EU funding enters its next generation

In October 2020, the EU embarked on a massively enhanced funding programme – immediately making it a major borrower on the international stage following a relatively quiet decade. But COVID-19 response funding was only the beginning of the EU’s medium-term debt-market plans, and it is now setting up to be a significant issuer for the foreseeable future with ramifications well beyond the Eurozone.

Matt Zaunmayr Deputy Editor KANGANEWS

The EU’s support to mitigate unemployment risks in an emergency (SURE) funding programme – designed to provide loans to member states during the pandemic – raised €90 billion (US$106 billion) via syndicated social-bond issuance between October 2020 and May 2021 in maturities from five to 30 years. The funding was a remarkable increase for the EU, which raised less than €70 billion in total from 2010-19.

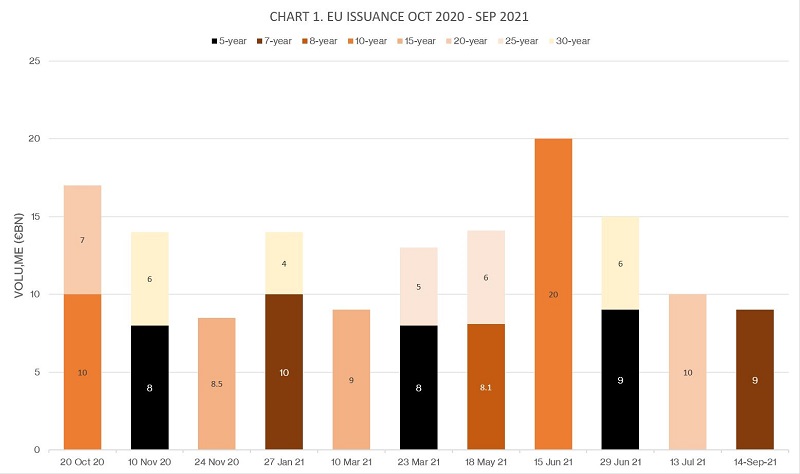

It is the new normal, though. Between June and September this year, the EU printed the first four deals associated with the next stage of its COVID-19 recovery stimulus – the next generation EU (NGEU) plan (see chart 1).

NGEU funding will enable a massive EU stimulus programme – potentially €800 billion – between 2021 and 2026. EU member states can apply for NGEU loans to invest in areas such as research and development, climate-transition measures, health preparedness, resilience and digitisation.

To facilitate this big funding task efficiently, the EU has added short-term bills and bond tenders to its toolbox. It has also unveiled a green-bond programme that is set to become the world’s largest (see box).

A European Commission (EC) spokesperson tells KangaNews: “NGEU is a different ball game. Given the volume of borrowing and the specificities of the programme, back-to-back lending is no longer a solution. The commission therefore decided to implement a diversified funding strategy in line with the best practice of other big issuers.”

During the SURE programme, there was some conjecture as to whether the EU should be considered a sovereign or supranational borrower. By introducing bond auctions, the bills programme and transparency of timing, the EU is becoming more predictable and transparent.

A SURE THING

Several questions surrounded the EU’s SURE funding programme when it kicked off in 2020. However, most euro market participants were confident investors could absorb the supply and that the EU would receive plenty of support.

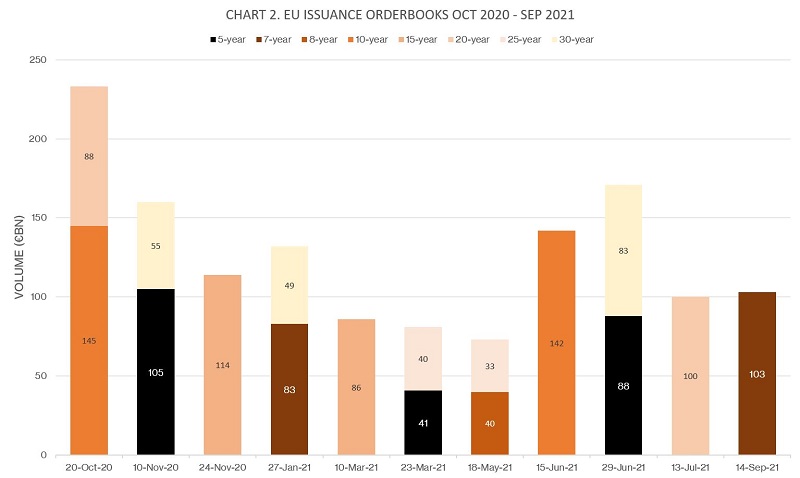

This hypothesis proved to be understatement as the EU’s syndicated deals over the last 12 months – for its SURE and NGEU programmes – have routinely received blowout orderbooks (see chart 2).

