Australasian retail REITs: pandemic leaves lasting pain

The fallout from COVID-19 will linger beyond lockdowns for rated retail REITs, according to S&P Global Ratings senior director, corporate ratings, Craig Parker, and associate, corporate ratings, Rhys Corry. In Australasia, COVID-19 containment measures are eroding retail REIT earnings and reducing asset value amid unprecedented structural disruption.

Faster take-up of online shopping and rising retailer defaults will weigh on demand for retail space, reducing rental levels and occupancy rates. Landlords’ ability to replace vacating tenants and resist pressure for greater turnover-linked rents will be critical to defending the sector’s credit quality. Greater differentiation in credit quality could occur as retail landlords with larger exposure to more vulnerable secondary-grade assets will be hit harder than those with superior assets.

For Australian and New Zealand retail landlords, revenues plunged over the past few months as stores were shuttered and tenants were unwilling or unable to pay their scheduled rents.

Still, S&P expects the fallout from the pandemic to extend well beyond lower rental collections over the next few months. The structural pain will go on as faster adoption of e-commerce and changing consumption patterns continue to buffet the sector.

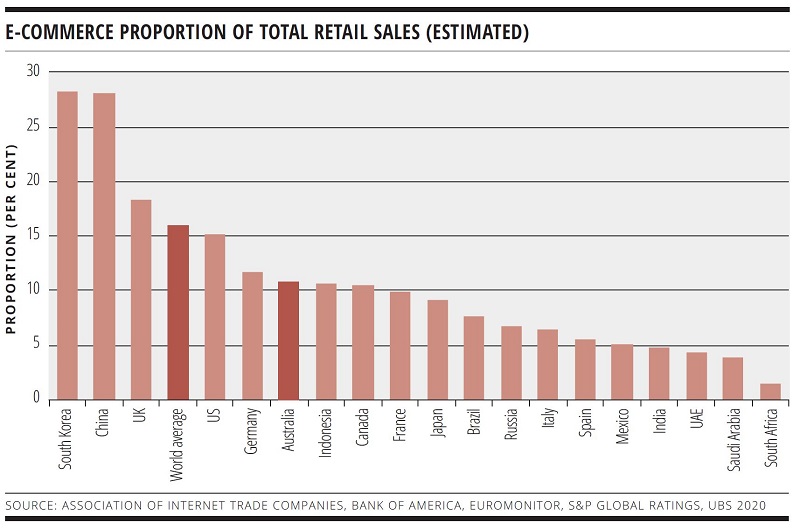

While online shopping has been a structural threat facing Australian retail landlords for some time, it has been a slow burn. The level of e-commerce sales as a proportion of in-store retail sales remains well below markets such as China, the UK and the US (see chart). However, the COVID-19 pandemic has fast-tracked growth in online sales, intensifying pressure on retail landlords.

The fundamental question remains whether the faster adoption of online transactions during 2020 is a temporary blip or something more permanent. Landlords are hoping for a rebound in fortunes as economies emerge from the pandemic.

We believe much of the shift online represents a more permanent change in consumption trends, although sales will meaningfully rebound in the short term as shopping centres emerge from lockdowns. COVID-19 has driven previously reluctant consumers online and encouraged online take-up at a much faster rate than witnessed in the past.

Australia Post reported that 200,000 new households shopped online for the first time in April 2020. More interestingly, two-thirds of those 200,000 households have continued to shop online five months after their initial purchase.

Similarly, retailers have been forced to adapt rapidly or initiate online offerings in light of government restrictions. For example, hardware giant Bunnings pivoted from its traditional brick-and-mortar business model to “click and collect” during the government-enforced lockdowns.

COVID-19 has also caught out some retailers that did not have an established, user-friendly virtual presence. Conversely, the e-commerce shift has benefited companies that manage their own distribution centres and were able to capitalise on the change in consumer spending patterns.

RENT STRUCTURES

Retailer distress caused by the COVID-19 pandemic and online stresses have also triggered a fundamental debate on rent structures between landlords and tenants.

The Australian retail REIT market has traditionally employed fixed-rent lease structures with predominantly fixed or annual rent increases linked to CPI. However, retailers argue that sales-based rent agreements should be the way of the future because they share the risk between retailer and landlord, and put greater onus on landlords to drive customer footfall.

Our ratings assume that REITs will resist any material changes to lease structures. To date, landlords from our pool of rated REITs have held firm against any replacement of these structures.

Nonetheless, risks remain that landlords of lower-quality shopping centres could succumb to tenant demands and allow sales-based leasing deals to maintain occupancy levels. This could reverberate through the sector, triggering competition for tenants among landlords.

