Australasian sustainable debt: fertile ground awaiting growth

Information on deal flow drawn from the KangaNews transaction database suggests the Australian and New Zealand sustainable-debt markets are still very much in an evolutionary phase. Product innovation continues to come thick and fast but sustainability-themed supply is only providing a fraction of total market activity.

Laurence Davison Head of Content and Editor KANGANEWS

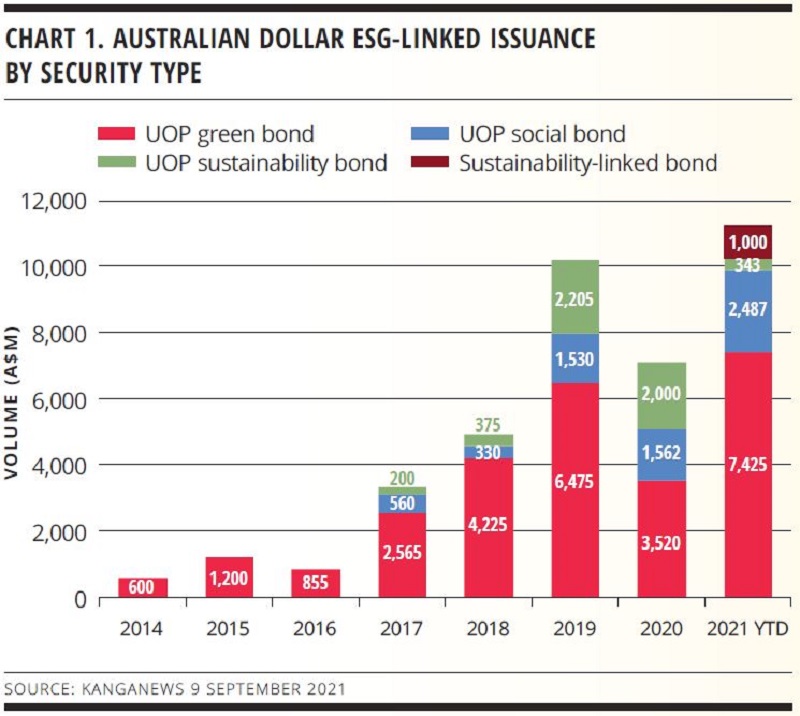

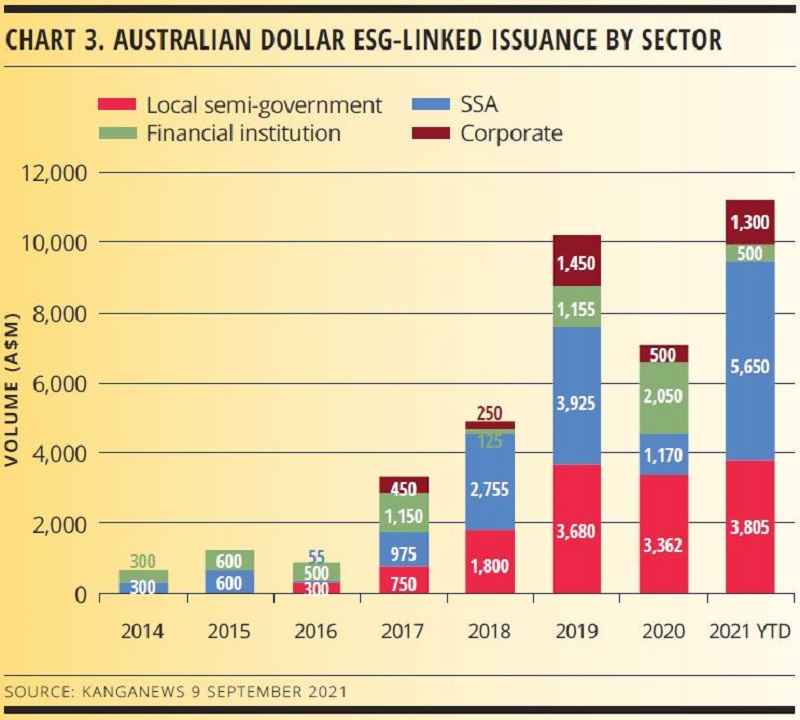

Aggregate issuance of bonds in line with environmental, social and governance (ESG) standards – comprising use-of-proceeds (UOP) green, social and sustainability (GSS) bonds, and now KPI-based sustainability-linked bonds (SLBs) – is now an established part of the Australian and New Zealand debt markets (see charts 1 and 2). However, outright volume of issuance has grown rather than exploded in both jurisdictions.