Florian Eichert, Frankfurt-based head of covered bond and supranational, sovereign and agency (SSA) research at Crédit Agricole, says European Central Bank (ECB) monetary policy has had a hand in this.

“The ECB buys bonds issued by supranationals such as the EU in secondary markets,” he explains.

“Even more importantly, though, its purchases as well as its TLTROs [targeted long-term refinancing operations] have created vast amounts of excess liquidity in the banking system. There is a shortage of assets to buy for investors other than the banks.”

The next layer of potential market impact was how the EU’s vastly increased issuance volume would affect other euro market borrowers – particularly other SSAs. Theoretically, investment in EU bonds could have come at the expense of allocations to other high-grade names.

SOURCE: EUROPEAN COMMISSION 20 SEPTEMBER 2021

SOURCE: EUROPEAN COMMISSION 20 SEPTEMBER 2021

However, Jean-Christophe Machado, euro rates and derivatives strategist at Natixis in Paris, says other borrowers have felt little impact, either in the form of higher rates or investment outflows. Again, the ECB’s market support has proven crucial, he adds.

EU's big green push

The EU intends to raise 30 per cent – up to €250 billion (US$294.4 billion) – of its next generation EU (NGEU) funding via a new green-bond programme, making it by far the world’s largest green-bond issuer.

The scale of the forthcoming labelled issuance has significant potential to develop the green-bond market as a whole, European market participants say. The first EU green-bond syndication is expected in mid-October.

The EU unveiled its green-bond framework on 7 September. Member states are also submitting recovery and resilience plans (RRPs) to the European Commission, detailing planned reforms and investments to 2026. These RRPs form the basis upon which the EU gives disbursements from the NGEU’s recovery and resilience facility (RRF), as well as the EU’s green-bond use of proceeds.

At a press conference on 7 September, EU commissioner, Johannes Hahn, said: “The NGEU green-bond framework will play an important role to finance the mandatory share of 37 per cent of climate expenditure under the RRF. Member states are eager to fulfil this goal. Many national plans go far beyond this and even allocate up to 60 per cent to measures that support climate objectives.”

SSA borrowers say their strategies have not yet had to change as a result of the EU’s funding programme. In fact, they are confident it has brought them some spill-over benefit (see box).

This is not to say issuance patterns are unchanged. Respondents to the KangaNews SSA Yearbook 2021 borrowers’ survey generally reported greater currency diversity in their funding compared with 2020. Increased volume in the Australian and New Zealand dollar markets is testament to this. However, European SSAs generally tell KangaNews their home market remains the most conducive for demand and pricing.

PRICING AND DEMAND

The impact of the EU’s funding programme on euro market pricing was perhaps the biggest question mark 12 months ago. Prior to the SURE funding programme, EU bonds traded wide of German and French sovereign bonds, but with such small volume on issue many market participants expected relativities to move.

Some feared EU pricing could move wider with the enormous volume being asked of the market, while others posited EU rates would tighten given greater liquidity in its bonds.

Those backing tightening had it right. The EU still trades wide of French sovereign bonds at the short end, says Machado, but its curve is flatter and therefore inside France for longer-dated bonds, with the crossover point at 8-10 years. The EU still trades wide to German sovereign bonds across the curve.

Eichert adds that EU bonds have become the tightest supranational or agency bonds in the euro market, having previously traded above names like European Investment Bank and KfW Bankengruppe.

Machado says: “Greater liquidity in the EU’s bonds compared with its previous issuance programmes – such as the European Financial Stability Mechanism – has brought much greater interest from investors outside Europe. Most non-European investors – particularly those in Asia – have shown greater appetite for shorter-dated deals and the EU could attract greater demand by supplying more in these tenors.”

The EC has noticed growing interest from a wider range of investors across the globe and expects this to continue with the development of its bills and green-bond programmes, according to its spokesperson. “It is our objective further to widen our investor base within and outside Europe, and to increase the attractiveness of the European capital market and of the euro.”

Machado adds that the relatively small percentage of allocations to hedge-fund accounts should provide reassurance to other investors, but that analysts will be watching this component of books closely in each new syndication.

The giant's shadow

Despite an imposing funding requirement, European market participants say the effect of the EU’s bond issuance on other European supranational, sovereign and agency (SSA) issuers has been a positive one, with spill-over demand in evidence.

Otto Weyhausen-Brinkmann, vice president and head of new issues at KfW Bankengruppe in Frankfurt, tells KangaNews the agency has not needed to change its issuance strategy due to the diversified funding options already available to it.

