Dissecting ESG in Australian private debt

The private-debt asset class is growing as investors seek reliable return in the ultra-low rates and spread environment. As private debt becomes increasingly mainstream, Commonwealth Bank of Australia and KangaNews explore how investors integrate environmental, social and governance practices in their strategies.

Helen Craig Head of Operations KANGANEWS

Laurence Davison Head of Content KANGANEWS

* All chart data compiled by KangaNews September 2021

This research forms the second part of an initiative to understand the extent of environmental, social and governance (ESG) adoption in the Australian debt investor base and the motivating factors. Earlier in 2021, Commonwealth Bank of Australia (CBA) and KangaNews surveyed mainstream Australian fixed-income investors for the second year, publishing the results and individual investor qualitative feedback in the H2 KangaNews Sustainable Finance supplement.

Also in 2021, CBA and KangaNews supplemented the initial survey with a second one, this time targeted at and tailored to private-debt investors. The survey, which investors responded to in August and September, was followed by a September roundtable of six leading local investors from the sector to explore the results in depth. Investor comments that follow come from the roundtable discussion. More than 30 investors participated in the survey – roughly the same number that provided information for the earlier fixed-income survey – including most of the leading asset managers in the sector.

Research into ESG investment drivers tends to be nascent in fixed income, with the focus typically on global equity markets. Private debt is arguably even less well understood than mainstream fixed income, given the relative youth of the asset class as an institutional investment option in most jurisdictions – including Australia – and of course its private nature.

The bond market has had the benefit of the light shone on buy-side preferences by a decade-plus of green, social and sustainability (GSS) bond issuance and the rise of KPI-based sustainability-linked instruments. Such headline-grabbing transactions are anathema to the private-debt world.

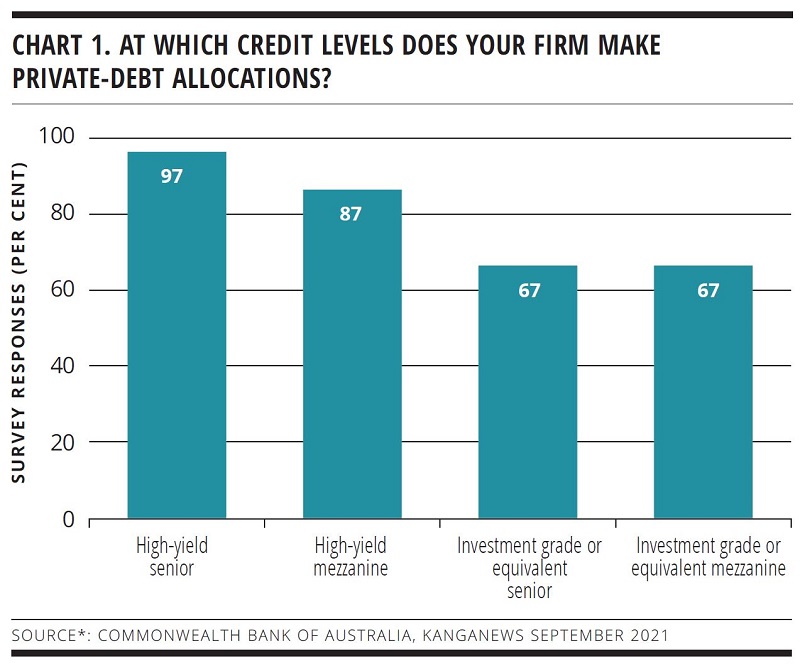

‘Private debt’ covers a raft of investment options, from major infrastructure projects to SME lending and from secure investment grade to high yield, as well as a range of securities including institutional loan placements, vanilla bond structures and securitisation. Responses to the CBA-KangaNews survey suggest the focus is on high yield but not exclusively so – almost all investors buy high-yield product but two-thirds say they are also active in investment-grade debt (see chart 1).

“It is clear that ESG, as a whole, is baked into investors’ decision-making process. We are still getting to grips with whether there are consistent criteria across E, S and G, or whether it is more ad hoc – including on a credit-by-credit basis.”

