Australian inflation market paints a complex picture

Inflation signs are emerging faster and more frequently in other global jurisdictions, but there is enough inflation smoke in Australia for market users to be contemplating the fire. When it comes to inflation-linked bond issuance, local experts say the market story is not as simple as more interest equating directly to demand for, or supply of, physical product.

Laurence Davison Head of Content and Editor KANGANEWS

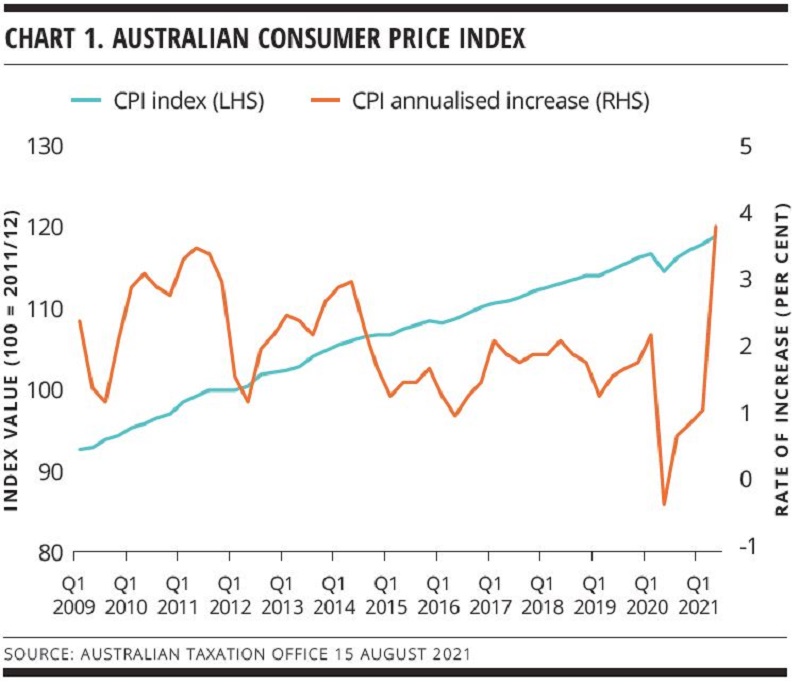

Australia’s consumer price index (CPI) print for Q2 2021 did not take anyone by surprise but was still notable. Annualised inflation leaped to 3.8 per cent, its first time as high as 3 per cent since the end of 2011 (see chart 1). Having barely dented the bottom end of the Reserve Bank of Australia (RBA)’s 2-3 per cent target for the past seven years, the print roared straight through the band and into territory that would, if sustained, likely put significant pressure on the RBA to revise its lower-for-longer rates outlook.

It is too early to say, however, that Australia is in the early stages of an inflation breakout. At least some of the CPI spike undoubtedly comes from a base effect driven by an economy reopening after the pandemic lockdowns of 2020. The global inflation debate, meanwhile, is also far from settled.

A reckoning on whether price rises from the first half of 2021 will be protracted has likely been delayed by new lockdowns that have affected more than half the population of Australia, including its three largest cities. Whether the latest COVID-19 catastrophe that originated in New South Wales (NSW) stalls CPI once more will only start to be known in the Q3 2021 print. Even then, a solid body of opinion suggests an inflation breakout is not the most likely outcome (see box).

Nonetheless, there are reasons to think inflation protection will become a livelier corner of the Australian fixed-income market. The very existence of differing views on the inflation outlook should mean a more vibrant sector. The base case for most market participants is clearly growing concern about the potential for higher inflation.

“We are far from alone in being concerned that we are seeing very, very strong inflation signals,” says Tamar Hamlyn, Sydney-based portfolio manager, interest rate strategies and macroeconomics at Ardea Investment Management. “They are much more than green shoots – they are more like green trees of inflation. The fact that they are occurring quite rapidly, associated with the reopening of the global economy, is quite concerning.”