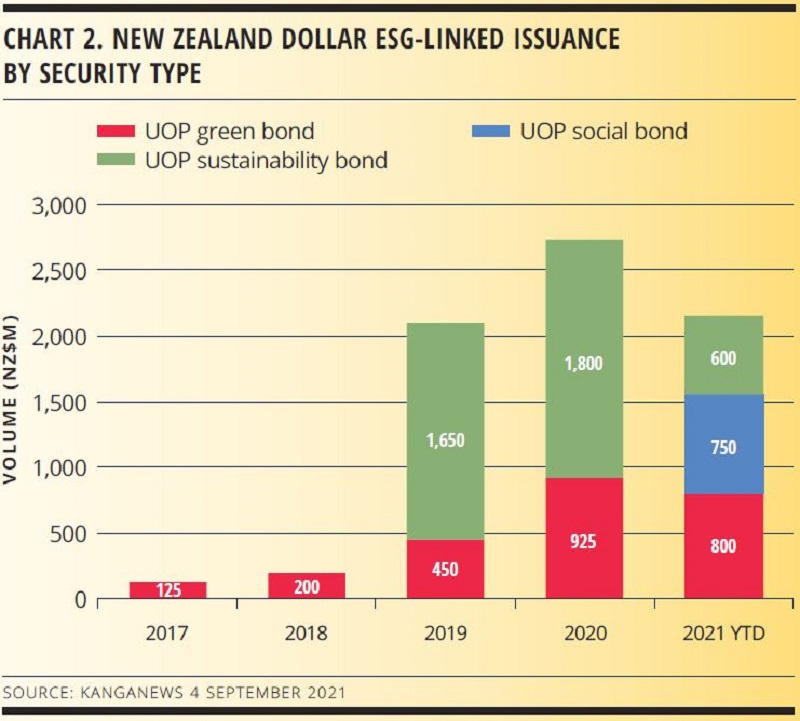

The first two-thirds of 2021 have only been somewhat productive for Australian domestic issuers. While total volume of ESG-themed issuance in 2021 by early September – of A$11.3 billion (US$8.3 billion) – was already greater than the full-year total from 2020, almost exactly half this year’s supply came from international issuers (see chart 3).

