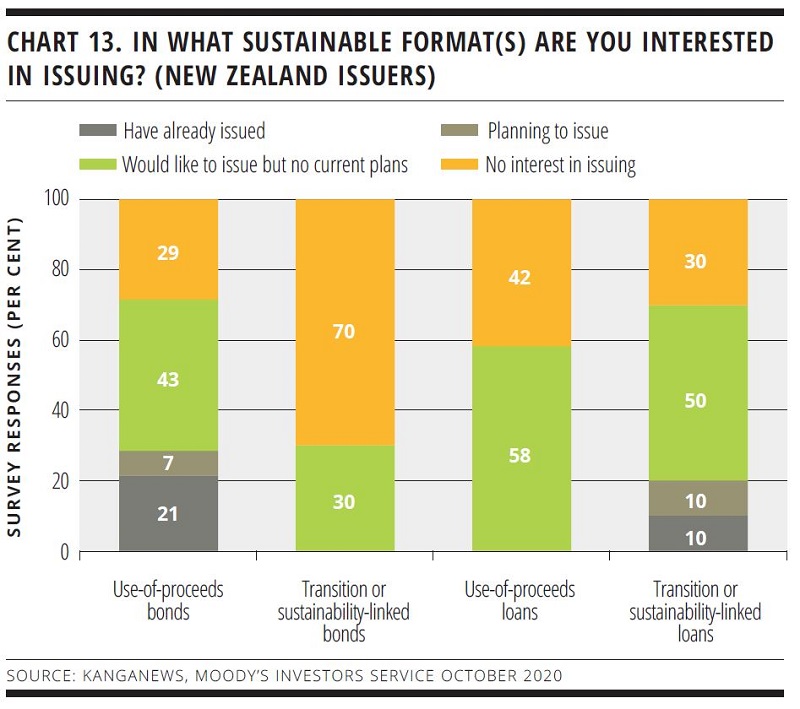

New Zealand borrowers that are interested in sustainable-finance products appear to have coalesced around use-of-proceeds product for bonds and transition or sustainability-linked product for loans, though the overall numbers are also low (see chart 13).

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.

Adelaide Airport rekindles investor relations in domestic return as it hits funding turning point

Following its first Australian dollar deal in seven years, Adelaide Airport says re-engaging with the local investor base was a top priority as it embarks on a new capex plan and plans for upcoming maturities. While issuance has slowed since a hectic end to Q1, the deal book demonstrates ongoing robust demand for Australian dollar corporate credit.