Holding pattern

Inflation speculation has intensified in 2021 as the world slowly emerges from the COVID-19 pandemic. Even so, investors in the world’s major inflation-linked-bond markets are in a holding pattern amid a mid-year rates rally based on renewed economic scepticism. The big question for markets is what might break the deadlock on inflation outlook.

Matt Zaunmayr Deputy Editor KANGANEWS

After a decade of stagnation, inflation indicators in the world’s major economies ran hot in the first quarter of 2021. The rollout of COVID-19 vaccines spurred sooner-than-expected reopening of economies, which – coupled with ongoing stimulus – convinced many that inflation was more of a risk than at any time since the 2008 financial crisis.

Inflation in the world’s major markets is higher in the middle of 2021 than it has been for many years. The US is reporting the most compelling figures: a 0.9 per cent consumer price index (CPI) increase in June equating to an annualised rate of 5.4 per cent. The monthly number softened slightly in July, to 0.5 per cent, but annualised inflation held steady at 5.4 per cent.

In the UK, the annual figure for June was 2.5 per cent and in Europe it was 2.2 per cent for July. The inflation target for the UK and the EU is 2 per cent.

Central banks so far remain convinced that these inflation prints are largely transitory – reflective of supply shocks wrought by COVID-19 a year ago – and that further monetary-policy stimulus by way of asset purchases and ultra-low interest rates remains necessary to set economies on a sustainable growth trajectory out of the crisis (see box).

Investors are sceptical, and many are preparing for a world where inflation is more of a risk than at any other time in the last decade. A BofA Securities survey of global fund managers – with total assets under management of more than US$800 billion – identified inflation as the most prevalent tail risk for the second month in a row in July this year.

Central-bank tapering, asset bubbles and a Chinese economic slowdown round out the top four tail-risk concerns for investors in the survey, with COVID-19 itself well down the list of considerations.

