The big renewal

One of the most exciting aspects of sustainable finance from a capital-market perspective is the potential for the transition to a low-carbon economy to produce a huge supply of investible assets in a world that has been capex constrained. Westpac Institutional Bank is taking a lead position in Australia’s renewable-energy space – a key sector for investment growth.

Perhaps contrary to some perceptions, renewable-energy facilities are not new in Australia. Solar started playing a role in the national power grid 10-15 years ago, wind facilities have existed for more than two decades and before these the country derived a small portion of its grid power from hydro generation.

Renewables contributed around 15 per cent of Australia’s total electricity generation by the end of 2018 according to International Renewable Energy Agency data. This is comparable with the US but significantly lower than other developed nations: the equivalent figure for Germany was 46 per cent, for the UK 33 per cent and for New Zealand 84 per cent.

Australia’s renewable-energy contribution had climbed to around 20 per cent of the total by the end of 2020 according to Westpac. But there is clearly still significant potential in the transition process – and the time to do it is fast approaching if it has not already arrived.

The vast majority – around 90 per cent – of coal-fired generation capacity in New South Wales (NSW) will reach the end of its functional lifespan by the mid-2030s. The increasing cost-effectiveness of renewable-energy sources, growing global concern about the impact of climate change and stranded-asset risk in the fossil-fuel space suggest the most rational course of action will be to replace the expiring capacity with renewable energy.

States and territories are mainly well progressed with the transition to renewables – perhaps most notably the Australian Capital Territory and South Australia. Most have made flightpath commitments to either or both of a proportion of power from renewables or net-zero carbon emissions (see table).

Australian state and territory progress on renewable energy

| State/territory | Net-zero emissions target | Proportion of renewable energy target | Proportion of renewable energy in 2019 |

|---|---|---|---|

| Australian Capital Territory | 2045 | 100% | 100% |

| New South Wales | 2050 | None | 17.1% |

| Northern Territory | 2050 | 50% by 2030 | 8% |

| Queensland | 2050 | 50% by 2030 | 14.1% |

| South Australia | 2050* | 100% by 2030 | 52.1% |

| Tasmania | 2050 | 200% off current need by 2040 | 95.6% |

| Victoria | 2050 | 50% by 2030 | 23.9% |

| Western Australia | 2050 | None | 20.9% |

*Also to reduce emissions by 50% below 2005 level by 2030

Source: Clean Energy Council, state governments 2020-21

It is the states that will drive investment in renewable energy. The scale of the task is vast even at current commitment levels. Myles Walkington, relationship manager, infrastructure and utilities at Westpac in Melbourne, points to NSW’s now-legislated energy roadmap as an example.

“Part of this is what is called ‘renewable-energy zones’ – effectively the placement of a lot of renewable-energy generation in areas where it makes sense and ensuring the appropriate network connections are in place to deliver the energy to where it needs to go. The state government’s expectation is that these renewable-energy zones could attract more than A$30 billion [US$23.2 billion] of private investment over the next 10-15 years,” Walkington says.

WIDER OPPORTUNITY

Nor is electricity transition merely a story of like-for-like generation replacement. There is no shortage of investment opportunities in the generation space and Westpac has supported more than its share of these (see box).

But two further system-wide issues are also at play: the fact that a predominantly renewables-based electricity grid works in a fundamentally different way from a fossil-fuel-powered one, and the likelihood that aggregate demand for grid power will grow substantially as part of an economy-wide low-carbon transition.

“One aspect of the transition is the shift from very large power stations with heavy load interconnect shipping into a central grid, to more distributed energy with smaller power stations that tend to be further away,” says David Scrivener, global head of energy, infrastructure and resources at Westpac in Melbourne.

He explains that this aspect of planning for the power network forms another piece of the NSW energy roadmap – not just designating and developing renewable-energy zones but also adding suitable connections to them so they can reliably transmit energy when and where needed. This marks notable progress, Scrivener adds, from a historical focus on building projects while neglecting the fact that they might be at the end of skinny, low-capacity transmission lines.

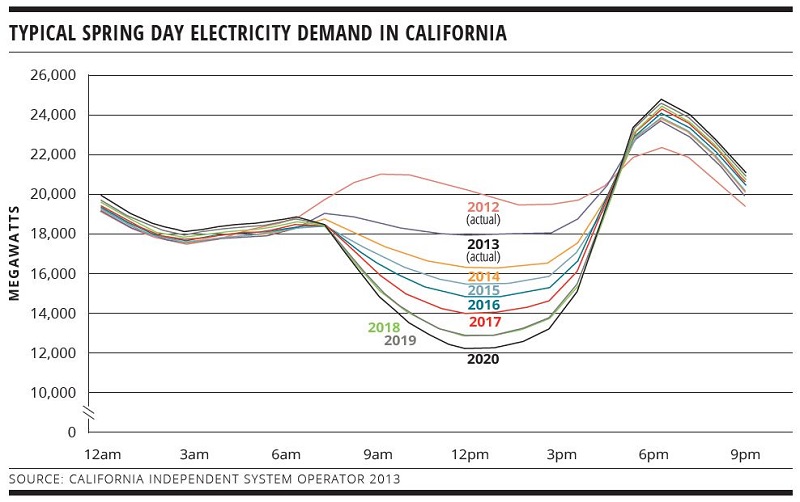

Of perhaps even more significance is the way demand patterns will shift as the source of power generation changes. In particular, increased take-up of household solar generation is likely to produce the “duck curve” – a pattern of electricity supply and demand that increasingly flexes around daylight hours (see chart). As household solar generation increases during the day, demand for electricity from the grid drops. As the sun sets and people return home in the evening, network demand rises to a peak.

