Changes for the long haul

With so much going on in the here and now, the fact that Australasian fixed-income markets have fundamentally changed in 2020 has passed almost without comment. It is time to start asking what impact massively increased sovereign-sector issuance and massively reduced bank supply will have – and whether these changes will be permanent.

Laurence Davison Head of Content and Editor KANGANEWS

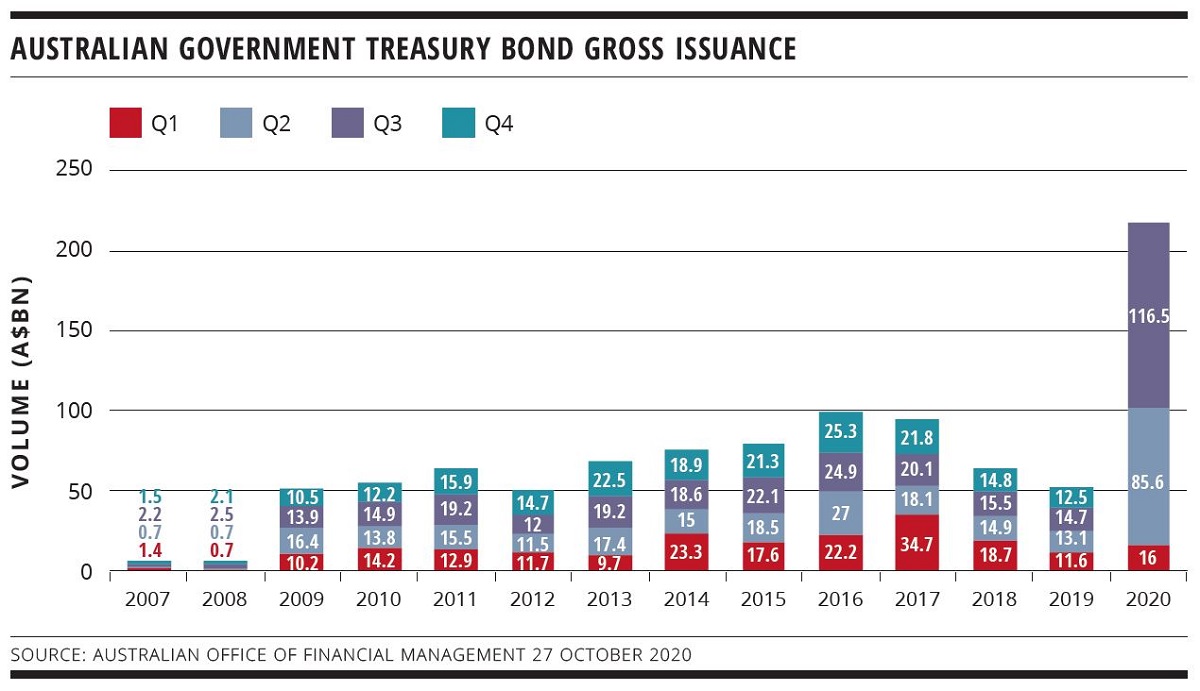

The trajectory of bond issuance by the Australian government is well known but still worth illustrating – particularly because gross annual Treasury bond supply has increased by a further A$37 billion (US$26.6 billion) since KangaNews last published the data, two months ago.

Gross Treasury bond issuance passed A$218 billion in the first three quarters of 2020 – more than A$200 billion of it coming in Q2 and Q3, after the COVID-19 pandemic hit. To put this in perspective, in 2013 – the year the Liberal Party won a general election on the back of a “Labor’s debt and deficit disaster” campaign – the full-year gross issuance figure was just shy of A$70 billion (see chart).

It seems government stimulus can be the right policy for Australia, after all – and I for one look forward to a 2022 election campaign that acknowledges the change in perspective. As my old housemate used to say: do get your hopes up, because it will happen.

