Fixed-income investor survey: pandemic risks abating

The 2021 iteration of the Fitch Ratings-KangaNews Fixed-Income Investor Sentiment Survey suggests Australian investor concern about COVID-19-related risk has eased. The buy side expects lending conditions to loosen further and net issuance to rise across asset classes – all predicated on the expectation of and reliance on support from ongoing unconventional monetary policy.

Helen Craig Head of Operations KANGANEWS

Matt Zaunmayr Deputy Editor KANGANEWS

More than 40 investors completed the survey in March 2021, up from the pandemic-affected numbers in March 2020 and once again representing the bulk of the Australian real-money fixed-income investor base. Participating accounts include traditional asset-management firms, pension funds and insurance companies.

KangaNews conducted the previous iteration of the survey at a point in 2020 when market conditions were unravelling at an accelerating pace. Fixed-income markets, along with the rest of the world, were approaching or had reached panic mode as COVID-19 spread on every continent, forcing unprecedented economic lockdowns and border closures. This made for a uniquely pessimistic – but hardly unrealistic – set of results in 2020. Australians had been warned by their government to prepare for lockdown conditions to persist for six months – the consequences of which would have been economically devastating.

Despite the unique timing of the 2020 data set, the strength of the rebound in sentiment by March 2021 is notable. The ability of Australian state and federal governments largely to avoid widespread COVID-19 infection and thus maintain a relatively elevated level of economic activity over the past 12 months, plus the emergence of several viable COVID-19 vaccines, clearly contributed to the perceived abatement of many risks investors identified as elevated in March 2020.

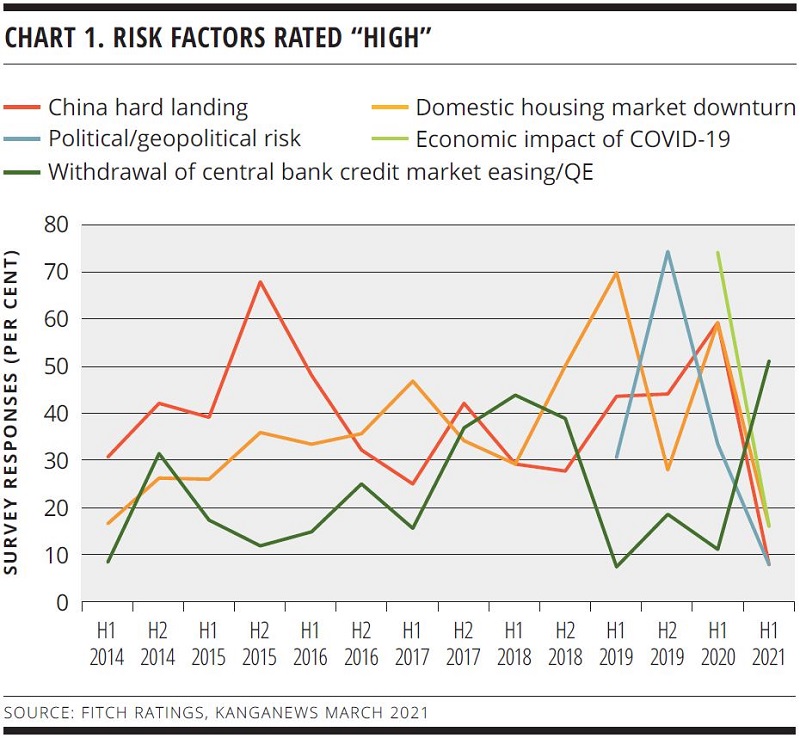

Among these, in 2021 the perceived risks of economic impact from COVID-19, a domestic housing-market downturn and a Chinese economic correction plummeted compared with 2020. Political and geopolitical risk also continue to fall from a peak in the second half of 2019 (see chart 1).

Fitch’s analysts point out that Australia’s economic contraction in 2020, of 2.4 per cent, was much less severe than the 3.8 per cent median for AAA-rated economies. They attribute this to the country’s successful containment of COVID-19 and effective policy response. As such, investor expectations for leading economic indicators such as unemployment and house prices have turned around to a startling degree.