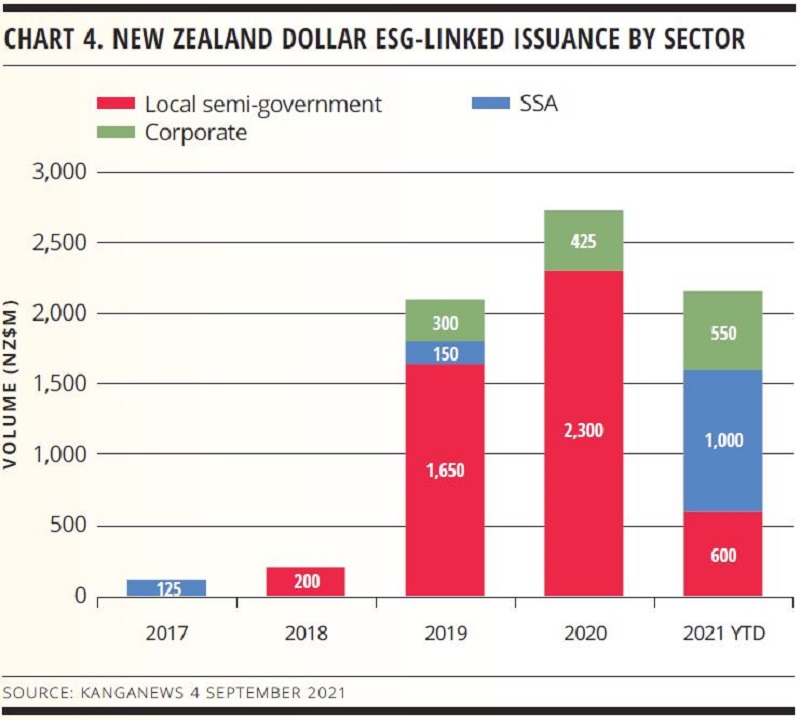

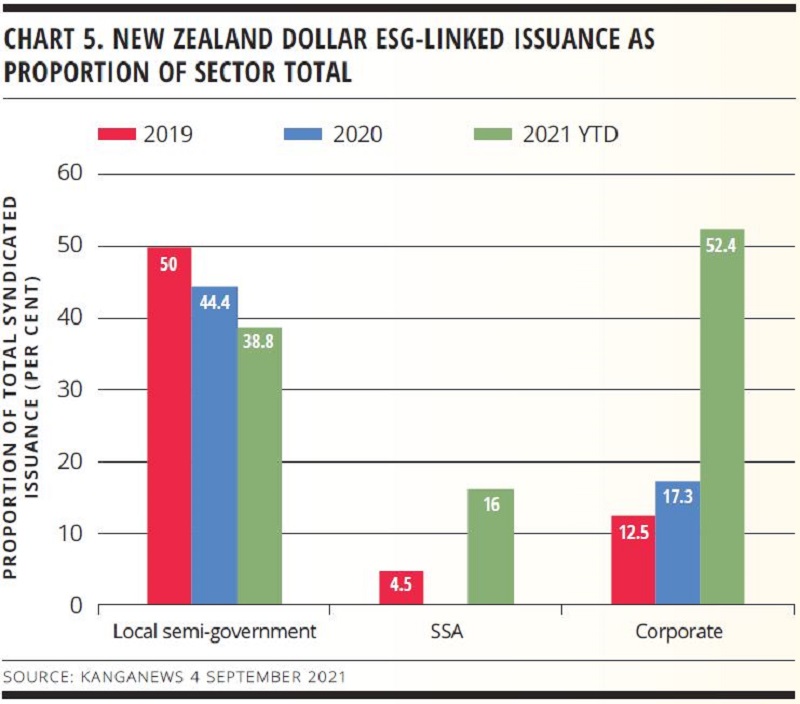

The New Zealand sustainable-debt market, while smaller, has built its foundations on domestic issuance. Indeed, it is only in 2021 that global supranational, sovereign and agency (SSA) issuers have found consistent opportunities to print Kauri deals using their GSS programmes (see chart 4).

The mainstay of the New Zealand market has been the local semi-government sector. Two of the three key local issuers in this space, Auckland Council and Kāinga Ora – Homes and Communities, print effectively all their own-name debt in green or sustainability format. New Zealand Local Government Funding Agency, the third mainstay of New Zealand’s semi-government market, has yet to issue GSS bonds but is exploring its options in the space.

Corporate issuers from New Zealand, meanwhile, have arguably been quicker to adopt GSS issuance as a funding mainstay than their Australian peers. While aggregate annual volume of corporate ESG issuance in New Zealand has never been more than the NZ$550 million (US$385.4 million) printed in 2021 to early September, this has to be viewed in the context of a smaller domestic corporate bond market.

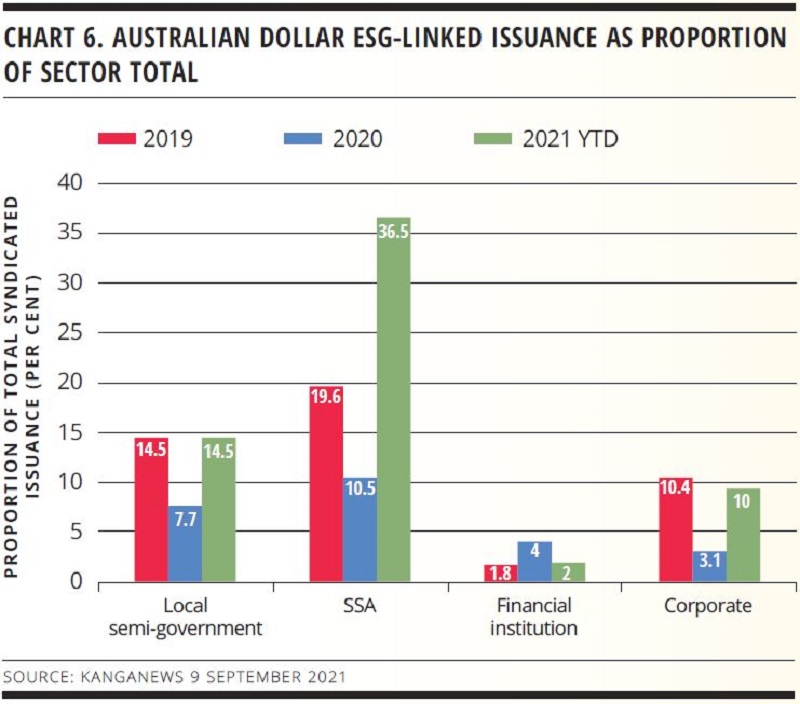

So far this year, more than half of all corporate bond issuance priced in New Zealand has been in GSS format (see chart 5) and two of five biggest issuers in the market are corporate names (see table 1). Just 10 per cent of Australian corporate bond issuance in 2021 has been ESG-themed (see chart 6), the large majority coming in a single transaction: Wesfarmers’ A$1 billion SLB, the first issuance of this type on either side of the Tasman Sea. Only one of Australia’s top-10 ESG issuers is a corporate name (see table 2).

