Securitisation market sets in for another deal surge

The Australian securitisation market is in the middle of another issuance deluge. Similar to the last concentration of deals, in March and April, a variety of issuers report strong demand producing record transaction volume and pricing. There is also more supply on the immediate horizon.

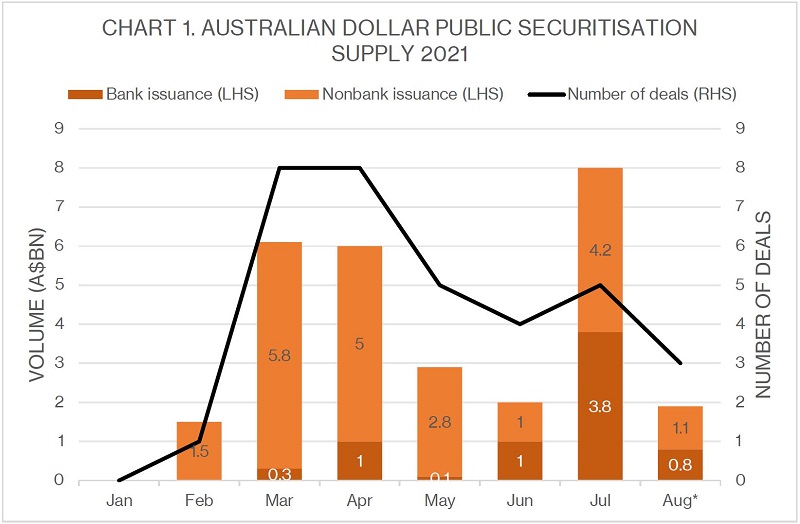

The last flurry of securitisation issuance around the end of Q1 was followed by quieter, though still solid, months of supply in May and June. Supply has ramped up once again since the beginning of the new financial year (see chart 1).

It is not uncommon for Australian securitisation issuance to come in clusters, but in 2021 the market has been turbocharged by supply factors including strong growth across the lending market, and by demand factors such as ongoing undersupply of bank vanilla bonds.

As such, volume and pricing records have been repeatedly broken. Among the notable deals to come since the beginning of July are a A$3.8 billion (US$2.8 billion) transaction from Macquarie Bank and issuer volume records for Metro Finance, Bluestone Group and RedZed.

Meanwhile, Columbus Capital set a new nonbank pricing record for its deal and Great Southern Bank (GSB) set a new post-2008 pricing record for a capital-relief transaction.

Source: KangaNews 10 August

Programmes coming to market have also been new and varied. Plenti printed its debut auto asset-backed securities (ABS) deal on 5 August and Bluestone Group debuted its prime residential mortgage-backed securities (RMBS) programme on 21 July. Supply includes bank and nonbank prime RMBS as well as nonbank nonconforming and auto ABS (see table).

Australian securitisation deals priced 21 July – 6 August 2021

| Pricing date | Issuer | Pool name | Asset type | Volume (A$m) | Senior pricing (bp/1m BBSW) | Leads |

|---|---|---|---|---|---|---|

| 21 Jul | Bluestone Group | Prime 2021-1 | Prime RMBS | 700 | 75 | CBA, MB, NAB |

| 28 Jul | Columbus Capital | Triton 2021-2 | Prime RMBS | 1,500 | 70 | CBA, NAB, Natixis, SC, WIB |

| 30 Jul | La Trobe Financial | La Trobe Financial Capital Markets Trust 2021-2 | Nonconforming RMBS | 1,250 | 80 | Citi, CBA, HSBC, MB, NAB, Natixis, UOB, WIB |

| 4 Aug | RedZed | RedZed 2021-2 | Nonconforming RMBS | 750 | 80 | CBA, NAB, WIB |

| 5 Aug | Plenti | Plenti Auto 2021-1 | Auto ABS | 306.3 | 80 | DB, NAB |

| 5 Aug | Great Southern Bank | Harvey 2021-1 | Prime RMBS | 750 | 60 | ANZ, MB, NAB, WIB |

Source: KangaNews 6 August 2021

More deals are in the immediate pipeline. Pepper launched its A$850 million PRS 30 RMBS transaction on 9 August while Firstmac is preparing an inaugural deal from its Eagle RMBS programme. Think Tank has also begun marketing its debut RMBS deal and Bank of Queensland joined the queue for an ABS deal on 9 August.