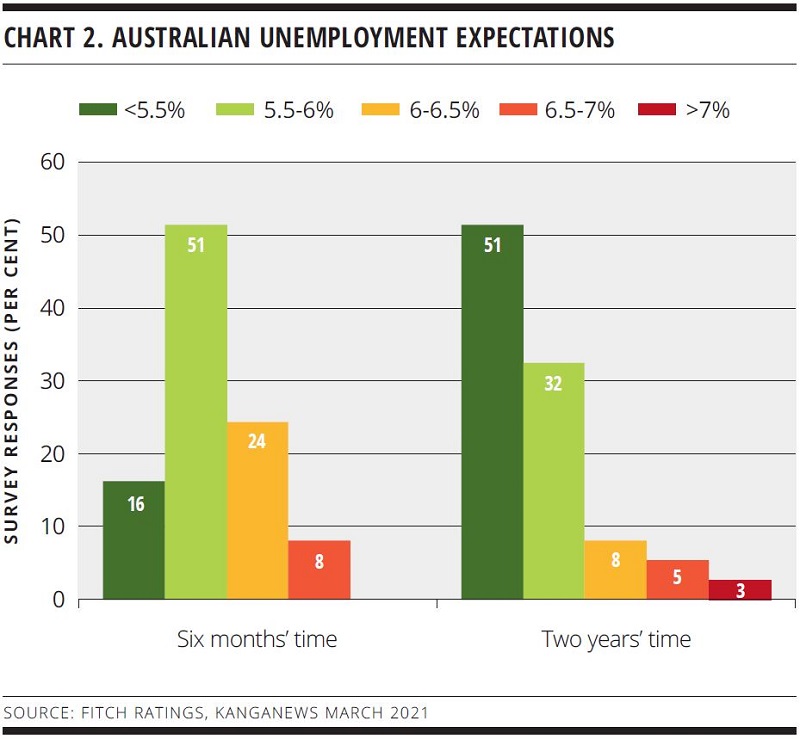

In March 2020, despite some responses coming in before the initial full lockdown in Australia, expectations for unemployment were already grim. Now, most investors expect unemployment to be less than 6 per cent in six months and to fall below 5.5 per cent in two years’ time (see chart 2).

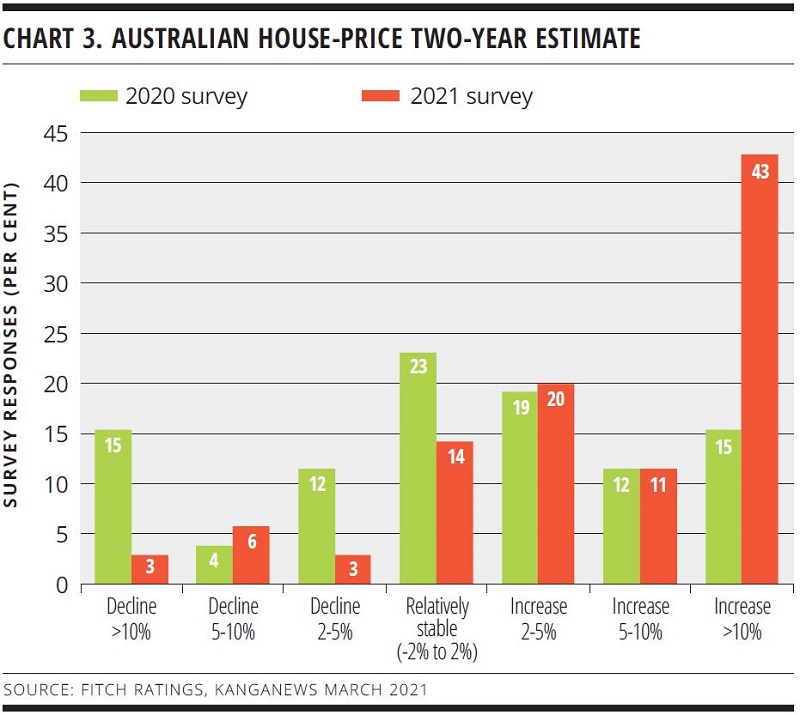

Similarly, investors now almost universally expect house prices to rise over the next two years after widespread predictions of house-price decline in 2020 (see chart 3).

The results also show, however, that debt markets remain largely reliant on unconventional monetary policy for stability. More than 50 per cent of respondents identify the withdrawal of QE as a high risk over the next 12 months.