STATE OF PLAY

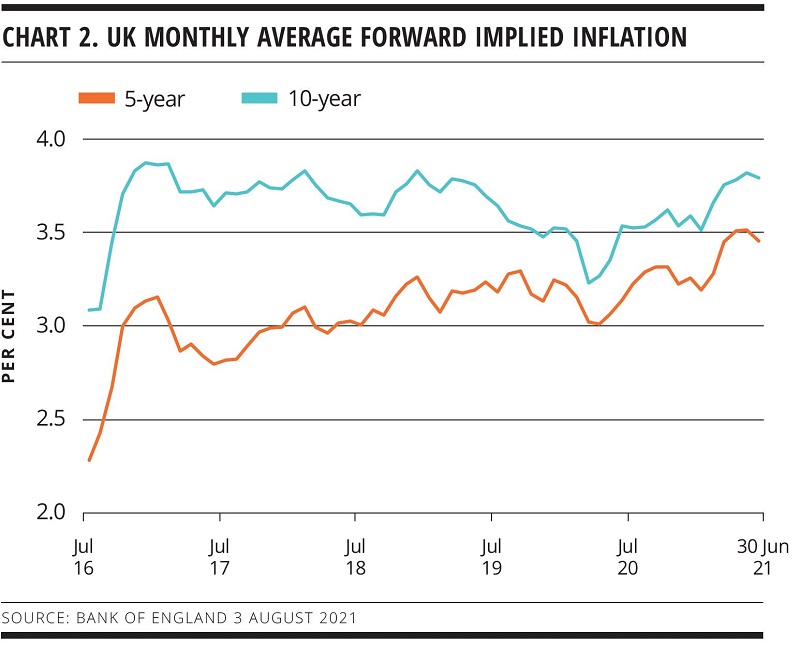

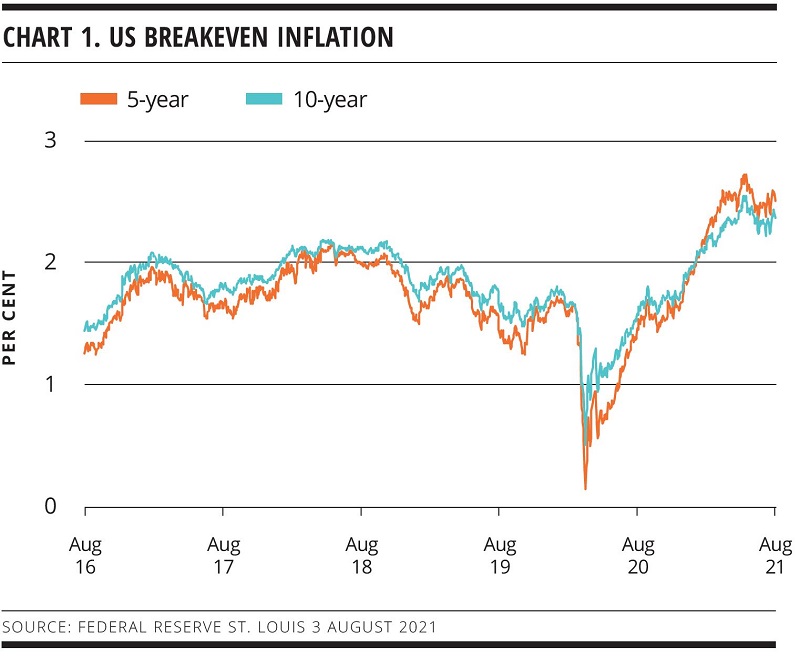

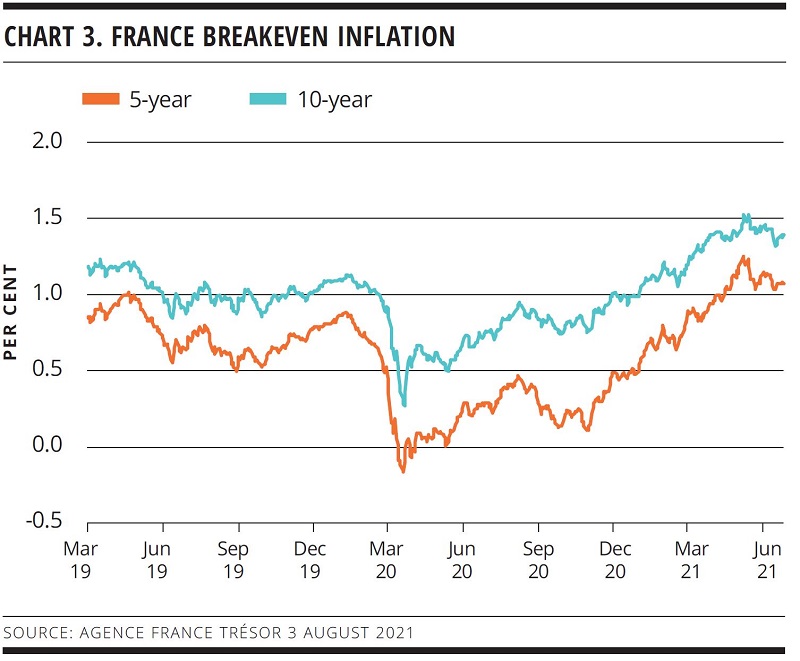

Reflecting this sentiment, demand for inflation-indexed bonds (IIBs) has picked up across global markets over the course of 2021. Short- and medium-term breakeven inflation rates, particularly in the US but also in the UK and France, are higher than at any point in recent years (see charts 1, 2 and 3).

Guy Winkworth, managing director at Deutsche Bank in London, tells KangaNews investors have transitioned through several waves of sentiment on inflation expectations since the first quarter of 2020 when the COVID-19 crisis hit.

First was the disaster of complete economic shutdown and the resulting attempts to stimulate economies, after which the emergence of some supply-side shocks led to expectations of short-term inflation. By the beginning of 2021, it was widely accepted that base effect would result in elevated inflation prints in the near term.

“We are now are in a holding phase, as short-term inflation outcomes peak and we wait to see whether or not inflation is structural and passes through to wages as the base effects tail off,” Winkworth explains.

This holding pattern can also be seen in the world’s major IIB markets. Breakeven and forward inflation levels tracked sideways in the US, UK and Europe in the second quarter of 2021 after rising over the preceding quarters.

At the same time, however, nominal yields have rallied. When they widened significantly over the first quarter of 2021, breakeven inflation moved in lock step. But the fact that they have held at higher levels while nominal yields have fallen suggests ongoing demand for IIBs based on higher inflation expectations.

The wrestle between those expecting inflation to be transitory and those in the sustained camp is playing out in breakeven inflation rates, according to Gennadiy Goldberg, senior US rates strategist at TD Securities in New York.

He tells KangaNews: “This sideways grind in breakevens is a factor of the market’s uncertainty about whether inflation is indeed transitory and how long it could last. If the Fed [US Federal Reserve] is correct and inflation starts to cool, investors do not want to be exposed to too much risk. Equally, they do not want to exit IIBs due to expectations that inflation will remain elevated at least in the near term.”

The inverted shape of the US Treasury inflation-protection security (TIPS) breakeven curve hints at an emerging consensus that inflation may be transitory. Phear Sam, vice president, rates strategy at BofA Securities in Sydney, says: “Short-term inflation expectations are currently higher than longer-term ones.

