Momentum builds in Asia Pacific sustainable finance

The need to transition economies to more environmentally friendly and socially conscious settings, and for financial markets to facilitate this transition, requires vast amounts of data to assess, measure and compare progress. Refinitiv has been collating environmental, social and governance data on companies around the world since 2002 and shares its findings on the Asia-Pacific region.

Movement in financial markets to act on climate change has come from all corners in 2021. Global issuance of green, social and sustainability (GSS) bonds has continued at record pace, while sustainability-linked bonds (SLBs) have become common in Europe and been issued for the first time elsewhere, including in Australia and Asia.

Meanwhile, regulatory pushes such as the EU Taxonomy for Sustainable Activities and mandatory disclosure regimes, using for example the Taskforce on Climate-related Financial Disclosures (TCFD), are also on the rise.

Together, these are causing clamour among market participants for useful and actionable data. Refinitiv’s environmental, social and governance (ESG) data cover more than 11,000 companies from 76 countries and account for more than 80 per cent of the world’s market capitalisation. It provides more than 500 ESG metrics. It has a scoring mechanism that considers 10 key ESG themes as well as a controversy score. In fixed income, Refinitiv has ESG content coverage on 769,000 bonds, including information on green bonds.

The data can be used to measure how companies and markets compare in their progress building sustainable-finance markets and toward objectives such as the UN Sustainable Development Goals (SDGs).

ASIA-PACIFIC PROGRESS

The Asia-Pacific region has often been considered a laggard in addressing climate change compared with Europe and, to a lesser extent, North America. The emerging-economy status of most of the region is one reason for this, as these markets are typically more reliant on carbon-intensive economic activity. Australia is somewhat of an outlier, being both a developed and carbon-intensive economy.

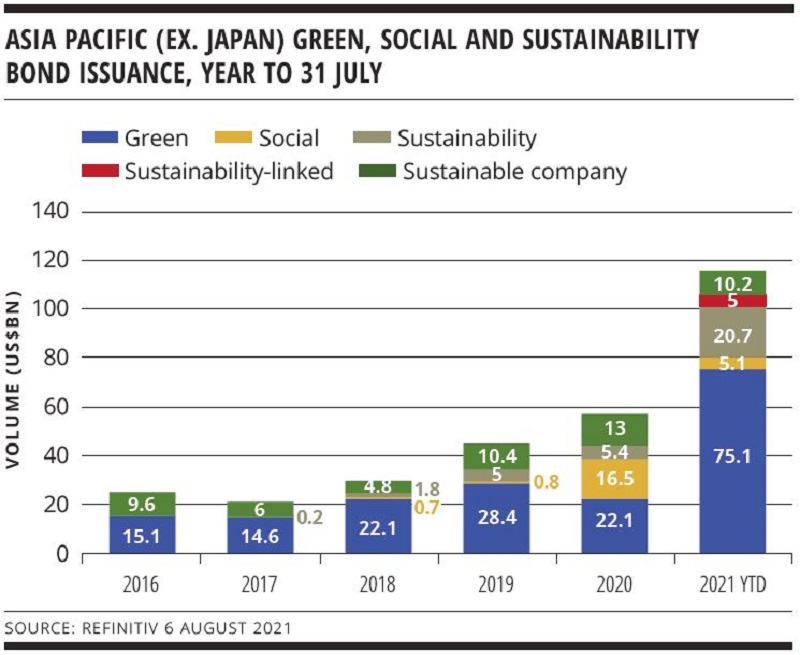

However, Michelle Cameron, account director at Refinitiv in Sydney, says data suggest strong momentum is building in Australian and Asia-Pacific financial markets toward sustainable outcomes. In the year to the end of July, issuance of GSS bonds and SLBs in Asia Pacific is easily at record pace in 2021 by volume and number of transactions (see chart).

Key trends in the Asia-Pacific sustainable-bond market are a large increase in green- and sustainability-bond issuance – up 168 and 280 per cent year-on-year respectively – and the inauguration of the Asian SLB market. To the end of July 2021, US$4.9 billion has been raised across 13 SLB transactions in Asia Pacific.

Cameron says this development is particularly important given the composition of most Asia-Pacific economies. “SLBs enable flexibility with use of proceeds so companies can align their financing with measurable sustainability outcomes and commitments. They are also more useful to smaller companies that are less likely to have the volume of assets required for a green or social bond.”