Fitch expects supportive monetary policy will remain in place for at least the next two years. “Wage growth and inflation should rise only gradually towards the Reserve Bank of Australia (RBA)’s 2-3 per cent target band in light of the sustained slack in the labour market relative to the central bank’s natural unemployment rate estimate,” write Fitch’s analysts.

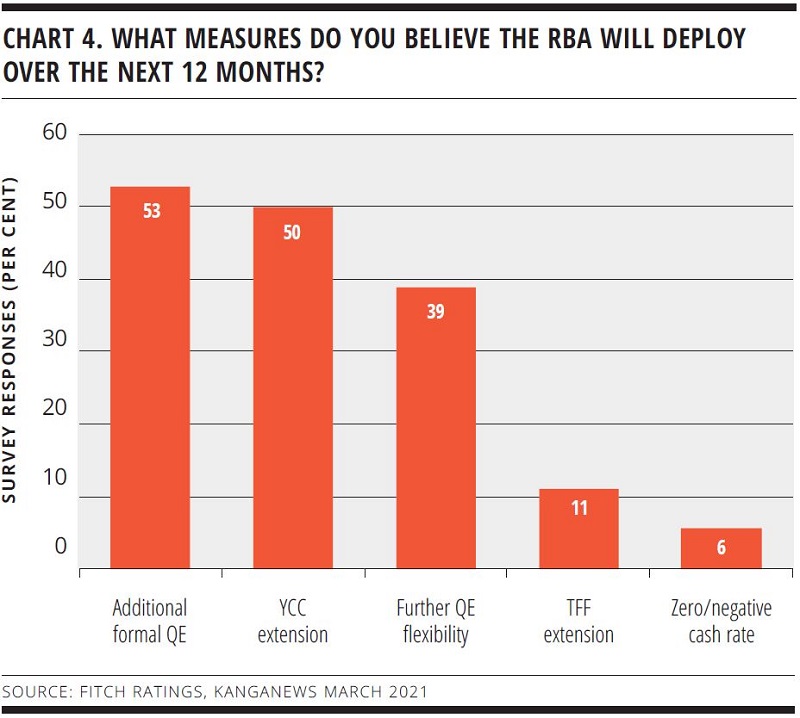

There is little love for the ‘reflation trade’ among the Australian domestic investor base at present. Fitch expects the RBA to maintain its cash rate at 0.1 per cent for the foreseeable future, as do 88 per cent of survey respondents. Investors in fact indicate a strong belief that further unconventional monetary policy or macroprudential measures will come online over the next 12 months (see chart 4).

CREDIT DYNAMICS

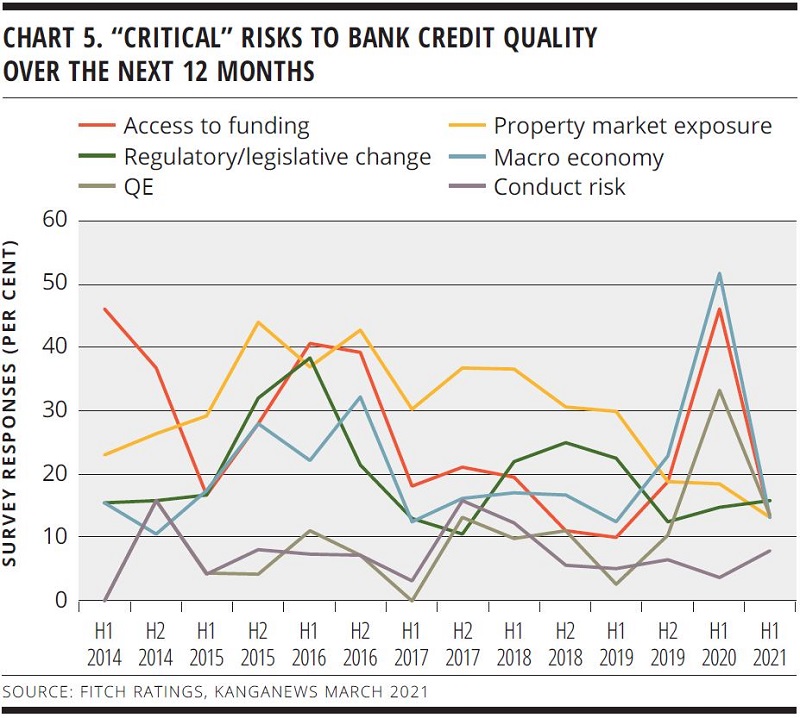

As the overall market and economic picture improves, it is not surprising that perceptions of risks to Australian bank credit have also improved dramatically.

