Predictors of default: Refinitiv’s StarMine models continue to perform

Refinitiv’s StarMine credit-risk models have been around since 2011 and the company says investors are increasingly turning to them as they grapple with risk management and alpha generation during the pandemic and now a rising interest-rate environment. The added challenges of the last two years led StarMine to review its models and performance, but its predictive powers have held during these turbulent years.

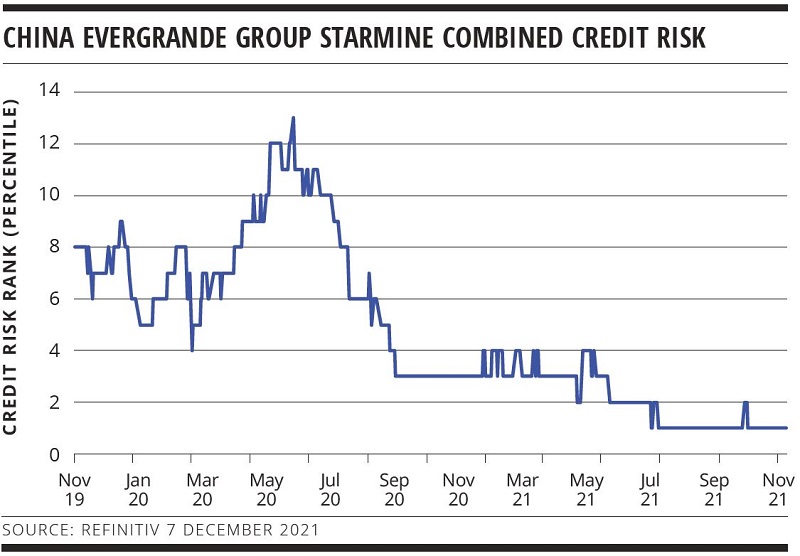

The Evergrande situation provides an example of the type of data analysis StarMine provides. StarMine’s credit-risk models tracked the default’s likelihood, with Evergrande’s combined credit-risk region rank peaking in July 2020 (see chart). Joe Rothermich, head of StarMine quantitative research at Refinitiv in San Francisco, says: “Before Evergrande’s problems became well known, we were able to see them evolve through the year. All four of our credit models adjusted proactively toward downgrading.”

StarMine’s credit-risk suite has three underlying models. The structural credit-risk model uses a proprietary extension of the Merton structural-default prediction framework to model a company’s equity as a call option on its assets. The SmartRatios credit-risk model uses financial-ratio analysis for credit-risk assessment. The text-mining credit-risk model takes data from sources such as news reports and corporate filings to evaluate potential financial distress.

A fourth model – the combined credit-risk model – adds the other three together to generate a single credit-risk estimate.

StarMine has published a white paper on the platform’s performance between 2019 and 2020. This suggests that from the end of February 2020 – the beginning of the COVID-19 market turmoil – StarMine users could have avoided more than 90 per cent of defaults in the following six months. Using the Altman Z-Score alone, fewer than 70 per cent of defaults would have been avoided according to the same paper.

Rothermich comments: “The data shows how well each model is predicting company defaults: 80-85 per cent of defaults were in the bottom 20 per cent of companies in our models. This is a powerful measure.”

He adds the paper also shows how fast the scores update and how rating agencies have moved toward StarMine’s predictions. “We found that our models are predictive of a rating-agency change,” Rothermich explains. “If there is a significant difference between scores, 81 per cent of the time when an agency updates its rating it moves toward our model. The rating agencies are 4.5-6 times more likely to move toward us than away.”

The ongoing evolution of fixed-income investment into systematic strategies means portfolio managers are increasingly aiming to trade around credit positions. This – combined with the pandemic and consequent economic uncertainty – has led to a spike in StarMine’s use.

Rothermich says: “We are known as a quantitative modelling group that sells to hedge funds and quantitative investors. But we share the details of what is going on within our models so our clients can understand them, and this transparent approach is also helpful for fundamental investors using our desktop version as it facilitates their research.”

The models are finding a range of uses among clients, some looking for alpha, others wanting to manage risk. “It has evolved from hedge funds seeking a little more alpha, or doing risk control, into a lot of different areas,” Rothermich continues. “Now we are starting to see interest from all over the market landscape, whether it is counterparty risk or companies looking at their overall supply chain, including the risk of a supplier defaulting. There is also an increasing number of regulations requiring companies to understand and report their exposures. It has moved from equity investors trying to avoid certain stocks to something greater.”