Covered bonds provide Australian majors path back to benchmark issuance

Rising geopolitical and inflation risks created turbulent market conditions in March, leading Australia’s big-four banks to push on with their funding tasks via covered-bond issuance. Three of the majors and one of their New Zealand subsidiaries issued covered bonds in recent weeks, targeting euro or sterling.

ANZ Banking Group and Westpac Banking Corporation printed €1.75 billion (US$1.9 billion) three-year and £700 million (US$922 million) four-year covered bonds on 8 March. National Australia Bank followed the day after with a four-year €1.5 billion deal. ANZ New Zealand was last to market, issuing a €750 million five-year covered bond on 14 March.

Lucy Carroll, Sydney-based director, global funding at Westpac, says market volatility driven by the Ukrainian conflict and central-bank signals on inflation made the covered-bond product a natural choice.

“When markets are volatile and windows difficult, use of covered bonds as a defensive product can be quite effective,” she says. “They have been quite resilient throughout this period of volatility in terms of what issuers have been able to achieve in primary markets and the spread moves we have seen in secondary markets globally. It felt like the right trade and right product to do.”

Issuers may continue to lean on covered bonds as an effective defensive product given the ongoing instability. “Making the right funding decisions ensures we stay ahead when things become increasingly volatile like this and ensures we are not forced into markets at any point,” Carroll tells KangaNews.

The covered-bond deal was particularly significant for ANZ as – unlike the other major banks – it has not completed any benchmark wholesale issuance since the end of the Reserve Bank of Australia’s term-funding facility (TFF) in June 2021 and has not issued an unsubordinated benchmark since January 2020.

The timing of its latest transaction was “a question of monitoring customer balance sheet dynamics and our funding position”, says Simon Reid, director, group funding at ANZ in Melbourne. “We have had a very different balance sheet position to some of our peers," says Reid, pointing to its smaller committed-liquidity facility, which it proactively reduced.

“We are also probably a little less focused on TFF refinancing, as we have a smaller TFF than some of our peers.” ANZ has also enjoyed strong deposit growth and a stable asset book, Reid continues.

DEAL DYNAMICS

ANZ’s March 2025 covered-bond transaction priced at 7 basis points over mid-swap after launching in the 12 basis points area, while NAB’s March 2027 transaction priced at 12 basis points over mid-swap. Previously, Commonwealth Bank of Australia (CBA) executed a February 2028 euro covered bond on 16 February that priced at 10 basis points over mid-swap.

Westpac’s four-year floating-rate note priced at 45 basis points over SONIA – in line with guidance. NAB priced a £1.5 billion December 2025 covered bond in December with a margin of 27 basis points over SONIA.

“Pricing was broadly in line with expectations but we were positively surprised with the size of demand,” says Reid. “We value the euro covered-bond market because it offers reliable access to term funding in difficult market conditions and it is clear the covered-bond market has grown since the last time we issued into that market.”

He adds ANZ was able to access a larger volume of funding than it expected at the price it was looking to achieve.

Westpac’s deal represents the bank’s first issuance in sterling since January 2018. Having issued covered bonds in the euro and US dollar markets in the past six months, Carroll says the opportunity provided by the sterling market suited the bank’s needs and allowed it to issue into a diversified pool of demand.

“It definitely felt like there was some capacity in the market,” she explains. “It was a good funding opportunity from a relative-value basis versus covered options in euros and US dollars, as well as offering the volume we were targeting.”