Many investors regarded risks related to the economy, funding and QE as critical in 2020, while in 2021 no more than 15 per cent of survey respondents label any of these factors as a critical risk. The risk most often regarded as critical in 2021 is regulatory and legislative change (see chart 5).

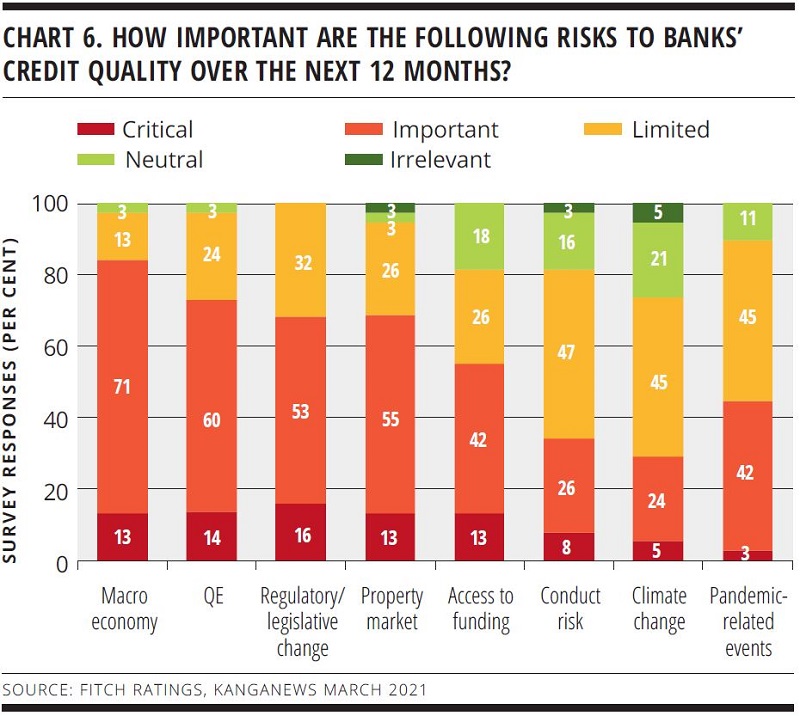

However, most investors still regard risks such as the economy and path out of COVID-19 as “important” for bank credit (see chart 6). Fitch says risks to Australian banks from the economic shock caused by the pandemic have eased in recent months. But its analysts are still wary of a bumpy recovery. “We still expect asset-quality metrics to weaken throughout 2021 as borrower support measures are unwound.