Button TextHIGH SELF-ASSESSMENT

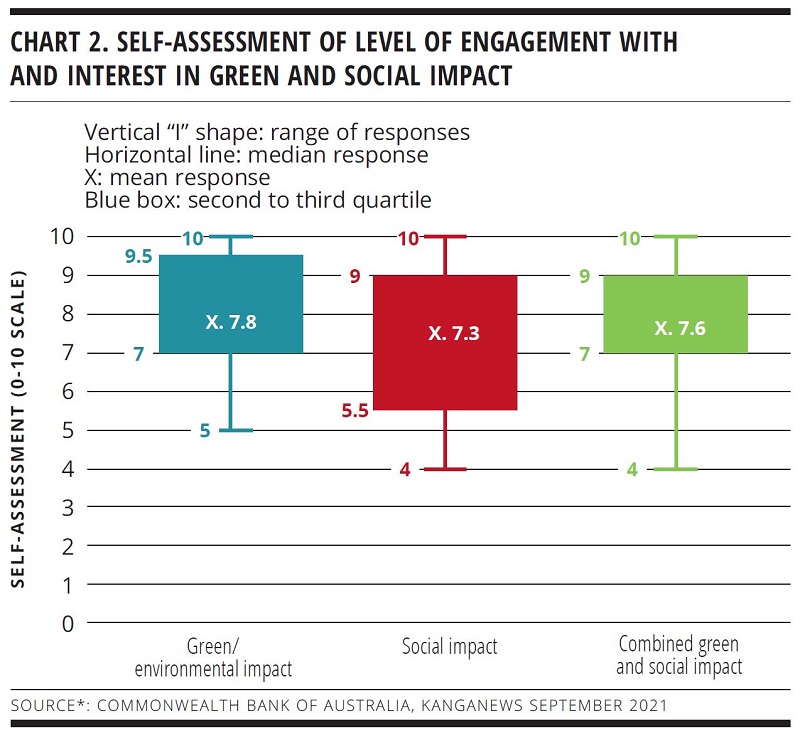

Perhaps the clearest signal from the survey is that private-debt investors do not consider themselves to be laggards in ESG – far from it. Asked to self-assess their firm’s level of engagement with and interest in environmental, social, and combined environmental and social factors on a scale of zero to 10, investors record an average response of more than 7 for all three – with at least some survey respondents registering a 10 out of 10 mark for all three (see chart 2).

“Private debt is fertile ground for ESG because we, as a group of investors, get a lot more engagement at fundamental level – we get to shape terms and conditions on every one of our private-debt deals. In a big corporate bond, often it is all prepackaged with a label on it, take it or leave it,” explains Bob Sahota, managing director and chief investment officer at Revolution Asset Management in Sydney.

Adam Scully, Melbourne-based senior portfolio manager at Alexander Funds Management, adds: “It is much easier to reach a suitable conclusion when the negotiation is between a few parties than when it is necessary to find something that appeals to a disparate range of investors. On the face of it, this means there is more scope to drive ESG agendas in the private space – because we are negotiating structures with senior management.”

In other words, private-debt investors believe the nature of their investments does not require them to be, in effect, sustainability takers – only able to respond to the ESG characteristics of borrowers and specific debt instruments as they are brought to market. An example of this is the sustainability-linked debt market, in which bond investors are typically offered a set of borrower- and arranger-developed KPIs, with limited opportunity to provide feedback or shape the instrument.

By contrast, Pete Robinson, head of investment strategy, fixed income at CIP Asset Management in Sydney, comments: “For us, the difference between public and private really comes down to the opportunity to engage with management on how they see the long-term sustainability of their businesses. This is why we talk about ‘sustainability with substance’.” He continues: “In private markets, with direct engagement and where we expect to hold an exposure through its life, it is an ongoing relationship with borrowers that includes far more opportunity to engage with substance.”

“In the private debt space, if we are participating in a debt transaction with a five-, seven- or 10-year horizon we are automatically thinking about what the borrower’s business is going to look like when the facility matures. This is a natural fit with an ESG lens – so I am not surprised the sector rates itself so highly on ESG engagement.”

Button TextIn some cases, private-debt investment affords fund managers the opportunity to seek opportunities aligned with their ESG goals. Richard Lovell, executive director and head of debt markets at Clean Energy Finance Corporation (CEFC) in Sydney, explains that the asset manager has been able to pursue opportunities where it believes there is a real need to promote emissions-reduction in particular sectors. Agriculture and manufacturing are just two examples.