Market participants say interest in inflation protection as an asset class has already grown. Andrew Barrelle, founding partner, fixed income trading at Barrenjoey Capital in Sydney, tells KangaNews: “There are more conversations about inflation and inflation-risk hedging taking place now than there have been for quite a while – and it is a local and global topic. It stems from the combination of extraordinarily low rates, QE and fiscal stimulus all happening at the same time.”

Meanwhile, a subtle change of approach flagged by the RBA and other central banks could have a significant impact on the range of possible inflation outcomes – and thus the volatility and appeal of inflation protection.

In the minutes of its March 2021 monetary-policy meeting, the RBA noted that it is now seeking wages growth to be “sustainably” greater than 3 per cent before it considers hiking the cash rate. The significance of an emphasis on wages rather than CPI is that it reweights policy response to a lagging indicator.

Barrelle explains: “The RBA is no longer trying to be ahead of the curve by moving rates in response to higher forecast inflation. Instead, it is deliberately waiting for actual inflation to be realised before responding. The value of the breakeven and the inflation-risk premium should both increase if inflation is able to move higher than it previously would have before triggering a rates response. The change in central-bank approach allows for more volatility and upside in the inflation outlook.”

Australian inflation outlook: transition thing

Even if the aftermath of Australia’s latest round of COVID-19 lockdowns is the same as the last one – a relatively rapid economic recovery – an accompanying inflation outbreak is far from the consensus expectation.

The sting in the pandemic’s tail in Australia has doused near-term economic optimism. For instance, Commonwealth Bank of Australia’s economics team has pushed back its expectation for the first Reserve Bank of Australia (RBA) rate hike to May 2023 from November 2022, based on the impact of the latest wave of lockdowns.

A CBA research note says: “Domestic financial-market participants are presently firmly focused on the unfolding COVID-19 situation in NSW [New South Wales] and how it will [affect] the near-term economic outlook. This fixation is completely justified. The economic impacts from the lockdown will be very significant in the near term and the economic data over coming months will deteriorate.”

Many analysts argue that consumer price index (CPI) data were not pointing to a protracted spike in inflation even before the latest COVID-19 outbreak. Core inflation was just 1.65 per cent at the Q2 print, up from 1.2 per cent three months previously but still comfortably below the RBA’s target band despite the base effect of 2020’s anomalous prints.

We are at something of a transition point at the moment, where we have seen some of the early signs of inflation but we have not yet seen enough to deliver sustained, elevated inflation at the upper end of the RBA target or perhaps even above it.

MARKET CONDITIONS

This should be fertile ground for a jump in demand for inflation protection and therefore for inflation-linked bonds – which in Australia means Treasury-indexed bonds (TIBs) issued by the Australian Office of Financial Management (AOFM). Barrelle predicts such demand will emerge. However, he also acknowledges that the change in central-bank strategy is taking some time to filter through to market consciousness and behaviour.

For now, the Australian linker market remains in something of a business-as-usual phase. Market participants report relatively consistent turnover and liquidity, based on issuance volume that has remained stable or even fallen.

