Beyond labels, corporate engagement marches on

If Australian corporate engagement with sustainable finance were measured by labelled green, social and sustainability bond issuance, progress remained underwhelming in 2020. However, issuers, investors and other market participants at the KangaNews Sustainable Debt Summit 2020 spoke of deepening commitments to environmental, social and governance risk mitigation.

Matt Zaunmayr Deputy Editor KANGANEWS

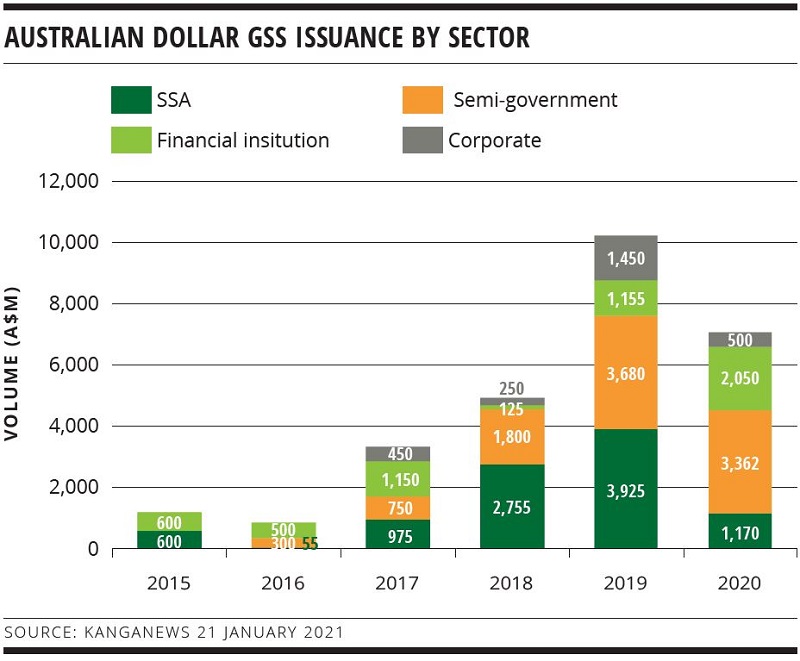

In 2020, Australian dollar green, social and sustainability (GSS) bond issuance lagged the record volume priced in 2019. Issuance was dominated by repeat semi-government and supranational, sovereign and agency issuers, as well as a large transaction from ANZ Banking Group (see chart 1).

Except for the sovereign, which is not currently actively considering labelled issuance despite a much higher funding task, corporate borrowers remain the missing link in a fully deployed local GSS bond market. Only one local corporate – Lendlease – issued labelled debt in the domestic market during 2020. One other, Sydney Airport, issued a sustainability-linked tranche as part of a US private placement (USPP) deal in February.

The scale and nature of Australia’s corporate landscape may be a limiting factor for engagement with labelled issuance. The property sector has been the primary source of corporate GSS supply, though environmental, social and governance (ESG) commitments and interest in use-of-proceeds bonds vary from issuer to issuer. Plenty of REIT issuers, for instance, still doubt the value of labelled funding on the basis that their sustainability commitments should be self-evident.

At the KangaNews Sustainable Debt Summit on 24 and 25 November, the topic of corporate engagement was prominent among active issuers and those that are not. The manifestation of the apparent interest may never fully flow into labelled debt products but those on the market front line are confident progress is being made.

COVID-19 EFFECT

The COVID-19 pandemic largely defined capital-markets activity in 2020, including in sustainable finance. For instance, the explosion of social-bond issuance – long the least developed part of the GSS landscape – has been widely touted in global markets. By the end of 2020, green and sustainability bond issuance had also rebounded to make total global GSS issuance volume in 2020 a record.

This is despite some fears at the beginning of the crisis that sustainable finance would be parked while issuers dealt with the immediate issues confronting them, said Katharine Tapley, head of sustainable finance at ANZ in Sydney, during the conference.

In Australia, the limited issuance of corporate GSS bonds during 2020 suggests it was hard to maintain momentum during the pandemic. Anne-Marie Neagle, partner at King & Wood Mallesons in Melbourne, said at the conference that legal enquiries typically form a reaction loop during a crisis.