While it is more typical for debt investors, including CEFC, to respond to borrower funding requirements rather than actively seeking lending opportunities, Lovell adds: “We spend a lot of time crafting deals from scratch, either way. We think it can be far more fruitful to seek ESG outcomes in private debt than in other asset classes, because we have the opportunity to negotiate on a bilateral basis.”

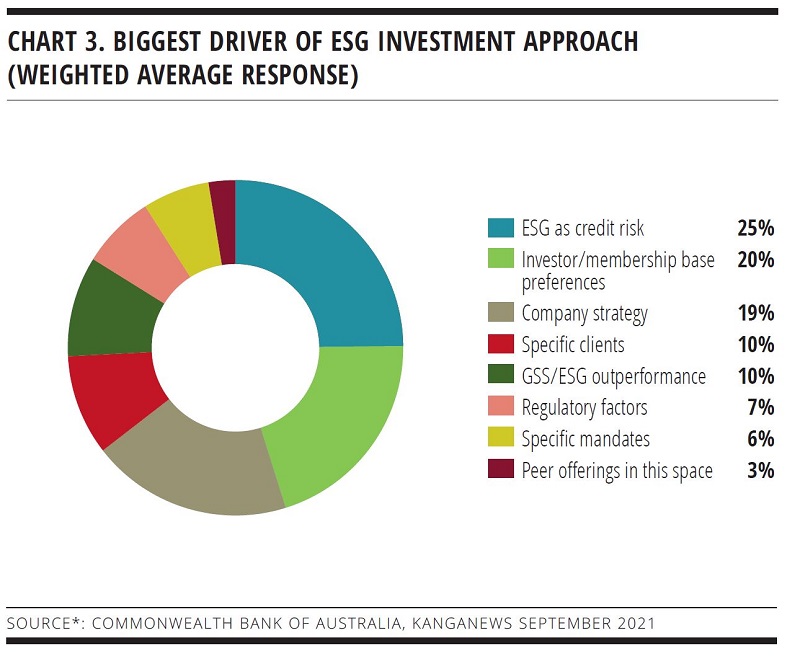

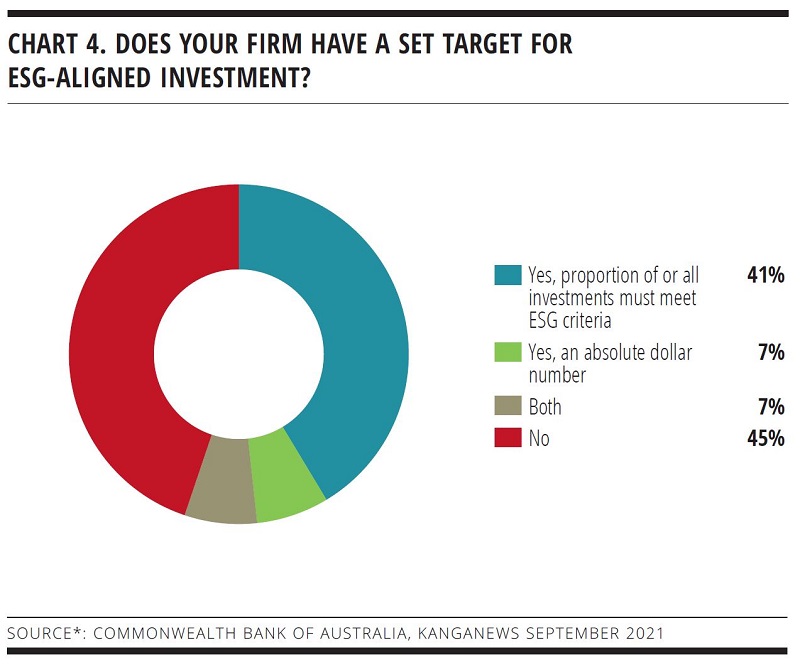

Private-debt investors certainly believe ESG is an integral part of their process. The most common driver, according to the CBA-KangaNews survey, is the growing understanding that ESG risk is a core component of overall credit risk (see chart 3). At the same time, only a small majority of private-debt investors say they have firm-level targets for ESG investment, either as a proportion of assets under management or – more rarely – as a fixed dollar amount (see chart 4).