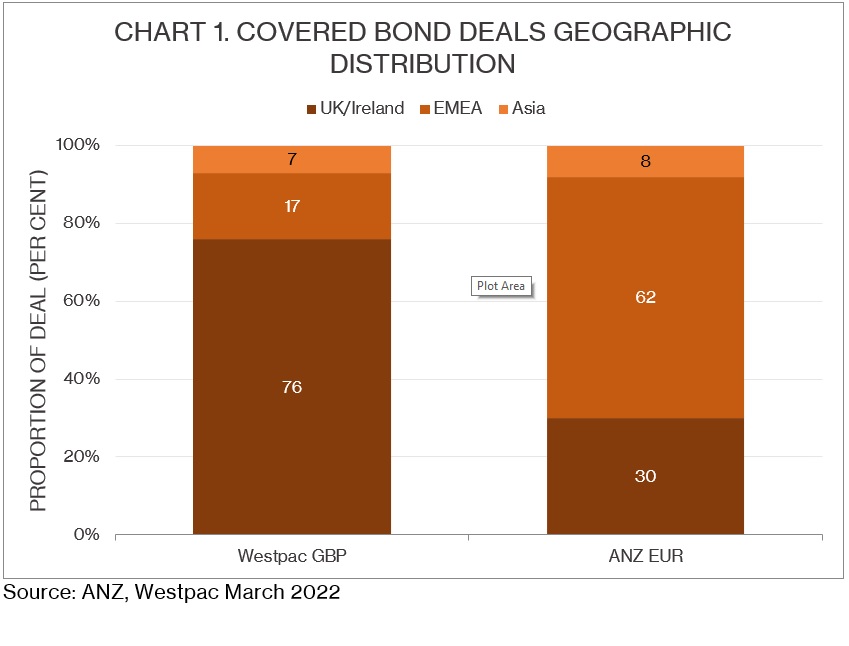

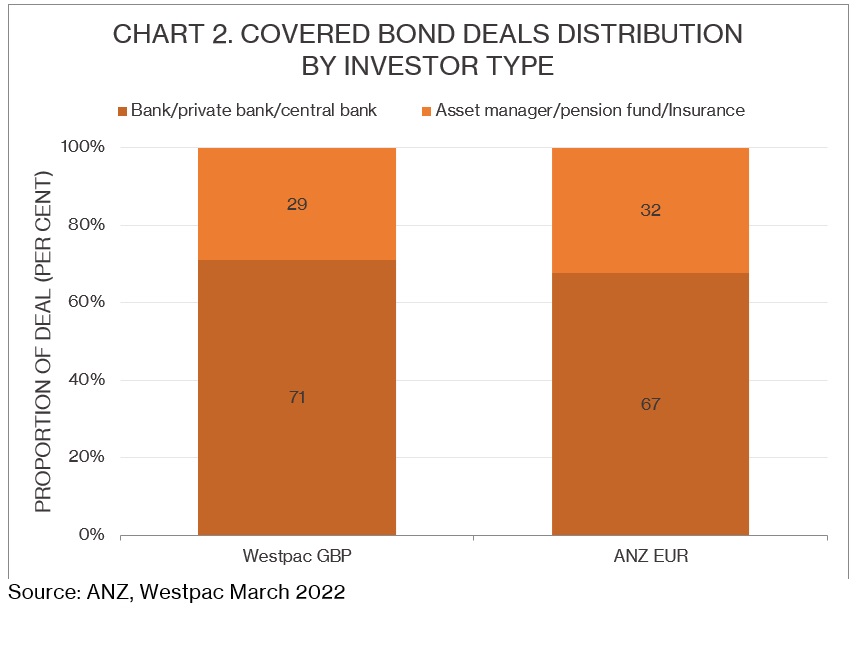

Bank books took most of the transactions, while investors from Ireland and the UK dominated the Westpac sterling deal (see charts 1 and 2).

COVERED CAPACITY

The banks do not expect to be exclusively reliant on covered bonds for their wholesale issuance despite challenging market conditions. For instance, Westpac returned to the domestic senior-unsecured market on 10 March with a A$2.5 billion (US$1.8 billion) three-year print. Nonetheless, they have ample covered-bond issuance capacity.

According to Guy Volpicella, managing director and head of structured funding and capital at Westpac in Sydney, the bank has about 47 per cent of its covered-bond capacity – capped at 8 per cent of total assets in Australia – on issue.

“Westpac’s percentage usage against the overall 8 per cent cap has remained reasonably steady over time, having generally ranged between 45 per cent and 55 per cent,” Volpicella says.

The bank expects to return to its pre-COVID-19 mix of debt products, which includes roughly a quarter of funding completed in covered-bond format. “We have a good degree of capacity across secured and unsecured product, as well as across markets, so we feel we have a range of funding options available,” Carroll says.

WOMEN IN CAPITAL MARKETS Yearbook 2023

KangaNews's annual yearbook amplifying female voices in the Australian capital market.

Related news