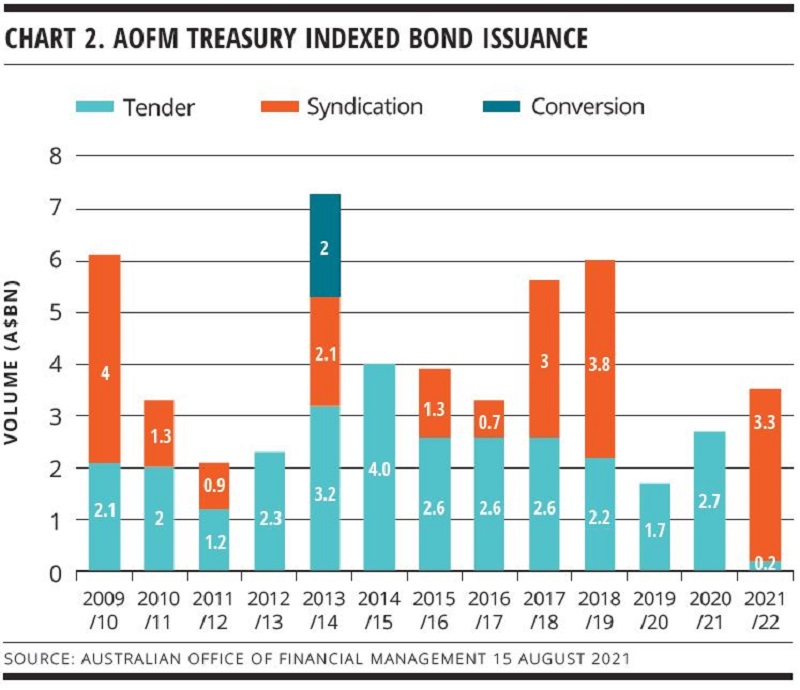

The AOFM has not syndicated a new TIB since September 2018. However, it committed to syndicating a new 2032 bond in 2021/22, eventually pricing A$3.25 billion in August 2021. Its tender issuance actually fell in 2019/20 before returning to something like its long-run average in 2020/21 (see chart 2). The AOFM plans to tender A$2-2.5 billion (US$1.5-1.8 billion) of TIBs in 2021/22, compared with forecast Treasury bond issuance of A$130 billion.

There is no obvious trend in demand to be found in coverage ratios. AOFM TIB tenders have typically been covered by 3-5 times since the agency returned to issuance in this format in 2009.

All this adds up to insufficient evidence to convince the AOFM to step up its supply of new TIBs at this stage. Rob Nicholl, the AOFM’s Canberra-based chief executive, tells KangaNews: “We have not experienced any significant change in demand to date – we have had pretty consistent outcomes for the past year or so. The core of our inflation market is domestic and we see our role very much as supporting the market through issuance and new maturities. This group of investors does not typically change quickly and has not done so of late.”

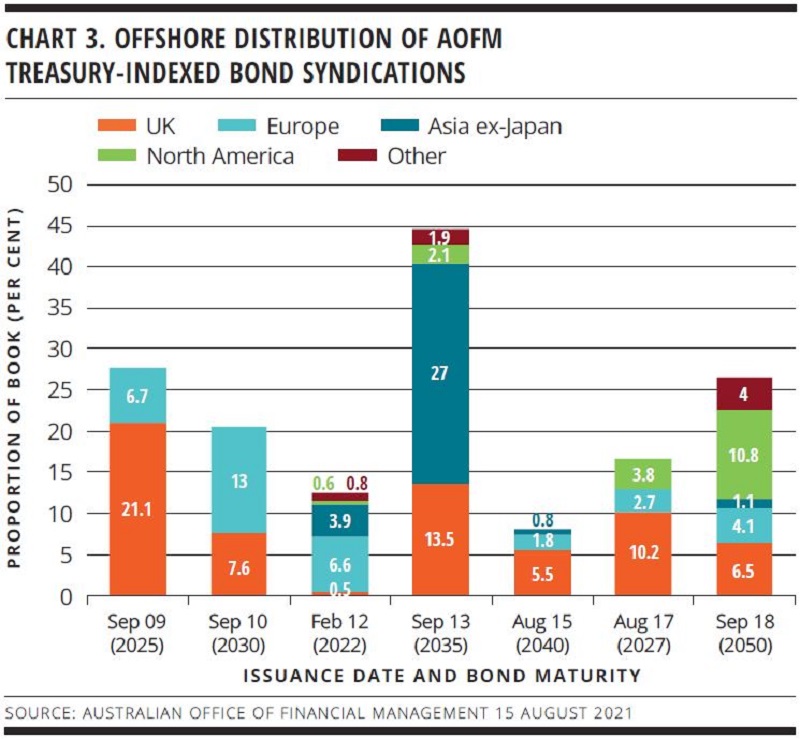

The source of demand is borne out by TIB syndication outcomes. Domestic investors took the majority of all six AOFM syndications conducted since 2009, often the overwhelming majority. The source of what overseas demand has come through has fluctuated significantly between deals (see chart 3).

