New Zealand securitisation starts to deliver on potential

Fulfilling the promise hinted at in 2019 but put on hold while the local lending market worked its way through the consequences of the pandemic, 2021 is now officially a record issuance year in the New Zealand securitisation market. Total year-to-date-issuance, of NZ$1.5 billion (US$1 billion), has ticked past the previous record and market participants are confident deal flow will continue despite the latest COVID-19 lockdown.

Kathryn Lee Staff Writer KANGANEWS

The securitisation asset class has long sought sustained traction in New Zealand. Improved appetite for the asset class – driven at least in part by an ongoing shortage of credit-asset supply – leads market participants to believe the tide could be changing.

Indeed, where the emergence of the pandemic in 2020 was sufficient to scupper an optimistic outlook for the asset class at the start of the year, the early signs are that deal flow may be able to continue despite the re-emergence of COVID-19 shortly after the latest trio of completed deals.

The clearest sign of a more robust market came on 30 August, when Resimac announced plans to return to the New Zealand residential mortgage-backed securities market despite the country having re-entered lockdown and case numbers continuing to accumulate.

RESUMED FLOW

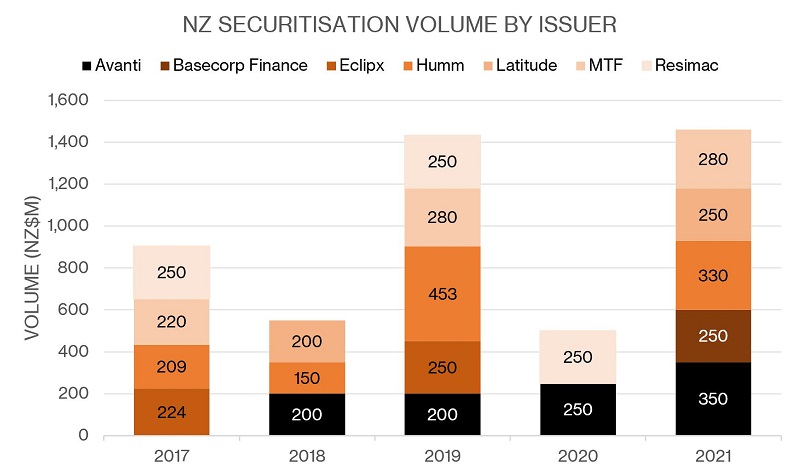

Already preceded by healthy supply in the first two quarters of the year – which included a debut deal from Basecorp Finance and market returns from humm and MTF – August proved a bumper month for New Zealand securitisation issuance with three trades going to market. The current year now marks a record for issuance volume in New Zealand (see chart), and with indication of regular issuance from key players these levels may be here to stay.

Humm kicked off the month with a NZ$240 million asset-backed securities (ABS) deal from its Q Card Trust programme – having already refinanced NZ$89.5 million in April.

Bianca Spata, the issuer’s Sydney-based group treasurer, says that while humm’s April transaction marked an important return to the New Zealand market, the size of its latest deal makes it even more meaningful. “It was quite a large transaction for the programme, representing more than a third of outstanding notes, and it was an opportunity for us really to test appetite following COVID-19,” she tells KangaNews.

Avanti followed, pricing a NZ$350 million residential mortgage-backed securities (RMBS) deal on 11 August. The issuer’s biggest deal to date, and the largest securitisation deal seen in New Zealand, Avanti has now printed a total of NZ$1 billion in funding through the asset class and aims to do more.

Source: KangaNews 1 September 2021

The third New Zealand securitisation in quick succession came from Latitude, with a NZ$250 million credit-card ABS transaction. Its first return to the New Zealand market since 2018, Eva Zileli, Latitude’s Melbourne-based treasurer, says it was a very good result, especially considering the preceding deal flow.

Originally launched with indicative deal size of NZ$200 million, it was Latitude’s upsize that tipped New Zealand securitisation into a new record year.

REGULAR ISSUERS

All three recent issuers say they plan to maintain a regular issuance pattern. Paul Jamieson, group treasurer at Avanti Finance in Auckland, says the issuer’s funding need is increasing and it is keen to take advantage of greater capacity in New Zealand dollar securitisation. “Our business is growing and our issuance will grow over time,” he confirms. “We need to decide whether we want to continue as an annual issuer with bigger deals or if we would rather print more frequently throughout the year.” he says.

Avanti also plans to begin nonmortgage ABS issuance, though Jamieson says this is a little down the road. A slowdown in auto-loan origination due to supply restraints has slowed progress. “We want to make sure our pipeline is strong and that we will be able to return to the market on a regular basis,” Jamieson explains.

The nature of Humm’s programme meant it was affected by reduced spending at the beginning of the pandemic, which influenced time to market. Latitude, which launched its inaugural trade in 2018, had initially planned to return earlier but timing was also influenced by the pandemic.

“Latitude hopes to be a regular issuer in the New Zealand market and we don’t plan to wait another three years before going back,” Zileli tells KangaNews. “The success of this trade gives us more confidence to perhaps go back next year. We issue every year in Australia and we want to build to that sort of cadence in New Zealand as well.”

INVESTOR BASE KEEN AND GROWING

KangaNews understands all the deals saw strong support and were roughly twice oversubscribed, with more than a dozen investors participating across the three. Deal information provided by Commonwealth Bank indicates that Latitude attracted a final orderbook of NZ$364 million across its tranches, allowing for a NZ$50 million upsize to the final deal volume of NZ$250 million.

Offshore demand continues to be a significant component of New Zealand deals: international investors took at least one-third and as much as two-thirds of each of the recent transactions.

All deals were dominated by real-money investors. The Avanti deal was all real money, primarily fund managers, while humm’s transaction was evenly split between real money and bank balance sheets. Latitude was 70 per cent real money and 30 per cent bank balance sheet.

Local market sources say emerging local investor support is a testament to ongoing market development, perhaps most notably growth in the domestic institutional funds base including through KiwiSaver. As KiwiSaver has grown in size it has supported increased analytical resources in the institutional-investor sector. This in turn has allowed the buy side to engage with a wider range of fixed income securities including securitisation.

New investors from the local market have come into securitisation transactions in 2020 and 2021, deal sources say. Existing investors have also increased ticket sizes, suggesting they are becoming more comfortable with securitisation as an asset class.

MARKET CAPACITY

As in Australia, New Zealand securitisation has benefited from a lack of other credit issuance. While only time will tell whether the current level of demand can be maintained once banks return to a more regular issuance pattern, market participants are confident enough groundwork has been laid to continue growing the asset class over the long term.

“I think securitisation offers a good diversity play for investors in New Zealand,” Jamieson tells KangaNews. “It offers an opportunity for yield pickup, especially in the lower-rated notes.”

Jamieson adds that the growth in KiwiSaver funds could support the market toward a positive period over the next few years. “Some of these funds are starting to diversify into the securitisation space and I see this expanding over time. Existing investors continue to support the market and there are new offshore investors coming into the market as well, all of which bodes well for the future.”

There are some grounds for scepticism, however. Spata agrees it is a positive time for the market but says continuing to maintain momentum is critical. “We have seen a good rebound in New Zealand over the past six months or so. Although there were a number of issuers in market at the same time as ourselves, we saw good support for our trade across our senior investor base which enabled us to execute a small upsize.”

She adds: “The market is going well and it’s great to see deal flow from different issuers. I think the key will be trying to retain this traction and to continue to see issuers and the industry invest time in building out the investor base in support of the market as a whole.”