“Institutional bandwidth needs to be triaged in a time of crisis,” she explained. “Urgent concerns around liquidity and shoring up funding against potential triggers can take centre stage during a crisis’s early stages. Anecdotally, where GSS finance was on an issuer’s funding radar, maintaining momentum at least at the height of the crisis to an extent depended on the issuer’s maturity and experience in GSS products.”

This could account for the high proportion of the Australian market’s 2020 GSS volume that came from repeat issuers. Lendlease’s green-bond deal, despite being a debut and the programme being developed during 2020, was the culmination of more than a decade of focus on sustainability in overall corporate strategy, according to Michael Larkin, group treasurer at Lendlease in Sydney.

However, the common message throughout the KangaNews Sustainable Debt Summit was that labelled deal flow alone is too narrow a lens through which to judge corporate Australia’s engagement with the sustainable-debt market.

Marayka Ward, senior credit and ESG manager at QIC in Brisbane, said a lot of time at the height of the crisis was spent with companies in debt-investor updates – in which the social component was more prominent than ever, despite the near-term uncertainty. This perhaps reflects the fact that while there has not been issuance of social bonds from Australian corporates, the COVID-19 crisis has nonetheless placed social concerns more prominently on their radars.

Investors in Australia frequently say issuers’ overall strategies are much more important than individually labelled bond deals. In part this is due to the slow growth of mandated, dark-green ESG debt investment funds. Chris Newton, executive director, responsible investments at IFM Investors in Melbourne, said at the KangaNews event that 80 per cent of Australian superannuation remains in balanced funds.

However, superannuation funds themselves are increasingly adopting net-zero emissions by 2050 targets and applying them to investment portfolios. This does not necessarily mean demand for a deluge of corporate labelled sustainable-finance transactions. It will, investors say, entail scrutiny around issuer strategies and therefore corporate engagement with sustainability is likely to come further under the microscope.

TRANSITION FOCUS

Social factors may have come into view more prominently in 2020 but the key long-term risk to corporate viability is still climate change. As a result, transition to a low- or zero-carbon future is increasingly a focal point for issuers and investors alike when creating and assessing corporate strategy. At the KangaNews conference, David Jenkins, global head of sustainable finance at National Australia Bank in Sydney, said capital markets will play a critical role in facilitating transition by providing finance to issuers looking to adapt their business models and by allowing investors to deploy capital in line with ESG goals.

“The concept of climate transition does not yet have a uniform, globally recognised definition. But it is rapidly becoming a key focus for companies and countries, including in Australia – especially those that are heavy emitters or in hard-to-abate sectors,” Jenkins added.

Australian issuers and investors across sectors are engaging with net-zero emissions targets or transition more broadly. Larkin revealed Lendlease is targeting net-zero emissions by 2025 and absolute zero by 2040.

Michael Bradburn, Sydney-based chief financial officer at Ausgrid, which manages electricity distribution for Sydney and other parts of New South Wales, outlined measures the company is taking to encourage more of its customers to use renewable-energy providers.

He added: “Ausgrid is actively adapting to the future of energy use and production, which is likely to be more reliant on household production and storage via solar panels and batteries with the ability to sell power that is not used back to the grid.”

Funding credible business transition has become a prominent topic among sustainability practitioners in capital markets, based on a realisation that goals and targets for climate-change mitigation cannot be met without involving the whole corporate-borrower landscape – not just those that can readily find assets suitable for use-of-proceeds instruments.

Sydney Airport is not a large carbon emitter itself but it is inextricably linked with the hard-to-abate aviation sector. It continues to be the Australian corporate leader in issuance of debt linked to transition measures. Sydney Airport executed the first-ever Australian syndicated sustainability-linked loan in 2019 and followed this up with a sustainability-linked USPP bond in early 2020.

Michael Momdjian, general manager, treasury, tax and insurance at Sydney Airport, told the virtual audience in November that one of its primary goals in both transactions was to ensure they were as dark green as possible. “Objectivity and transparency were front of mind for us when partnering with our banks and bond investors. This is why we tied our sustainability performance to an externally derived rating with ambitious stretch targets,” Momdjian explained.

SIGNALS AND NOISE

Reaching net-zero carbon emissions in Australia will take a committed effort from much of the corporate sector. Unless there is a radical change in federal government approach, it will need to achieve this without the policy signals that corporates in other jurisdictions are receiving.