“In the private-debt space, if we are participating in a debt transaction with a five-, seven- or 10-year horizon we are automatically thinking about what the borrower’s business is going to look like when the facility matures,” says Linda Cunningham, head of debt at Cbus in Melbourne. “This is a natural fit with an ESG lens – so I am not surprised the sector rates itself so highly on ESG engagement.”

“As a very bespoke asset class, private debt takes in a range of industries and businesses. This means we can’t have a single checklist that applies to all deals. Our ESG view can have an impact on a deal’s economics but we are also advocates of greater reporting and information provision.”

Button TextESG APPROACHES

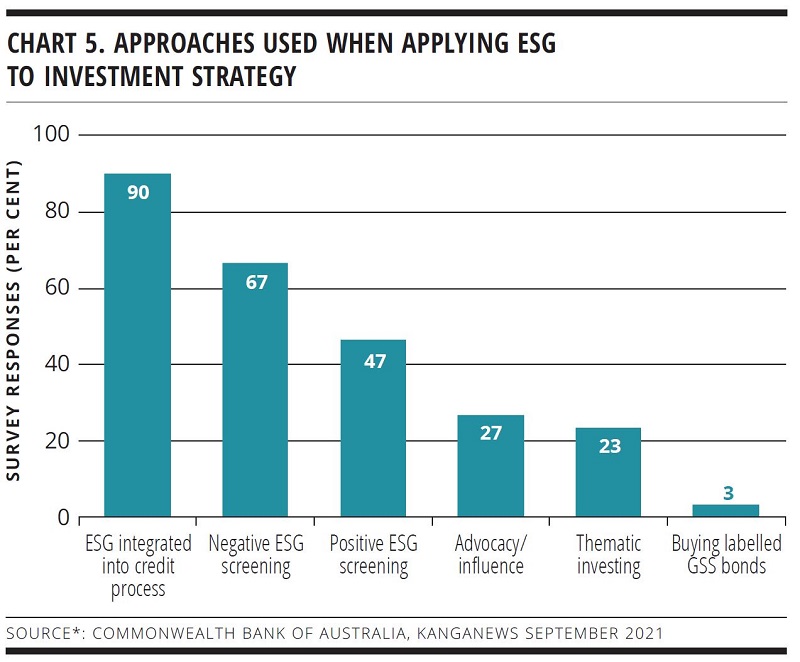

It is no surprise, then, that 90 per cent of responses to the CBA-KangaNews survey report that their firm integrates ESG into the overall credit process as opposed to having a separate ESG function. This ranks well ahead even of negative screening (see chart 5).

“ESG is part of our risk assessment, and credit analysis is a risk-assessment exercise,” Scully explains. “Any ESG topic that is relevant to a particular individual credit will – if we think it is a risk to the success of our investment – be something we look to mitigate. This might be through documentation or advocacy for changed business practices, but it is an integral part of making sure that everything we do makes sense in a risk-adjusted manner.”

Two-thirds of surveyed private-debt investors report using negative screens, and while this is the second-most used ESG approach, it significantly lags the equivalent result from the CBA-KangaNews survey of mainstream Australian fixed-income investors. Negative screening was ubiquitous in the earlier survey, being deployed by 97 per cent of responding investors.

At the private-debt roundtable, investors suggested the heterogenous nature of their asset class makes uniform ESG overlays less useful. This also explains why most ESG approaches do not produce a red-line outcome for investment decisions.

Sahota explains: “As a very bespoke asset class, private debt takes in a range of industries and businesses. This means we can’t have a single checklist that applies to all deals. Our ESG view can have an impact on a deal’s economics but we are also advocates of greater reporting and information provision.”

Scully adds: “We have negative screening that rules out industries we think have inherent ESG risk that cannot possibly be mitigated, as well as placing limits on those that have higher levels of ESG risk as the norm. Then we have our own policy and procedure on credit modelling across corporate and structured credit. This is really a qualitative process, though we would love to generate a quantitative outcome over time.”