CREDIT SHIFT

On the other hand, the Australian credit market has seen supply cut off at source. The domestic big-four banks have issued at least A$20 billion combined domestically in every year since 2008 and as much as A$43 billion in particularly busy or conducive years. That figure will be less than A$10 billion in 2020, as the Reserve Bank of Australia (RBA)’s term funding facility (TFF) and deposit inflows have reduced the majors’ wholesale funding need to a relative trickle of tier-two issuance.

With the TFF now extended and a more or less universal expectation of further QE to come, market participants are now resigned to the majors being absent for a matter of years. There is practically no expectation of their return in calendar 2021, certainly – and one of the lessons of QE globally is that it is easier to enter than to exit.

The big question, presumably, will come to be whether the RBA is confident to remove the TFF before the volume of lending it has outstanding to the major banks exceeds their refinancing capacity in global markets.

The three-year tenor TFF maturity spike was more than A$80 billion by the end of September and could be more than double this by the end of June next year. It has effectively replaced the Australian banking system’s aggregate wholesale-funding task. The manner in which the pendulum swings back toward capital markets – and thus moves from fixed-rate 0.25 per cent cost of funds to prevailing market-clearing rates – will be fascinating and challenging at the same time.

The ripples of the TFF have spread across the Australian credit market. One notable consequence has been the decimation of inbound Australian dollar issuance from global borrowers.

The most active sector of such issuers – supranational, sovereign and agency (SSA) names – tends to be price focused. Without a counterweight on the cross-currency basis swap provided by large and consistent foreign-currency issuance from Australian banks, Kangaroo deal economics have been harder than ever in 2020 – and SSA issuance has fallen precipitously as a result.

On the flip side, other than the banks themselves perhaps the biggest winner in funding markets has been corporate borrowers. While the crisis has been intensely difficult for many – though not all – large companies in Australia, funding markets have held up much better than might have been expected.

Corporate borrowers generally turned to their banks in the early days of COVID-19, and those who have spoken to KangaNews universally report no widespread retreat of liquidity – certainly nothing remotely comparable to the financial crisis – and doors open for renegotiation of terms and conditions.

Even more surprisingly, the Australian corporate bond market has rebounded hard and fast. I wrote about this in the last edition but suffice to say the availability of Australian dollar liquidity has continued to surprise on the up side, especially at extended tenor. The investor view seems to be that if a company can make it through the next couple of years it is probably good for a decade – so one might as well take the extra term premium on offer.

It is a mixed picture, meanwhile, for nonbank borrowers. The good news is that the same demand for alternative credit assets that has been spurred by lack of bank supply appears to be fuelling a buoyant Australian securitisation market. Nonbank transactions have been coming to market thick and fast, including more than twice a week in October alone. Deal flow now includes a raft of assets from buy-now, pay-later loans to commercial mortgages, and also features deal structures that top out below triple-A rating level. Clearly the market is functional and well supported.

On the other hand, a competitive landscape that has been predominantly supportive for Australia’s nonbanks has clouded significantly thanks to government and RBA support for the bank sector. Even the most cost-effective structured-finance market cannot provide funding at cost competitive with three-year TFF loans at 0.25 per cent; the going rate for triple-A, prime mortgage-backed securitisation is more than five times as much.

In the prime-mortgage space, at least, it is increasingly hard for nonbanks to compete with the regulated bank sector on price – and service proposition only goes so far in winning business.

“The past decade has been a story of vast quantities of liquidity chasing yield into increasingly disparate jurisdictions and asset classes. For some time, Australia was a recipient of such funds. In future, it may increasingly be a source of them."

LASTING CONSEQUENCES

At the same time, bank lenders may be about to have the handbrake released in nonprime lending due to the promise of eased responsible-lending requirements. As an aside, it seems quite astonishing that barely a decade after the financial crisis took the world banking system to the brink of collapse, the Australian government thinks it is time to remove or substantially relax the requirement on banks to verify the credit quality of their own customers.

