Reconstructive surgery

New Zealand investors face ultra-low rates and a radically reshaped credit-supply picture. As New Zealand struggles in the wake of COVID-19 – despite having been, at least for now, effectively able to eliminate the virus locally – the domestic buy side is considering its new strategy.

Matt Zaunmayr Deputy Editor KANGANEWS

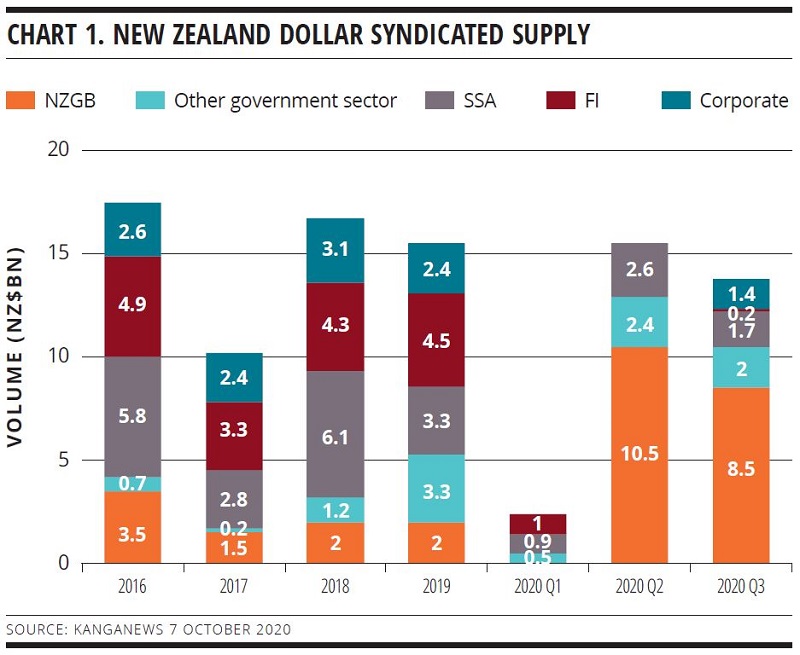

The New Zealand debt capital market sprang to life in Q3 2020, after Q1 was derailed by the beginning of the COVID-19 crisis and Q2 issuance was dominated by a few government-sector borrowers and opportunistic supranational, sovereign and agency issuance.

New Zealand Debt Management (NZDM) still accounted for more than half of overall syndicated supply in Q3. But the credit market re-emerged with a steady flow of corporate deals from across the rating spectrum – for the first time since the end of 2019 (see chart 1).

Within the high-grade sector, issuance pushed tenor boundaries in Q3. Kainga Ora – Homes and Communities, New Zealand Local Government Funding Agency (LGFA) and Auckland Council all extended their New Zealand dollar bond curves, the latter to 30 years in green-bond format. The long-dated green bond in particular is a major breakthrough for the New Zealand market, adding seven years to the longest tenor ever issued in a local benchmark and 10 years to any deal placed by a borrower other than the sovereign.

The emergence of long-tenor debt availability for government-sector issuers and the low yield on offer to corporate borrowers are a positive development for borrowers. These evolutions also bring the New Zealand dollar environment more in line with larger global markets.

For investors, both developments demonstrate the scarce options on offer locally to achieve acceptable returns in the new operating environment. There are plenty of challenges for New Zealand fund managers, particularly as the market has condensed years of development into a mere six months. But the circumstances also offer some potential to cement the market as one with a wider set of investment options.

ECONOMIC REPAIR

Virtually all rates analysts now expect New Zealand monetary policy to go negative in 2021 – an option reiterated by the Reserve Bank of New Zealand (RBNZ) following its August Monetary Policy Committee (MPC) meeting. The reserve bank also expanded and extended its large-scale asset purchase programme (LSAP), indicating that the NZ$100 billion (US$66.1 billion) of purchases available could mean it ends up owning 60 per cent of the NZGB market.