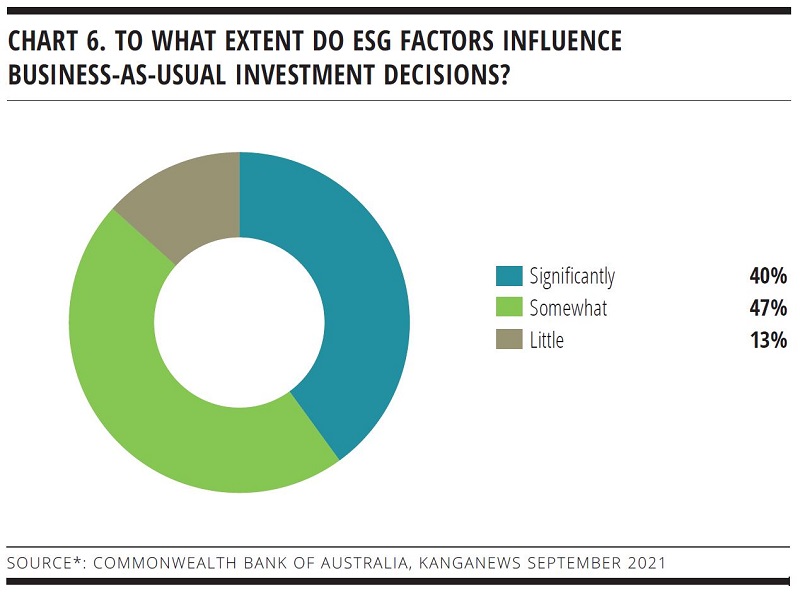

Further illustrating the degree to which ESG considerations are part of the business-as-usual environment in the private-debt space, nearly 90 per cent of respondents to the CBA-KangaNews survey say ESG has a “significant” or “somewhat” of an influence on investment decisions – including 40 per cent at significant level (see chart 6).

“Entity-level assessment certainly seems to be absolutely front of mind nowadays, before an assessment of the debt instrument takes place. We hear it across the public and private side, which shows how the market is maturing in its thinking.”

Button TextWhile the impact may be significant it is rarely as straightforward as a simple red or green light to buy. The fact that private-debt investors can negotiate with borrowers on sustainability strategy and the trajectory of their environmental performance means there can be more impact than a pure negative-screen-led ESG approach. Investors suggest this is often more art than science, however.

Robinson comments: “Even when we are looking at something like cutting thermal coal, the question becomes really difficult when it is not 60 per cent of a business’s revenue but 10 or 15 per cent of revenue and declining. In this case, we would look at the trajectory of this component of revenue. We would rate this type of business as at least a medium environmental risk, but we would be willing to engage with its management team about what it believes to be the direction of the business.”

Angus St John, Sydney-based global head of investor client management at CBA, adds: “It is clear that ESG, as a whole, is baked into investors’ decision-making process. We are still getting to grips with whether there are consistent criteria across E, S and G, or whether it is more ad hoc – including on a credit-by-credit basis.”

There is also some doubt about the idea of using debt financing explicitly to fund borrowers’ environmental transition, based on the fundamental role of debt as a stable part of the capital structure. There is significant interest in the concept but it has yet to garner universal support – and some private-debt investors do not believe transition is an appropriate use of debt financing for risk reasons (see box).

“I have heard it said that relying on third parties for data is like wearing someone else’s glasses – it is really difficult to get a clear picture. Creating tools internally allows for a very holistic and consistent view, right across our business and throughout the world, as well as access to information from an amazing amount of data sources.”