In our view, this change in lease structures would likely precipitate further negative property revaluations and disrupt the predictability of fixed net operating income. More fundamentally, it would likely increase the cost of capital and worsen the debt capacity and credit quality of our rated REITs.

TENANT POOL AND DEFAULTS

Retailer defaults rose substantially in the first nine months of 2020. Despite significant government stimulus and other support programmes, many retailers, already under strain from online competition, were forced into administration or liquidation as shutdown measures decimated their remaining cash flows and liquidity.

Furthermore, an escalation in tenant defaults remains a material risk as government benefits and subsidies taper off, and the mandatory code of conduct for SME tenancies ends in early 2021 as currently scheduled. The code of conduct is designed to share the burden of a subdued trading environment during the pandemic between tenants and landlords.

In our view, the ability of shopping-centre landlords in Australia to use international retailers to fill vacating space is diminishing. These tenants – including retailers such as UNIQLO, H&M and Zara – had previously been eager to fill space, underpinning centre expansions. Since the pandemic, however, Zara and H&M announced the permanent closure of 1,200 and 250 stores, respectively, in their global networks as they turn their attention to e-commerce.

Given this challenging outlook for brick-and-mortar retailing, it is unclear what the future tenant pool for shopping centres looks like. Since e-commerce emerged as a retail distribution channel, landlords have been moving away from traditional fashion retail into an experiential food and services offering.

While we think this transition has some room to expand, it is slowly becoming more limited as the segment matures. Scentre Group, for example, already has 43 per cent of its store portfolio designated as experience- or service-based. Moreover, the space requirement for experiential and service-based tenants is generally smaller than other retail formats.

New retailers that have entered the market have also showed that a physical presence is no longer needed to generate sales growth and customer brand awareness. The Iconic, Adore Beauty, Temple & Webster, Koala and Kogan use their social-media presence, customer following and delivery options to let them exploit gaps in the market without physical stores.

Still, not all online pure-play retailers can weather losses for what could be an extended period of ramping up their online capabilities without an omnichannel offering. These steps include developing distribution networks, management and returns policies.

GROWTH PROSPECTS

In our opinion, growth opportunities for retail landlords will be limited over the next 3-5 years at least. Over recent decades, shopping-centre developments and expansions were justified in an environment where rents were rising every year. Although the Australian market benefits from materially lower shopping centre space per capita than markets like the US, we expect the economics of future investment to prove more challenging as negative rental reversion takes hold and competition intensifies.

Nevertheless, we believe community shopping centres will continue as residential developments sprawl outside city centres, albeit tempered by slower population growth over the next 12 months at least.

We also expect to see greater differentiation in retail-asset performance. We believe destination centres will continue to attract footfall and tenants. These centres have positioned themselves not only as a retail destination but also as a social destination, driven by experiential offerings and services that are entrenched in their respective catchment areas.

However, we believe less well-positioned assets in the regional and subregional space are likely to bear the brunt of the fallout. Furthermore, CBD assets will be hit as flexible working arrangements become the new norm.

Despite these significant online threats, however, we believe shopping centres will remain an integral, albeit reducing, part of most retailers’ strategies. While retailers are looking for a better mix of physical and online offerings, most continue to see physical stores as integral to their brand and growth strategy across a broad range of product lines. Accordingly, the main uncertainty remains the level of future demand for physical retail space relative to available supply.

The key challenge for landlords, therefore, is to understand and adapt to this changing landscape. This will include remixing their tenancies toward more experiential offerings that are not readily substituted online and matching supply to reducing retailer demand.

Digital integration into the physical shopping experience could help better merge the physical with the digital and drive consumers back into stores. In addition, significant opportunities exist for landlords to use their centres as a last-mile delivery node for retailers, given their proximity to residential populations.

For creditors, the key issue is not only whether landlords can adapt their business models to remain a central hub of community activity, but whether they can achieve this while also keeping their occupancy rates, rental levels and fixed rent structures intact. The most exposed are likely to be those with secondary-grade assets that are subject to strong competition and are unable to adapt their assets and tenant mix to meet this changing demand environment.

Related news

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.

Adelaide Airport rekindles investor relations in domestic return as it hits funding turning point

Following its first Australian dollar deal in seven years, Adelaide Airport says re-engaging with the local investor base was a top priority as it embarks on a new capex plan and plans for upcoming maturities. While issuance has slowed since a hectic end to Q1, the deal book demonstrates ongoing robust demand for Australian dollar corporate credit.