Offshore securitisation back on the menu for nonbanks

Market talk is growing about a potential return to offshore issuance by Australian securitisation sponsors – including some nonmortgage asset-backed securities – if, as expected, issuance needs remain high while domestic market tailwinds abate. Australian investors note recent and expected developments in the credit market could soften demand and issuers are already starting to venture offshore once more.

Dan O'Leary Editor KANGANEWS

Chris Rich Staff Writer KANGANEWS

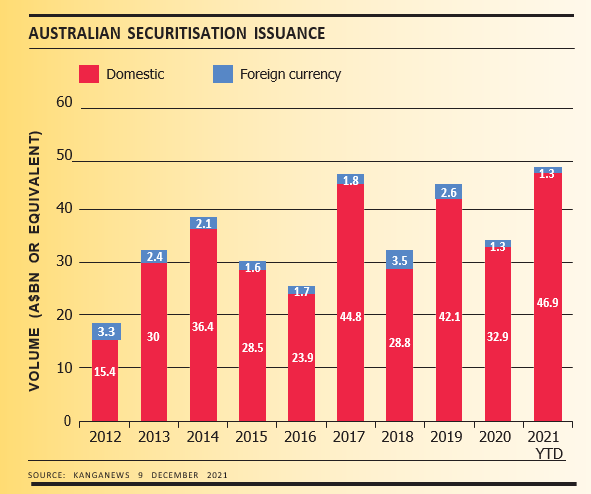

With a few deals still to print in mid- December 2021, Australian securitisation has had a record year: the A$47.3 billion (US$33.5 billion) of total issuance, driven by nonbank names, surpasses the A$46.6 billion priced in 2017 (see chart). On the other hand, Australian issuers have focused on domestic-currency deal flow to a greater extent than ever before. With just A$1.3 billion equivalent priced, foreign-currency securitisation actually failed to surpass a decade-long low in 2021.

Australia’s nonbank financial institutions have driven 2021’s record securitisation issuance, taking advantage of ideal pricing conditions and ample demand. Fixed-income investors have ploughed into deals thanks to a lack of supply in other asset classes, notably bank senior issuance, and a hunt for yield.

But recent changes to the committed liquidity facility (CLF) are likely to mean more competing issuance as banks increase funding to meet high-quality liquid-asset requirements. Australian banks were already returning to the wholesale market at pace after the end of the term-funding facility. In fact, the big-four banks say their wholesale issuance expectations are already back to pre- pandemic levels.

Securitisation issuers acknowledge the tight pricing levels of 2021 are unlikely to be maintained. Nonbank securitisation is typically priced relative to the major-bank senior secondary curve and bank spreads have drifted 20-25 basis points wider since the CLF announcement in September, market users confirm.

The A2 senior tranche of Resimac’s latest deal from its Bastille programme priced at 100 basis points over three-month bank bills, 15 basis points wider than the equivalent notes from the programme’s previous print, in April 2021. The two have slightly different weighted-average life figures. Resimac also included US dollar notes in its market return (see box below).

Lillian Nunez, executive director, debt investments at IFM Investors in Melbourne, says investors were something of a captive audience in the absence of bank supply. “There has been very little else to invest in with yield for some investors,” she tells KangaNews. “A lot of investors that typically buy other credit paper have come into the securitisation market as an alternative. We still think there is strong appetite particularly in the mezzanine space, but the spread compression we have seen over the last nine months or more is starting to ease.”

Nunez says investors were willing to buy primary securitisations at ever tighter spreads in 2021 – but conditions are changing. “Investors, particularly senior, are either getting full or they are thinking about alternative assets,” she adds.

Resimac breaks foreign-currency securitisation drought

Resimac returned to foreign-currency issuance in October with the inclusion of US dollar notes in its Bastille Trust Series 2021-2NC transaction. The same issuer followed in December with a yen tranche in Premier Series 2021-3. These deals are two of just three Australian-origin securitisation transactions priced in 2021 that include foreign-currency tranches.

The A$1.5 billion (US$1.1 billion) equivalent Bastille residential mortgage-backed securities (RMBS) deal included two US dollar tranches, totalling A$727.5 million equivalent. The Premier RMBS included a ¥16 billion (US$140.8 million) note.

Speaking after the Bastille deal, Andrew Marsden, general manager, group treasury at Resimac in Sydney, told KangaNews the issuer included the US dollar tranches for greater volume certainty, supported by attractive landed cost of funds relative to Australian dollar pricing.