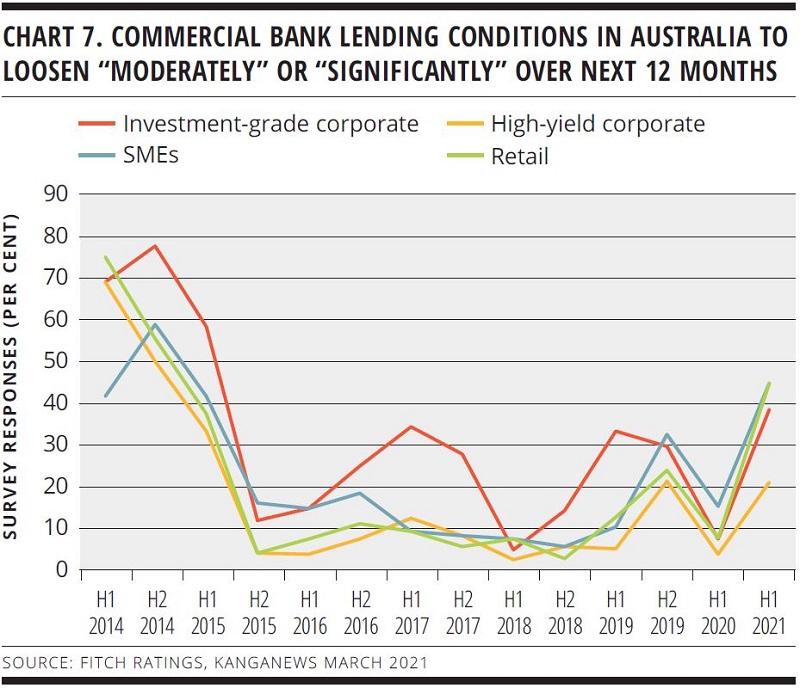

Loans to sectors hit hard by the pandemic are especially vulnerable, but these exposures are low and should not pose significant risks to bank capital positions,” Fitch’s survey report explains. Regardless, a greater proportion of investors than at any point in the survey since 2015 expect commercial-bank lending conditions to loosen over the next 12 months. This result is particularly evident for investment-grade corporates, SMEs and retail (see chart 7).

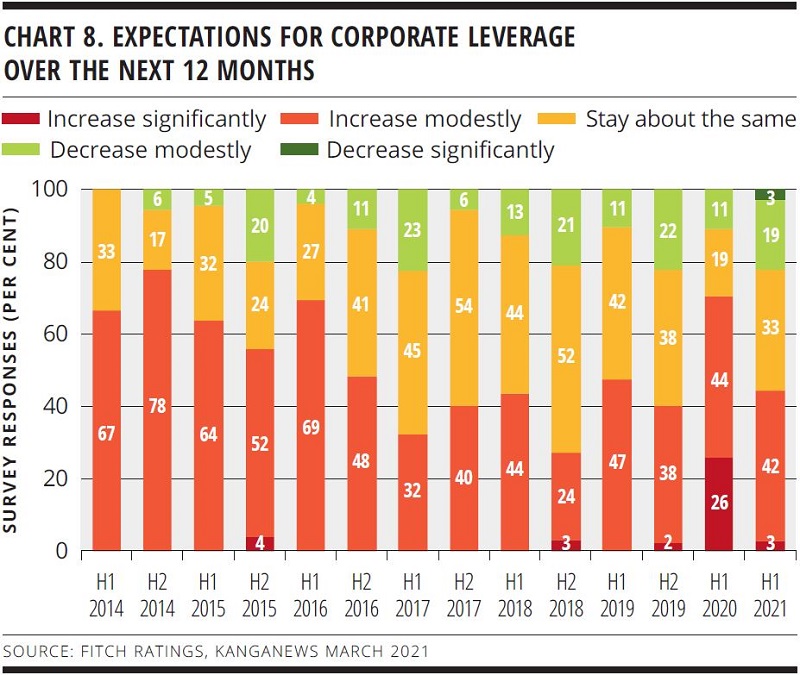

In a microcosm of the challenge facing policymakers as they attempt to stimulate economic growth, Australian fixed-income investors believe funding will remain readily available – but there may be few takers for new credit in the business sector. A much lower proportion of 2021 survey respondents believe corporate borrowers will increase leverage compared with 2020. For the first time in the survey’s history, a portion of respondents even expect a significant drop in corporate leverage (see chart 8).