The AOFM is cautious about responding to near-term demand spikes. Nicholl says: “We have scaled issuance volume to support the market at what we view as its consistent level of demand. We would always be hesitant to change our issuance in response to offshore demand signals alone – because this bid is more likely to be opportunistic, and it also has the potential to come back in volume. The consequences of a market swamped by paper coming back from offshore could be problematic.”

In particular, Nicholl continues, the AOFM would want to be confident that an increase in demand represents a structural shift before committing to greater supply. This would likely have to include a substantial domestic component.

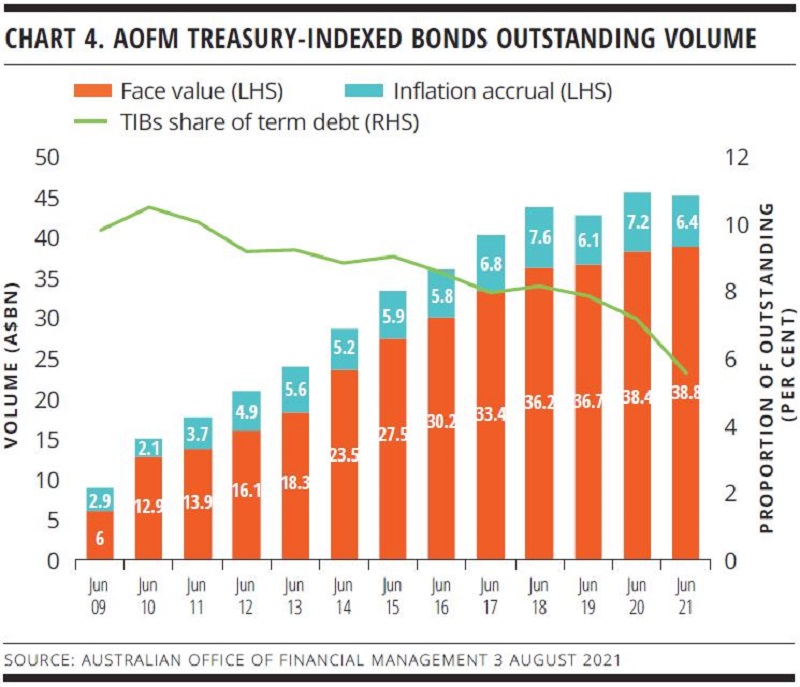

With no growth in TIB issuance, the contribution linkers make to the AOFM’s overall issuance has actually fallen. After a jumbo year for nominal issuance, TIBs represented less than 5 per cent of total Australian Commonwealth government bonds on issue by the end of the 2020/21 financial year (see chart 4).

SUPPLY CONSIDERATIONS

Increasing the relative contribution of TIBs to the overall funding task could have wider consequences for the AOFM’s cost of funds, too. The inflation component of this type of issuance adds a contingent liability to the AOFM’s balance sheet. It benefits if inflation undershoots the breakeven level, but an inflation breakout could have a significant negative impact on debt-servicing cost.

Barrelle points out that the AOFM has paid a lower cost of funds than it otherwise would have since it returned to TIB issuance in 2009. Persistent inflation undershoots mean the issuer’s funding cost in inflation-linked borrowing has been less than in equivalent-tenor nominal bonds.

This may be a moot point, however. At the very least, the AOFM likely has sufficient headroom that it would be able substantially to increase its linker issuance without incurring a dramatic cost impact even in the event of a significant and protracted uplift in inflation.

Nicholl tells KangaNews: “We absolutely think about the potential impact of increased use of linkers on our overall cost of funds. But this has to be viewed in the context of the scale of our issuance. We don’t have a precise view on where the impact could become meaningful, but whether it is 10 per cent or 20 per cent of overall issuance it is clear that we are not even in the neighbourhood at the moment.”