The US dollar component follows only a US$360 million tranche in Resimac’s Premier Series 2021-1 deal in March and limited foreign- currency issuance has carried over from 2020.

Record demand in the Australian dollar market for senior tranches over the last year – off the back of an abundance of liquidity and altered supply dynamics in the banking complex – has kept issuance at home.

Marsden says borrowing costs in the domestic market over this period have been as low as they have been at any point since the financial crisis. “However, it is fair to say the spread cycle has turned and we will probably see a normalisation of securitisation margins in line with the comparable COVID-19 recovery seen in the US dollar and sterling markets,” he tells KangaNews.

“While I would not say the domestic senior securitisation market has capacity constraints for single issuers, Australia has always been a net importer of capital and I believe this should be reflected in a sustainable and resilient nonbank funding strategy, just as it is for ADI [authorised deposit-taking institution] programmes,” Marsden continues.

He explains Resimac has always maintained the view that currency and jurisdictional diversity is essential for its funding strategy through cycles, and to underpin its assets-under-management growth objectives.

Marsden says there was robust demand in the A2 tranche of Resimac’s Bastille deal from real-money and bank balance- sheet accounts. “There seems to be a discovery process for pricing taking place,” he notes. “But I do not think the CLF [committed liquidity facility] changes will have a long-term impact on nonbank RMBS demand as the triple-A product should continue to feature in bank and real-money mandates, and be attractive to offshore buyers when the relative-value proposition works.”

Another notable development in Resimac’s market return was that tranche A1b of the Bastille deal referenced SOFR – the first time an Australian issuer securitisation has issued using the alternative reference rate for the US market as a benchmark. It took the same approach with the Premier transaction, in which the yen notes priced off TONA.

Marsden says using SOFR was an easy change for Resimac to adopt. “We still offered a LIBOR tranche but the bulk of demand was in the SOFR bond,” he says. “As we make plans for 2022 US dollar issuance, SOFR will be our future along with offering fixed-rate bonds where there is appetite.”

He adds the US dollar book was 2.3 times oversubscribed, with strong interest in the product in evidence given the consistent performance of Australian RMBS.

Many market users expect issuers increasingly to explore foreign-currency options to find additional liquidity. Traditionally, offshore issuance has been the domain of Australia’s largest nonbank securitisers and larger bank names outside the majors – specifically Macquarie Bank. But some believe a larger cohort of Australian names may be willing to engage with international markets.

Sarah Samson, Melbourne-based global head of securitisation origination at National Australia Bank, says other nonbank residential mortgage-backed securities (RMBS) issuers will likely tap offshore markets, while established nonmortgage asset-backed securities (ABS) issuers – particularly auto-loan lenders – are likely to begin exploring US dollar offerings. “Once nonmortgage ABS issuers grow and become a bigger proportion of what is issued in Australia, they will likely need to go offshore,” she notes.

Samson says a clutch of nonbank RMBS issuers are growing quickly and will also likely need to tap offshore markets to build funding diversity and even to sustain their programmes at attractive pricing levels. “Origination volumes are growing and issuing domestically is a little more challenging than it was a couple of months ago,” Samson adds.

DOMESTIC BID

However, some domestic investors say their level of interest in securitisation could also step up if spreads widen. IFM, for instance, stepped back from public securitisations in favour of private warehouse allocations as public spreads tightened through 2021. However, Nunez tells KangaNews the firm will explore public issuance again if spreads become more attractive.

Tim van Klaveren, Sydney-based managing director and head of fixed income portfolio management at UBS Asset Management, argues more traditional investors will return should some of the newer entrants on the buy side step back from senior RMBS tranches in favour of renewed bank senior-bond issuance.

“We have been active in the ABS and RMBS market in 2021 but we have only participated in one deal recently as current pricing looks too tight,” van Klaveren adds. “If the market were to step back a bit and spreads widened, we would step back in – especially for high-quality RMBS.”

Samson argues there is still strong appetite domestically even though some investors have recently stepped back from the market as spreads softened. “Looking at the last 10 years, spreads are still good compared with where they have been,” she explains. “If I told an issuer it could print a deal at 100 basis points over BBSW a few years ago, it would have been very, very happy. While it may not be as good as it was a couple of months ago, pricing is still at a healthy level.”

nonbank Yearbook 2023

KangaNews's eighth annual guide to the business and funding trends in Australia's nonbank financial-institution sector.

Related news