Mixed support for transition

Some market commentators believe funding environmental transition is the holy grail of sustainable finance, as doing so creates the greatest impact from the investment dollar. Private-debt investors are interested but not universally convinced transition is a suitable use of their capital.

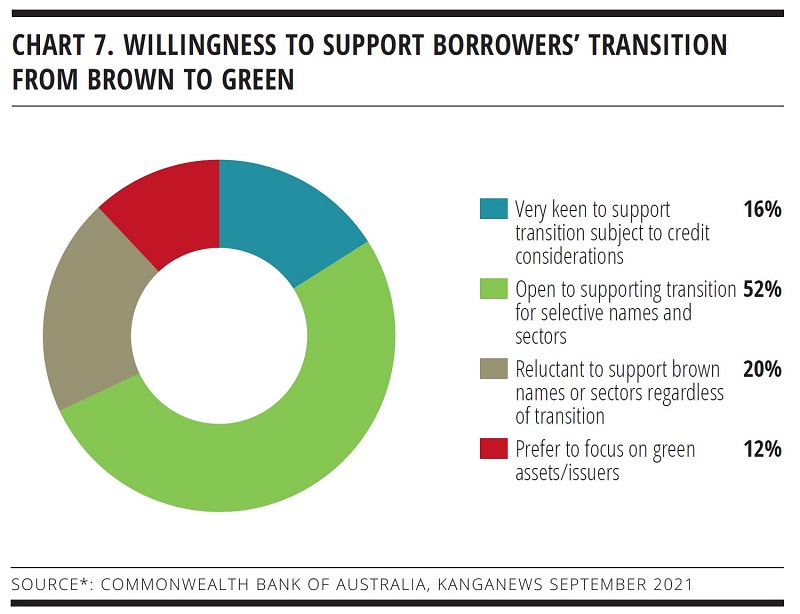

Two-thirds of respondents to the Commonwealth Bank of Australia-KangaNews private-debt investor environmental, social and governance (ESG) survey say they are willing to support ‘brown-to-green’ transition with their allocations, but the clear majority add this would only be on a highly selective basis (see chart 7).

Revolution Asset Management’s managing director and chief investment officer, Bob Sahota, says: “A key part of the equation with transition is where we sit on the risk-return spectrum and the risk tolerance in our strategy. We are not running a high-return-seeking strategy that is prepared to take transition risk – because, clearly, there is execution risk in transition. Investors willing to support this are likely to be demanding a lot higher return than we typically target at Revolution.”

Linda Cunningham, head of debt at Cbus, has a similar perspective about the risk inherent to financing transition. In fact, it leads her fundamentally to question whether debt should be used extensively for this purpose.

“Transition financing is a challenging area, especially if we are dealing with a borrower facing the real risk of holding a stranded asset,” she explains. “As debt investors, we are meant to be at the conservative end of the capital stack. If we look at a business and conclude there are significant risks involved in the level of debt, we would probably be expecting to see a greater degree of support and contribution from the equity owners for the funding of these assets.”

For private-debt investors, it may just be a case of being highly selective about what transition opportunities to pursue. Richard Lovell, executive director and head of debt markets at Clean Energy Finance Corporation, says plenty of opportunities are available and it is relatively straightforward to rule out those with no plausible path to a sustainable future – where stranded assets are an inevitability.

The main goal is to come up with an appropriate basis on which to assess whether the transition being proposed is legitimate. Private debt is a good place to make this work because both the asset class and transition require bilateral negotiations.

From there, he adds: “The main goal is to come up with an appropriate basis on which to assess whether the transition being proposed is legitimate. This is where things like science-based targets and a plausible emissions trajectory for the industry, sector and company come in. Private debt is a good place to make this work because both the asset class and transition require bilateral negotiations.”

The wealth of opportunities is too great to ignore, some investors believe. Indeed, the significance of transition in today’s economy is so great it may become, if it is not already, impossible to ignore. Nicole Kidd, head of private debt, Australia at Schroders, argues the transition universe is much larger than its commonly discussed focus in the energy, natural resources and transport sectors.

“Most companies are not actually green and, on some level, are on their own sustainability journeys,” Kidd notes. “As investors, we have to break down what is actually going on within each company. We want to understand how each business we are considering financing is improving and contributing to reducing carbon emissions or driving a more circular economy.”