Timing considerations

The Australian securitisation market is clearly able to accommodate more deals and more volume in a compressed time period than it has been at any point since the 2008 financial crisis, particularly from nonbank issuers.

Even with multiple deals in the market at once and more in the pipeline, issuers do not indicate that they are concerned with their place in the issuance queue or with buy-side digestion. Instead, deal timing is often more a matter of bringing a transaction when it is ready to go than trying to pick the market perfectly.

As a debut issuer, Miles Drury, Sydney-based chief financial officer at Plenti, says the borrower was keen to make the most a very strong market. But its issuance timing was determined more by the natural progression of its funding and in particular the milestone of its auto lending book surpassing A$300 million.

Paolo Luzzani, head of funding at Plenti in Sydney, says the fact the issuer was offering an auto ABS was appealing for investors given other deals in the market were primarily residential-mortgage assets. This gave Plenti confidence that it would have strong engagement.

Conditions at are also sufficiently compelling to attract even bank issuers that do not have the need constantly to fund through securitisation. GSB’s latest RMBS deal was its first since 2018 and since rebranding from Credit Union Australia. Tim Moore, treasurer at GSB in Brisbane, says the bank did not have an immediate need for funding or capital.

But with uncertainty prevalent in the wider economy, Moore says: “It was important not be complacent and instead make the most of the strong issuance conditions, balancing immediate needs with medium-term considerations best to support the bank’s strategic aspirations.”

He adds that GSB did not want to come into the market at a point of saturation but also was aware of its point of difference for investors as a bank RMBS deal in a market that remains undersupplied with bank paper.

Money on the table

Demand statistics suggest there should be sufficient liquidity for the upcoming deals. GSB’s senior tranche was more than twice oversubscribed and priced 5 basis points inside launch guidance with little attrition according to Moore, while the bank’s junior tranches priced up to 15 basis points tighter than initial guidance.

Meanwhile, Columbus Capital had 1.5 times coverage in its largest senior tranche and 4.5-6.6 times coverage for its class C, D and E notes. The deal’s senior pricing record – 70 basis points over one-month bank bills – was marginally inside pricing expectations according to the issuer’s Sydney-based treasurer, David Carroll.