Asia-Pacific social-bond issuance has waned in 2021, however. Cameron says this is due to the wave of pandemic-relief social bonds printed in the region last year. She adds that it will be interesting to see whether social issuance related to areas such as diversity, inclusion and human rights can regain the momentum built in social bonds during the worst of the pandemic.

Refinitiv data also show increasing engagement with sustainable finance on the part of Asia-Pacific banks. GSS and sustainability-linked lending in 2021 to the end of July had already eclipsed the annual volume record set in 2020.

As encouraging as the overall rise in Asia-Pacific sustainable finance is, Cameron warns against any assumption that it will on its own address the region’s decarbonisation challenges. Sustainable finance remains a small portion of total capital raised. However, use of ESG reporting and disclosure in Asia Pacific is also growing, meaning progress toward meeting the challenges of decarbonisation can be made clearer.

Cameron says Europe remains the global leader for ESG reporting but China has taken significant strides. More than 90 per cent of companies in China now produce ESG reporting, while Singapore and Hong Kong have also improved.

In the antipodes, New Zealand leads Australia in ESG reporting as it plans to make TCFD mandatory for listed and large companies by 2022. Cameron adds that Australia remains a laggard in its progress toward sustainability goals. In a recent UN report, Australia ranked last out of 170 UN members for action in response to climate change. Australia also ranks just 35th globally in progress toward meeting the SDGs.

“While we see Australia voicing some commitments to international climate change and carbon-emissions reduction, we see little evidence of this in practice,” Cameron comments. “Australia remains in the top-three countries in the world for exported greenhouse-gas emissions per capita and among the top-10 for fossil-fuel use per capita.”

DISCLOSURE DEMANDS

Assessing the progress companies are making toward sustainability outcomes, such as net-zero emissions or the SDGs, remains a somewhat difficult task for investors and other market participants. The impact of ESG factors on a company’s credit can also be obscure.

This is exacerbated by the fact that most companies are still reporting on ESG factors as a separate and self-contained exercise – in other words apart from their traditional financial reporting. Cameron says companies should be moving toward ESG becoming a part of standard financial reporting so it becomes intrinsically linked to credit.

“A lack of government-driven mandates has impaired reporting progress. It has been left to industry bodies such as the UN Principles for Responsible Investment, Global Reporting Initiative and Sustainability Accounting Standards Board to create reporting standards and drive momentum,” Cameron explains.

Fixed-income market engagement with companies on ESG performance has historically trailed the equity market. However, Cameron says growth in sustainable debt, whether it is via GSS-labelled or sustainability-linked bonds or loans, gives investors greater ability to assess tangible impact and how each business aligns with sustainability goals.

“Our role as a data provider is to help clients manage this variation and evaluate investment risks, including ESG. As market trends evolve, our methodologies for data reporting also need to adapt. Investors require consistent data and companies report in varying formats. Harmonisation and more stringent reporting standards across jurisdictions can help solve this challenge,” explains Cameron.

This degree of harmonisation across jurisdictions would be helpful for many market participants. This is happening in some pockets, though it is typically driven by industry bodies such as work being done by the International Financial Reporting Standards Foundation, rather than governments.

Refinitiv believes its data solutions can be used by market participants to cut through their requirements. In particular, the availability of quantitative rather than qualitative data enables clients to manipulate and interpret inputs in ways that suit their mandates.

While continuing to align with existing mandates, Refinitiv is also looking to stay ahead of the regulatory curve by incorporating new regimes such as the Taskforce on Nature-related Climate Disclosure. Cameron says this standard will be particularly important for Australian clients because of the acuteness of local nature and biodiversity risk.

She adds that buy-side clients typically use Refinitiv’s workflow tools to help incorporate ESG into investment decision- making, valuations, portfolio reporting and aggregation, negative screening and regulatory mapping. “The factors we know are important to our buy-side customers include global coverage, focus on risk, and materiality and analyst research. Our priority is to provide quality, reputable ESG data to aid the allocation of capital,” comments Cameron.

In addition, Cameron says sell-side research teams also make use of these tools and Refinitiv aims to continue broadening its ESG solutions, particularly through identification of where its recent partnership with FTSE Russell can be leveraged.

“An area of focus for Refinitiv has always been the development of partnerships that complement our offering. An example of this is MarketPsych, which performs high-speed text analysis on news, social media and regulatory filings to deliver corporate insights to clients,” Cameron comments.

Sponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.