A month later, following another MPC meeting, the RBNZ reinforced its willingness to use further monetary-policy measures, highlighting its view that weak underlying domestic and international economic conditions are likely to cause a rise in unemployment and business failures.

The expectation of further monetary and fiscal stimulus is a product of the depth of the hole the New Zealand economy has to climb out of. GDP posted a 10.1 per cent real year-on-year drop in the June quarter of 2020, and the second lockdown in Auckland in August and September will inevitably slow the rebound.

On the other hand, New Zealand’s apparent success in combating COVID-19 gives some hope for a more positive than expected outlook. For instance, the unemployment rate actually decreased to 4 per cent in the June quarter, from 4.2 per cent in March. This was in part due to more people exiting the labour force but still represents an upside surprise.

New Zealand’s economy had reopened domestically by early October though its international borders remain strictly closed. There should be enough juice locally for a rebound of some degree.

David McLeish, Auckland-based senior portfolio manager and head of fixed income at Fisher Funds, says the economy has moved into the repair phase after a sharp and significant downturn in March and April – but adds that growth does not have the typical characteristics of a more positive environment. “In a repair phase, we expect growth and inflation to be below long-term average and, as the name suggests, households and businesses to be repairing their balance sheets through cutting costs and paying down debt.”

Interest rates are normally already at their lowest ebb once an economy is in the repair phase of a cycle, rather than predicted to go significantly lower – as is the case in New Zealand in late 2020.

Diana Gordon, head of fixed income at Kiwi Invest in Wellington, says at face value the New Zealand economy may not appear to warrant negative cash rates. However, the RBNZ and other analysts have an extremely bearish outlook for the next 12 months largely because of the global picture.

COVID-19 is not under control internationally and the largest economies are likely to be tested, Gordon explains. As a small, open economy, it will be difficult for New Zealand to escape the reality of a global recession. As a result, the RBNZ may well be willing to push the cash rate even lower than it already has in the hope that still-lower borrowing costs will give a tailwind to investment and growth.

RATES RALLY

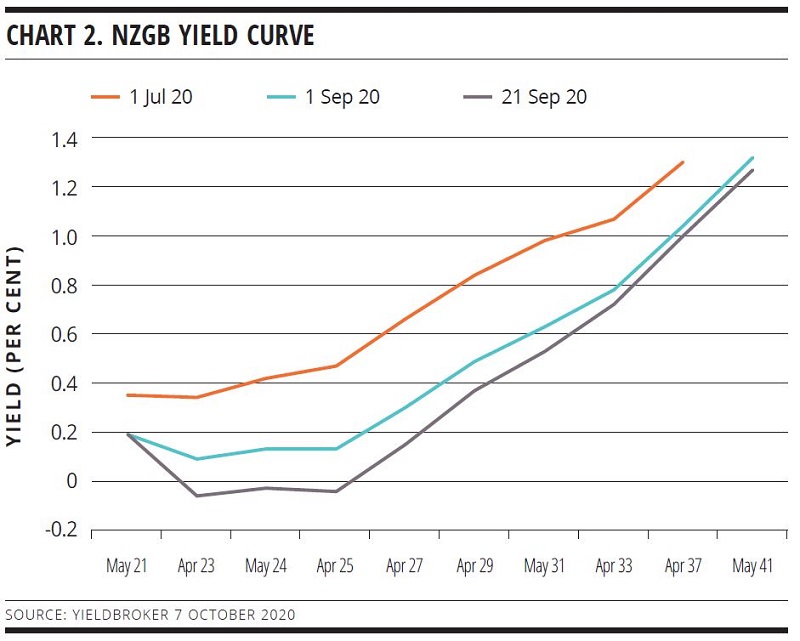

This context creates a challenging environment for New Zealand investors, starting with the government sector. The NZGB curve rallied significantly in Q3 as investors digested the RBNZ’s message and revised future cash-rate expectations accordingly. By late September, NZGB yields were negative in much of the mid-curve (see chart 2).

Some fund managers have been happy to ride the NZGB curve down through the COVID-19 crisis. Gordon says most of Kiwi Invest’s allocations in the last 4-5 months have been in the New Zealand dollar high-grade sector, based on the RBNZ’s strong language and bond buying.