This reflects expectations that some price pressures will not be sustained over the longer term and is consistent with the Fed’s commentary that inflation will be transitory.”

At the same time, Sam adds: “We have seen a repricing of central-bank hiking expectations, which puts a brake on the possibility of inflation overshooting target levels. This, combined with renewed uncertainty about COVID-19 and its effect on the economy with the spread of the delta variant, means we probably need to see real evidence of output gaps closing before we can be confident that inflation will be sustained.”

Central bank sentiment

Central banks are dealing with difficult conditions in 2021. Almost uniformly, they face economies that are growing and prices that are inflating rapidly, while they need also to maintain extraordinarily loose monetary policy to guarantee long-term economic recovery.

Most central banks have moved away from their most dovish positioning of 2020, acknowledging the improving path of economies compared with a year ago. Some, such as the Reserve Bank of New Zealand and Bank of Canada, have taken significant steps toward unwinding stimulus in response to local inflation and growth indicators. But most remain committed to maintaining asset-purchase programmes and ultra-low rates until inflation is clearly sustained.

US Federal Reserve (Fed) chair, Jerome Powell, caused something of a stir in global markets late in 2020 when he suggested that inflation could be allowed to run beyond the Fed’s target levels in the aftermath of COVID-19 to ensure economic recovery was in full swing before beginning a tightening cycle.

This sentiment, in more or less explicit terms, has become consistent across central banks in most major economies and has stayed in place even as inflation data has printed consistently strong results in recent months.

INFLECTION POINTS

Inflation speculation has made 2021 a busier year for traders in the asset class than any in recent memory. Winkworth says dialogue with investors on inflation is greater than at any point in the last decade and that demand has been spread across jurisdictions. He adds, though, that the cohort of investors buying inflation protection has not changed – it is just that interest from these investors has increased. This seems to match the market pattern in Australia to date.

A range of demand themes is playing out across markets. Winkworth says demand for TIPS has been fairly strong at all points of the curve. Real-money investors are the main supporters at the long end while hedge funds are more active in shorter-dated bonds, he adds.

Sam tells KangaNews that, so far in 2021, TIPS have returned around 4 per cent – a much better result than nominal US Treasuries and a result that is reflected in most major economies. He adds that a record level of inflows to TIPS occurred in the last week of July. Meanwhile, Goldberg says broad-based pickup in demand from investment funds and exchange-traded funds suggests investors are allocating more of their portfolios to inflation-protections strategies.

In the UK, the inflation-linked Gilt market has been beset by technical factors that are influencing the short and long ends of the curve. Winkworth explains that front-end pressure already existed due to concerns about labour shortages and supply-chain issues caused by Brexit. COVID-19 has accentuated this. Meanwhile, a reformulation of the inflation index in the UK initially lowered the long end.

Nonetheless, demand has been strong. In March, a UK Debt Management Office (UKDMO) auction of August 2031 index-linked Gilts attracted a record bid-to-cover ratio of 3.5 per cent. Other auctions have attracted bid-to-cover ratios of 2.4-2.8 per cent. European inflation pressures are not as evident as in the US and UK, though the emergence of increased liability hedging has still been evident in euro IIBs.

SUPPLY COMPLICATIONS

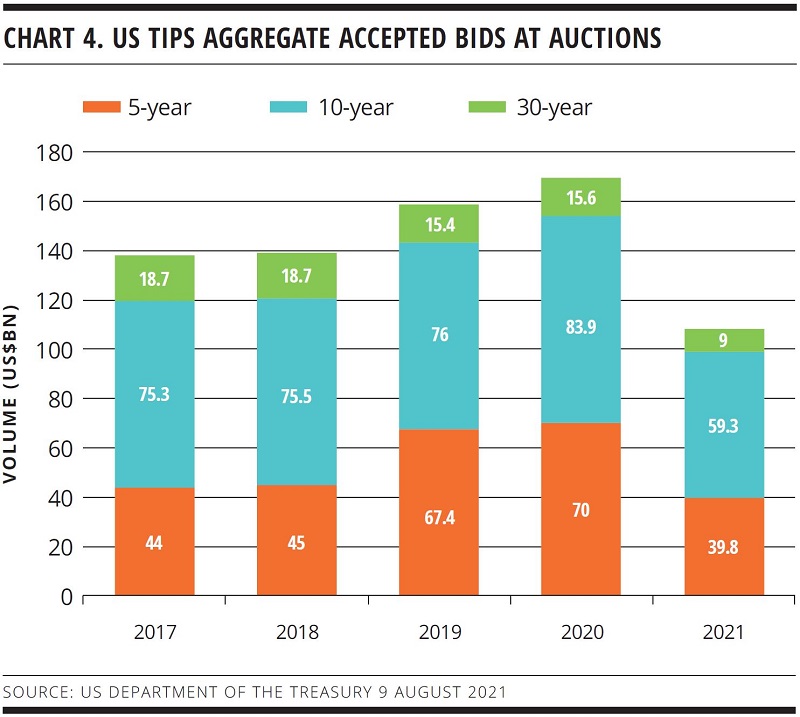

With most governments still pumping fiscal stimulus into their economies to aid COVID-19 recovery, it might be expected that sovereign borrowing authorities would meet the heightened demand for IIBs with increased issuance in this format.

