Singapore sling helps quench Australian market’s FI credit thirst

Two Singapore-based banks printed Australian dollar deals via local branches in early August, both achieving pricing records and one brought its green-bond programme back to the local market. Deal sources tell KangaNews the dearth of senior term funding from financial institutions (FIs) means credit spreads should remain tight for the foreseeable future.

Oversea-Chinese Banking Corporation Sydney Branch (OCBC Sydney)’s 5 August deal was also the first FI green bond to price in the Australian dollar market this year. The new transaction is for A$500 million (US$368.5 million) and had ANZ, Commonwealth Bank of Australia, National Australia Bank (NAB), OCBC and UBS as leads.

United Overseas Bank Sydney Branch (UOB Sydney) followed on 10 August, printing a A$750 million tap to its May 2024 line – originally a A$250 million private placement executed in May. ANZ was sole lead manager.

“We hope the reopening of the bonds to a broader and more diverse investor base, to reach a substantial benchmark size of A$1 billion, will improve the overall liquidity of the line and be beneficial to our investor universe,” says Koh Chin Chin, head of group central treasury at UOB in Singapore.

The two banks have already taken advantage of tight Australian dollar attractive margins in the past year. According to KangaNews data, OCBC Sydney’s deal is the tightest three-year, senior-unsecured, Australian dollar deal from any FI since the 2008 financial crisis, excluding government guaranteed transactions (see table), while UOB Sydney printed 2 basis points tighter even than OCBC Sydney’s level for long two-year tenor.

Tightest margin three-year senior-unsecured FI deals in Australia*

| Pricing date | Issuer | Volume (A$m) | Rating (S/M/F) | Maturity date | Margin (bp/swap) |

|---|---|---|---|---|---|

| 5 Aug 21 | OCBC Sydney | 500 | AA-/Aa1/AA- | 12 Aug 24 | 26 |

| 11 Mar 21 | OCBC Sydney | 325 | AA-/Aa1/AA- | 18 Mar 24 | 35 |

| 13 Apr 21 | Rabobank Australia | 500 | A+/Aa/AA- | 19 Apr 24 | 35 |

| 20 May 21 | HSBC Sydney Branch | 500 | AA-/Aa1/AA- | 28 May 24 | 42 |

| 9 Oct 20 | UOB Sydney | 500 | AA-/Aa1/AA- | 16 Oct 23 | 46 |

*Excluding government-guaranteed deals

Source: KangaNews 11 August 2021

Market dynamics

OCBC Sydney’s deal launched at 32 basis points area over three-month BBSW before tightening. Ronald Woo, director, debt origination Asia at NAB in Singapore, tells KangaNews that the margin of 26 basis points over BBSW looked like fair value even ahead of launch but the deal group wanted to test the validity of comps.

“There was some uncertainty as to whether these secondary marks were theoretical given the lack of recent primary supply in senior-unsecured format – [they could have been] simply being quoted at tight levels due to market technicals and may not have been reflective of where a primary-market deal may land,” Woo says.

The ongoing dearth of senior bank issuance has provided a technical tailwind for other FIs and corporate borrowers issuing in Australian dollars. The landscape may be about to change again, however, as National Australia Bank announced plans for a domestic five-year senior-unsecured transaction on 16 August.

Even with major-bank supply to return, market participants expect spreads to hold at or close to recent levels. The demand OCBC Sydney’s orderbook received was substantial, reaching approximately A$2.3 billion with 60 investors participating.

Having already secured a number of anchor orders at the pricing level of 24 basis points over three-month bank bills, UOB Sydney launched its transaction with minimum volume of A$500 million. Kang Jae Jim, head of Asia DCM at ANZ in Singapore, says the execution strategy resulted in “an attractive pricing outcome and satisfied the large investor demand for short-dated paper”.

OCBC green bond

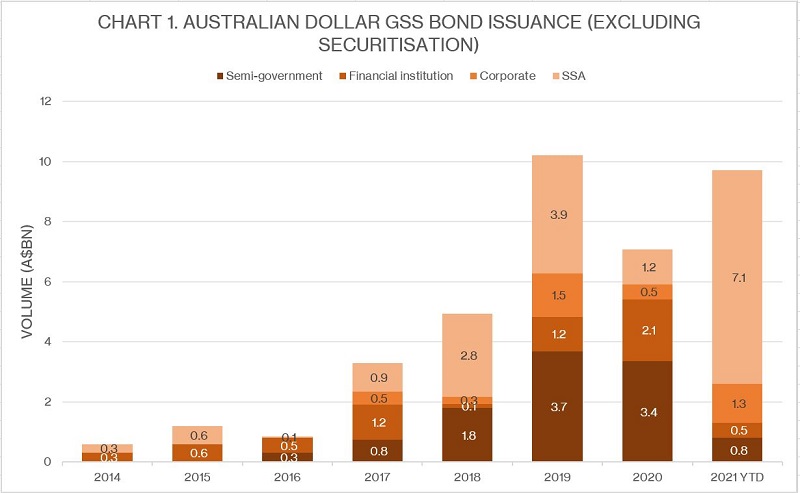

Green, social and sustainability (GSS) bond issuance from FIs has been sporadic in the Australian dollar market. According to KangaNews data, OCBC Sydney’s green bond is the first GSS bond from an FI this year while issuance in 2020 came from ANZ Banking Group, Shinhan Bank and Woori Bank (see chart 1).