Perhaps the most notable gap in the Australian and New Zealand ESG bond issuance space is financial-institution (FI) supply. Such deal flow forms only a tiny proportion of the overall FI market in Australia, and no bank has yet issued a GSS bond in New Zealand dollars – though both countries’ banking complexes have provided some euro-denominated flow. The near-absence of the big-four banks from both countries’ wholesale bond issuance since early 2020 perhaps explains the lack of momentum, though the first new domestic senior deal from an Australian major bank to price in 2021 was not in labelled format.

Table 1. Top five ESG-themed issuers in New Zealand dollars by syndicated volume

| Issuer | Volume (NZ$m) | Number of deals | Lines outstanding | First issue date | Most recent issue date | Format(s) issued |

|---|---|---|---|---|---|---|

| Kāinga Ora – Homes and Communities | 3,900 | 7 | 6 | 28 Mar 19 | 20 Apr 21 | UOP sustainability |

| Auckland Council | 850 | 3 | 3 | 21 Jun 18 | 16 Sep 20 | UOP green |

| Asian Development Bank | 750 | 1 | 1 | 27 Jul 21 | 27 Jul 21 | UOP social |

| Mercury | 550 | 4 | 3 | 4 Sep 20 | 14 Apr 21 | UOP green |

| Argosy Property Group | 325 | 3 | 3 | 6 Mar 19 | 16 Oct 20 | UOP green |

Source: KangaNews 4 September 2021

Table 1. Top 10 ESG-themed issuers in Australian dollars by syndicated volume

| Issuer | Volume (NZ$m) | Number of deals | Lines outstanding | First issue date | Most recent issue date | Format(s) issued |

|---|---|---|---|---|---|---|

| Queensland Treasury Corporation | 6,500 | 4 | 4 | 15 Mar 17 | 9 Sep 21 | UOP green |

| European Investment Bank | 5,425 | 17 | 6 | 25 Jul 17 | 25 Mar 21 | UOP green, UOP sustainability |

| New South Wales Treasury Corporation | 4,900 | 3 | 3 | 9 Nov 18 | 20 Oct 20 | UOP green, UOP sustainability |

| KfW Bankengruppe | 2,650 | 7 | 1 | 26 Mar 15 | 28 Jul 21 | UOP green |

| National Housing Finance and Investment Corporation | 1,997 | 5 | 3 | 21 Mar 19 | 9 Jun 21 | UOP social, UOP sustainability |

| ANZ Banking Group | 1,850 | 2 | 1 | 27 May 15 | 19 Aug 20 | UOP sustainability |

| International Finance Corporation | 1,700 | 18 | 2 | 6 Mar 18 | 21 May 21 | UOP social |

| Asian Development Bank | 1,330 | 4 | 2 | 8 Jan 19 | 22 Jan 20 | UOP green |

| Wesfarmers | 1,000 | 1 | 1 | 16 Jun 21 | 16 Jun 21 | SLB |

| Oversea-Chinese Banking Corporation Sydney Branch | 1,000 | 2 | 2 | 26 Nov 19 | 12 Aug 21 | UOP green |