This has been the case in the US, where Treasury has been gradually increasing its TIPS auctions, citing stronger demand for the product (see chart 4). The increase is clearest in the US Treasury’s five-year TIPS auctions, of which it has held two so far in 2021 and accepted greater volume in each than in any other auction since at least 2017.

Goldberg says this is likely to continue even once nominal issuance is pared back, expected to be from November. He adds that greater TIPS issuance is possible partly because of the Fed’s asset-purchase programme, which has included larger purchases of TIPS than nominal bonds and resulted in negative net TIPS issuance in 2020 and 2021.

Elsewhere, the supply picture is not as clear. The UK has most outstanding IIBs as a proportion of total sovereign debt among developed economies, at just less than 24 per cent as of 31 March 2021. However, the UKDMO’s predilection for linkers in the past may give it pause for thought on increased supply now.

Winkworth explains that the UKDMO is cautious on increasing the supply of inflation-linked gilts due to concerns of over-exposure to a rising inflation environment. He adds that index reform has contributed to the hesitation to supply more index-linked Gilts, at least until the process is complete.

Meanwhile, in Europe Winkworth says sovereign borrowers have not been in a rush to commit to more IIB issuance but could do so when new funding requirements are announced for 2022.

The key balancing act for sovereigns is the temptation to ease debt burdens by ‘inflating away’ debt – which is possible with nominal bonds but not IIBs – versus satisfying growing demand for linkers and the need to retain credibility. Sovereigns that are clearly seeking to let inflation do their heavy lifting for them are unlikely to gain much support from global investors.

The UKDMO’s hesitation to increase its supply of index-linked Gilts highlights the dilemma, though its current level of outstanding linkers is much higher than peers and thus suggests its challenges may be idiosyncratic.

Winkworth says while an effective cap on incremental IIB issuance is plausible, it is unlikely to be among the priorities of governments in the wake of the COVID-19 crisis. Instead, he refers to the purpose of IIBs at their inception in the 1980s and 1990s – as a tool for governments to reinforce and give confidence around their inflation targeting – as a reason for governments to continue issuing them.

“We are now are in a holding phase, as short-term inflation outcomes peak and we wait to see whether or not inflation is structural and passes through to wages as the base effects tail off.”

The path of demand and supply dynamics in IIB markets will be determined primarily by ongoing evidence of inflation or lack thereof. CPI and other leading inflation indicators have continued to print emphatically in favour of greater inflation since April, but investors appear yet to be fully convinced.

Winkworth says the biggest question in IIB markets is what data breaks either the bulls or the bears out of their holding pattern – and when. Economic sentiment is showing signs of having already peaked.

BofA’s July investor survey shows lower growth and profit expectation following peaks in the June survey.

Sam explains that the spread of the delta COVID-19 variant in developed economies has added uncertainty to the global growth outlook. Combined with weaker risk appetite in markets, it means breakeven inflation may struggle to push higher in the near term. Significantly, however, breakeven levels have not collapsed despite nominal yields rallying aggressively since June.

Sam tells KangaNews the majority of investors are still siding with central banks in their inflation assessments. BofA’s July investor survey shows 70 per cent of respondents viewing inflation as transitory despite it also being viewed as the greatest risk.

This weighting of expectations could lead to a further acceleration of linker demand if data begin to show evidence of sustained inflation. “There is scope for investors to be surprised if inflation proves to be more sustained, so there is potentially a second chapter to this inflation story that could support ongoing demand,” Sam says.

Should the opposite transpire, and inflation proves to be transitory, Sam says the concentration of demand for TIPS in the short end could leave investors vulnerable.

Goldberg expects CPI prints over the next several months to be telling. “Investors overall remain somewhat cautious about adding more inflation-hedging bets, but enough are seeking inflation protection to keep TIPS breakevens elevated. If CPI starts to cool it could suggest the transitory inflation story is correct. However, the market is on a hair trigger and could move very quickly if the outlook shifts dramatically.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news