Based on the position at the end of 2020/21, the AOFM could issue approximately A$35 billion in face value of new TIBs before the proportion of its outstanding issuance in this format reached 10 per cent – even if it stopped issuing nominal bonds entirely while it completed this accumulation. As things stand, it seems highly unlikely that TIBs will even comprise 10 per cent of new issuance, so reaching a point of concern is likely not on the cards at this stage.

“Last year we issued A$2.5 billion of linkers out of total bond issuance of A$210 billion. Capacity to increase linker supply is clearly substantial. As things stand, these instruments really aren’t contributing to our overall funding task in a meaningful sense. This highlights our focus on supporting the market,” Nicholl adds.

Equally, it seems unlikely that the AOFM would seek to back away from the inflation-linked market even in the event of significantly higher inflation. Nicholl emphasises that the reason the sovereign issuer is not likely immediately to respond to near-term demand growth with substantially increased supply – its desire to provide a consistent and reliable approach through the cycle – also gives it sufficient reason to maintain issuance even during periods when TIBs are not the most cost-effective option.

This is likely the appropriate choice for a responsible sovereign issuer. Maintaining at least some inflation-linked exposure sends a signal to the market that a sovereign borrower is not turning a blind eye to inflation. Taking an extreme case, if any sovereign decided not to issue linkers at all while inflation was increasing, it could suggest a willingness to inflate away debt. This would likely have a negative impact on nominal-bond pricing.

COMPLEX OUTLOOK

The linker demand story is also not as simple as a straight line from expectations of higher inflation to desire for more TIBs. Inflation-linked bonds offer ‘perfect’ inflation protection in the sense that the future coupon and principal flows the bonds provide are 100 per cent immunised against future changes in CPI. The problem is that – like any other long-term fixed-income instrument – the underlying coupon rate is fixed.

An investor buying an inflation-linked bond with real yield of 5 per cent is fixing an after-inflation rate of return that is locked at 5 per cent throughout the life of the bond. Real yield is of course currently close to an all-time low, and if inflation did break out rates would inevitably increase. This would potentially wipe out any gains investors made on the inflation component of TIB exposures.

The core investor base for TIBs – buyers from the insurance sector, for instance – has specific motivations for ongoing interest in the product. Marginal demand growth will depend on a more complex matrix incorporating breakeven relative value and, for some investors, outright opportunism.

Even investors with longstanding engagement with the asset class say it is not a simple solution to inflation risk. “We have always viewed inflation-linked bonds as fantastic building blocks. But they are not necessarily something we would want to have 100 per cent of a portfolio allocated to on a set-and-forget basis,” Hamlyn reveals.

Even so – and also notwithstanding the sovereign’s capacity to add supply – it is possible that a more widespread awakening of the Australian dollar investment base to the possibility of revived inflation could run ahead of the AOFM’s willingness to increase TIB issuance.

Hamlyn says: “If all the investors that own Australian fixed income decided tomorrow that they wanted to take even a neutral view on inflation – by moving to 50 per cent linkers and 50 per cent nominal bonds – there are not enough inflation-linked bonds on issue to meet the demand. This is unlikely, but given the increasing likelihood of an inflation breakout there are scenarios in which there is high demand for a scarce supply of inflation-linked bonds.”

The most likely outcome, Hamlyn argues, is a more vibrant inflation market across maturity points and products. He believes demand for inflation protection is coming and that breakeven inflation will therefore be priced higher – but probably differently across the curve and very differently among instruments. During episodes of dislocation, he adds, Ardea has already seen significant variation in the pricing of breakeven on physical inflation bonds versus inflation swaps.

“We actually see this as positive because a lot of our ability to add alpha comes from market dislocation, mispricing and asymmetries,” Hamlyn reveals. “Whenever there are large shifts in expectations, which includes inflation, they tend to create significant instrument pricing differences. This is something we continue to observe. Based on changes in inflation expectations over the past year, it will continue to be a factor.”

HIGH-GRADE ISSUERS YEARBOOK 2023

The ultimate guide to Australian and New Zealand government-sector borrowers.

Related news