SSAs generally have not faced any issues funding in euros alongside the EU. Weyhausen-Brinkmann says: “Given the ECB [European Central Bank]’s ongoing buying programme, we have seen favourable conditions in the euro market over the course of the year. Oversubscription levels are high and new-issue premia limited for KfW’s transactions as well as for many other euro deals.”

Weyhausen-Brinkmann adds that the Bund swap spread widening over the European summer has further helped pricing. With large redemptions through Q3 2021, he expects favourable conditions to persist.

EU bonds are very liquid and make the entire SSA segment more attractive. Some investors that previously focused on government bonds are now looking at supranational and agency borrowers.

SOVEREIGN STYLE

The SURE programme and the first few NGEU syndications have gone smoothly. But the EU is gearing up for a new phase of funding in which it is pursuing a more transparent issuance strategy. Instead of syndicating on an ad-hoc basis, the EU will issue one bookbuilt transaction per month, with the issuance week determined in advance and communicated via a quarterly newsletter. Bond auctions will also be held once per month and communicated in the same newsletter.

In September, the EU also introduced a short-term bills programme that issues three- and six-month bills to bridge the gap between its long-term funding and loan disbursements. Each bill line has a target new-issuance volume of €2-3 billion and is also available for taps of €1.5-2 billion. The first EU bills auction took place on 15 September, raising €5 billion.

Following the auction, the EC’s commissioner, budget and administration, Johannes Hahn, said: “With the possibility to issue EU bills each month, the commission now has a cheap and efficient bridge financing solution at its disposal. The success of today’s issuance confirms market interest in this brand-new short-term paper. The EU bill programme will attract yet more investors to EU capital markets and boost the role of the euro.”

Mark Byrne, syndicate at TD Securities in London, says the evolution of the EU’s funding strategy reflects a move toward a sovereign-style issuance pattern. “During the SURE programme, there was some conjecture as to whether the EU should be considered a sovereign or supranational borrower,” he says. “By introducing bond auctions, the bills programme and transparency of timing, the EU is becoming more predictable and transparent.”

The size of the EU’s bond lines was already more akin to sovereign than supranational borrowers, and Byrne adds that the behaviour of investors in the secondary market suggests the buy side has placed the issuer in, or close to, the sovereign category. Over the European summer, government bonds rallied to swap to a greater degree than SSAs. Byrne says the EU’s bonds showed stronger correlation to sovereigns than other SSAs.

The EU still sits somewhere between the two sectors, according to Eichert. He explains: “Some investors already view the EU more as a euro risk-free asset with a pick-up to Bunds than as a supranational. But for many this step would require current funding volume not only to last for a few years but to be permanent. If this were the case, a more fundamental shift in how the EU trades versus the likes of Germany could occur.”

Whether the full move to effective sovereign status happens is a question for the longer term. Eicherts notes it is “a political issue and nothing the EU funding team can address with its strategy”.

“Greater liquidity in the EU’s bonds compared with its previous issuance programmes has brought much greater interest from investors outside Europe. Most non-European investors have shown greater appetite for shorter-dated deals and the EU could attract greater demand by supplying more in these tenors.”

SCANNING THE HORIZON

While transactions have proceeded seemingly without a hiccup, the high degree of correlation between this success and the ECB’s various QE measures is front of mind for European market watchers. The ECB’s asset-purchase programmes remain supportive of the euro market. Machado says net supply is likely to be negative by €50-100 billion in the remainder of 2021.

The ECB has also pushed back against speculation it will begin tightening liquidity conditions in 2022. In a speech on 20 September, ECB executive board member, Isabel Schnabel, said: “Given the remaining uncertainty regarding the pandemic and the economic and inflation outlook, our asset purchases will remain crucial in the time to come, paving the way out of the pandemic and toward reaching our inflation target.”

However, consensus remains that some degree of tapering will take place in 2022. With the NGEU programme set to run until at least 2026, the EU is likely at some point to contend with a market less supported by central-bank purchases.

This may not matter, though. Eichert expects ECB asset purchases will be lower in 2022 but that exceptionally high levels of excess liquidity will remain in the euro system for years to come. “Hence, if priced fairly, EU orderbooks will remain large,” he says. “The EU may not always have 11-times oversubscribed books as it had in its September deal, but this is not necessary.”

A crucial factor for the viability of the EU’s funding programme over the medium term may be that it has become an established part of the market while the backdrop is so supportive.

“By the time QE is meaningfully withdrawn, EU issuance will be a normal part of the European market,” Eichert comments. “The removal of QE could bring more scope for market turbulence, but the EU’s borrowing programme will not be anything new for the market to grapple with.”

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

SSA Yearbook 2023

The annual guide to the world's most significant supranational, sovereign and agency sector issuers.

Related news