She acknowledges, though, that this strategy is likely only to work in the short term. With rates expected to reach a floor in 2021, investors need to consider other options to enhance returns for their clients (see box). “As a fiduciary, we have to take risks. But at the same time, if there is no value in the market – because it is being run by central banks – we also need to keep an eye on the exit even as we play along.”

Going further out on the curve is one way of doing this while maintaining the credit quality of a portfolio. Fergus McDonald, Auckland-based head of bonds and currency at Nikko Asset Management New Zealand, says Nikko’s portfolios have preferred the long-dated bonds of local nonsovereign government-sector borrowers.

For portfolios with a requirement to hold sovereign bonds, McDonald says Nikko has been buying inflation-linked bonds in expectation that stimulus measures will usher in an inflation pick-up over the medium term. This theme has clearly been identified elsewhere as there was solid buying of New Zealand government inflation-indexed bonds (NZIIBs) in Q3.

Elsewhere, ANZ Investments has broadened its definition of eligible government bonds to allow for more purchases of bonds from the likes of Kainga Ora, according to Mia Prkusic, Auckland-based portfolio manager. “This gives us government-like exposure with extra spread and it is not a material increase in risk compared with the sovereign,” she says.

Long-dated demand is a boon for most government-sector issuers, which will likely have higher funding tasks in the wake of the COVID-19 crisis. It is no surprise, therefore, that issuers have been quick to take advantage of the availability of long-dated liquidity. Syndicated supply of New Zealand government-sector bonds has been larger and broader in 2020 than ever before.

KangaNews understands long-dated primary deals from Kainga Ora, LGFA and Auckland Council have performed well since pricing, indicating further latent demand for long-dated, high-grade New Zealand dollar bonds.

But not all fund managers are confident that holding long positions, even in high-grade names, is the best strategy for the current environment. Gordon says either of a COVID-19 vaccine in 2021 or a large US stimulus package following its presidential election could cause long positions to become unfavourable. She acknowledges that neither is close to certain at this stage, though.

Alternative appetite grows

New Zealand debt has long been a high-quality, high-yield and highly intermediated market, which has deterred and limited asset managers from exploring opportunities in alternative assets such as private debt. The increasing likelihood of a negative cash rate and regulatory change could change this.

Yield has plunged in 2020 across the full spectrum of the New Zealand dollar debt capital market. This only accelerates what was already a trend. The impetus for asset managers to look outside the realm of vanilla debt securities in order to achieve clients’ expected returns was already there but has now become greater.

Diana Gordon, head of fixed income at Kiwi Invest, explains: “There is now a fundamental mismatch between the needs of long-term investors and the vanilla instruments we have relied upon for return. We need to take risk as our clients need to retire – so it is likely that the whole industry will need to think more about alternative assets.”

Kiwi Invest recently made its first foray into venture capital, as a cornerstone investor in New Zealand firm Movac’s new technology fund, Movac Fund 5. Gordon says Movac aligns with Kiwi Invest’s prerequisite of being a high-quality manager that is expected to generate solid returns from its funds.

There is now a fundamental mismatch between the needs of long-term investors and the vanilla instruments we have relied upon for return. We need to take risk as our clients need to retire – so it is likely that the whole industry will need to think more about alternative assets.

LSAP PLAY OUT

The LSAP has also contributed to the suppression of rates in New Zealand. Meanwhile, RBNZ bond buying ramped up in Q3 after a formal programme extension and expansion. At the end of September, the RBNZ owned approximately 27 per cent of NZGBs on issue as well as 8 per cent of NZIIBs and around 11 per cent of LGFA bonds.

Investors report that the desired outcome of putting downward pressure on rates even outside the direct subjects of LSAP purchases is coming to fruition, though with the wider market lagging the tighter yield in the curves of issuers that are LSAP eligible.