Industry groups are attempting to build coalitions large enough to step in and provide such signals. The Australian Sustainable Finance Initiative (ASFI) released its roadmap for sustainable finance in late November 2020. Among its recommendations are for Australia’s largest companies all to be reporting against the Task Force on Climate-related Financial Disclosures (TCFD) by 2025.

Unlike in other countries – including New Zealand – there is no current drive from regulators to make TCFD reporting mandatory. However, it could become effectively mandatory if the trajectory of investors globally to require this kind of disclosure continues its upward trend.

Brian Cahill, managing director, global environmental, social and governance at Moody’s Investors Service in Sydney, said at the KangaNews conference: “There are broad market trends focusing on transition-risk implications in financial markets. These may be somewhat hidden at the moment but they are accelerating to a point where the mainstreaming of transition risk into all financial decisions is not that far away.”

He continued: “There is recognition of a significant issue that needs to be understood, and this is beginning to underpin a lot of investment. Relatively soon, this concept will affect access to and cost of capital in a far broader way than just transition-finance instruments.”

Cahill pointed to a growing array of investor alliances, such as the Principles for Responsible Investment and Climate Action 100+, as examples of the coming degree to which capital could be mobilised. These have a focus on implementing Paris Agreement goals into lending decisions.

Cahill also pointed to the role being played by the Network for Greening the Financial System, a group of central banks and prudential supervisors looking at how properly to manage transition risk in the context of their own prudential oversight responsibilities.

Newton agreed that global policy and regulatory settings are headed in one direction, which could make Australia’s increasingly isolated position of not committing to a net-zero carbon by 2050 target a problem for investment. “Policy and regulation will bring more certainty and better outcomes,” Newton said.

While federal-government signals on sustainable finance may remain in relatively short supply for the foreseeable future, Neagle said Australia’s regulatory bodies are beginning to make more noise in the area.

She pointed to the Reserve Bank of Australia’s messaging that climate change exposes financial institutions and the financial system to considerable risk, as well as the reserve bank’s endorsement of a warning that, unless significantly more ambitious action is taken, the impact of climate change could cause global GDP to fall by 25 per cent by 2100.

The Australian Prudential Regulation Authority has also been vocal in its view that transition risk is a prudential risk. In 2020 it announced that it would produce a cross-industry prudential-practice guide on climate-change financial risk, which would set out its views on best practice, governance, risk metrics and disclosure.

ANZ’s Tapley said it is critical for companies to be aware of the developing regulatory environment. She added: “While the prudential regulator only directly regulates the banks, this has a flow-on effect for clients in where capital can be deployed.” This, Tapley said, suggests GSS bond issuance may be a good place for companies to start gaining an advantage on reporting and mitigating against some of the disclosure risk that could be forthcoming.

THE ROAD AHEAD

Australian corporates are operating in an environment where federal policy settings are divergent from international peers and the increasing weight of investor preferences. This potentially creates some friction, if not for the scale of corporate engagement then at least for its speed.

At the same time, there is no shortage of sustainability leaders in the Australian corporate landscape – including some that issue labelled debt instruments and others that do not. More companies than ever are incorporating a transition to a low-carbon economy to their short-, medium- and long-term strategies.

For some this may be investor-driven, but for others it is just prudent business strategy. Bradburn said at the KangaNews conference: “We are not doing this because our investors and financiers want it, we are doing it because our customers want it and it is good business. Letting investors know what we are doing, as opposed to being reactive, is also important.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

Sydney Airport the latest domino to fall as Australia’s corporate market proves its mettle

Sydney Airport’s largest-ever transaction in the Australian dollar market – which is also its first public domestic deal since 2011 – provides another sign of growing corporate borrower confidence in the local funding option. The chance to access extended tenor at volume in line with a global core market benchmark print clearly moved the dial for an issuer that has historically been wary of the reliability of domestic issuance.

Adelaide Airport rekindles investor relations in domestic return as it hits funding turning point

Following its first Australian dollar deal in seven years, Adelaide Airport says re-engaging with the local investor base was a top priority as it embarks on a new capex plan and plans for upcoming maturities. While issuance has slowed since a hectic end to Q1, the deal book demonstrates ongoing robust demand for Australian dollar corporate credit.