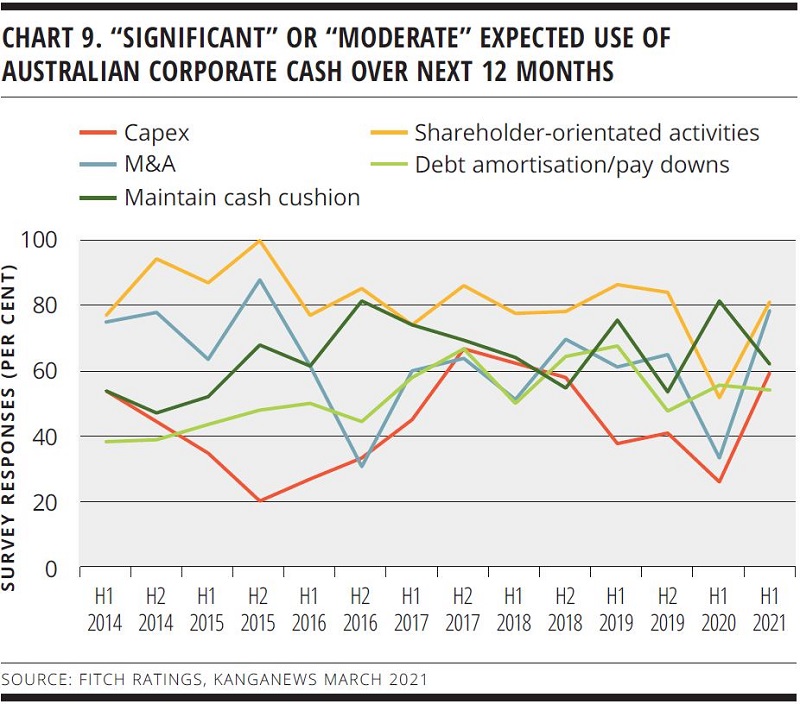

Investors are also expecting corporates to return to more normal uses of cash, such as shareholder-oriented activities and M&A, in the next 12 months compared with this time last year when maintaining cash cushions was expected to be high on the agenda (see chart 9).

Fitch says: “Overall, we expect structural and industry changes to return as key earnings drivers for Australian corporates and believe companies with structural advantages to adapt to change will benefit; for example, our expectation for a flight to quality in retail and office property.”

MARKET MOVES

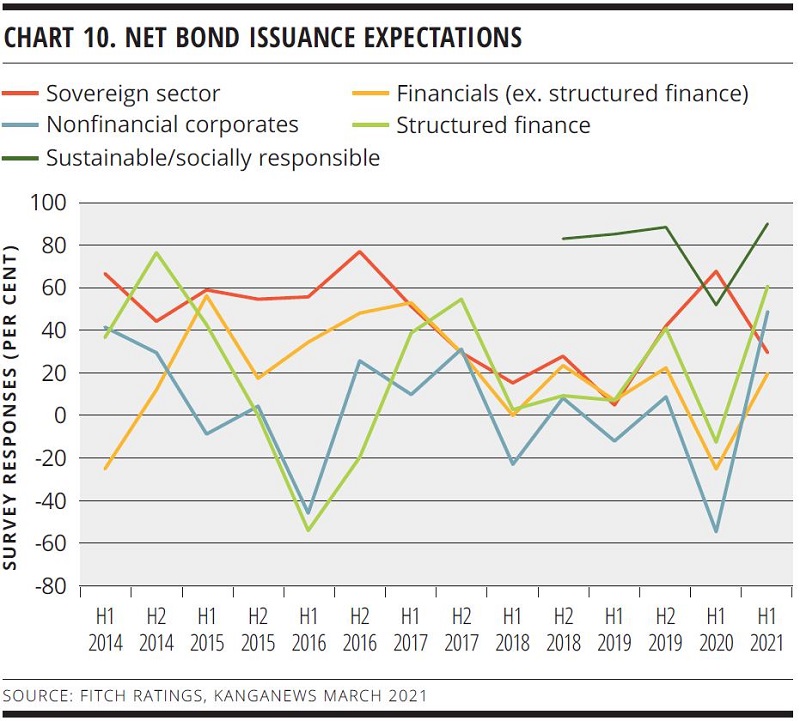

In March 2020, the COVID-19 crisis meant investors did not expect a rebound in debt issuance from any sector outside the sovereign and state governments. However, policy responses eventually enabled strong issuance across sectors and markets in 2020 – with the notable exception of banks. Investors believe trends from H2 2020 will persist in the current year.

The corporate sector has experienced the biggest swing in net-issuance expectations over the last 12 months, but structured-finance and financial-institution issuance are also strongly expected to rise. Expectations for sovereign issuance are down on 2020 but remain net positive (see chart 10). This is coming off an unusual base in H1 2020, when government-sector borrowing soared and banks were effectively absent from the wholesale funding market.