Source: KangaNews 9 September 2021

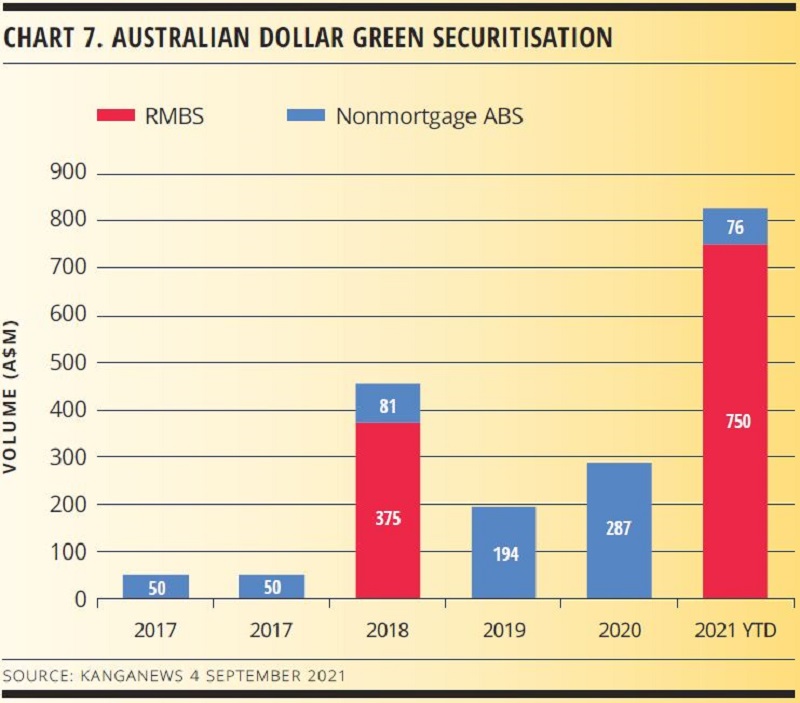

Australian dollar sustainable issuance is boosted to some extent by the emergence of green securitisation (see chart 7). Volume has been limited to date – indeed, Firstmac’s privately placed A$750 million green residential mortgage-backed securities deal priced in July this year represents more than a third of total all-time volume. But there has been a reasonably consistent supply of green nonmortgage asset-backed securities issuance and market participants are hopeful the asset class will grow as suitable loans accumulate on issuers’ books.

The challenge in the securitisation sector is largely on the asset side. A clutch of Australian lenders offer green-labelled mortgage products but their application is limited – in many cases, only new-build home buyers can even think of qualifying for this type of financing. Work is being done on data capture for a wider range of homes, but it is taking time. Nonmortgage issuance capacity is limited by the volume of loans taken on qualifying assets such as home solar systems and electric vehicles.

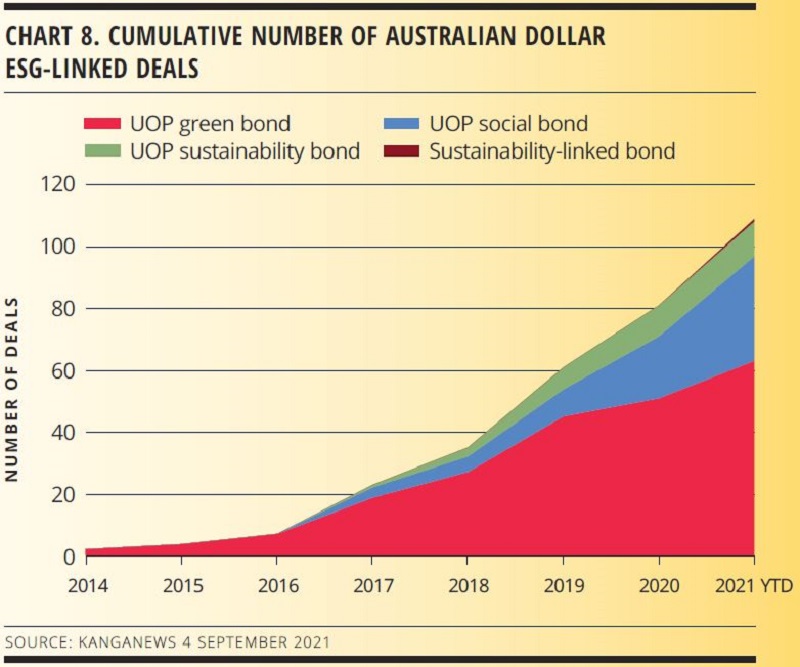

Perhaps the biggest reason for optimism in Australia is the local market’s willingness to engage with new ESG structures. Far from becoming a market that accepts periodic green-bond issuance but lacks diversity of security type, Australia has readily adopted social and sustainability UOP bonds and, most recently, the SLB. There were actually more individual social-bond transactions in 2020 than there were green bonds (see chart 8).

Sustainability-linked loan transactions have proliferated in Australia over the past 12 months and market participants hope the SLB will catch hold in much the same way – albeit possibly with a lag after the first deal, as issuers engage with the asset class and prepare to bring their own transactions.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.