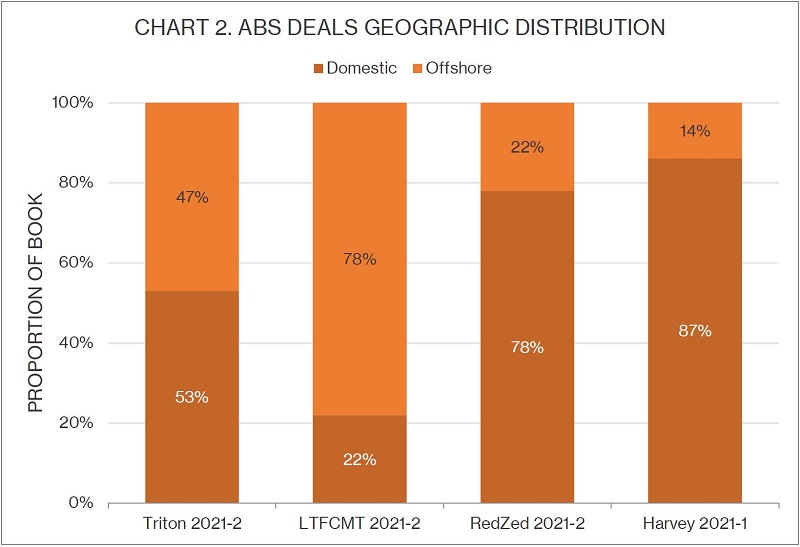

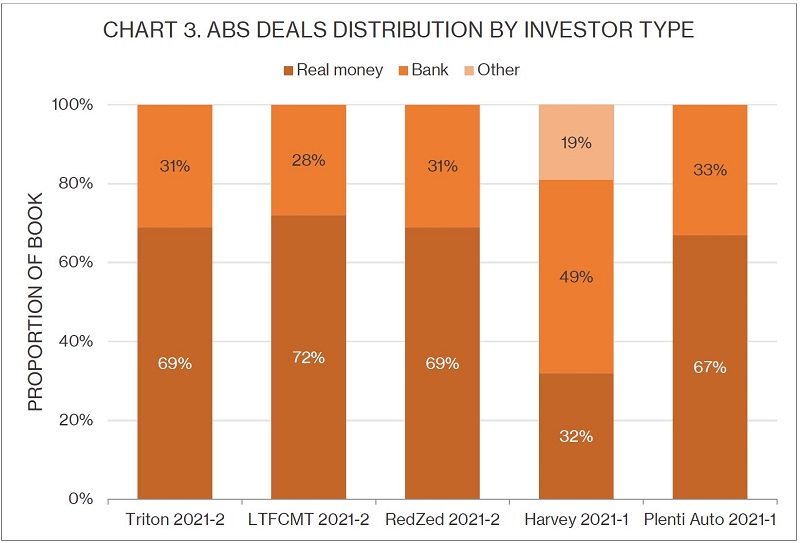

Geographic demand for recent deals vary, with La Trobe Financial and Columbus seeing strong engagement from offshore while unsurprisingly GSB was a majority domestic affair. Real-money accounts are prevalent in all transactions for which KangaNews has received distribution data (see charts 2 and 3).

Source: Columbus Capital, Great Southern Bank, La Trobe Financial, RedZed 9 August 2021

Source: Columbus Capital, Great Southern Bank, La Trobe Financial, Plenti, RedZed 9 August 2021

Rick Li, Sydney-based group treasurer at RedZed, tells KangaNews the issuer had strong engagement across the capital stack for its deal, primarily from domestic accounts but with some offshore investors also involved.

Plenti also reports strong demand with 14 investors participating in its inaugural deal, two of which were offshore accounts. Some of these investors were existing supporters of Plenti, the issuer reveals – but the majority were new.

Luzzani says price guidance was gained by reference to recent comparable ABS deals. He says favourable pricing and ratings attachment points reflect the strength of Plenti’s credit profile.

Volume for growth

Growth in lending across the Australian economy has supported securitisation deal flow and deal volume in 2021. In turn, the securitisation market is providing integral funding and capital for lenders to continue operating and expanding in a competitive lending market.

“With ultra-low mortgage rates it is important to compete on more than just price. We need a compelling value proposition with a consistent strategy based on operational excellence,” Moore says. “Like many banks, we are continuing a transformation journey having recently implemented an improved lending platform – one of many steps to ensure we can provide a seamless and reliable experience to all our customers in our lending processes.”

Moore adds that maintaining a presence in secured and unsecured funding helps GSB’s balance sheet and is important to continue supporting the growth of the business.

Platform optimisation has also been a focus for RedZed and allowed it to print its largest-ever securitisation deal volume. Li says over the last year RedZed has upgraded its systems to gain greater efficiency and scale in its underwriting abilities, as well as improving its distribution platform.

He adds that RedZed’s investment in its lending and origination, as well as its focus on self-employed borrowers who remain underserviced by banks, should allow it to continue growing its customer base.

Drury expects Plenti’s technology will also enable it to continue to grow origination volume. “We are focused on the prime end of the market. Our technology sets us apart and allows us to build a strong book, which we can then bring to the market – hopefully at regular intervals.”

Drury adds that it is likely Plenti will also eventually term out its personal loans and renewables warehouse.

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

Related news