Household battery storage is still a nascent technology, although some energy retailers are exploring how they can work with households to install batteries to help manage supply and demand. Meanwhile, major projects like Hydro Tasmania’s “battery of the nation” – a 4.5-5GW battery that will be used to balance the grid as it moves from coal-fired power to more intermittent styles of generation – are already demanding investment capital.

Powered up: Westpac's commitments and project outcomes

Westpac Institutional Bank’s renewables team says the pace of project financing in their sector has never been greater. The bank is committed to deploying balance sheet and deals are closing thick and fast.

“Westpac recognises that climate change is one of the most significant issues that will impact the long-term prosperity of the global economy and our way of life,” says the bank’s 2020 Sustainability Performance Report. “As a financial institution, we believe the most constructive role we can play is to work with customers and communities to respond to the challenge of climate change.”

Five core principles guide and inform Westpac’s approach to climate change: the need to transition to a net-zero-emissions economy by 2050, the complementary nature of economic growth and emissions reduction, that addressing climate change creates opportunities, that climate-change risk is a financial risk, and the need for collective action, transparency and disclosure.

Either way, the capex component will be substantial. “We are still working through questions around how to plan a network under these conditions. Who operates and has control of it will also become an interesting issue,” Scrivener says.

The importance of answering these questions will only be heightened by the wider process of electrification. Take-up of electric vehicles is still minimal in Australia but 2019 government analysis predicted that half of new vehicle sales will be electric by 2035 even at the current rate of market growth. The transition away from petrol-powered cars will naturally mean more demand on the electricity grid.

The extent of this additional demand may be impossible to estimate accurately as Scrivener suggests a wholesale transmission to electric vehicles brings several variables into play.

“The question to answer is when users plug in,” he suggests. “If they all do so at the same time, peak energy demand will go through the roof. On the other hand, if everyone times charging their cars when wind power is abundant – for example in the very early morning when there is also typically lower demand on the network – there might not be the need for as great an increase in capacity.”

The same applies, Scrivener continues, if there is a continued buildout of solar power in the sunnier states and improved interconnection between the states to distribute this power. A figure of A$80 billion might not be an unreasonable estimate of the scale of investment needed to power a full-scale transition to electric vehicles, he argues.

“The grid was designed a century ago and needs to be made fit for purpose,” Scrivener concludes. “The good news is that all the regulated transmission distribution companies are alive to this change. But it is inevitable that we will need a significant amount of capital to deal with the transition.”

FUNDING METHODS

The pipeline of this capex to the debt capital market is likely to be protracted but should in time produce new credit issuance – potentially in labelled-debt format. The slow transmission is a result of the age-old disconnect between bond financing and greenfield infrastructure development.

“Debt capital market issuance has not to date been looked at for renewable-energy projects that are done via traditional project financing,” Walkington acknowledges. “This primarily reflects the fact that they tend to be in the sub-to-just investment-grade credit profile.”

The Australian policy landscape remains relatively infertile soil for the type of revenue certainty bond markets tend to crave. Scrivener explains, for instance, that some German renewable-energy project finance has achieved bond-market funding because generators were given a guaranteed tariff by the government for the life of the project. Australian renewable-energy assets still offer attractive investment opportunities but they tend to carry merchant-power risk – which makes investment-grade bond issuance challenging.

Even so – and setting aside the theoretical potential for more esoteric funding mechanisms like multiple-project securitisation – the scale and breadth of the transition task in Australia is likely to provide debt-capital-market opportunities.

“The more likely piece is in electricity transmission, investment in which will drive additional capital-market issuance,” says Scrivener. “Typically, a regulated-utility company is one piece of an entity that also builds bespoke transmission lines for renewable-energy projects on an unregulated basis. These entities can secure 25-year contracts and we have seen some capital-market issuance off the back of them, including long-dated, 25-year paper being written.”

It is also possible that renewable-energy projects with mainstream, established sponsors from the electricity and resources sectors could be used as eligible assets for use-of-proceeds green bonds. There may be something of a Goldilocks factor here, however. Scrivener points out that while standalone projects may not offer a bond-market-suitable credit profile, the other side of the same coin is that major global energy companies – the likes of BP, Shell and Total – tend to be cash-rich and thus not in great need of capital-market funding for specific projects.

The middle road is likely to be local power and utility companies, and banks themselves. Near-term conditions have all but removed Australia’s major banks from wholesale funding markets, but they are likely to be keen to explore further green-bond issuance as and when they return. Electricity transition could be a crucial source of suitable assets.

“Green lending will inevitably drive more green-bond issuance. From a Westpac perspective, lending to renewable-energy projects can be wrapped up in our green-bond programme – which should enable Westpac to issue more green bonds. The decision ultimately is with group treasury but certainly the billions of dollars of capex will create more capacity for our green programme,” Scrivener suggests.

Sponsored by

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news