Westpac’s domestic print resets pricing but uncovers robust underlying demand

Westpac Banking Corporation reopened the Australian dollar credit market on 10 March, offering a significant pricing concession to secondary marks. The execution reflected the reality of a volatile environment but it also received substantial support from local real money in particular.

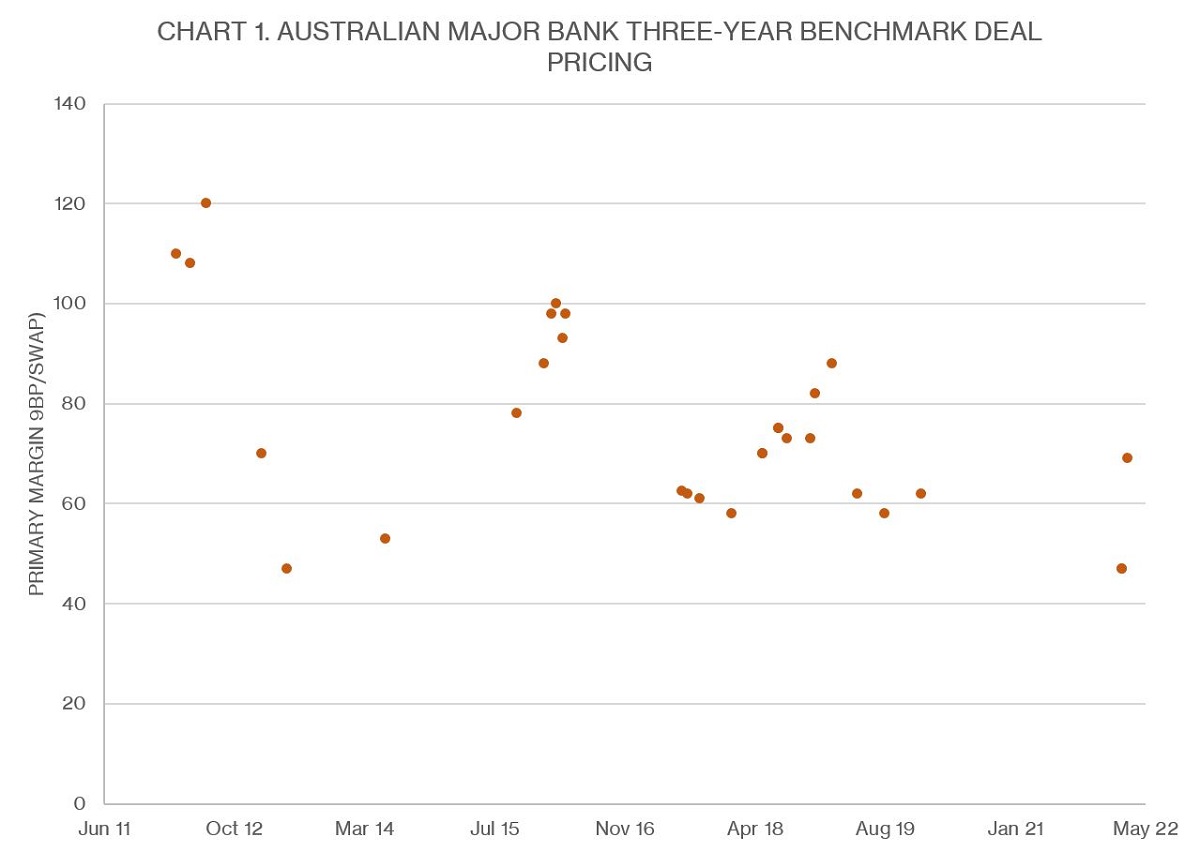

Westpac’s A$2.5 billion (US$1.8 billion), three-year transaction priced at 69 basis points over swap, 22 basis points wider than National Australian Bank’s A$850 million tranche issued in February – the most recent previous big-four bank three-year senior deal in Australian dollars. Market users say Westpac’s level reset the secondary market 6-10 basis points wider following minimal trading volume in recent weeks.