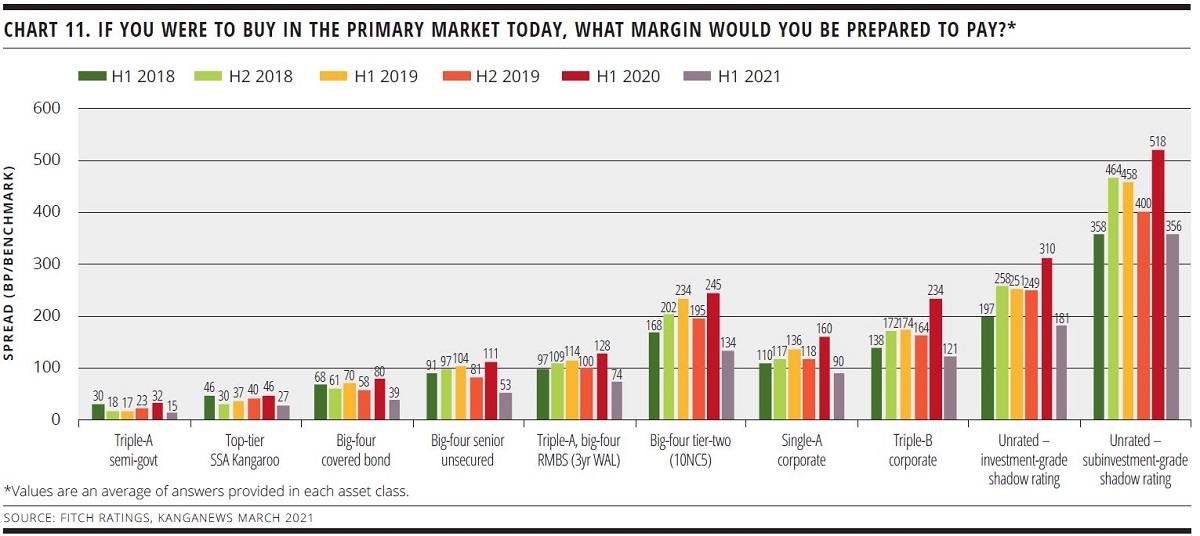

Unsurprisingly, the margin investors expect to pay for all asset classes declined significantly over the last 12 months (see chart 11). For many asset classes the results are a record low in this survey’s history.

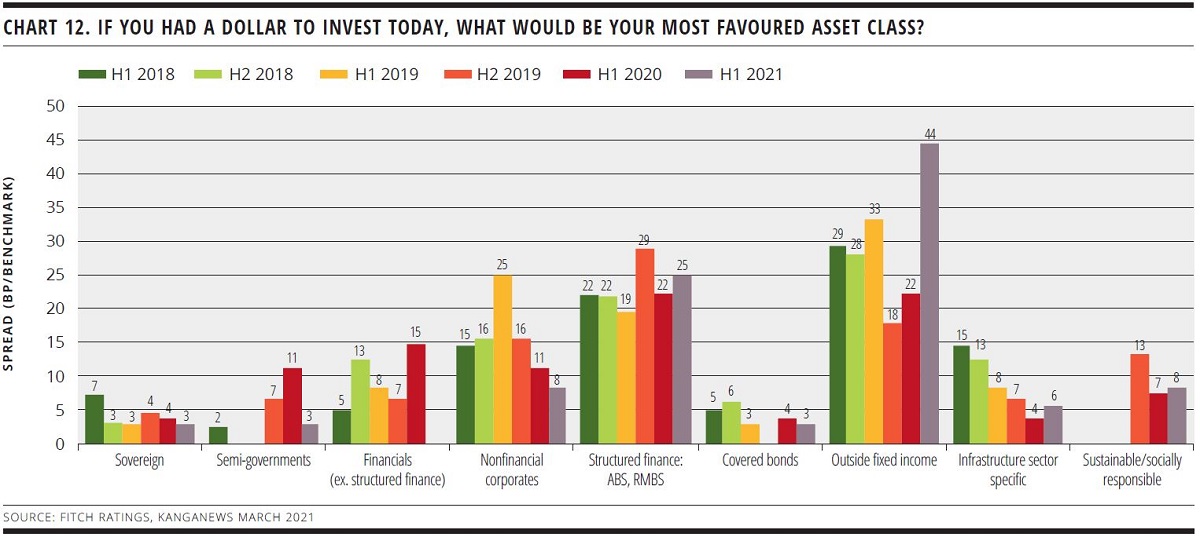

More than half of survey respondents expect an increase in fixed-income assets under management over the next 12 months, the second-highest result for this category in the survey’s history. However, nearly 45 per cent of investors identify assets outside fixed income as their most favoured asset class. Structured finance is the most popular of the fixed-income options (see chart 12).

Sponsored by

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news