Iain Cox, head of fixed interest and cash at ANZ Investments in Auckland, tells KangaNews the market is exhibiting a preference for government-sector bonds that are ineligible for LSAP based on an expectation that the bond-buying programme will eventually lead to wider performance.

The RBNZ expects that when the LSAP concludes in June 2022 it may own as much as 60 per cent of the NZGB market. While free float should remain substantial and may even grow, given NZDM’s expanded issuance programme, the scale of reserve-bank activity has also spurred questions about the effectiveness of the NZGB curve as a benchmark for the market.

Cox says: “NZGBs remain a reliable benchmark for sovereign portfolios, but it is up for debate when you are talking about a credit portfolio. Given how sticky some sovereign-wealth funds are, the remaining free float of NZGBs is likely to be even less than what is implied by the RBNZ’s holding.”

How the LSAP plays out over the next 18 months will continue to be crucial to the shape of the New Zealand dollar market, investors say. The RBNZ’s programme expansion means there will be plentiful support for the government to execute its fiscal plans, which are likely to be updated but not totally overhauled following the resounding re-election of the Labour government on 17 October.

The degree to which the RBNZ continues to intervene is likely to be crucial in determining the flow of demand and pricing discounts to other government-sector and corporate borrowers. In the more remote future, the question of how the reserve bank starts to pare back its intervention looms.

McDonald says one of the key risks he is considering is what the market response to an economic recovery that is either quicker or better than expected may be. However, he adds: “We think it will be a long time before the cash rate returns to 1 per cent or higher. Maintaining exposure to high-quality names is the right strategy for this environment.”

CORPORATE FLOW

Market conditions were already favourable enough in Q3 to entice the return of New Zealand corporate borrowers to the domestic primary market after an absence of more than six months. Many were attracted by the yield environment heralded by central-bank intervention.

New Zealand corporate spreads have also benefited from the same technical factors present in Australia, specifically the absence of major-bank issuance removing a significant portion of competing supply. In the past, banks have been a sweet spot for New Zealand institutional investors, being highly rated and relatively liquid while offering spread.

Cox says the ongoing absence of bank supply could free up capacity for other corporate borrowers to access the market at a lower spread than they could in the past. As a result, he believes the New Zealand market is likely to become more “bar-belled” – with higher issuance volume from liquid, government-sector borrowers and from less liquid, higher yielding corporates.

McLeish says the level of corporate borrowing being undertaken in New Zealand is also not typical of an economy in the repair phase of an economic cycle. He adds that this debt does not appear to be for productive purposes at this stage.

“The reason for borrowing is often stated as ‘general corporate purposes’, so it is not always clear what the funds are going to be used for. This typically indicates that companies are undertaking the funding because rates are cheap and they either want to get ahead of future refinancing needs or for growth opportunities that may come in the recovery phase,” explains McLeish.

He tells KangaNews that, given the tough economic environment, he does not believe corporate credit spreads appropriately reflect the risk of default for some issuers.

Gordon agrees, adding that the corporate competitive environment posed complex risks for investors even before the pandemic. “We were already in a period of extreme technological change, where previously safe companies were having their moats crossed by new players. This has only been accelerated, so it is more important than ever to focus on what the corporate landscape looks like in future.”

New Zealand corporates may be seeing the economy differently, though. In the KangaNews-Moody’s Investors Service Corporate Treasury Survey 2020, New Zealand borrowers primarily indicate either a belief that New Zealand is either still in the downturn phase of the cycle or has already entered recovery.

Most of the corporate supply has been well supported despite the question marks, including by institutional investors keen to snap up investment-grade credit and retail investors increasingly getting to grips with ultra-low yield even for unrated deals.

McDonald says Nikko’s credit investments have tended more toward the investment-grade and government-regulated entities that have come to market. “We do not think it is appropriate to be going down the credit spectrum in an environment such as this,” he confirms.

Meanwhile, Cox says ANZ Investments has been confident to invest based on the recommendations of its credit council and the fact that many borrowers have been investment-grade rated and regular issuers. He adds that some of the unrated supply that has come has been secured, which adds protection for investors.

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

Related news