Button TextMixed support for transition

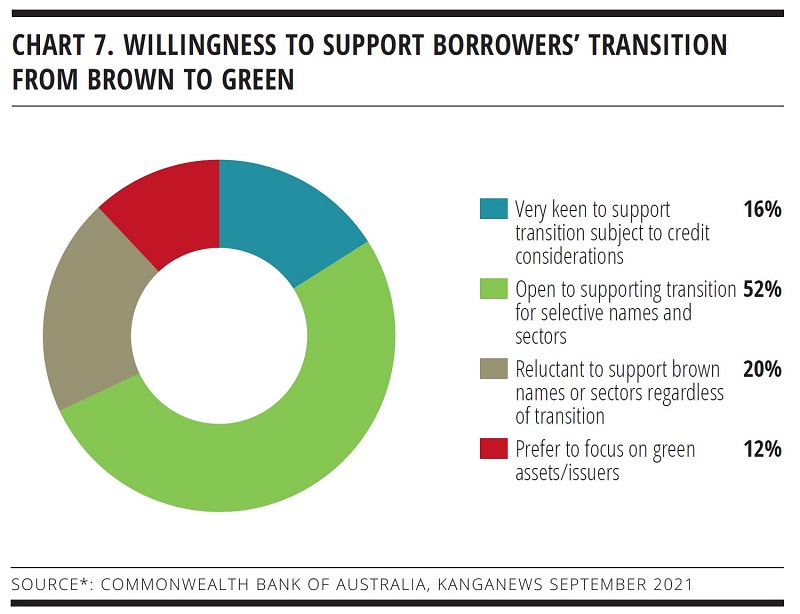

Some market commentators believe funding environmental transition is the holy grail of sustainable finance, as doing so creates the greatest impact from the investment dollar. Private-debt investors are interested but not universally convinced transition is a suitable use of their capital.

Two-thirds of respondents to the Commonwealth Bank of Australia-KangaNews private-debt investor environmental, social and governance (ESG) survey say they are willing to support ‘brown-to-green’ transition with their allocations, but the clear majority add this would only be on a highly selective basis (see chart 7).

Revolution Asset Management’s managing director and chief investment officer, Bob Sahota, says: “A key part of the equation with transition is where we sit on the risk-return spectrum and the risk tolerance in our strategy.”

The main goal is to come up with an appropriate basis on which to assess whether the transition being proposed is legitimate. Private debt is a good place to make this work because both the asset class and transition require bilateral negotiations.

LABELS AND REPORTING

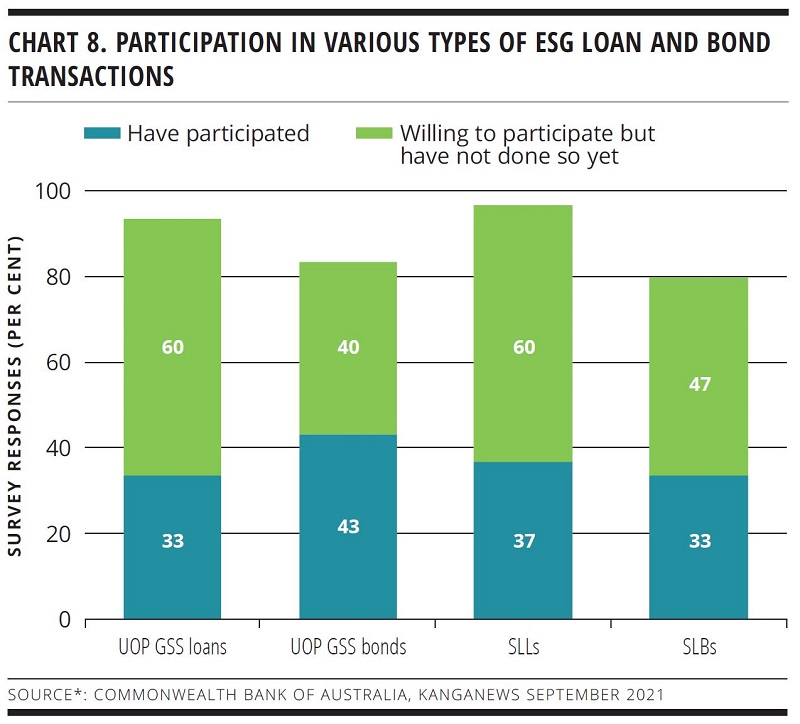

Given the degree of ESG integration in the normal investment process, private-debt investors have an interesting relationship with labelled instruments. Only a tiny minority say buying GSS bonds is a component of their ESG strategy in and of itself, but a clear majority of investors responding to the CBA-KangaNews survey say they either have bought or would be willing to buy use-of-proceeds (UOP) GSS or KPI-based sustainability-linked securities (see chart 8).

The suggestion seems to be that the private-debt investor base has not relied on instrument-level labelling. “We are willing to do our own work to understand what companies are doing and how they are doing it,” Cunningham explains. “In fact, while it is certainly not always the case, we have on occasion concluded that an issuer seems to be focusing primarily on getting a good news story with the issuance of a labelled loan or bond.”