The devil will be in the detail, of course. But with the housing market already rebounding well ahead of a wider economic recovery, the idea that yet more cheap credit needs to be pushed into residential property is about as counterintuitive as the government’s belief that front-loading a massive tax cut for the demographic segment least likely to spend the windfall is the best available mechanism for economic stimulus.

Coming back to capital markets, the long-term consequences of new Australian supply dynamics are as yet unknown. So far, the sovereign market has shown no sign of capacity issues even when the RBA has not been an active market participant. Even with a likely expanded QE programme and greater demand from local bank liquid-asset books, the Australian sovereign market seems set for a bigger place in the global market.

This should be good news for sovereign-bond traders and for the Australian Securities Exchange’s new five-year futures contract – as well as its existing 20-year future, assuming liquidity continues to build in the long-dated part of the curve. I have never been totally convinced that a bigger sovereign market is in and of itself a growth catalyst elsewhere, but it surely cannot harm the Australian market if more global capital has its biggest borrower on the radar.

On the other hand, while nature may abhor a vacuum it is hard to predict what might fill the credit supply gap. Australian dollar credit was struggling for supply diversity even before the bank issuance hiatus, and a protracted economic downturn does not seem likely to spark a surge in domestic corporate issuance. Some supply that previously would have found its way to the US dollar or euro markets may remain onshore but this would not represent exponential growth.

Whether demand is elevated enough to produce sufficiently attractive pricing conditions to draw international names – SSAs and credit borrowers – to Australian dollars is as yet unknown. But it is hard to be too optimistic.

With a glut of domestic high-grade supply, Australian investors’ impetus to buy global SSAs seems as low as ever. Global banks have seen their own issuance needs drop for the same reasons as their Australian peers, and regular Kangaroo corporate issuance does not seem to be on the agenda at this stage.

Much more likely, I think, is that Australian credit funds will increasingly spread across the globe. The size of the local superannuation market relative to domestic credit suggests this is all but inevitable, even without the new supply dynamics of 2020. The collapse of the local issuance core will surely only accelerate the process.

On the other hand, it is not as if there is an easy path to appealing credit absolute return anywhere in the world at present. The past decade has been a story of vast quantities of liquidity chasing yield into increasingly disparate jurisdictions and asset classes. For some time, Australia was a recipient of such funds. In future, it may increasingly be a source of them.

Perhaps this period of extraordinary government liquidity will pass, and Australia will be left with a larger sovereign-bond market and a rejuvenated and restored credit market. But, like so much else associated with this pandemic year, it would take a brave person to say with conviction that we will soon return to the old normal.

Related news

Input complexity clouds Australian debt strategy outlook

KangaNews hosted its annual roundtable discussion for Australia’s leading bank fixed-income strategists in March amid a fast-changing world. While inflation, interest rates and geopolitical risk are on the rise, financial markets are not yet in crisis territory. The strategists agree Australia is in relatively sound financial shape as the world moves into a higher rates regime.

ESG to the fore as New Zealand business emerges from the pandemic

The agenda at the KangaNews New Zealand Debt Capital Market Summit in December 2021 included a panel of high-level local corporate executives who discussed how business responded to the challenges of the pandemic and the future outlook. Sustainability is playing an increasing role in corporate strategy.

New Zealand’s banks resilient despite lingering uncertainty

New Zealand’s banks are returning to a more normal business environment but the spectre of the pandemic remains. At the KangaNews New Zealand Debt Capital Markets Summit in December 2021, Daniel Yu, senior analyst at Moody’s Investors Service in Sydney, broke down some of the key themes the rating agency expects the country’s banks to face over the next 12 months and their credit quality.

The economic arc of recent history

Having celebrated his 30th anniversary with Westpac Banking Corporation in 2021, chief economist Bill Evans is in a unique position to view the challenges facing markets and economies thanks to his deep understanding of how they have responded to comparable events in the past. Evans speaks to KangaNews about the economic outlook, the wealth trade-off between wage earners and asset owners, the risk of deglobalisation and how sustainability is factoring in to his forecasting.