Alex Bischoff, managing director, balance sheet, liquidity and funding at Westpac in Sydney, says the premium was the right balance given market risk and allowed the issuer to find very strong underlying demand at the new level. The deal book closed at around A$3.9 billion, allowing scaling of bids.

The deal outcome was also sufficient to persuade other issuers to return to the primary market in the following days. Bendigo and Adelaide Bank issued A$750 million of three-year notes on 11 March – at 98 basis points over swap – and on 15 March Svenska Handelsbanken printed a A$500 million senior-preferred Kangaroo transaction with a margin of 85 basis points over swap on the three-year tranche.

Westpac’s final margin does not represent a cost of funds out of line with the historical three-year major bank issuance range and remains attractive to the issuer, Bischoff says.

KangaNews data confirm that pricing is in line with a margin that would have been typical prior to the start of the COVID-19 pandemic. The average margin for major-bank three-year domestic benchmarks over the past decade is 75 basis points over swap, making Westpac’s latest print if anything slightly tighter than the long-run norm (see chart 1).

Source: KangaNews 16 March 2022

“The size and diversity of the book supported our view that we had the right clearing price,” Bischoff tells KangaNews. “We launched the deal after a more positive overnight session allowing demand to drive the final landing point.”

Westpac issued a covered bond in the sterling market just two days before the domestic print and Bischoff says the bank had also been contemplating the Australian dollar market when it executed in the UK. “The advice we were receiving from our institutional bank suggested there was strong liquidity in the domestic market, with three years being the right tenor for a volatile environment,” he reveals.

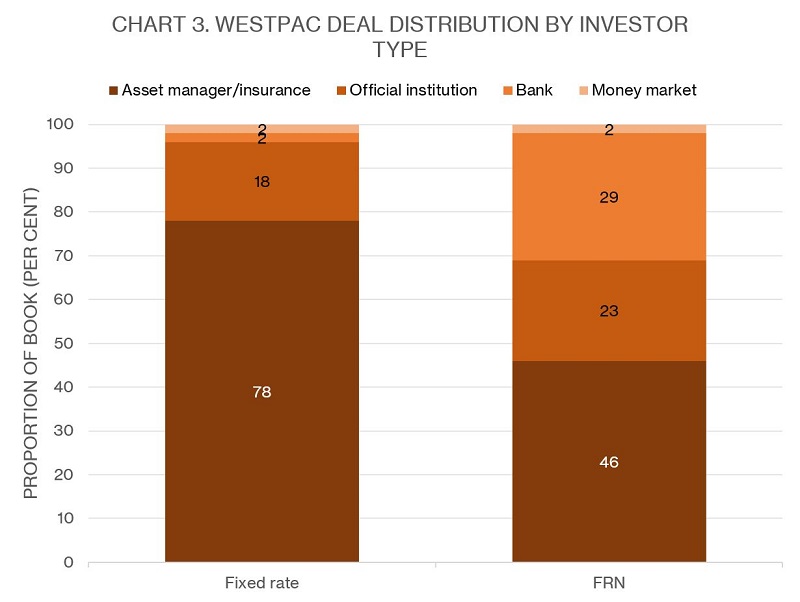

The final book skewed heavily domestic in both the deal’s fixed- and floating-rate tranches (see chart 2). The real-money bid was notably strong, especially in the fixed-rate note (see chart 3).

Source: Westpac Banking Corporation 15 March 2022

Source: Westpac Banking Corporation 15 March 2022

Westpac has been notably active in wholesale funding markets, at home and offshore, though it has consistently emphasised that it views its activity as a return to a historical funding range. The bank has now completed about A$21 billion of a financial-year wholesale funding plan that it has revised to A$30-35 billion from an original expectation of closer to A$40 billion.

Bischoff says: “We are ahead of the run rate but we feel comfortable being in that position. We have taken a relatively proactive approach to funding, stretching back to May 2021 when we returned to the US dollar market well before we needed the liquidity.”

As a result, Westpac will continue to monitor funding markets when opportunities arise. Bischoff notes in this context that the bank has ample capacity to issue covered bonds and securitisation as defensive funding options if suitable.

Related news