On the other hand, the process of certifying a security can, and often does, add to ESG transparency and improves investor response to the borrower, according to Charles Davis, managing director and head of sustainable finance and ESG at CBA in Sydney. The survey suggests this is increasingly becoming a component of the conversation between companies and their debt investors on sustainability rather than its end point, though.

“As the UOP market started to develop, there was a lot of focus on specific debt instruments, such as green bonds, and maybe not as much focus at the overall borrower level,” Davis adds. “Entity-level assessment certainly seems to be absolutely front of mind nowadays, before an assessment of the debt instrument takes place. We hear it across the public and private side, which shows how the market is maturing in its thinking.”

“It may be a liquidity-rich world, but I believe companies deemed poor ESG performers are already finding their available liquidity reducing. Institutional and individual investors are constantly expecting more influence over where their capital is allocated, to ensure its use aligns with their beliefs and values.”

Button TextCunningham adds: “Some of the ongoing reports that come out of the deal certification process will be really important and indeed I wouldn’t be surprised if we start seeing more of a lens turned on these over the next couple of years. The market in general will start holding companies to account over whether they have or have not achieved the goals they set themselves.”

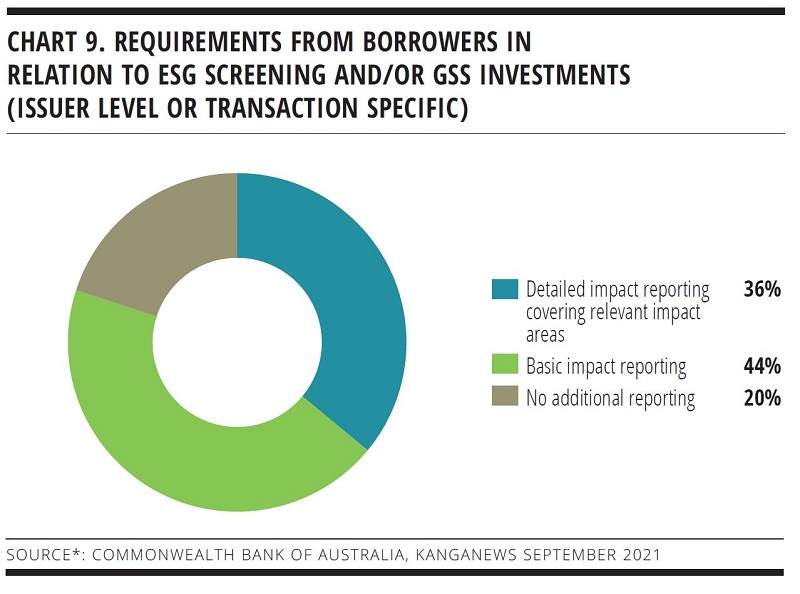

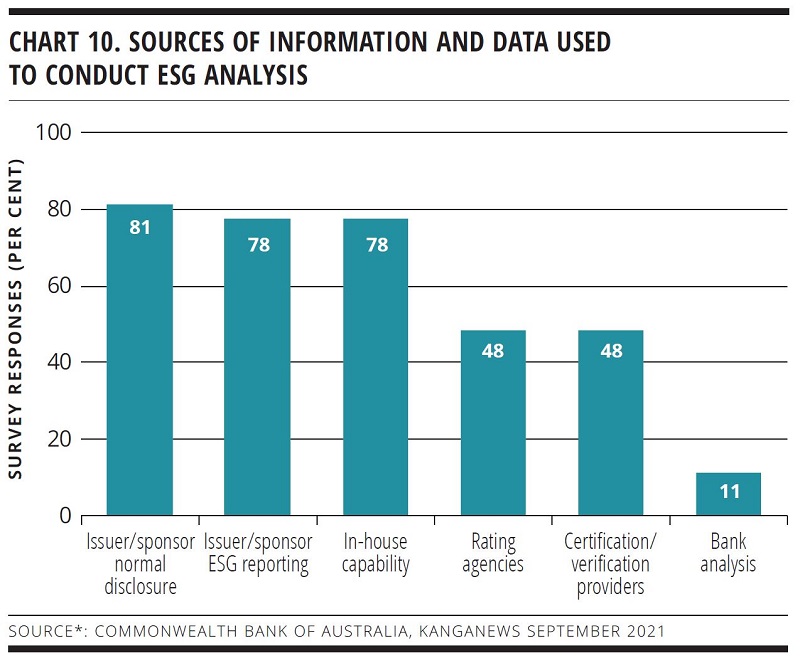

More than a third of private-debt investors already require detailed impact reporting from borrowers, while only 20 per cent require nothing beyond standard reporting (see chart 9). Meanwhile, although issuer reporting – standard and ESG-specific – is the most-used source of sustainability data, more than three-quarters of private-debt investors say their in-house analysis is key (see chart 10).