Ang Suat Ching, head of corporate treasury at OCBC in Singapore, tells KangaNews the bank recognises the role it plays in promoting long-term sustainable development. “The second OCBC green bond demonstrates our commitment to promote and embrace sustainable financing, which is a priority of our board and management.”

Source: KangaNews 11 August 2021

Ching also says strong investor participation in its inaugural deal was a key determinant in returning to the Kangaroo market. “We have a long-term view toward engaging capital markets… The continuity in our investor engagement was important and it drove our decision to follow up with a second green bond.”

Woo says the green label brought in a number of accounts that typically would not have otherwise participated in the transaction while some investors put in larger orders than they usually would have for a bank deal. “They came in early in the bookbuild process with relatively sizeable tickets and stayed in despite the price tightening,” Woo says. “This clearly helped orderbook momentum from the outset.”

He continues: “One would typically expect the final allocations for a short-dated senior-unsecured floating-rate note to be dominated by bank treasuries as opposed to asset managers, as this is more of a natural fit from an asset-liability match perspective. The dynamic was flipped in this transaction.”

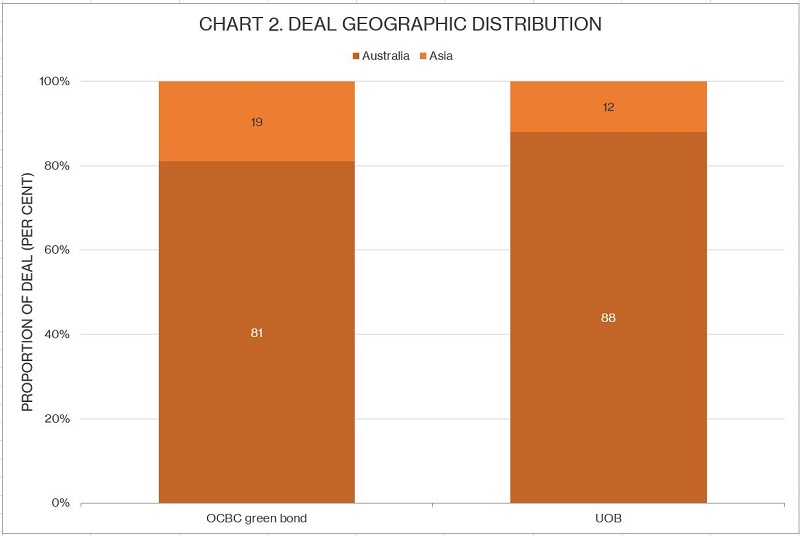

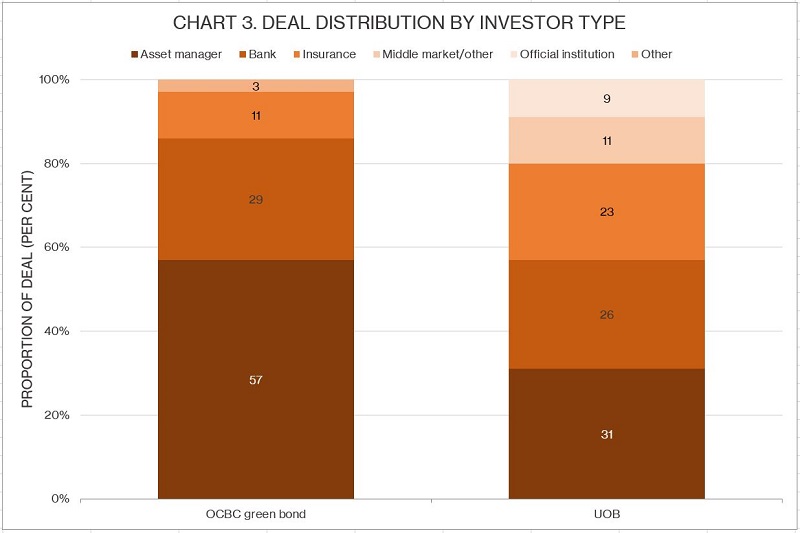

Indeed, the majority of OCBC Sydney’s transaction went to asset-manager accounts (see charts 2 and 3).

Source: ANZ, National Australia Bank 11 August 2021

Source: ANZ, National Australia Bank 11 August 2021

From the peak orderbook of A$2.6 billion, Woo says most of attrition came from bank treasuries. “They were very well represented throughout the bidding process, alongside real-money accounts, but as we tightened from initial price guidance by 4-6 basis points a number of bank treasuries dropped or scaled back their orders.”

KangaNews understands a large proportion of the demand out of Asia participated in the transaction specifically for the green-bond element, with a tailwind provided by the fact labelled issuance from FIs in Australian dollars has been difficult to come by of late.

Like its first green bond, OCBC Sydney’s eligible green assets include renewable energy and green buildings in Singapore and Australia. “OCBC has a growing portfolio of Australian green projects to support the country’s transition to a low-carbon economy,” Ching says.

In June last year, OCBC set a 2025 target of S$25 billion (US$18.5 billion) for its sustainable-finance portfolio, having surpassed its original S$10 billion target in the first quarter of 2020 – two years ahead of its 2022 schedule. Ching adds: “Accompanying our goal, we have also launched a suite of sustainable financing products across different customer segments such as eco-care home and renovation loans, and SME sustainable financing loans.”

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news