This should not come as a surprise, as Nicole Kidd, Sydney-based head of private debt, Australia at Schroders, explains. “I have heard it said that relying on third parties for data is like wearing someone else’s glasses – it is really difficult to get a clear picture. Creating tools internally allows for a very holistic and consistent view, right across our business and throughout the world, as well as access to information from an amazing amount of data sources.”

The scale and depth of in-house analysis used by private-debt investors is extensive. Kidd continues: “The criteria we use to assess businesses from an ESG lens is vastly more thorough than I was used to from my background in investment banking – and it is evolving all the time. How we look at a company today is probably not going to be how we look at it in 12 months.”

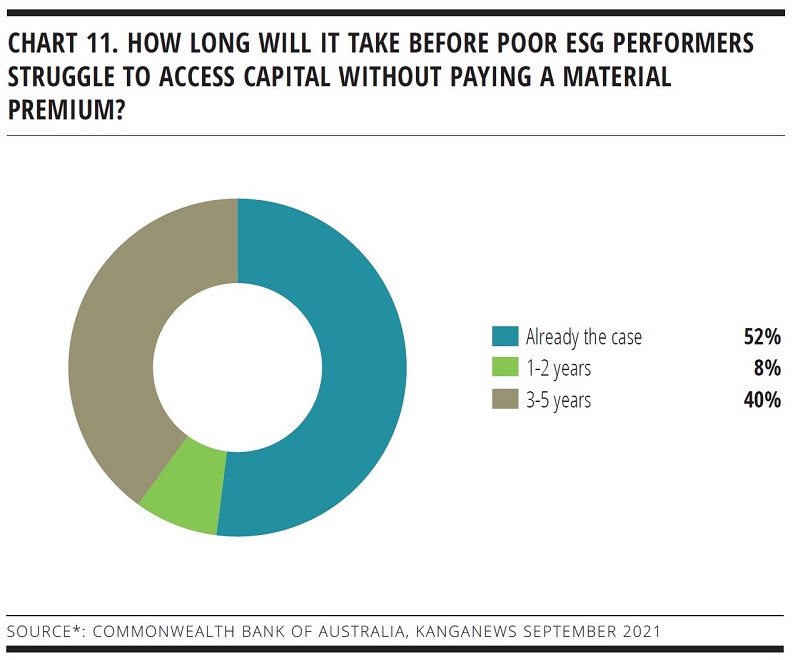

The theme of rapid evolution comes up again and again in the private-debt space, and its investors clearly anticipate poor ESG performers having to pay a material capital premium. More than half the respondents to the CBA-KangaNews private-debt survey say this is already the case and all respondents predict this outcome within 3-5 years (see chart 11).

As Scully points out: “It may be a liquidity-rich world, but I believe companies deemed poor ESG performers are already finding their available liquidity reducing. Institutional and individual investors constantly expect more influence over where their capital is allocated, to ensure its use aligns with their beliefs and values.”

“For us, the difference between public and private really comes down to the opportunity to engage with management on how they see the long-term sustainability of their businesses. This is why we talk about ‘sustainability with substance’.”

Button TextSponsored by

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news

SAFA reflects on 100 per cent sustainable debt plans in wake of debut issuance

South Australian Government Financing Authority has been working on plans to map its whole debt book – and thus pave the way for a fully sustainability-labelled issuance programme – for a matter of years. In the wake of its debut labelled transaction, Peter King, head of financial markets and client services at the state issuer, talks to KangaNews about the reception and the importance of a programme that is unique in Australia.

Financing Australia’s energy transition narrows focus on challenging areas

There is more to Australian energy transition than delivering a big volume of renewables generation capacity. Industry leaders suggest the faster than anticipated exit of coal is changing the focus of those responsible for delivering the transition, to areas that require particular technological or investment attention.